Author: Merkle3s Capital

This article is based on the annual report "The Crypto Theses 2026" released by Messari in December 2025. The full report exceeds 100,000 words, with an official estimated reading time of 401 minutes.

This content is supported by Block Analytics Ltd X Merkle 3s Capital. The information herein is for reference only and does not constitute any investment advice or offer. We are not responsible for the accuracy of the content, nor do we assume any consequences arising therefrom.

"Deciphering Messari's 100,000-Word Annual Report (Part 1): Why Did Market Sentiment Collapse Completely in 2025?"

Introduction: When ETH Starts Underperforming, What's the Problem?

Over the past year, ETH underperforming BTC has almost become an indisputable fact.

Whether in terms of price performance, market sentiment, or narrative strength, BTC has been continuously reinforced as the "only core asset":

ETFs, institutional allocation, macro hedging, dollar hedging... Every narrative is converging on BTC.

In contrast, ETH's situation seems somewhat awkward.

It remains the most important underlying network for DeFi, stablecoins, RWA, and on-chain finance, yet it continues to lag in asset performance.

This raises a question that has been repeatedly discussed but never thoroughly dissected:

Is ETH underperforming BTC because it is being marginalized, or because the market is pricing it using a flawed method?

The answer given by Messari in their latest 100,000-word annual report is not one that caters to sentiment or takes sides with any particular chain.

They are more concerned with: where capital is actually being deployed, and what institutions are truly putting on-chain.

From this perspective, ETH's "problem" might be different from what most people imagine.

This article will not discuss beliefs or compare TPS, Gas, or technical roadmaps. We will do only one thing:

Follow Messari's data to clearly break down why ETH is underperforming BTC.

Chapter 1: ETH Underperforming BTC Is Not Inherently Abnormal

If you only at the price performance from 2024–2025, ETH underperforming BTC might lead many to an intuitive judgment:

Has something gone wrong with ETH?

But from a historical and structural perspective, ETH underperforming BTC is not an "anomaly" in itself.

BTC is an asset with a highly singular narrative.

Its pricing logic is clear, consensus is concentrated, and variables are extremely few.

When the market enters a phase of macro uncertainty, regulatory shifts, or institutions reassessing risk assets, BTC often captures the premium first.

ETH is the complete opposite.

ETH simultaneously plays three roles:

-

Decentralized settlement layer

-

Infrastructure for DeFi and stablecoins

-

A "productive network" with a technical upgrade path and execution risks

This means that ETH's price does not only reflect "macro consensus" but is also forced to absorb multiple variables such as technical节奏 (rhythm/timing), ecological changes, and value capture structure.

Messari clearly states in the report:

ETH's problem is not "disappearing demand," but "increasingly complex pricing logic."

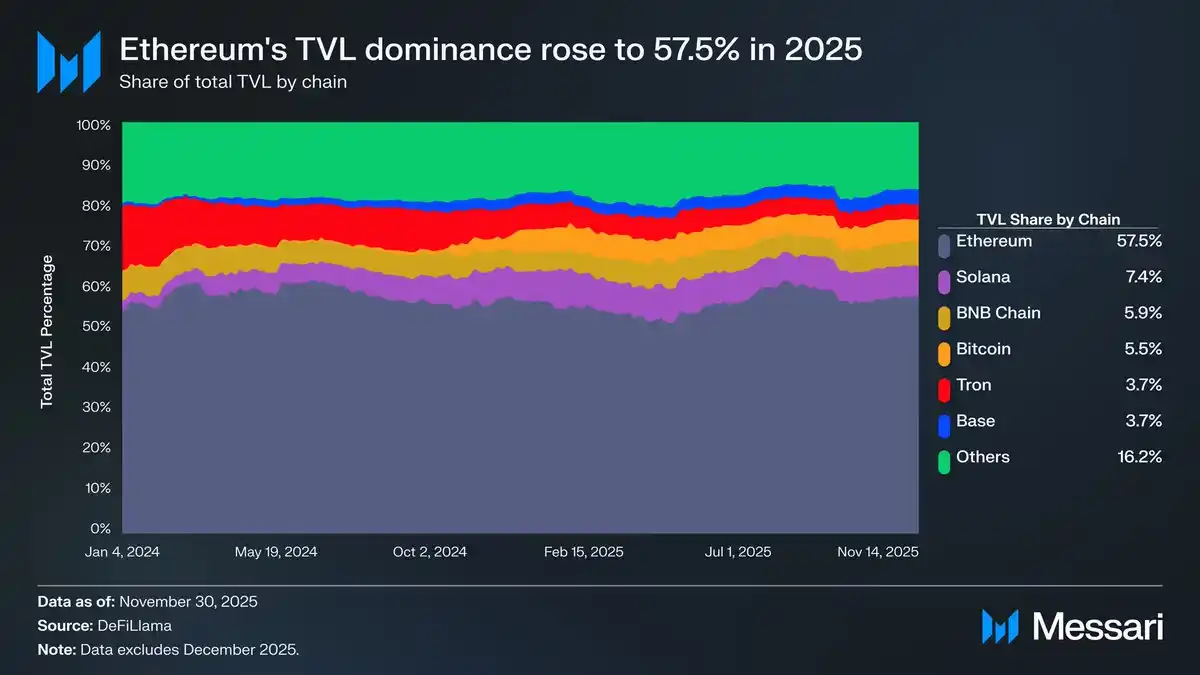

In 2025, ETH still held a dominant position in key metrics like on-chain activity, stablecoin settlement, and RWA hosting.

But this growth does not immediately translate into asset premium, unlike BTC's ETF or macro narratives.

In other words, ETH underperforming BTC does not mean the market is rejecting Ethereum.

It more likely means the market temporarily doesn't know how to price it.

What is truly worth警惕 (vigilance/caution) is not the "underperformance" itself,

but rather: when ETH is heavily used, whether this usage can continue to feedback into the ETH asset.

This is the real issue Messari is concerned about.

Chapter 2: Usage is Increasing, But Value Isn't Keeping Up? ETH's Value Capture Dilemma

What really made the market start doubting ETH was not the price underperforming BTC,

but a more glaring fact: Ethereum is being heavily used, but ETH asset itself is not benefiting proportionally.

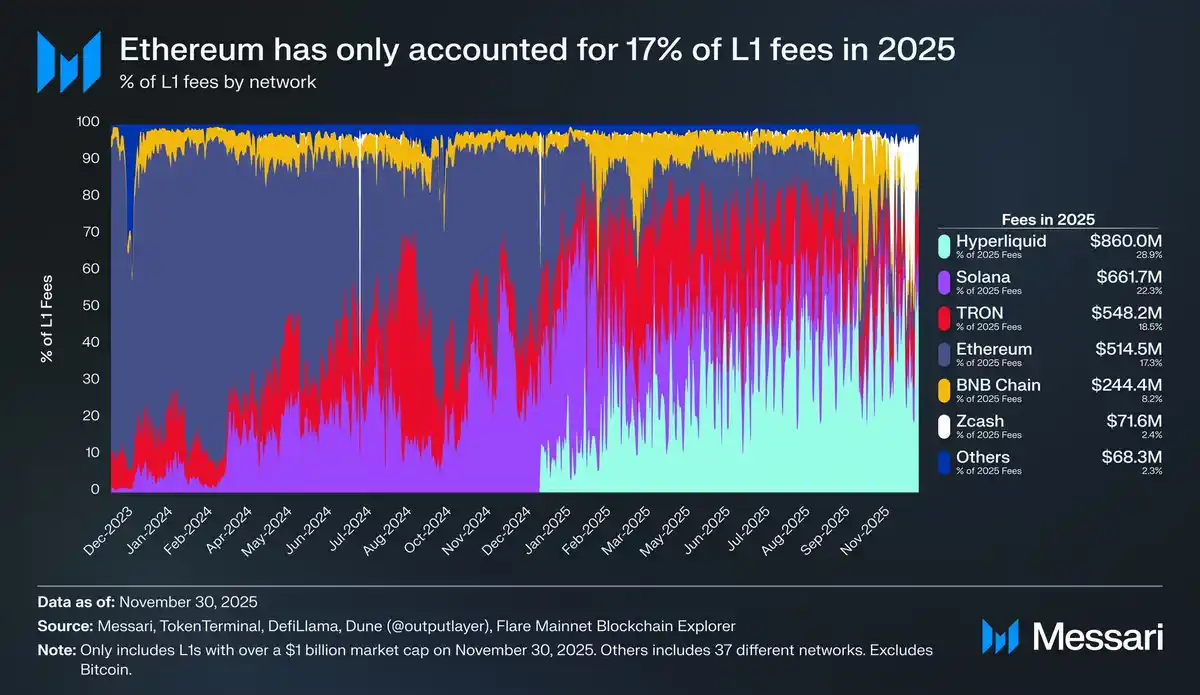

Messari provides a set of key data in the report:

With the rise of competitive L1s, Ethereum's share of L1 transaction fees has been continuously declining.

-

Solana re-established its position as a high-performance execution layer in 2024,

-

Hyperliquid rapidly scaled through on-chain derivatives in 2025,

-

Together, they squeezed Ethereum's share in the dimension of "direct monetization of economic activity."

By 2025, Ethereum's share of L1 fees had fallen to about 17%,

dropping to fourth place among L1s.

Just a year earlier, it firmly held the top spot.

Fees are not the only indicator of network value, but they are an extremely honest signal:

Where fees are collected is where real trading behavior and risk appetite reside.

This is also where ETH's core矛盾 (contradiction) begins to show.

Ethereum has not lost users. On the contrary, its position in areas like stablecoins, RWA, and institutional settlement has become more solid. The problem is, these activities are increasingly happening on L2s or at the application layer, rather than being directly reflected as L1 fee revenue.

In other words: Ethereum as a system is becoming more important, while ETH as an asset is increasingly resembling "diluted equity."

This is not a technical failure, but an inevitable consequence of architectural choices.

The Rollup scaling route successfully reduced transaction costs and increased throughput, but it also objectively weakened ETH's ability to directly capture usage value.

When usage is "outsourced" to L2s, ETH's revenue comes more from abstract security premiums and monetary expectations, rather than cash flow.

This is also why the market hesitates when pricing ETH:

Is it an asset that compounds with usage growth, or is it becoming more like a "public infrastructure" neutral settlement layer?

This issue is further amplified as multi-chain competition intensifies.

Chapter 3: Multi-Chain is Not the Threat, the Real Pressure Comes from "Execution Layer Substitution"

If you only look at the narrative level, ETH seems to have more and more competitors.

Solana, various high-performance L1s, app-chains, even dedicated trading chains have emerged one after another,

easily leading to the conclusion: ETH is being marginalized by a "multi-chain world."

But Messari's judgment is calmer, and also more残酷 (cruel/harsh).

Multi-chain itself is not a threat to ETH.

The real pressure comes from the continuous substitution of the execution layer, while the value of the settlement layer is difficult for the market to price directly.

Take Solana as an example:

-

Solana recaptured the主场 (home ground) for high-frequency trading and retail activity in 2024–2025,

-

Leading明显 (significantly) in spot trading volume, on-chain activity, and low-latency experience.

But this growth is more reflected in "trading experience" and "traffic density," rather than stablecoin清算 (settlement/clearing), RWA custody, or institutional-grade settlement.

Messari repeatedly emphasizes a fact in the report:

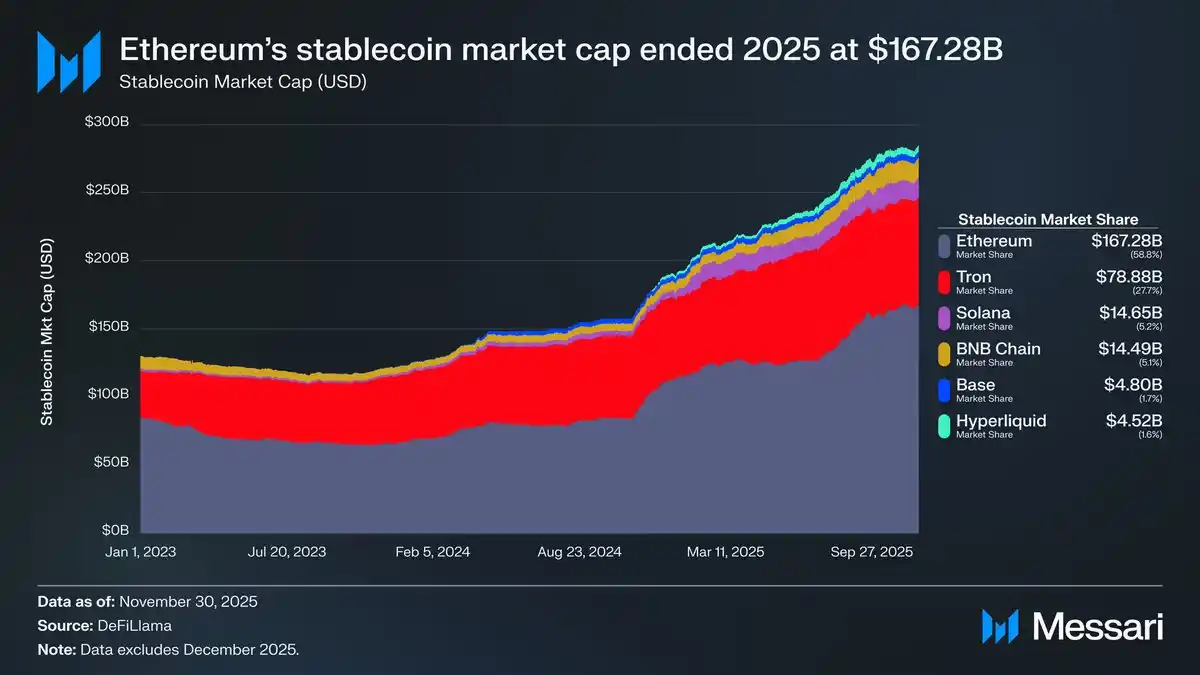

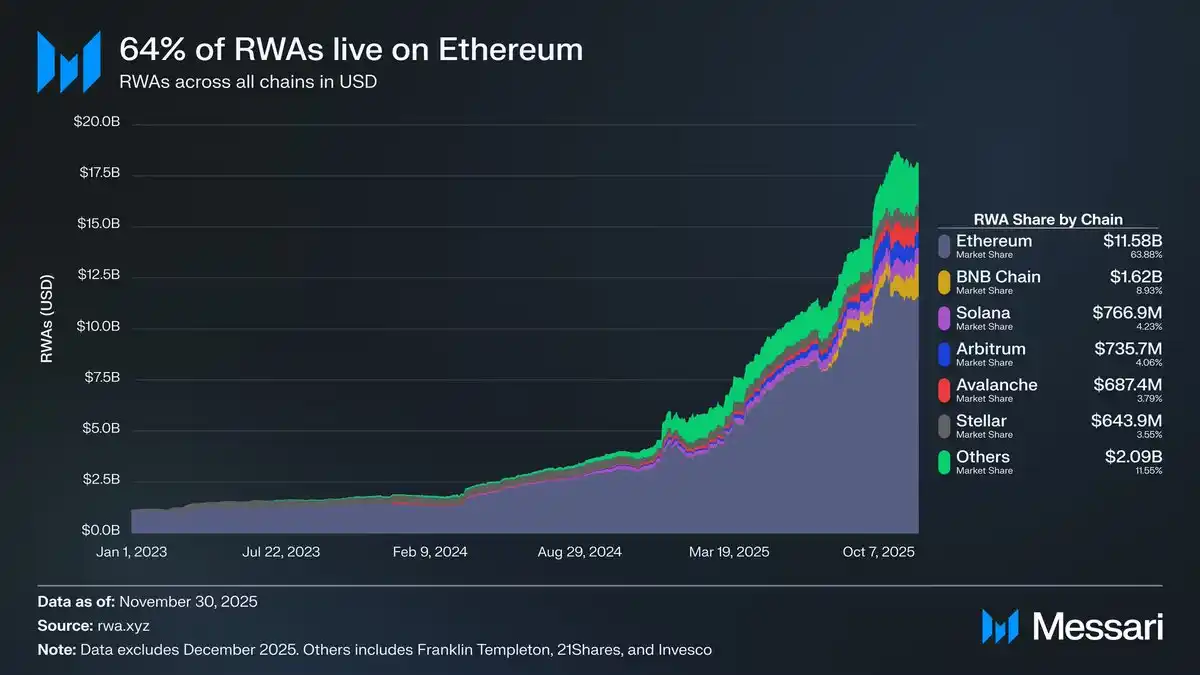

When institutions actually put money on-chain, they still首选 (prefer/choose first) Ethereum.

Stablecoin issuance, Tokenized T-bills, on-chain fund shares, compliant custody paths—these most "boring" but most critical financial infrastructures—are still highly concentrated in the Ethereum ecosystem.

This also explains a seemingly contradictory phenomenon: ETH's asset performance is under pressure, but Ethereum has反而 (instead) further consolidated its leading advantage in the dimension of "blockchain institutions are willing to use."

The problem is, the market does not automatically pay a premium just because "you are important."

When execution layer revenue is taken by other chains, and the value of the settlement layer is more reflected in "security" and "compliance credibility," ETH's pricing logic inevitably becomes abstract.

In other words:

ETH is not "being replaced," but is being pushed to assume a role more akin to public infrastructure.

And infrastructure often sees higher usage rates, yet finds it harder to tell a story for asset premiums.

This is where the fundamental difference between ETH and BTC begins to彻底 (thoroughly) diverge.

Chapter 4: ETH Still Relies on BTC's "Macro Anchor"

If the first three chapters answer one question—Has ETH been marginalized?

Then this chapter must face a more残酷 (cruel/harsh) and realistic judgment:

Even if ETH is not replaced, at the asset pricing level, it remains deeply依附于 (dependent on) BTC.

Messari repeatedly emphasizes a fact overlooked by many in the report:

The market is not pricing "blockchain networks," but rather things that can be abstracted as macro assets.

On this point, the divergence between BTC and ETH is extremely clear.

BTC's narrative has been彻底 (completely) simplified to three things:

-

Macro hedging asset

-

Digital gold

-

A "monetary asset" acceptable to institutions, ETFs, and national balance sheets

ETH's narrative, however, is much more complex.

It is both a settlement layer and a technical platform; it承载 (carries/bears) financial activities while constantly undergoing upgrades and structural adjustments.

This makes it very difficult for ETH to be directly纳入 (incorporated into) a "macro asset basket" like BTC.

This difference is particularly evident in ETF fund flows.

When the ETH spot ETF was first launched in early 2024, the market一度 (once) believed: institutions had almost no interest in ETH.

For the first six months, ETH ETF inflows were significantly weaker than BTC's, reinforcing the narrative that "BTC is the only institutional asset."

But Messari points out that this conclusion itself is misleading.

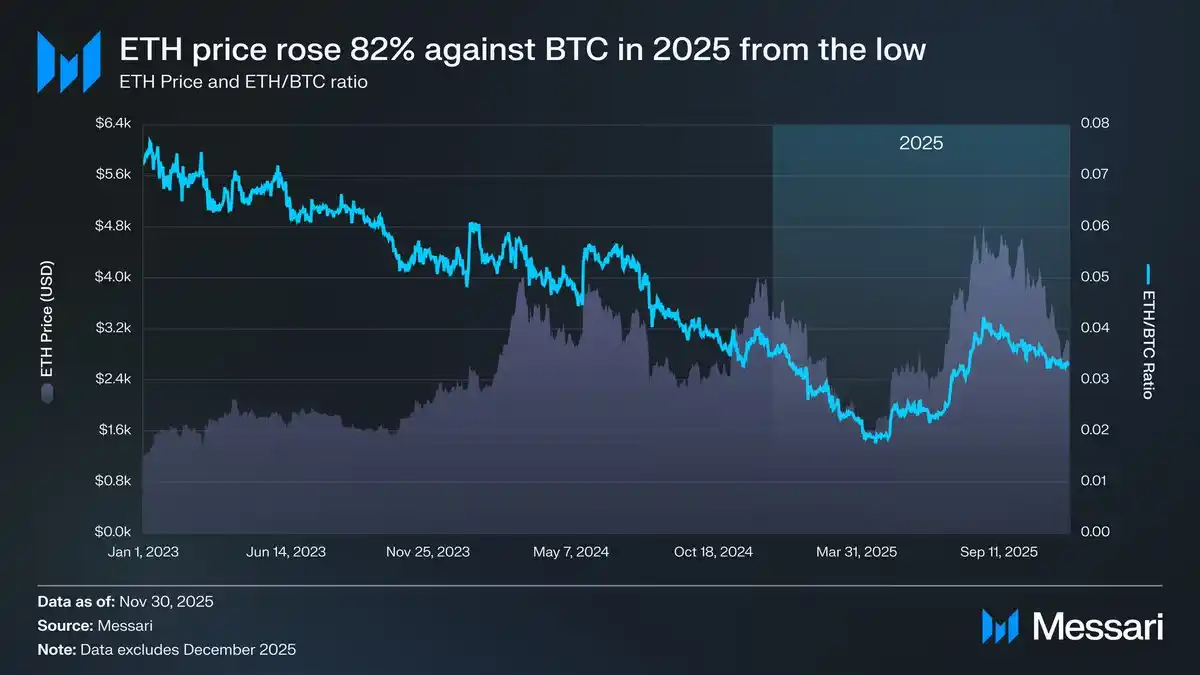

As the ETH price and the ETH/BTC ratio rebounded simultaneously in mid-2025, fund behavior began to change.

-

ETH/BTC rebounded from a low of 0.017 to 0.042, a gain of over 100%

-

ETH's USD price rose nearly 200% in the same period

-

ETH ETF inflows began to accelerate significantly

In some periods, new inflows into ETH ETFs even briefly surpassed those of BTC.

This说明 (indicates/shows) one thing:

Institutions are not unwilling to buy ETH, but are waiting for "narrative certainty."

Even so, Messari still offers a sobering conclusion:

ETH's monetary premium remains, to this day, a "secondary derivative" of BTC's monetary consensus.

In other words, the reason the market is willing to embrace ETH again at certain stages is not because ETH has become an independent macro asset, but because BTC's macro narrative remains valid and spills over to the risk curve.

As long as BTC remains the pricing anchor for the entire crypto market, ETH's strength or weakness will inevitably be measured in BTC's shadow.

This does not mean ETH has no upside potential. On the contrary,前提 (provided that) the BTC trend holds, ETH often possesses higher elasticity and stronger Beta.

But it also means:

ETH's asset narrative has not yet completed its "de-BTC-ification."

Until ETH can demonstrate, over longer cycles, lower BTC correlation, more stable independent demand sources, and a clearer value capture path,

it will still be viewed by the market as:

A second-layer belief asset built on top of BTC.

Chapter 5: Is ETH Threatened? The Real Question Was Never About Winning or Losing

By discussing this far, we can actually answer a question that is repeatedly raised:

Will ETH be "replaced" by other chains?

Messari's answer is clear:

No.

At least for the foreseeable future, Ethereum remains the default foundation for on-chain finance, stablecoins, RWA, and institutional settlement.

It is not the fastest chain, but it is the chain最先 (first) allowed to carry real funds.

What is truly worth worrying about is not "whether ETH will lose to Solana, Hyperliquid, or the next new chain,"

but another, more uncomfortable question:

As an asset, can ETH still持续 (continuously) benefit from Ethereum's success?

This is a structural problem, not a technical one.

Ethereum is increasingly resembling "public financial infrastructure":

-

Usage is growing

-

System importance is increasing

-

Institutional reliance is deepening

But at the same time, ETH's value capture relies increasingly on:

-

Monetary premium

-

Security premium

-

Spillover from macro risk appetite

Rather than direct cash flow or fee growth.

This is also why ETH's asset performance increasingly resembles a "high-Beta derivative asset of BTC," rather than a network equity with an independent pricing system.

In a multi-chain world, execution layers can be competed for, traffic can be分流 (diverted/split), but settlement layers do not migrate frequently.

Ethereum恰恰 (precisely) stands in this most stable, yet最难 (most difficult) position to be rewarded by market sentiment.

Therefore, ETH underperforming BTC does not signify failure.

It is more like a result of role division:

-

BTC承担 (bears/undertakes) macro narrative, monetary consensus, and asset anchoring

-

ETH承担 (bears/undertakes) settlement, financial infrastructure, and system security

The only problem is, the market is more willing to pay a premium for the former, while remaining克制 (restrained/cautious) towards the latter.

Messari's conclusion is not激进 (radical), but足够 (sufficiently) honest:

ETH's monetary story has been repaired, but is not yet complete. It can rise significantly when the BTC trend is established, but it has not yet proven it can be priced independently脱离 (detached from) BTC.

This is not a negation of ETH, but a阶段性 (stage-specific) positioning.

In an era where BTC remains the only macro anchor of the crypto market,

ETH is more like the financial operating system built upon this anchor.

It is important, it is irreplaceable, but for now, it is not yet the asset that gets "priced first."

At least for now, it is not.