Original Author: CM(X:@cmdefi)

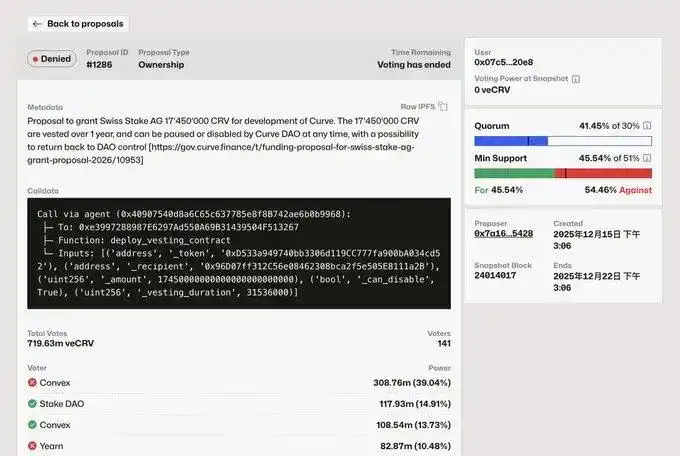

A few days ago, a funding proposal on Curve was rejected. It involved allocating 17M $CRV in development funds to the development team (Swiss Stake AG). Both Convex and Yearn voted against it, and their voting power was sufficient to influence the final outcome.

Since the governance issues at Aave began to gain attention, governance has started to be scrutinized by the market, and the habitual practice of approving funding requests is being broken. Behind this Curve proposal lie two key points:

1. Some voices in the community are not opposed to funding AG, but they want clarity on how previous funds were used, future plans for usage, sustainability, and whether the projects have generated returns for the protocol. Simultaneously, this primitive grant model means that once funds are disbursed, there are no constraints. In the future, the DAO needs to establish a Treasury, ensure transparent revenue and expenditure, or add governance constraints.

2. The large veCRV holders do not want to dilute their value. This is a clear conflict of interest. If the projects supported by CRV grants cannot foreseeably create benefits for veCRV holders, they likely won't receive support. Of course, Convex and Yearn also have their own private interests and agendas, but we won't delve into those issues here.

This proposal was initiated by Curve founder Mich. AG is also one of the teams that has been maintaining the core codebase since 2020. For this funding round, AG's presented roadmap included continuing to advance llamalend, including support for PT and LP, as well as expansion into on-chain foreign exchange markets and crvUSD. These seem like worthwhile endeavors, but whether they justify a 17M $CRV grant is another calculation. Particularly because Curve's governance differs significantly from Aave's; its power is distributed among several teams with distinct stances.

Let's compare the ve model with conventional governance models:

First, the conclusion: most conventional governance models currently have essentially no design advantages. Of course, if a DAO is mature enough, traditional structures can also function well, but unfortunately, no project in Crypto has yet matured to that level, as evidenced by the problems even at market-consensus leaders like Aave.

So, if we talk specifically about model design, the ve model has some advanced aspects. Firstly, it has cash flow; it is backed by liquidity control rights. When there is external demand for liquidity, this power is "bribed." Therefore, even if you don't want to lock your tokens long-term, you can delegate them to proxy projects like Convex/Yearn to earn收益 (yield).

Thus, the ve model binds voting rights with cash flow. Its future evolution will likely follow the path of "governance capitalism." The vetoken binds voting rights with "long-term locking," essentially筛选 (screening for) those with large capital, the ability to bear liquidity loss, and the capacity for long-term博弈 (game theory). Over time, the result is that governors gradually shift from ordinary users to the "capital class."

Furthermore, due to the existence of proxy layers like Convex/Yearn, many ordinary users, even loyal ones, who wish to gain yield without losing liquidity and flexibility, will increasingly choose to delegate their governance power to these projects.

This vote also reveals some clues. In the future, Mich may not be the main character in Curve's governance; instead, power lies with these large vote holders. When governance issues arose at Aave, some proposed ideas of "delegated governance/elite governance," which is quite similar to the current structure of Curve. As for whether this is good or bad, it will take time to tell.