Original | Odaily Planet Daily (@OdailyChina)

Author | Azuma (@azuma_eth)

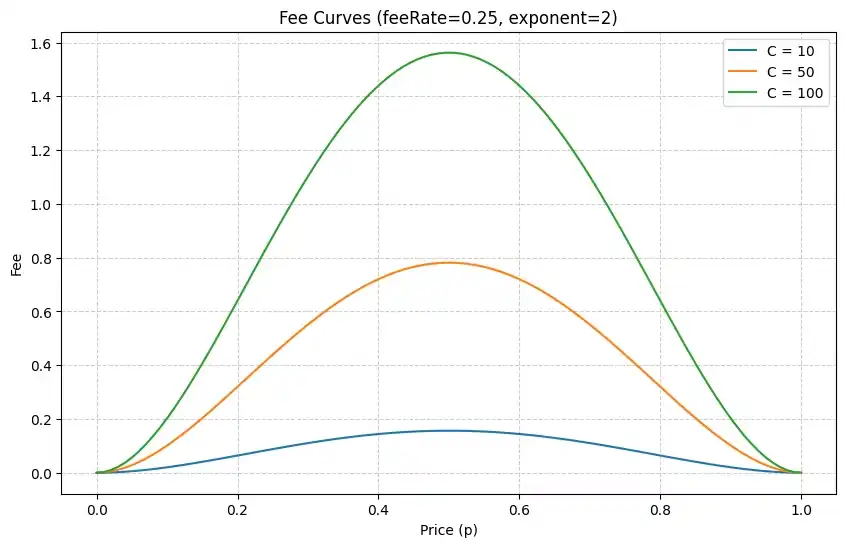

On January 6th of this year, Polymarket officially began charging transaction fees for markets related to "15-minute cryptocurrency price movements." The specific fee rate varies with the real-time odds of the market — the closer the odds are to 0% or 100%, the lower the fee; conversely, the closer the odds are to 50%, the higher the fee, with a maximum of 1.56%.

This marks the first time, outside of the U.S. market (where Polymarket charges a 0.01% fee), that Polymarket has ended its completely free model and started charging transaction fees for a specific type of market. Now, three weeks later, there is a sufficient observable data sample, making it time to conduct a rough estimate of Polymarket's revenue potential.

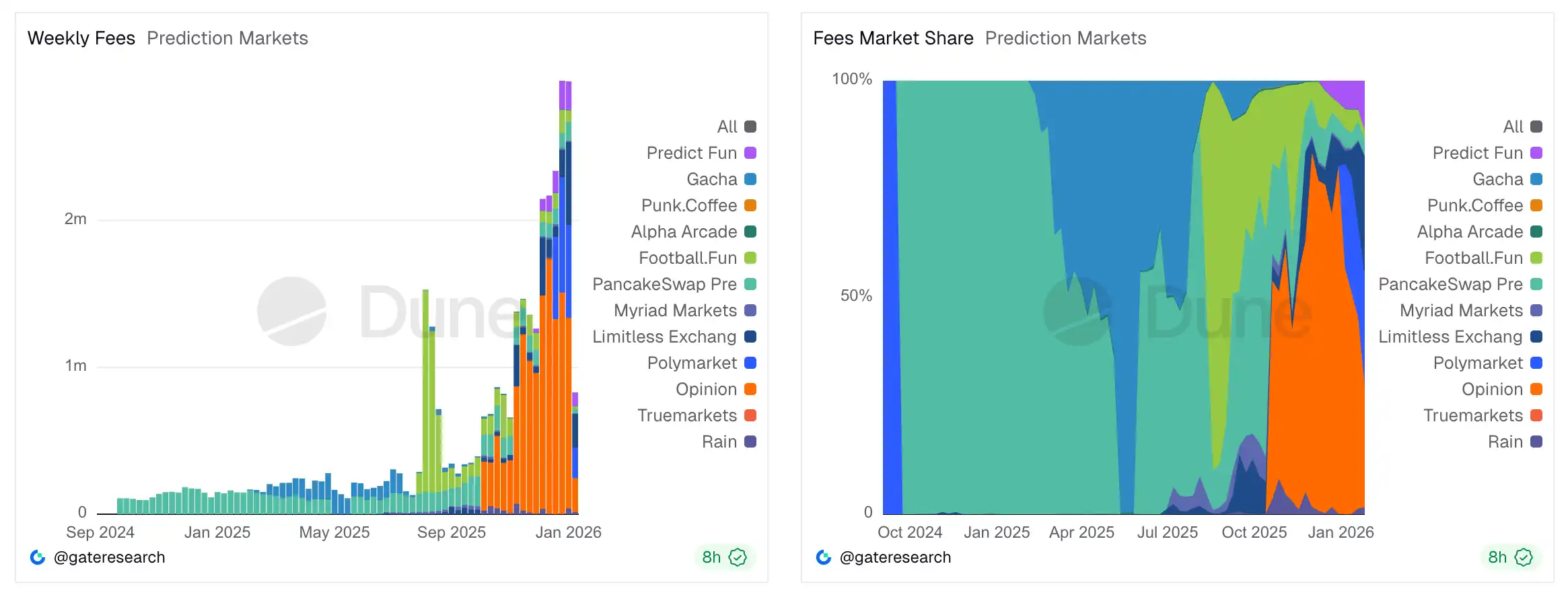

First, let's look at the most direct measure: the scale of fee revenue. According to data compiled by Gate Research on Duna, since the introduction of these fees, Polymarket has accumulated approximately $2.19 million in fee revenue, averaging about $730,000 per week. Based on this data, if the trading volume and activity structure of the relevant markets remain unchanged, it is projected to generate approximately $38 million in annual revenue for Polymarket.

It is foreseeable that Polymarket's fee-charging scope will not be limited to just the "15-minute cryptocurrency price movements" category. Prior to officially charging fees for this category, Polymarket had long maintained a completely free model while also subsidizing market liquidity out of its own pocket. At the end of last year, Coplan himself admitted that Polymarket was operating at a loss... But we have seen too many such "burning cash" stories in the internet market. As Polymarket's user habits and market position gradually solidify, it would not be surprising to see fees introduced for more markets in the future.

- Odaily Note: For more on Polymarket's revenue issues, refer to Odaily's recent Tea Talk column "Odaily Editorial Tea Talk (January 7th)."

Assuming Polymarket continues to apply the current fee standards to other markets in the future, we might gauge the theoretical revenue ceiling for Polymarket at the current trading volume level by comparing the trading volume of the "15-minute cryptocurrency price movements" market with Polymarket's total platform trading volume. The more markets that charge fees, the higher the revenue.

Data obtained by Odaily shows that the total trading volume of the "15-minute cryptocurrency price movements" market on Polymarket over the past week was approximately $159 million (among the four major tokens, BTC accounted for $114 million, ETH for $30.29 million, SOL for $8.93 million, and XRP for $5.73 million). This represents about 9.1% of Polymarket's total trading volume of approximately $1.75 billion over the past week. Based on this ratio, if Polymarket introduces a similar fee model across all markets under the current trading volume and structure, it is projected to generate $418 million in annual revenue for the platform.

It should be noted that the above are all estimates by Odaily based on historical data. In reality, Polymarket's actual revenue situation will inevitably deviate due to various variables — first, Polymarket has only been charging fees for three weeks, so the sample size is still relatively small; second, Polymarket may not adopt a similar fee mechanism for other markets, and differences in user trading habits across markets will also lead to variations in the final fee results under a dynamic fee mechanism; third, and most crucially, Polymarket is still in a strong growth phase. It is expected that with the further popularization of the prediction market concept, coupled with potential highlights like the 2026 World Cup and mid-term elections, the platform's trading volume will continue to grow in the future.

Even considering these uncertainties, one trend is already quite clear — Polymarket is demonstrating the revenue potential of this entirely new format of prediction markets. It is no longer just a novel innovative concept but a truly sustainable, self-generating business with immensely imaginative profit space.