Author: Deep Tide TechFlow

Original Title: 2025 Crypto Industry Workplace Survey: 70% Earn Less Than $4,000 Monthly, N+1 Severance Becomes a Distant Hope

While Xiaohongshu still glorifies the "get-rich-quick myths" and "six-figure salaries" of Web3, what is the true state of the crypto industry?

Through 506 survey questionnaires, we engaged in a candid conversation with practitioners, and the results were surprising, even harsh: there is no gold rush here. Over 70% of people earn less than $4,000 per month, which is generally lower than in developed regions like Europe and the United States. Even a quarter of respondents are in a "pay-to-work" loss-making state; there is also no comprehensive protection, with nearly half having experienced layoffs, and most not receiving N+1 compensation.

Yet, despite this, over 80% choose to stay. Is it because of the 70% remote work freedom? Or is it because of the shared dream of "retiring with $5 million"?

In this report, we attempt to use cold, hard data to reveal the most genuine anxieties, desires, and survival strategies of Web3 workers.

This content is the questionnaire results section of the "Web3 Recruitment and Job Hunting 2025 Year-End Review: Who's Making Money, Who's Paying to Work?" Full report available at:

https://www.techflowpost.com/article/detail_29702.html

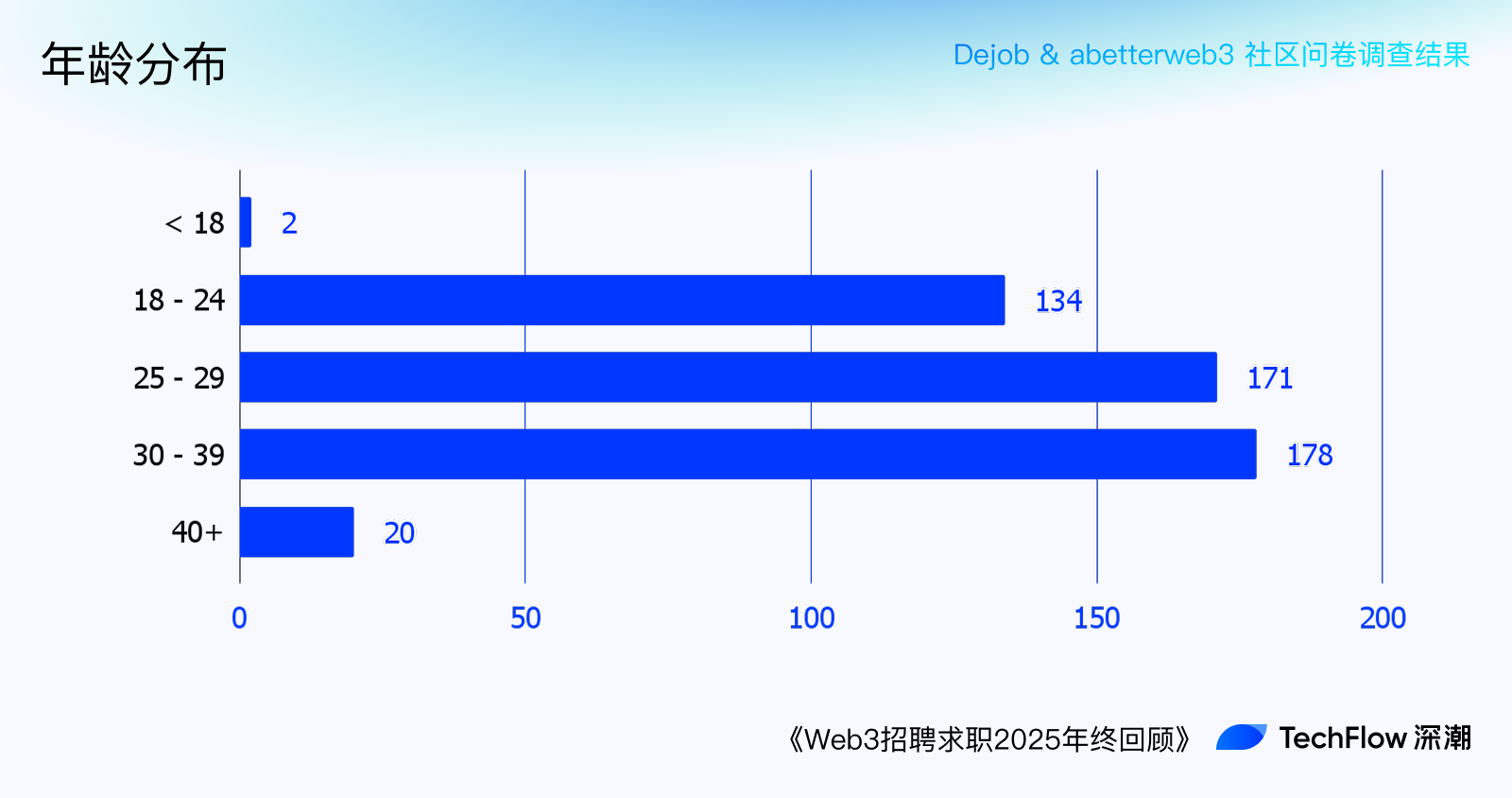

Regarding age distribution, the main workforce aged 18-29 is indeed the majority, but middle-aged practitioners (>30 years old) are also quite numerous. This might be related to the less severe "age 35 ceiling" in the Web3 industry. Compared to internet companies, Web3 companies value experience, ability, and efficiency more, with many hoping that seasoned professionals can quickly build products "plug-and-play".

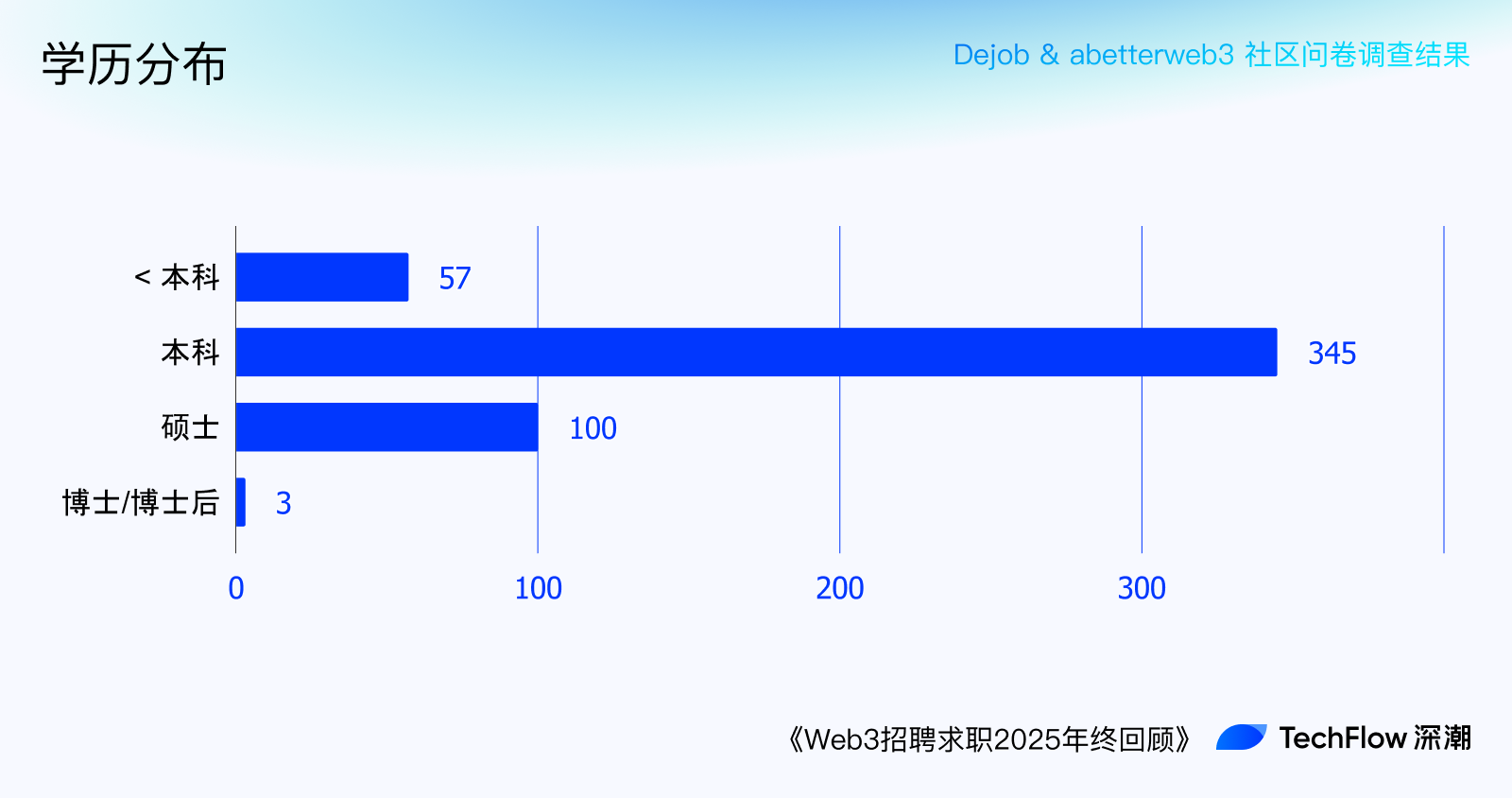

The distribution of educational background is largely consistent with the earlier talent data statistics, predominantly undergraduate degrees, with some having less than a bachelor's and others holding master's or doctoral degrees, though the proportion of postgraduates is not high.

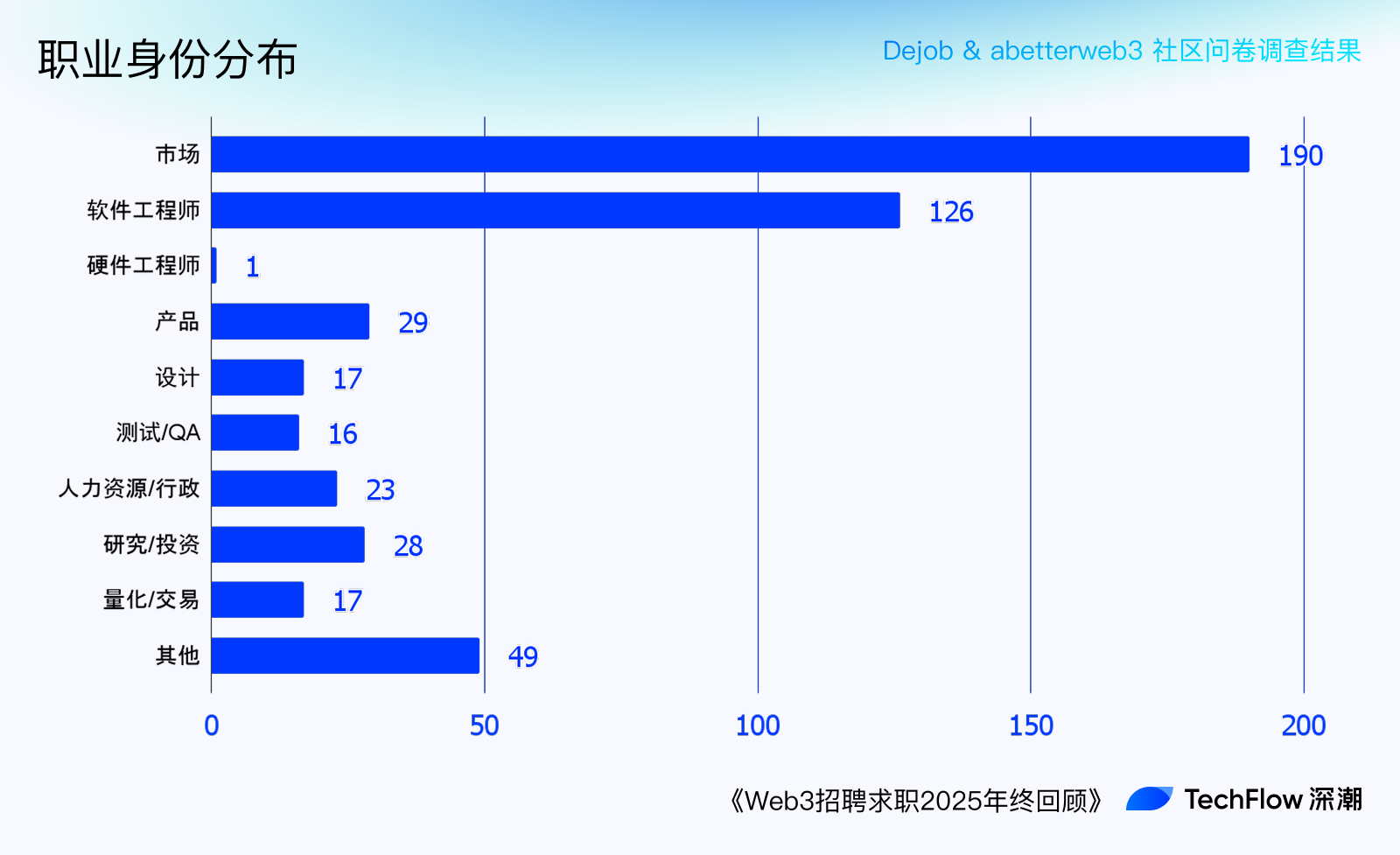

In terms of professional roles, the largest group is in market-related roles (operations/BD/customer service, etc.), followed by developers (front-end/back-end/smart contracts/blockchain, etc.). Then come product, human resources, investment research, design, trading, etc. Among the "other" submissions, common roles included risk control & security, KOLs, etc.

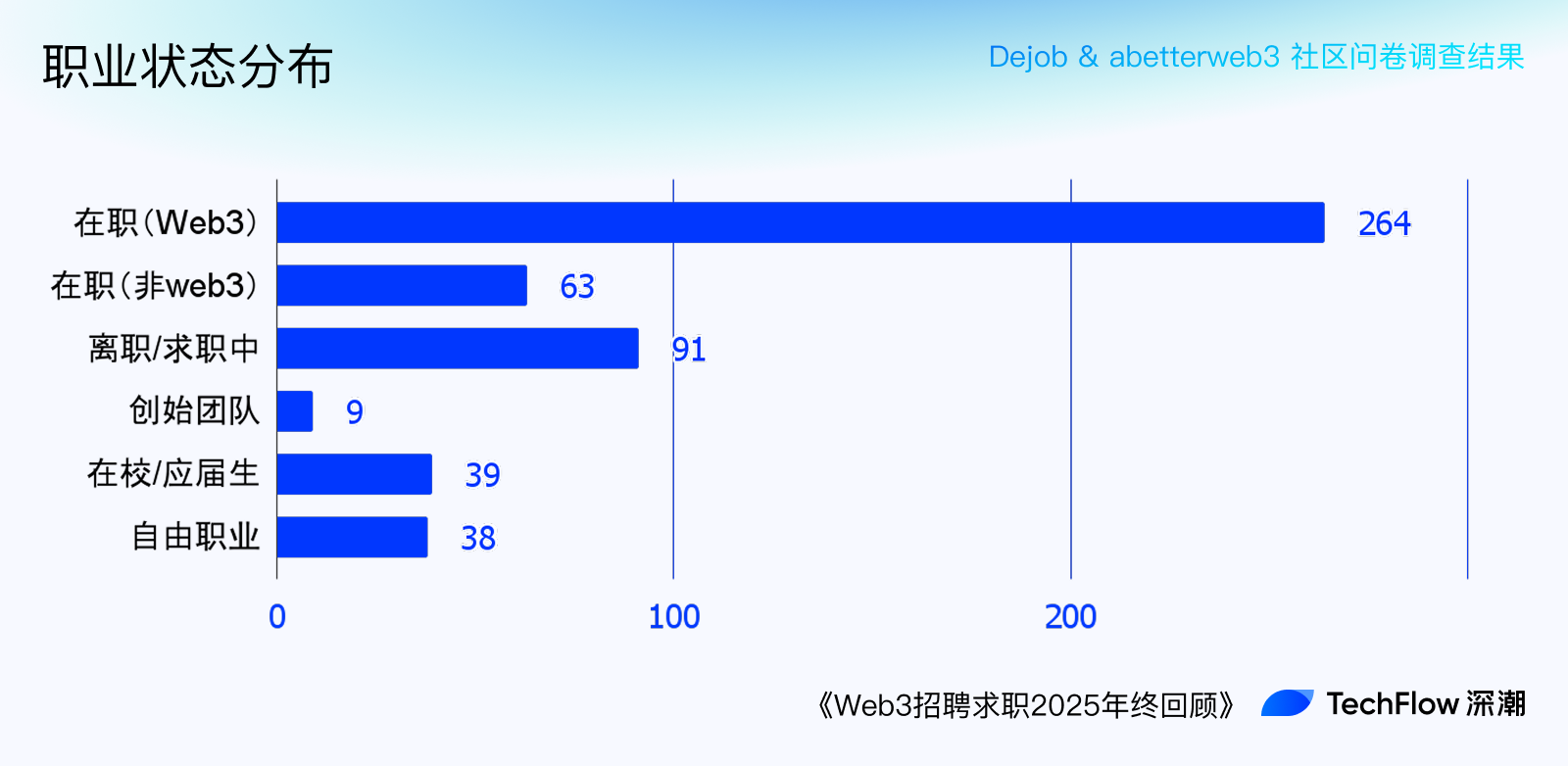

Regarding employment/attrition status, only 52% of respondents are currently employed in Web3. Over 30% are in a more flexible life situation. This indicates, on one hand, that market conditions affecting company headcount have impacted many; on the other hand, it might be because certain unique Web3 business models have made some people less reliant on traditional employment for cash flow, such as KOLs and traders.

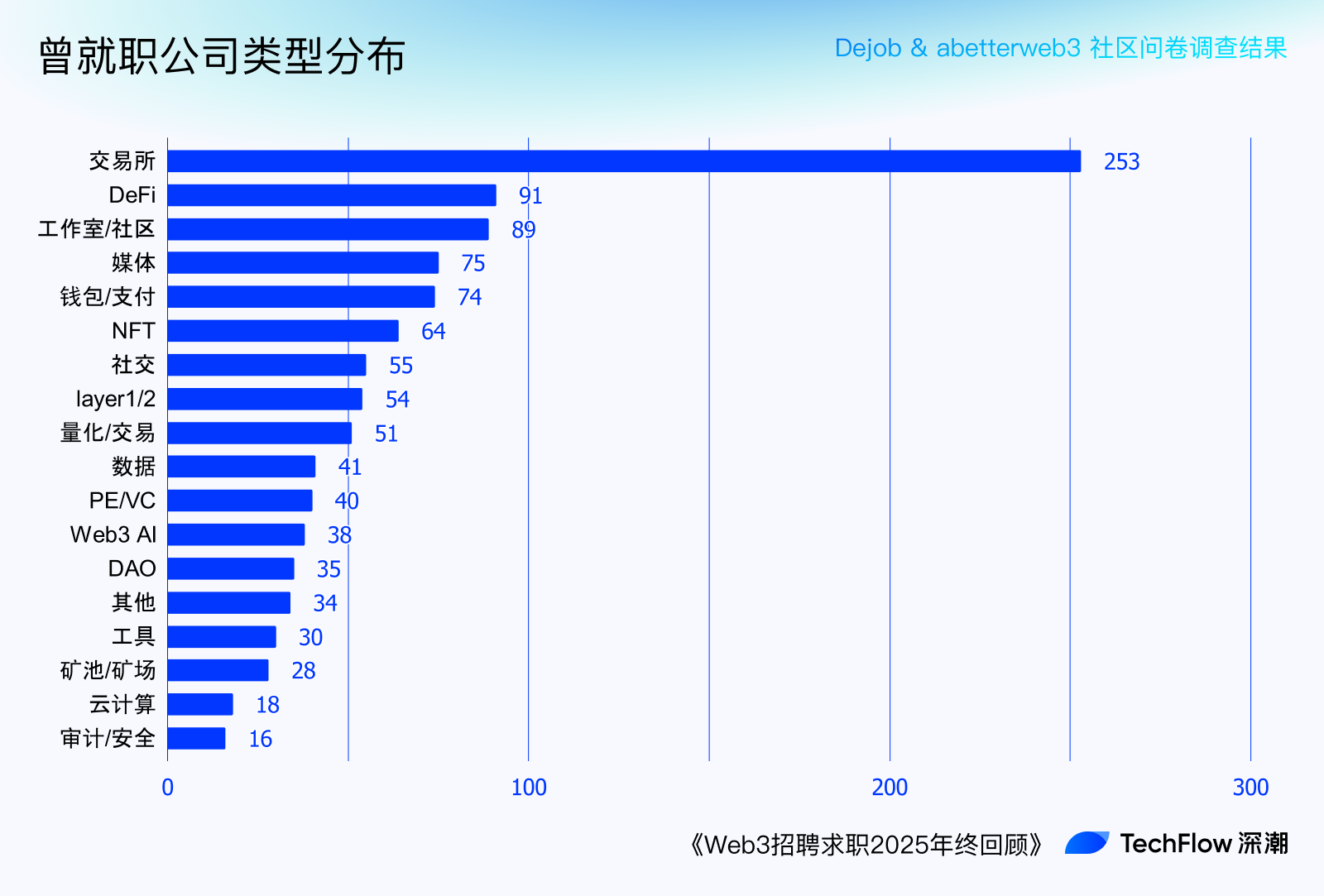

Over half of the submissions indicated having worked at exchanges, followed by studios/communities, DeFi, media, wallets, and other common business types. Both talent and job providers are heavily concentrated in exchanges due to the Matthew Effect. This also reflects, to some extent, the current industry dilemma: apart from exchanges, the revenue-generating capabilities of other business models mostly decrease from C-end — tools — underlying layers.

Regarding remote collaboration tools, as this survey took place in a Chinese-language vertical Web3 recruitment community, Telegram is favored by most companies for its confidentiality and usability, followed by mainstream Chinese tools like Feishu and WeChat, and finally tools commonly used by foreign companies like Google Suite, Discord, Slack, etc.

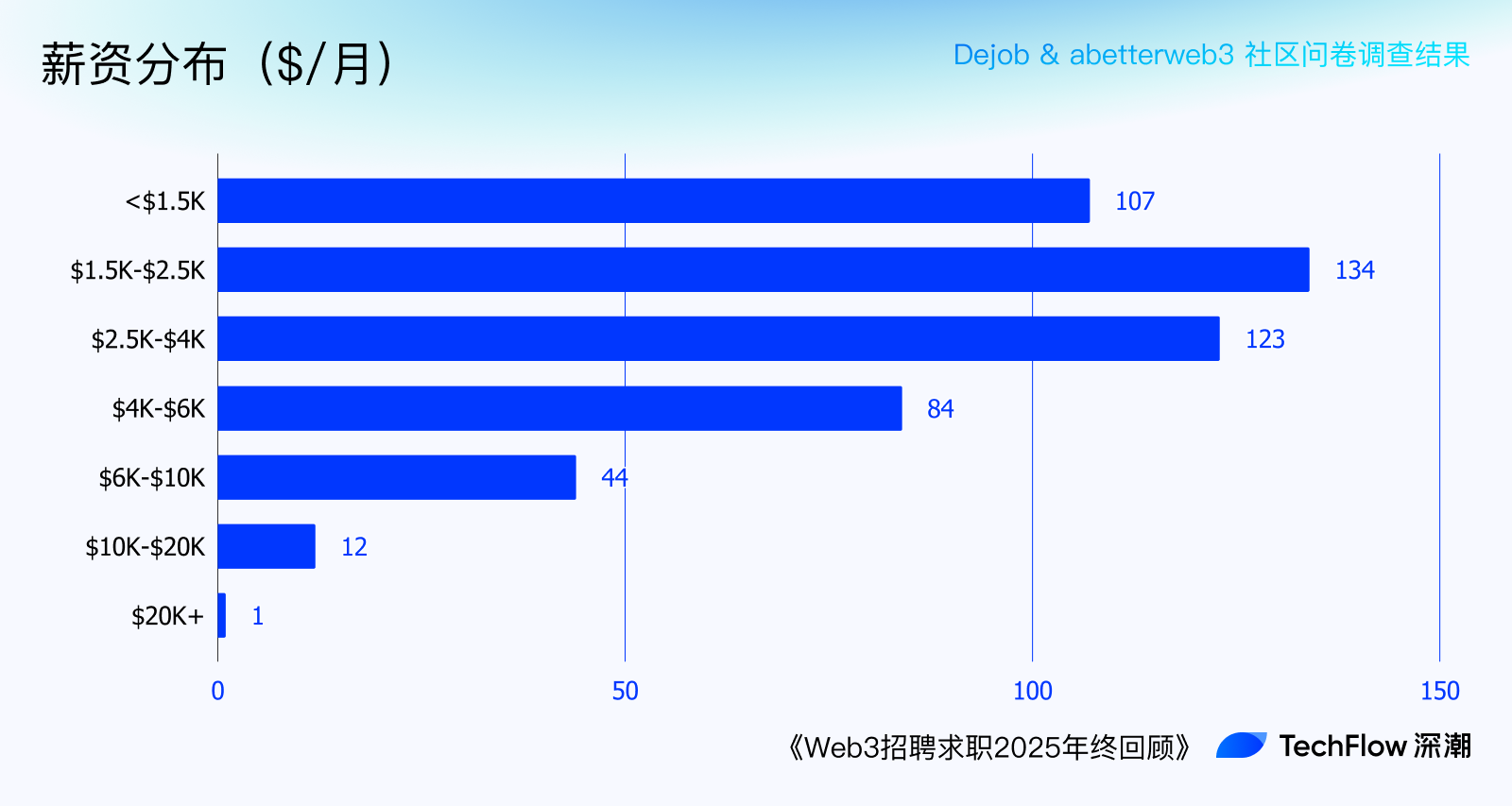

In terms of income levels, contrary to the external myths of immense wealth, most Web3 workers' incomes are not only lower than those in many top internet companies but also severely lacking in long-term incentives (tokens/equity), year-end bonuses, and layoff compensation.

Over 70% of people have a monthly salary income of less than $4,000 (approximately RMB 28,000), and the frequently mentioned monthly salary of $10,000 on Xiaohongshu is a rarity.

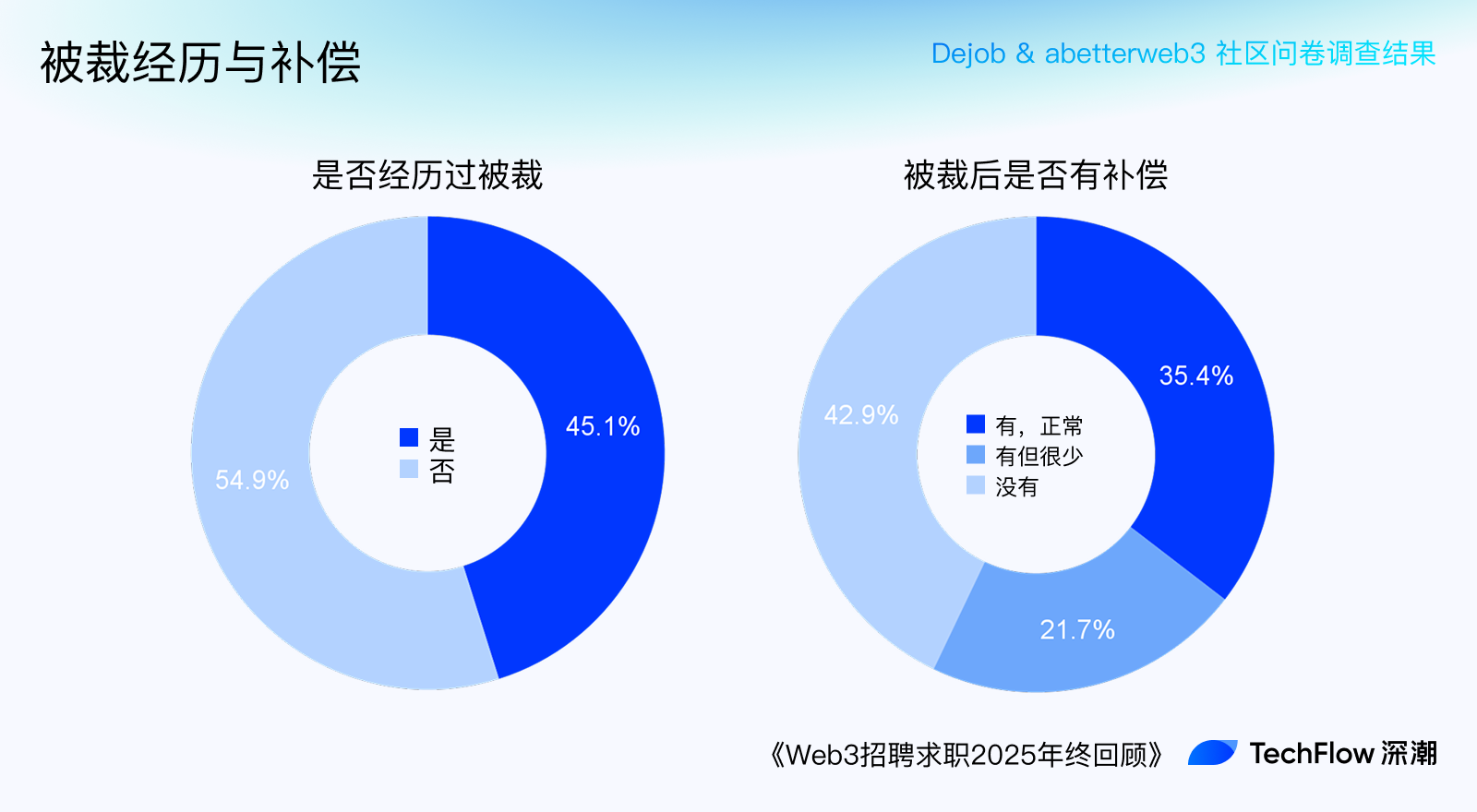

Close to half of the people have experienced layoffs, and 40% of those laid off reported no compensation, while 21% said that even if there was compensation, it fell far short of legal standards (e.g., n+1).

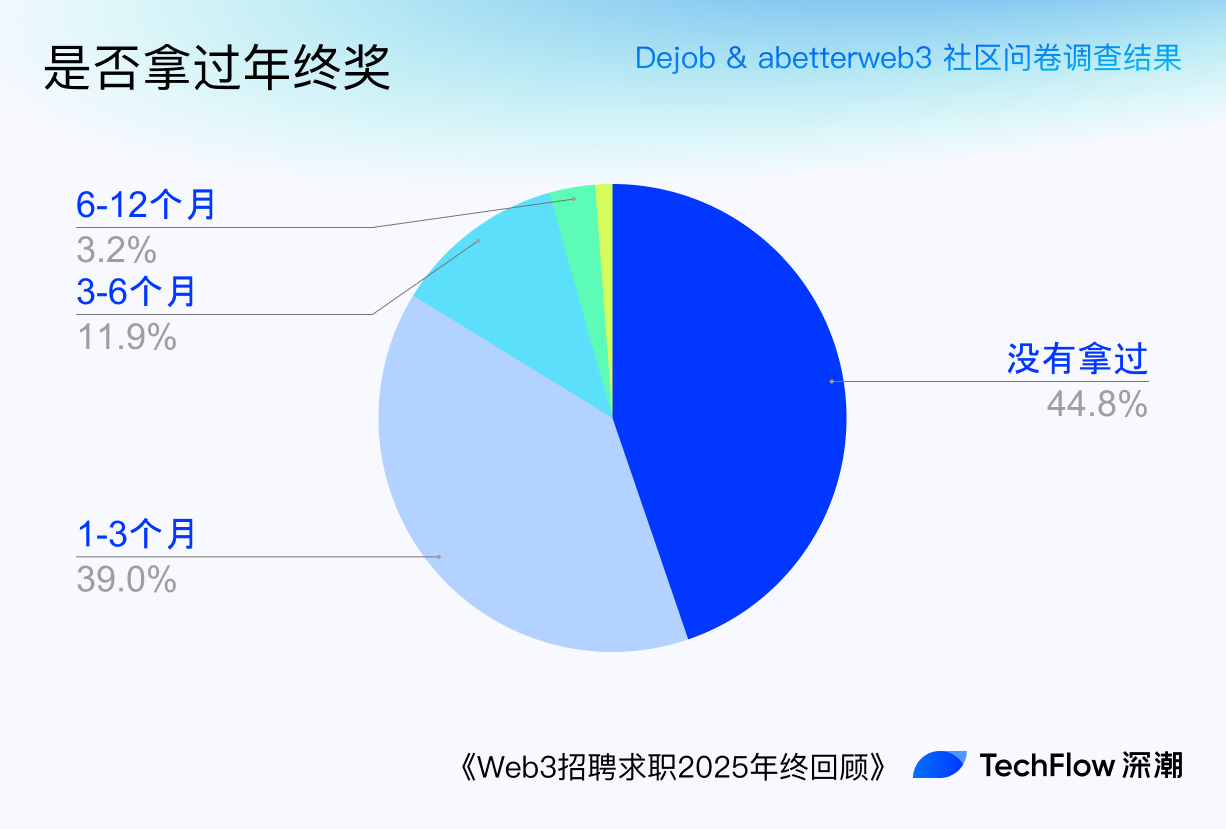

Nearly half reported not having received a year-end bonus; even among those who did, it was generally 1-3 months' salary, on par with most internet companies outside the Web3 industry.

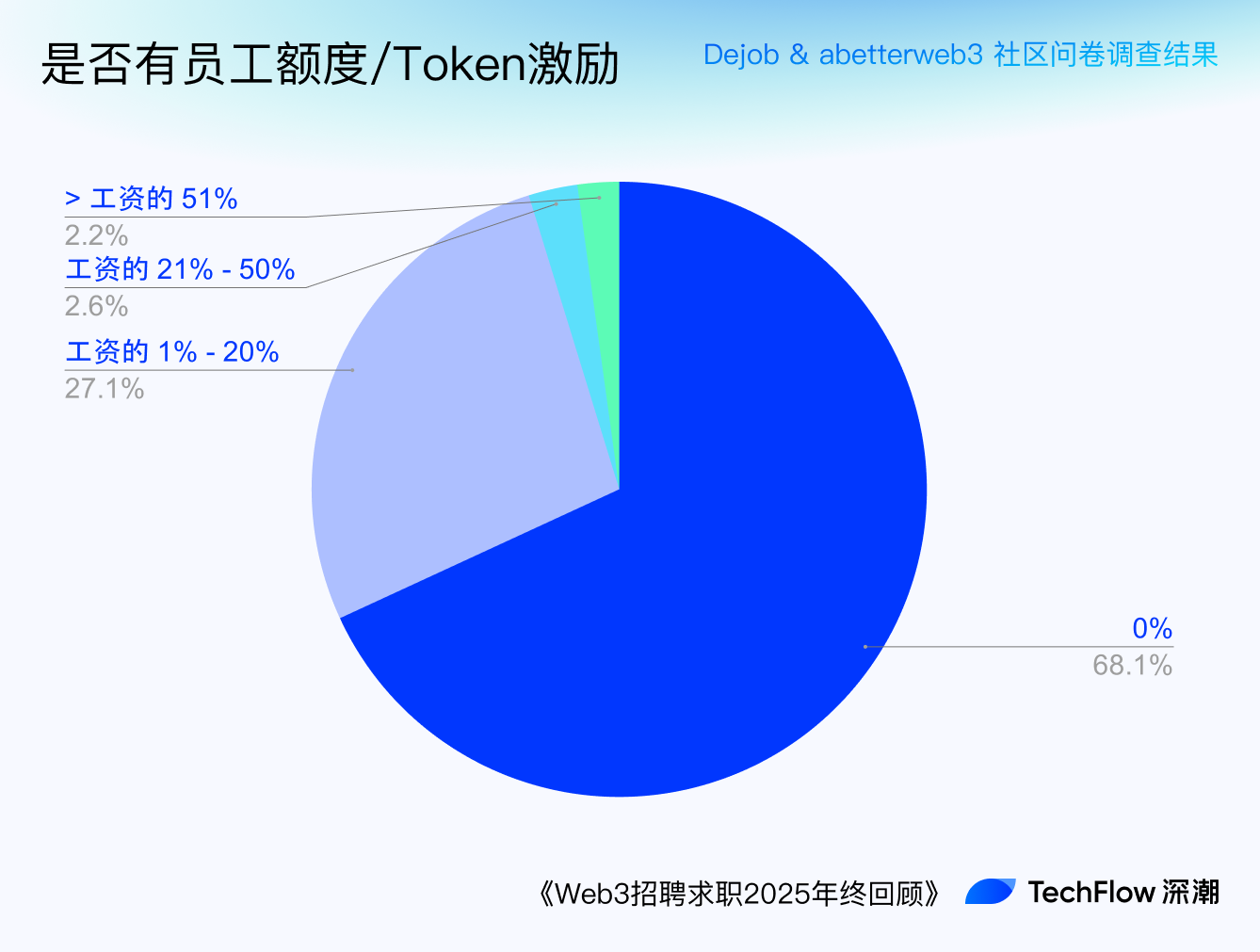

Regarding the well-known "upward channel" of token equity incentives, nearly 70% of practitioners reported not having received any. Even among those who did, very few received more than 20% of their salary's value.

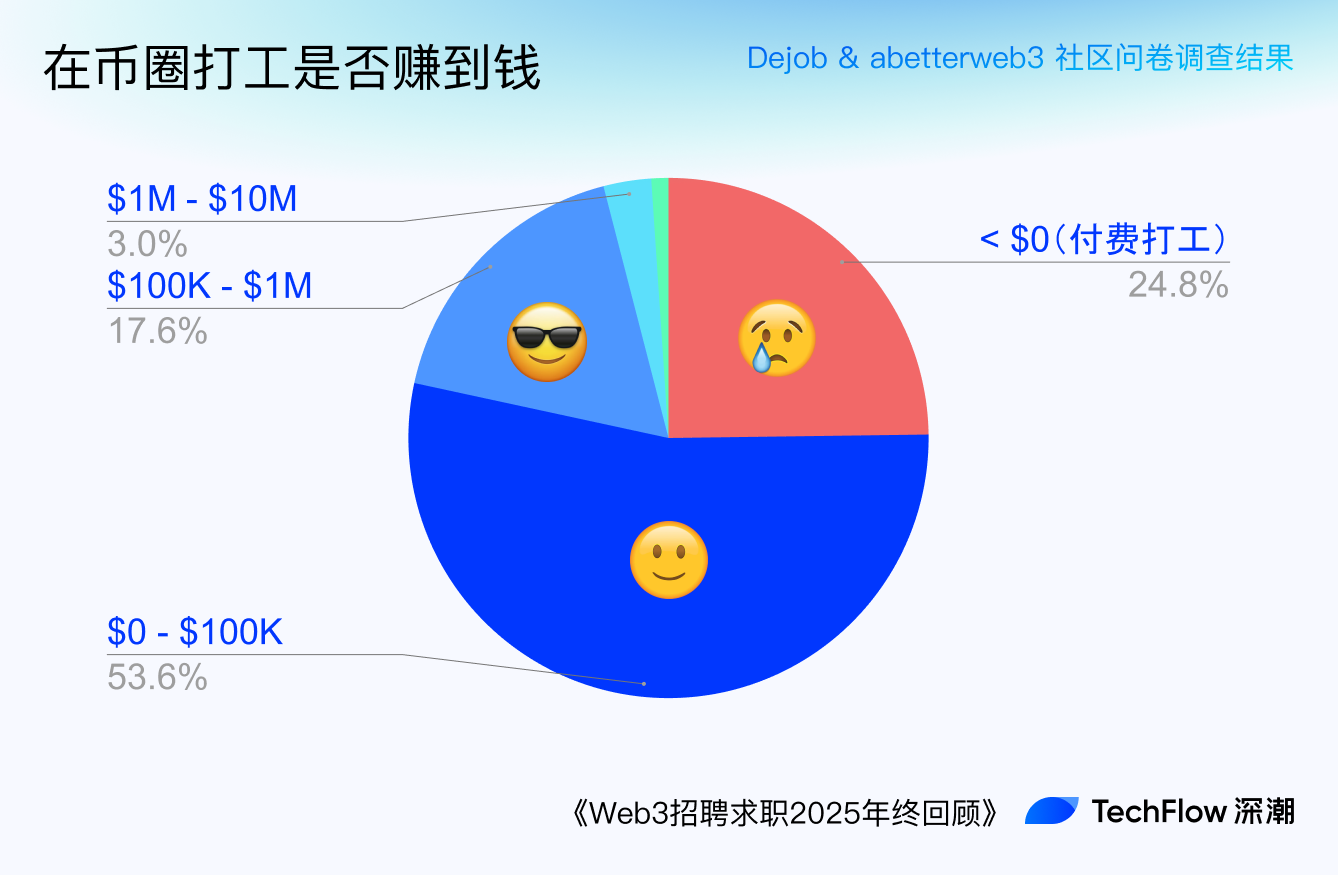

Even a quarter of people have accumulated an overall wealth "loss" since entering the crypto space, in a "pay-to-work" state; other respondents mostly accumulated wealth around $100K (approximately RMB 700,000).

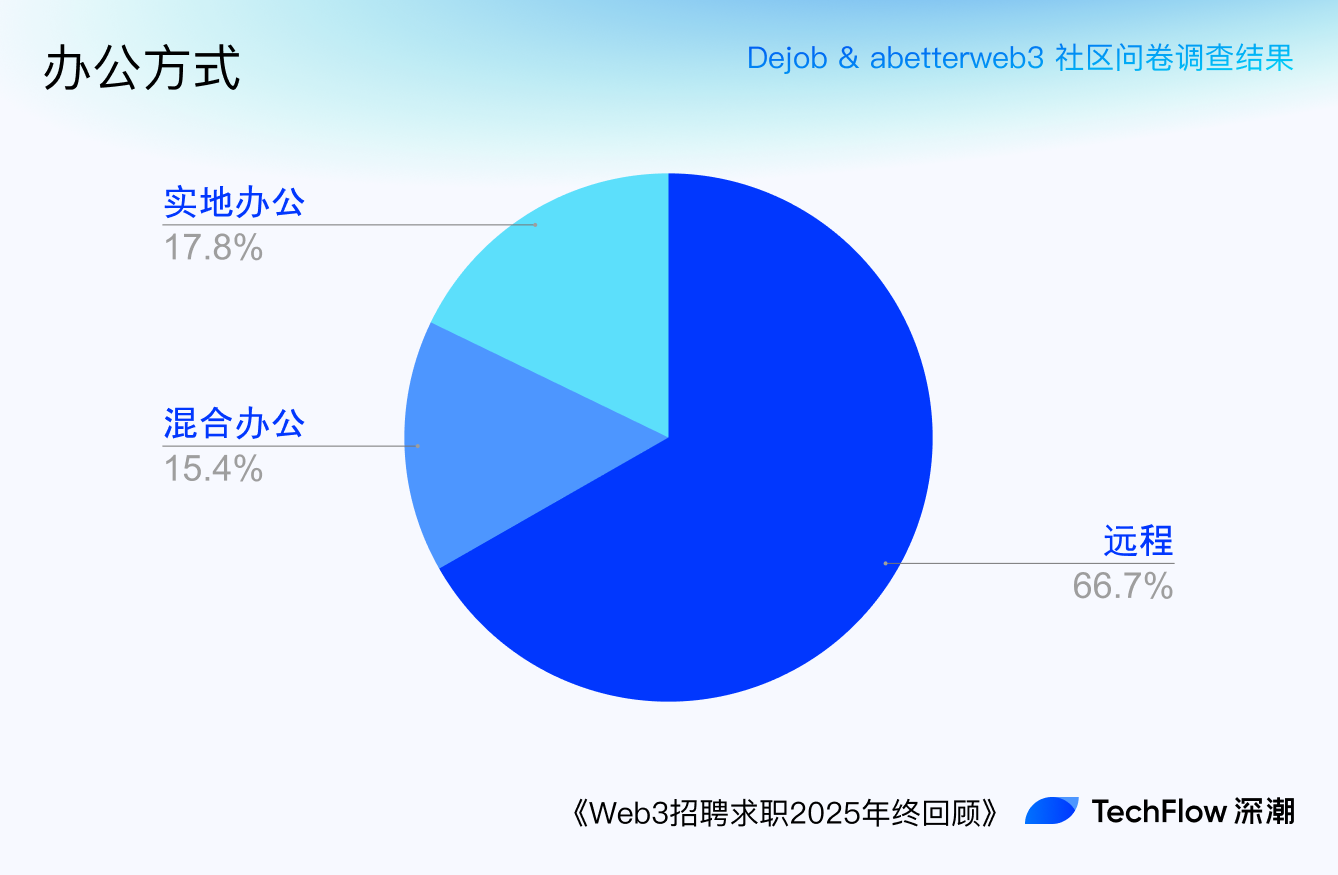

However, on the flip side of this seemingly hopeless income level, Web3's strong remote work culture offers some relief. Nearly 70% of respondents indicated their companies support remote work, and another 15% reported support for hybrid work, meaning虽然有办公室 but attendance is not mandatory, or working from home is allowed a few days a week.

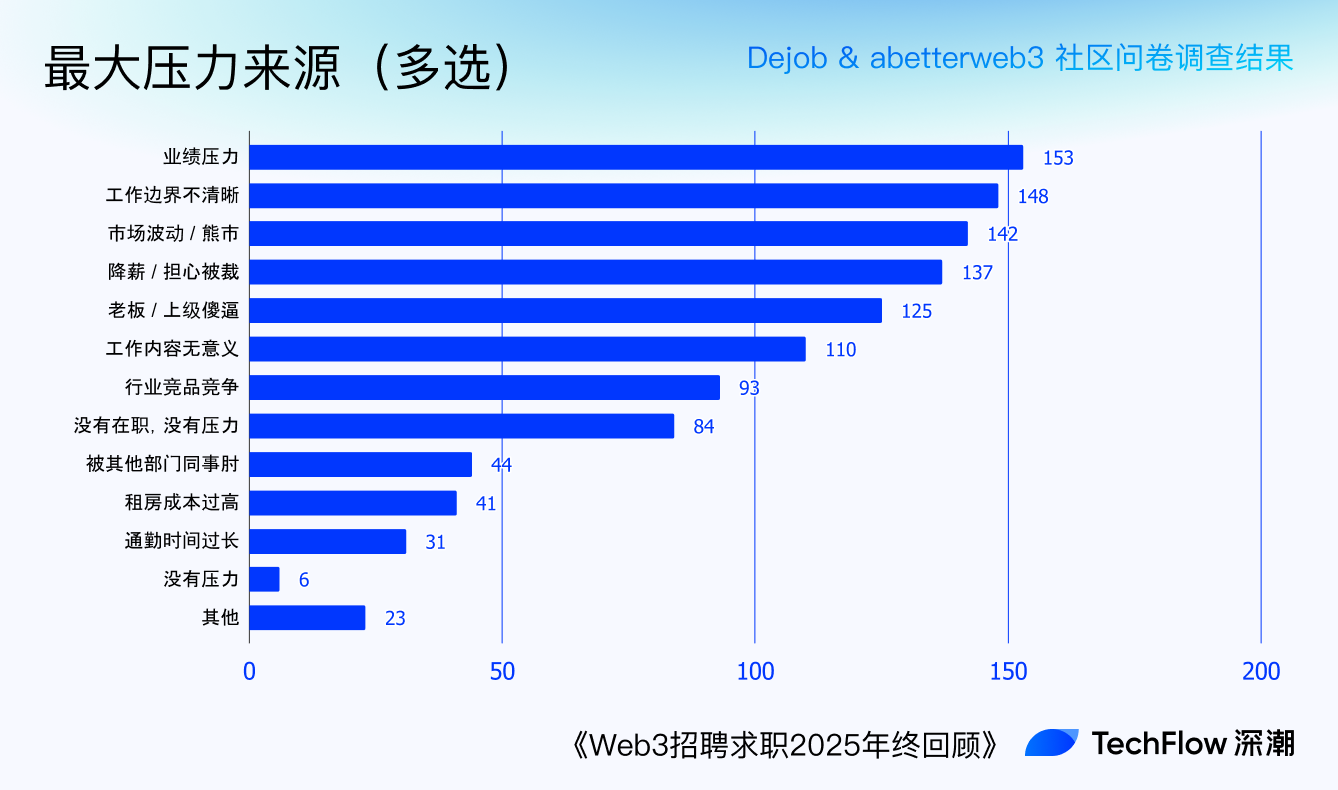

Remote work does alleviate some of the pain of being a worker. In the "biggest source of stress" question, 31 respondents selected "excessively long commute." Other top sources of stress included product growth, work boundaries, market volatility, fear of being laid off, and having a foolish boss.

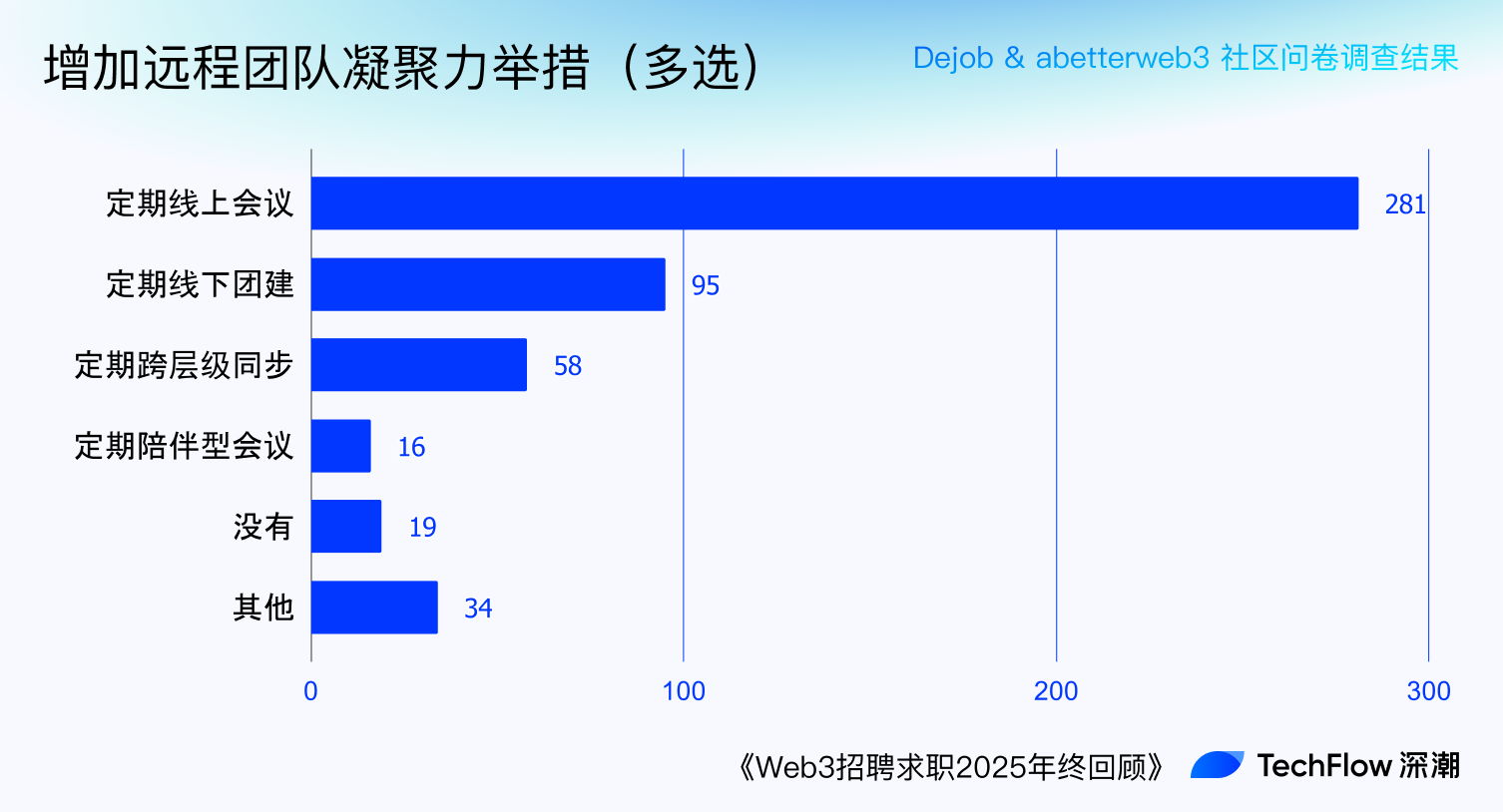

To maintain employees' mental health as social beings, many companies have taken measures to sustain team cohesion.

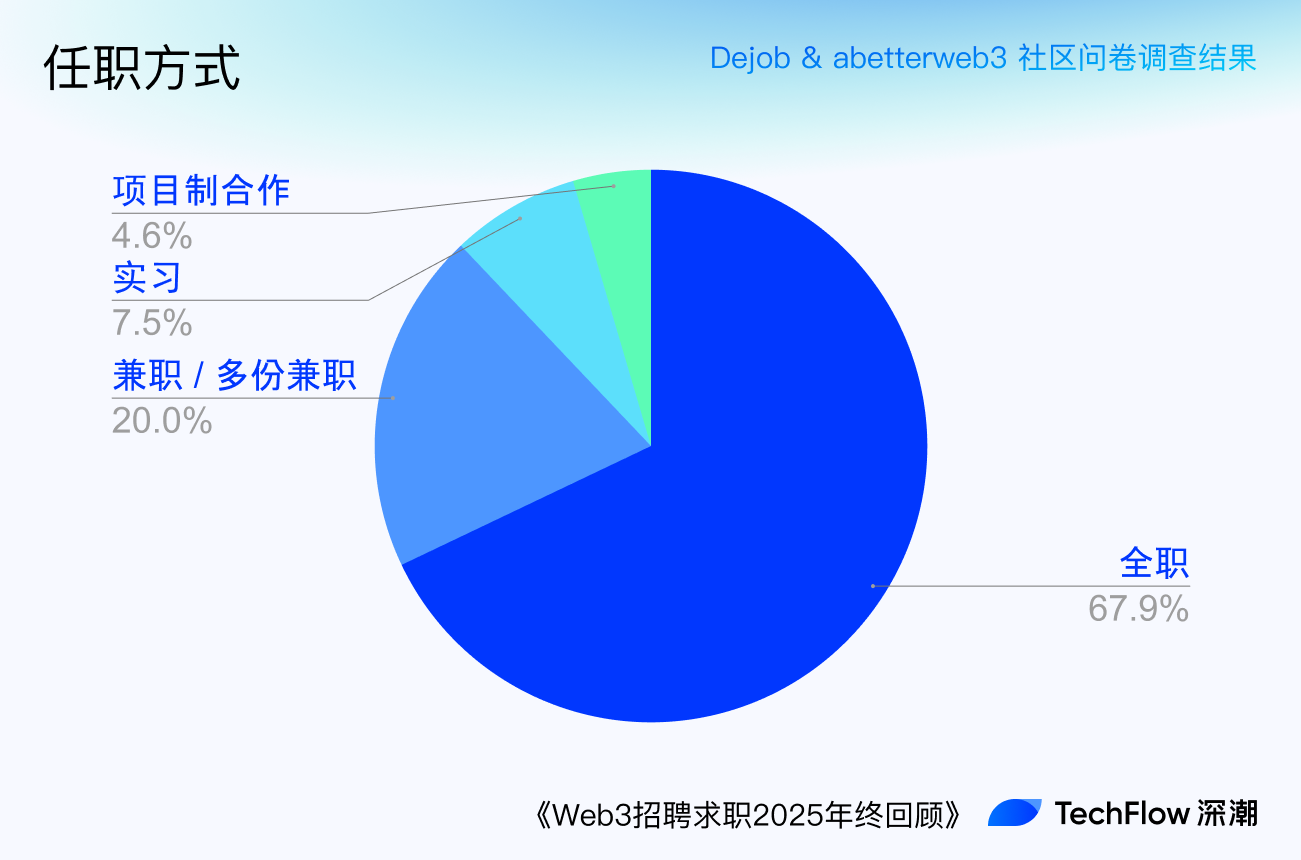

Under the combined effect of low income and instability, many choose to hold multiple jobs. 20% of respondents indicated having side jobs. This also reflects the tech-oriented culture of most Web3 companies: as long as problems are solved and competence is demonstrated, they don't interfere with employees' lifestyles and income methods.

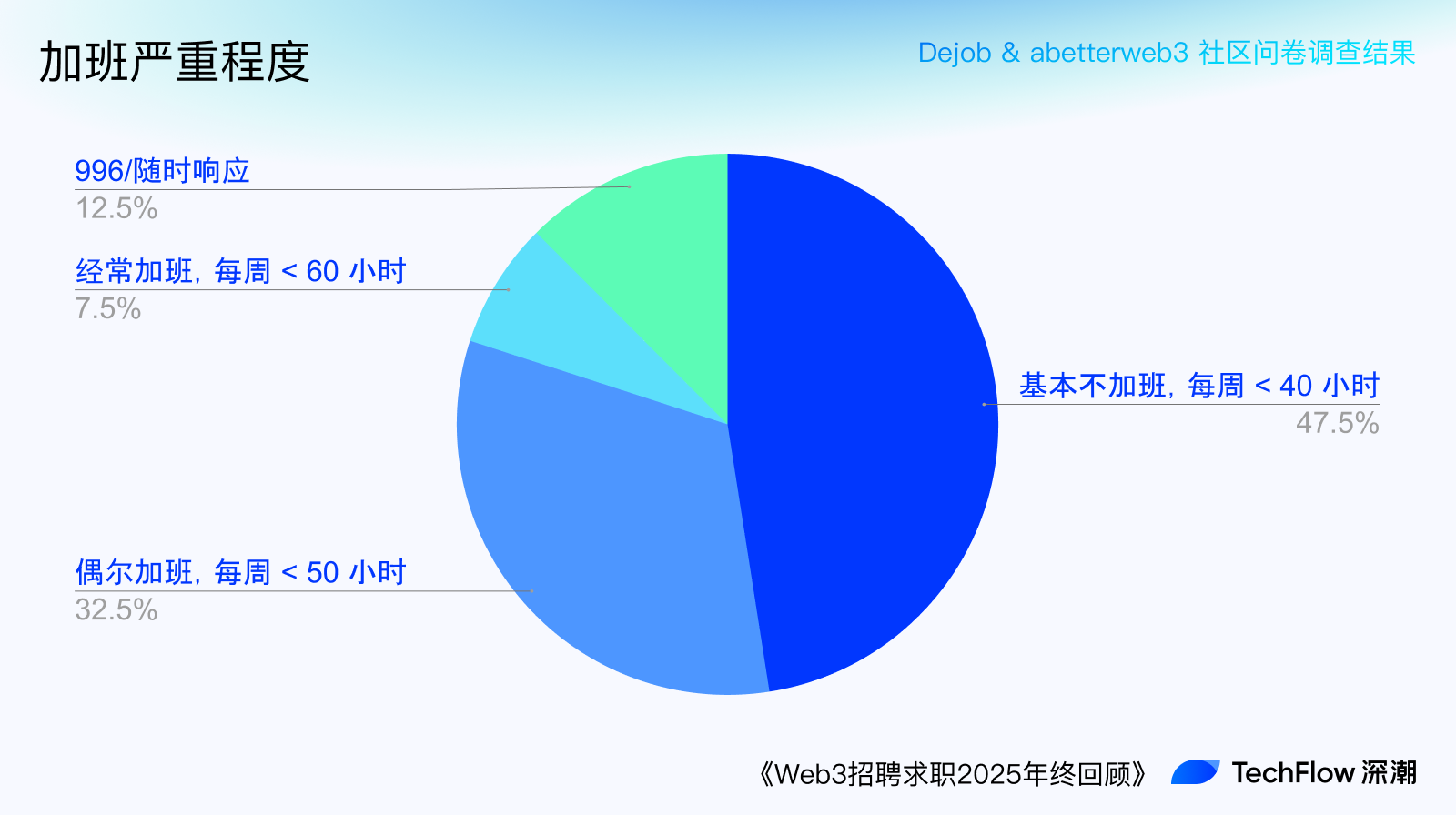

Regarding overtime intensity, 80% of people work approximately 40-50 hours per week. Thus, Web3 overtime seems less intense than many 996/007 sweatshops in web2.

Regarding job hopping, over half want to change companies, with 30% planning to do so within 3-6 months. But about a quarter are satisfied with their current situation, and 8 respondents even found "companies they hope to work for for a lifetime".

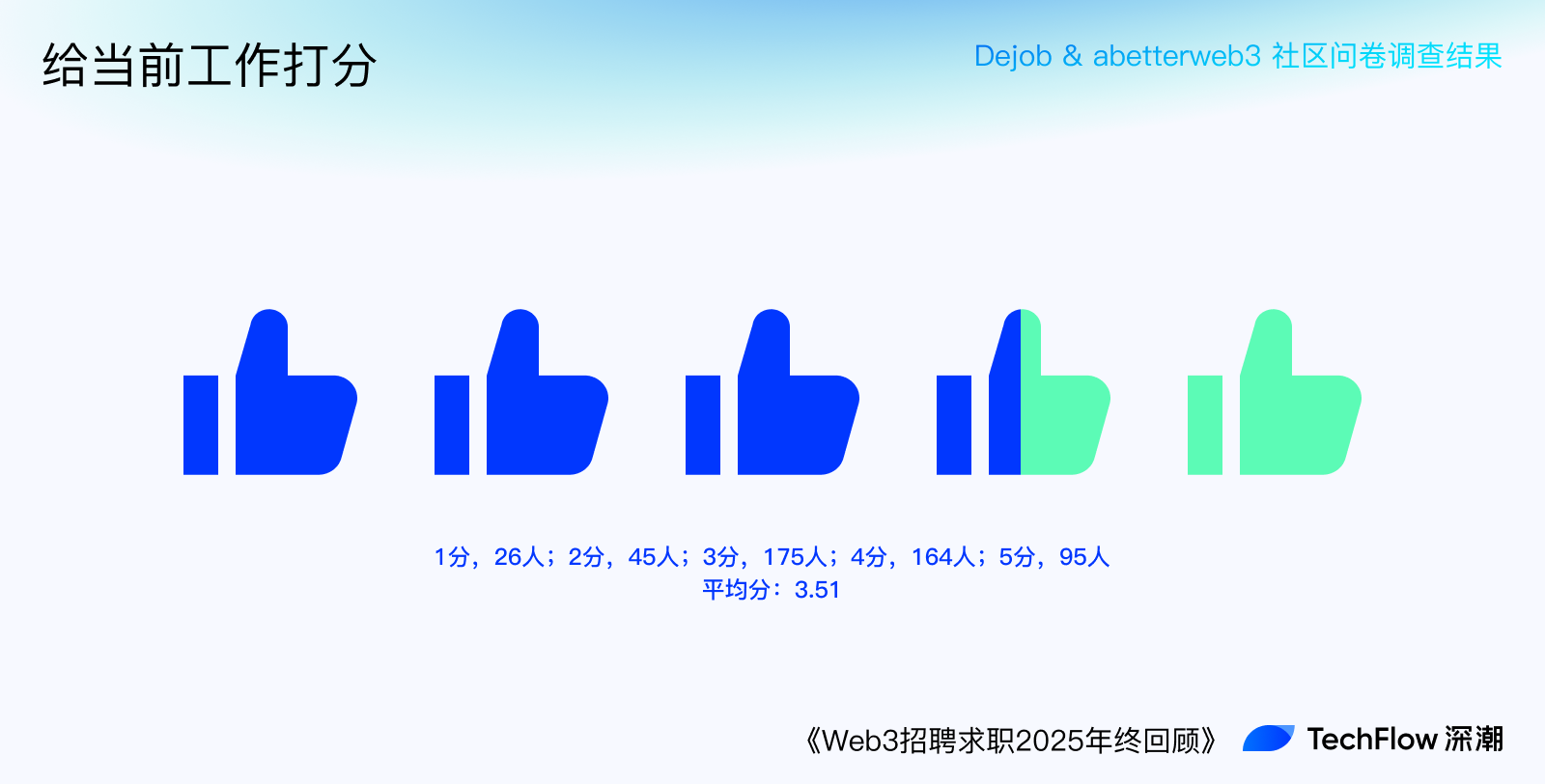

Considering factors like minimal overtime, remote work options, and side jobs allowed, many rate their current job positively. In the rating section for their current job, the average score was 3.51.

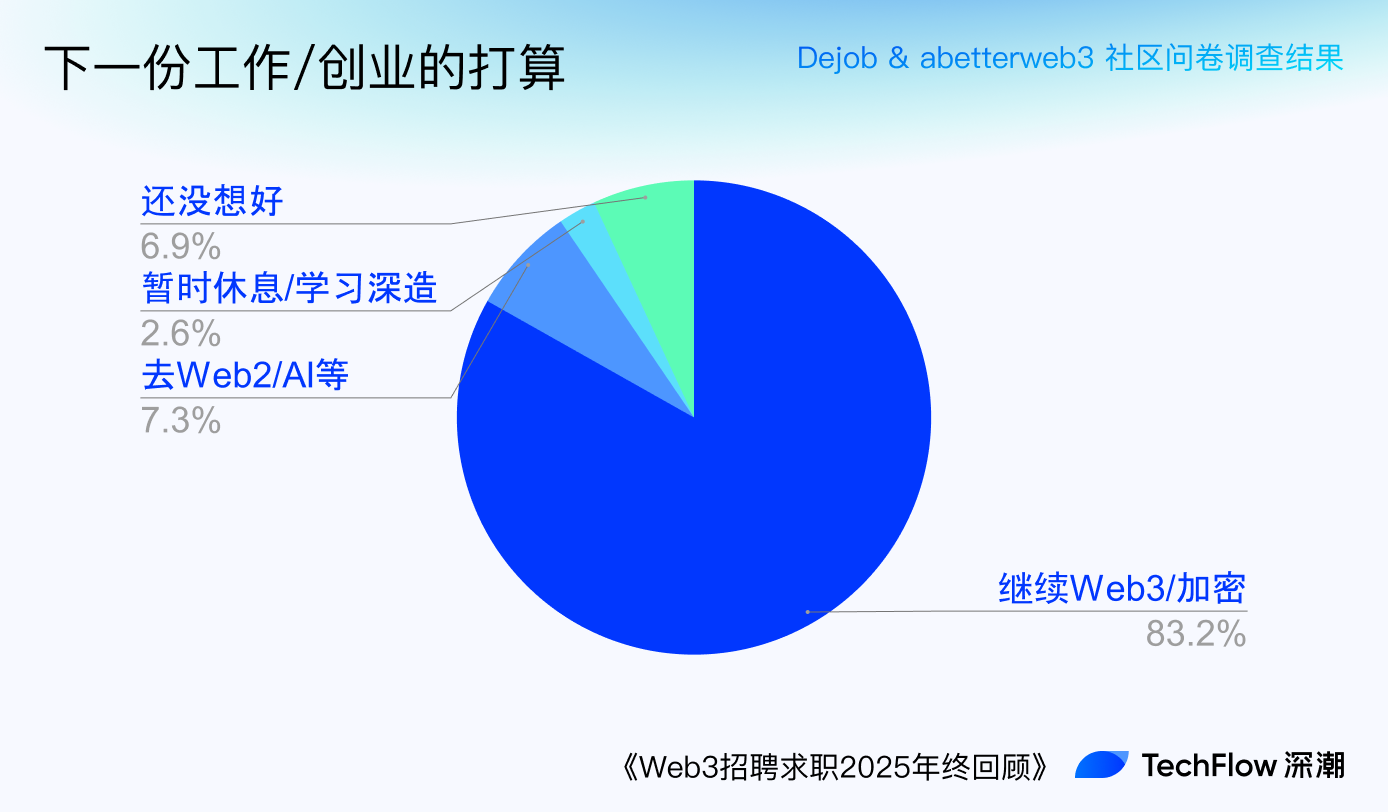

Regarding whether their next job will still be in the crypto space, over 80% choose to stay, while 7% choose to leave.

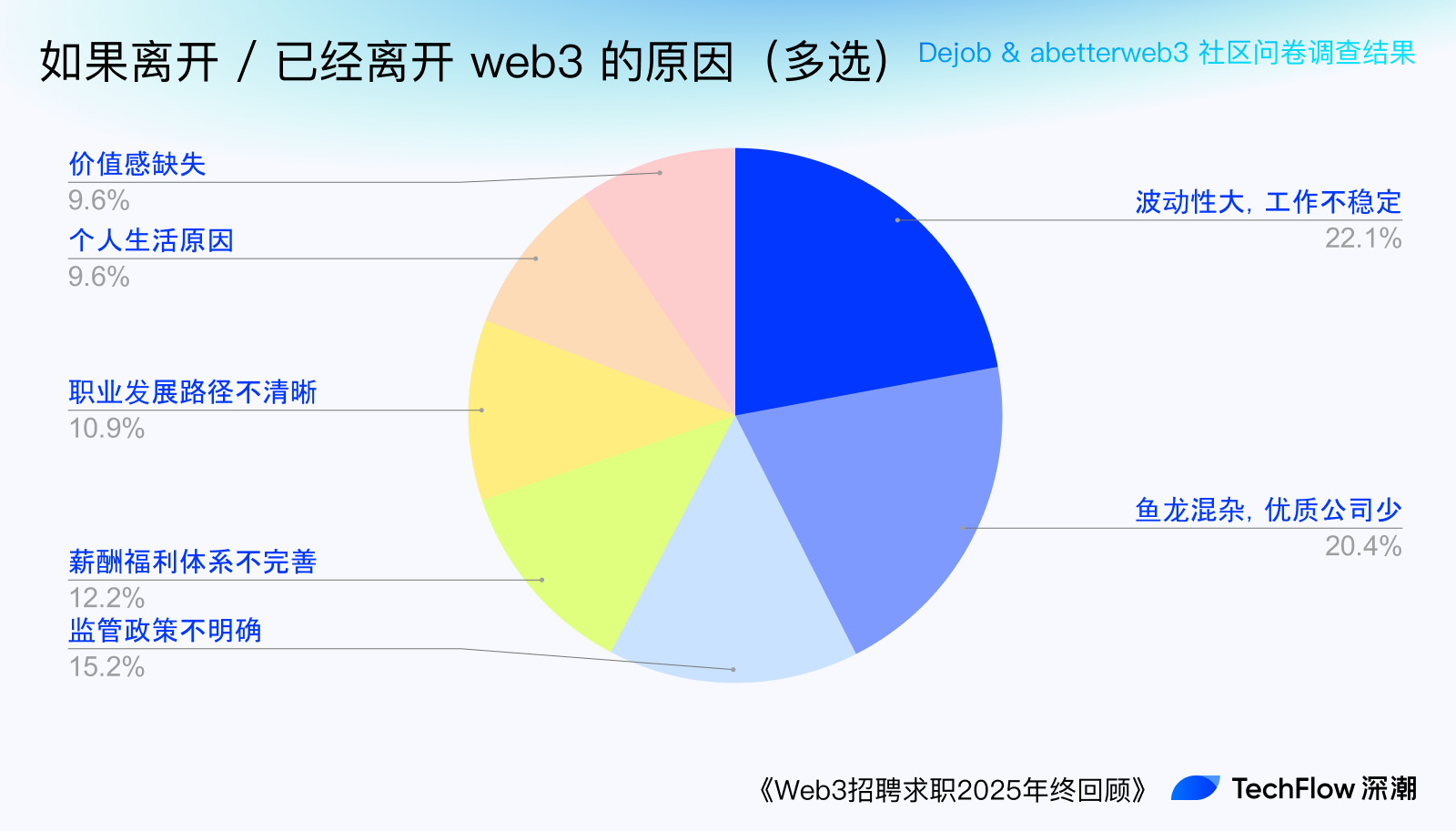

In the reasons for leaving section, the choices reflect the industry's most genuine, cold inner reality.

But all this preparation is for early retirement. For "how much wealth would make you consider resigning", the vast majority chose $1M – $5M (approximately RMB 7 million ~ 35 million). This might indeed be the wealth limit one can achieve through salaried work. But 20% chose "no limit", reflecting confidence in their abilities.

Regarding optimism about the 2026 job market, only 28% believe it will improve, with most being pessimistic or taking a wait-and-see attitude.

Truth Session