Recent market sentiment has hit rock bottom. The bull-bear debate over ETH is a "separation of ways" of symbolic significance: David Hoffman, co-founder of Bankless, publicly disclosed that he has sold all his ETH.

Conversely, institutions on the other side of the market are buying on the dip. Tom Lee's BitMine has been consistently buying ETH recently and elevated ETH to a core company strategy.

On one side, a long-term evangelist sells all ETH; on the other, public companies and institutional funds continue to buy more ETH. Is ETH losing its value capture ability, or is it facing a new round of institutional revaluation? Biteye has compiled the bull and bear views for everyone👇

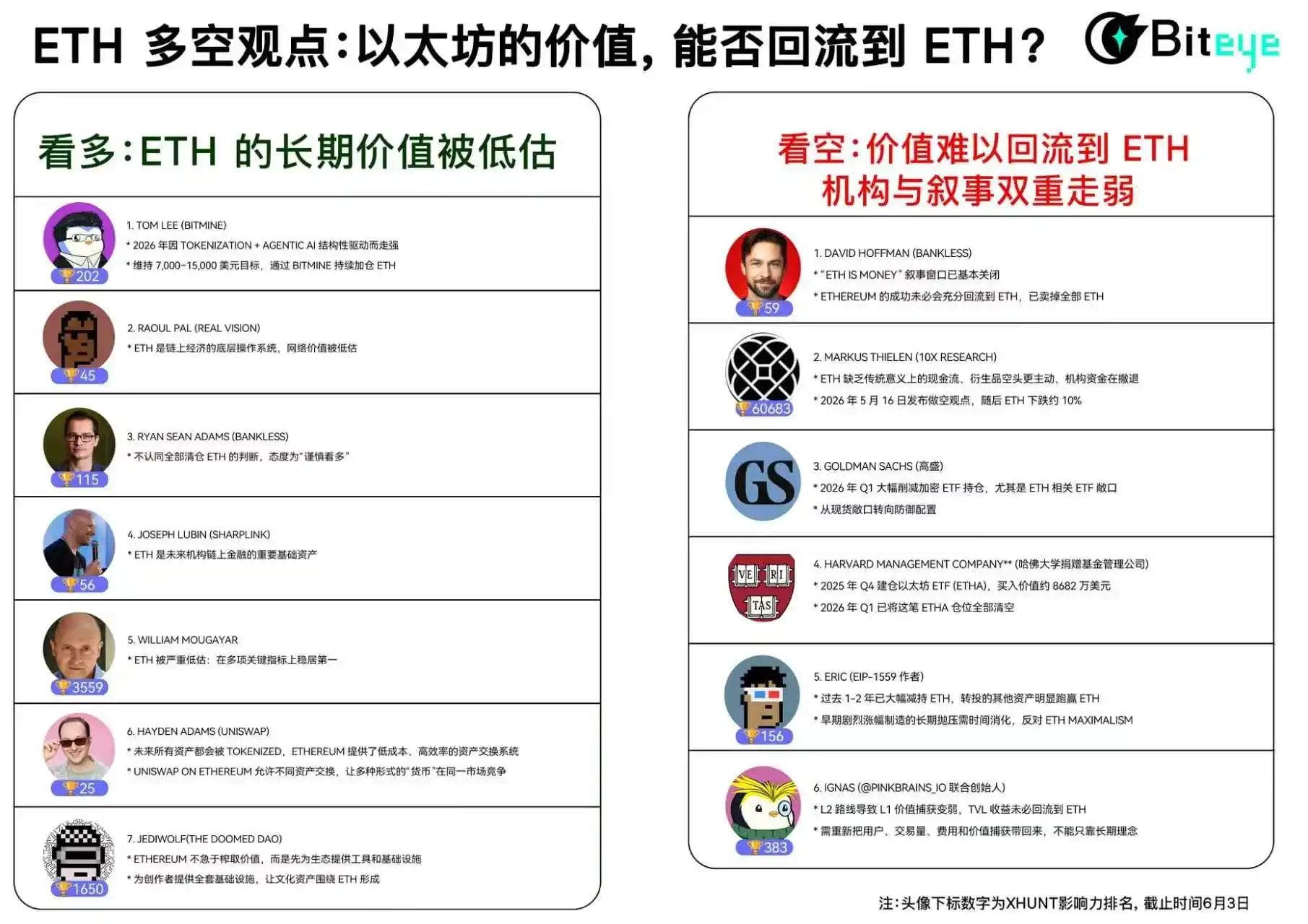

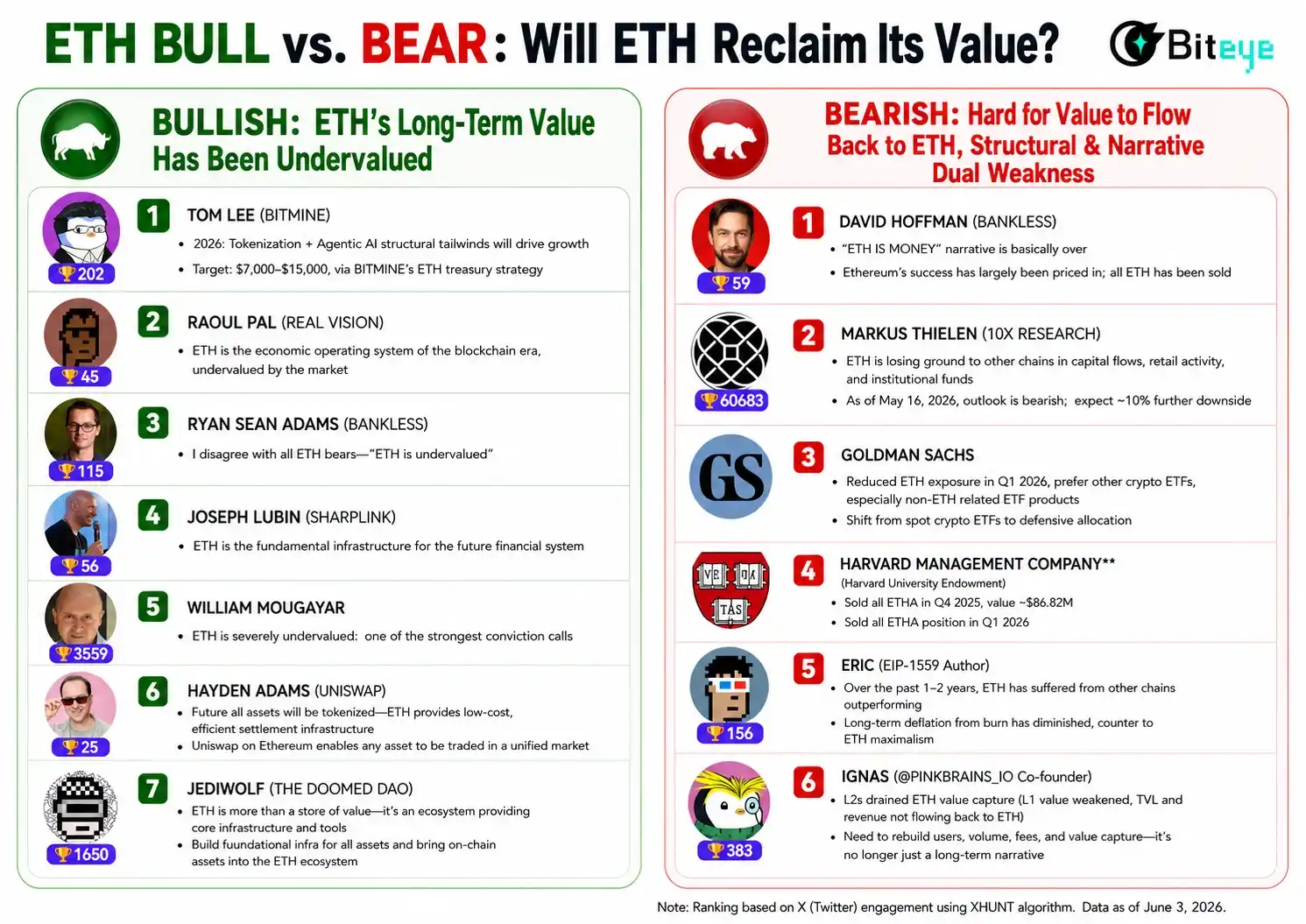

🌟 Bullish

The bullish side does not deny ETH's weak short-term performance and acknowledges the market is re-evaluating ETH's value capture problem.

But they believe ETH's core logic remains intact.

Whether it's stablecoins, RWA, DeFi, L2, institutional tokenization, or Agentic AI, many new financial activities still need a secure, neutral, and composable underlying network. And Ethereum remains the most important candidate.

Therefore, the bulls are betting not on a short-term fee rebound, but that ETH will be reintegrated into the pricing framework of institutions and long-term capital as on-chain finance continues to expand.

1️⃣ Tom Lee@fundstrat | BitMine CEO | XHunt Rank: 202

Core view: Short-term decline is noise; ETH will strengthen structurally in 2026 driven by tokenization + Agentic AI. He maintains a $7,000-$15,000 target for end of 2025, stating "ETH thesis not broken".

More importantly, Tom Lee is not just talking; he is buying ETH through BitMine.

BitMine's latest purchase on June 2 was about 26,497 ETH, worth approximately $52 million; in the last week of May, BitMine had already accumulated purchases of 111,942 ETH, about $237 million, one of the largest single-week buys since 2026.

BitMine aims to hold 5% of ETH's circulating supply and is nearing this goal.

2️⃣ Raoul Pal @RaoulGMI | Real Vision CEO | XHunt Rank: 45

Core view: ETH is one of the underlying operating systems of the on-chain economy. Raoul Pal's logic is not short-term price, but network value: If Ethereum were shut down today, a vast amount of economic activity from Layer2, DeFi, NFTs, RWA, etc., would be severely impacted, suggesting ETH's current valuation might still be undervalued.

3️⃣ Ryan Sean Adams @RyanSAdams | Bankless Co-founder | XHunt Rank: 115

Core view: Does not agree with David Hoffman's judgment to sell all ETH. Ryan is more like "cautiously bullish": he admits ETH's window has narrowed, but does not believe ETH's long-term potential is over.

After David Hoffman sold all ETH, Ryan Sean Adams called it "the end of an era" for Bankless, but he himself still disclosed holding ETH and continues to support the narrative of Ethereum as an institutional asset and underlying asset for the on-chain economy.

4️⃣ Joseph Lubin@ethereumJoseph | Ethereum Co-founder/SharpLink CEO | XHunt Rank: 56

Core view: ETH is not just a crypto asset, but a key foundational asset for future institutional on-chain finance.

Joseph Lubin repeatedly retweeted and supplemented an article by SharpLink CEO Joseph Chalom in late May, clearly expressing his long-term judgment on Ethereum.

In his view, stablecoins, RWA, DeFi, smart contract treasuries, and Agentic AI financial systems are collectively driving a restructuring of global financial infrastructure. And Ethereum is one of the most important underlying networks for these assets and applications.

On May 29, Lubin stated: Consensys' institutional team is bringing Ethereum into the world's major financial market infrastructures and large financial institutions, emphasizing: "TradFi keeps choosing Ethereum."

SharpLink's Q1 2026 financial report shows that as of May 4, 2026, SharpLink holds 872,984 ETH.

5️⃣ William Mougayar @wmougayar | Author of The Business Blockchain | XHunt Rank: 3559

Core view: ETH is severely undervalued.

Whether it's stablecoins, DeFi TVL, tokenized assets, settlement volume, or transaction volume, Ethereum ranks first in all key metrics, with market shares of 21%-64%, but ETH's market cap only accounts for about 10% of the entire crypto market, which is completely unreasonable.

"Ethereum is infrastructure, just like the internet; value naturally accumulates at the base layer, not just by looking at App-layer revenue or fees."

6️⃣ Hayden Adams @haydenzadams | Uniswap Founder | XHunt Rank: 25

Core view: After David sold ETH, it should be even more acknowledged that the thesis "ETH is money" is correct, just that the way it holds true might be different from what many imagine.

Hayden believes all assets will be tokenized in the future, and people will hold the assets they value most, not just treat one asset as the sole unit of account.

In such an environment, what truly matters is not who becomes the sole currency, but who can provide a low-cost, high-efficiency, 24/7 asset exchange system.

From this perspective, Uniswap on Ethereum itself is a decentralized monetary system: it allows different assets to be exchanged at any time, enabling multiple forms of "money" to compete in the same open market.

7️⃣ Jediwolf@Jediwolf | Member of The Doomed DAO | XHunt Rank: 1650

Core view: David Hoffman's statement "Ethereum is a Giver, not a Taker" is accurate, but the conclusion might be the opposite.

Jediwolf believes the crypto market is too accustomed to understanding a chain through 'value extraction': high fees, high take rates, value capture. But Ethereum's most unique aspect is precisely that it is not in a hurry to extract value from users, but first provides the ecosystem with tools, trust, and infrastructure.

Take on-chain art as an example: Ethereum provides artists and collectors with almost a full suite of infrastructure: issuance, provenance, settlement, custody, identity, global liquidity, and composability. It may not directly cause ETH to appreciate immediately, but it will lead more artists to price in ETH, collectors to think in ETH, and cultural assets to form around ETH.

🌟 Bearish

Besides price, personnel changes within the Ethereum community since 2026 have also become important context for market discussions about ETH.

Since early 2026, several senior researchers, protocol leaders, and management members have left the Ethereum Foundation. In May alone, several core members announced their departures successively.

Due to the high concentration in timing, this wave of departures has been called the "Spring 2026 Reshuffle" by some community members and media.

Against this backdrop, some investors have begun to re-evaluate ETH's long-term value capture ability, while others believe this is merely necessary adjustment before Ethereum enters a new phase.

1️⃣ David Hoffman @TrustlessState | Bankless Co-founder | XHunt Rank: 59

Core view: The "ETH is Money" narrative window has essentially closed. Ethereum as a network is still successful, providing secure block space and open infrastructure for L2, DeFi, stablecoins, RWA, and applications, but this success may not fully flow back to the ETH token itself. In other words, Ethereum may continue to grow, but ETH may not be the primary beneficiary asset.

Therefore, David sold all his ETH, reallocating capital to other places in the market with better opportunities.

2️⃣ Markus Thielen@markus10x | 10x Research Founder | XHunt Rank: 60383

Core view: 10x Research published a high-conviction short ETH view on May 16, 2026. ETH is not just weak in price; its fundamental narrative and institutional capital flows are also weakening. Its core logic can be summarized in three points:

-

ETH lacks traditional cash flow.

-

Derivatives markets show bears are more active.

-

Institutional capital is also retreating.

Markus Thielen later stated that since the publication of this short view, ETH has fallen about 10%, and their bearish thesis was actually formed as early as October 31, 2025.

3️⃣ Goldman Sachs - Shifting from Spot Exposure to Defensive Allocation

Core view: Goldman Sachs has not publicly issued strongly bearish statements on ETH, but judging from the Q1 2026 13F holding changes, it significantly reduced its spot ETF exposure to Ethereum.

13F filings show Goldman Sachs sharply cut holdings in some crypto ETFs in Q1, especially being more cautious with ETH-related ETF allocations.

4️⃣ Harvard Management Company (Harvard University Endowment Management Company)

Core view: Harvard has not publicly expressed bearish views on ETH, but it expressed retreat with its actual positions.

Harvard Management Company established a new position in BlackRock's spot Ethereum ETF ETHA in Q4 2025, buying about 3.8709 million shares worth approximately $86.82 million.

But by Q1 2026, Harvard had completely cleared this ETHA position. That means this Ethereum ETF exposure was held for only one quarter.

5️⃣ eric@econoar | EIP-1559 Author | XHunt Rank: 156

Core view: Can't blame David for selling all ETH, because ETH has indeed significantly underperformed the entire crypto market for many consecutive years.

eric stated he agrees with many of David's points and has also significantly reduced his ETH holdings over the past 1–2 years. The other assets he switched to have clearly outperformed ETH.

However, he does not believe ETH's underperformance is necessarily due to a fundamental error with Ethereum itself. Instead, he thinks a easily overlooked reason is: ETH's early gains were too sharp, creating a large number of early wealthy holders in a very short time, and this long-term selling pressure takes a long time for the market to fully digest.

So, eric's stance is not to completely negate Ethereum, but to oppose ETH maximalism from a portfolio management perspective.

The market doesn't lie; there's no need to fight it. If ETH becomes hot again, it can be bought back anytime.

6️⃣ Ignas@DefiIgnas | Co-founder of @PinkBrains_io | XHunt Rank: 383

Core view: ETH has shifted from consensus hold to contrarian bet.

Ignas believes ETH's weakness over the past 2–3 years partly stems from market style changes, and partly from Ethereum's own issues: the L2 roadmap weakens L1 value capture, L1 scaling progresses relatively slowly, user experience hasn't improved significantly long-term, and the fee and revenue narratives have also weakened.

He acknowledges Ethereum still has long-term moats like decentralization, censorship resistance, and cypherpunk ideals, but the market cares more about revenue, trading volume, and valuation multiples in the short term.

This is also ETH's current problem: Ethereum still dominates DeFi TVL, but much of TVL's yield flows to protocols, stablecoin issuers, and L2s, not necessarily back to ETH.

Meanwhile, the former "ultrasound money" narrative has also weakened. Lower fees benefit users, but if transaction volume cannot scale up simultaneously, ETH's burn and deflation logic becomes hard to reestablish.

Therefore, Ignas's view is: For ETH to regain market confidence, it cannot rely solely on long-term ideals; it needs to bring back users, trading volume, fees, and value capture.

🌟 Conclusion

The most interesting aspect of this debate is that ETH is no longer just a faith asset within the crypto circle.

In the past, ETH's narrative focused more on technical upgrades, ecosystem prosperity, and the developer network. As long as Ethereum was being used, the market defaulted to ETH benefiting.

But now, this default premise is being re-examined. The market will continue to ask: Where's the revenue? Where's the cash flow? Why should capital buy ETH instead of BTC? Why should institutions hold long-term instead of trade short-term? How much of the ecosystem growth will actually translate to ETH?

This is also where ETH is most awkward and critical right now. What ETH truly needs to prove next is not just that Ethereum will continue to exist, nor that its ecosystem will continue to thrive.

But that when more assets, more users, and more institutions enter this network, ETH can truly transform from "the underlying facility being used" into "the core asset being continuously bought and held."

This is the core question behind this round of bull-bear controversy.