When the Dogecoin Exchange-Traded Funds (ETFs) were first approved back in November 2025, it came as a welcome development for the community. This put the meme coin in the league with the likes of Bitcoin and Ethereum, as they continue to make waves with their Spot ETFs. The first month of trading had gone as expected, attracting over $2 million in inflow from investors. But with the month of March 2026, things look to be going left for the Dogecoin ETFs.

Dogecoin ETFs Have Seen Only 2 Days Of Inflow So Far

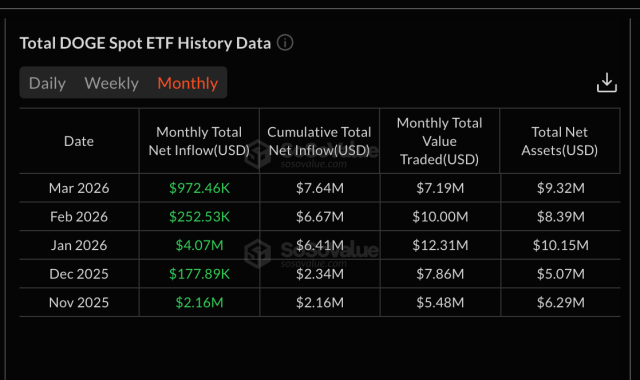

The month of March is almost over, with only about five days left, but so far, Dogecoin ETFs have only seen two days of net inflow, according to data from SoSoValue. The first of these inflows was at the start of the month when around $779,100 flowed into Dogecoin ETFs, pushing its cumulative total inflow so far above $7.6 million for the first time.

After this initial inflow that was recorded on March 2, 2026, the Dogecoin ETFs would go dormant again. In the almost two weeks that followed, there was 0 inflow into the exchange-traded products, while traded values fluctuated wildly, and interest waned.

Then, on March 13, 2026, there was another inflow trend, although lower this time. The value came out to $193,360 in daily inflows, and this brought the total inflows for the month to $972,460. Interestingly, this figure was miles ahead of what was recorded in the previous month of February, with total monthly inflows of $252,530, with only a single day of inflows.

Since the March 13 inflows, Dogecoin ETFs have gone back to 0 inflows once again, with over a week of no liquidity moving into the funds. Total daily traded values across the funds have also remained below the $1 million mark, while Total Net Assets sit at $9.51 million at the time of this report.

How The ETFs Have Fared So Far

With barely five months of trading, the Dogecoin ETFs have had a rather interesting trajectory. Following the first month of trading that saw monthly net inflows hit $2.16 million in November 2025, the funds would go on to have their worst month so far right after. In December 2025, total net inflows to Dogecoin ETFs came out to only $177,890, and the total net assets dropped from $6.29 million in November to $5.07 million by December.

January 2026 has been the most bullish month so far, with $4.07 million in monthly net inflows, $12.31 million in total traded value, and total net assets hitting $10.15 million. The funds are yet to reclaim the peak set in January, with total net assets falling to $8.39 million in February before rising to $9.32 million in March 2026.