Author: Xia Fanjie, China Securities Co., Ltd. (CSC)

After the sell-off in broad-based ETFs and the sharp volatility in international gold and silver prices, market sentiment has noticeably cooled. The short-term market faces correction pressure; however, the adjustment space for the All-Share Index is limited, and it is expected to stabilize before the Spring Festival, ushering in a new round of upward movement around the Spring Festival. In terms of sector allocation, we remain optimistic about the dual main themes of "Technology + Resources" in the long term. In the short term, market style rotation is accelerating. Technology sectors that have already experienced corrections, the financial sector, and midstream manufacturing are expected to perform relatively well in the near term. Key sectors to focus on include: Power Equipment (energy storage, UHV, photovoltaics, solid-state batteries, etc.), Non-Bank Finance, Banking, AI (optical communication, storage, etc.), Coal Power, Home Appliances, Automobiles, Steel, etc.

Abstract

Behind the Gold and Silver Turmoil: Profit-Taking in the "Weak Dollar Trade"

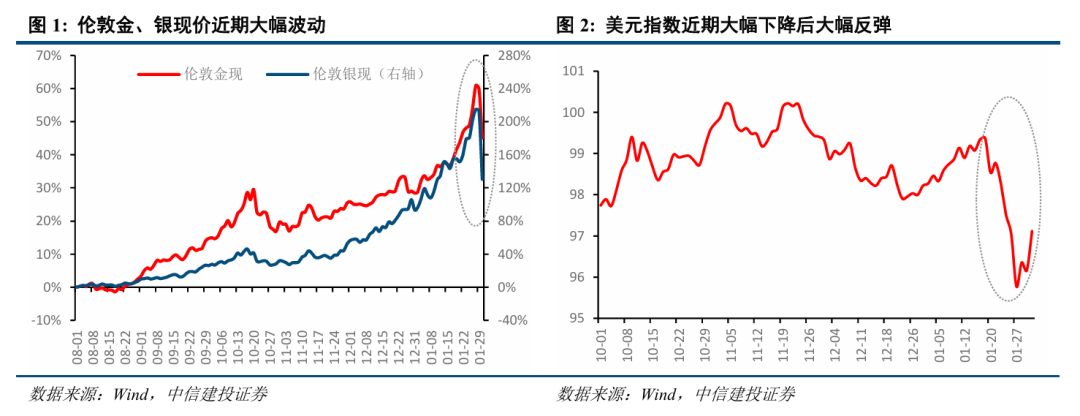

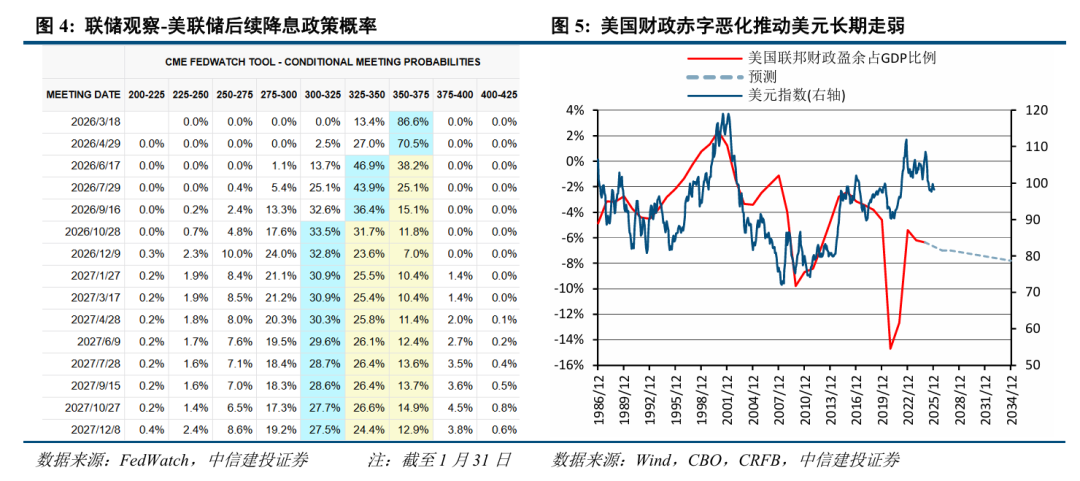

Reasons for the recent sharp volatility in international precious metal prices include the Fed Chair nomination shattering market dovish expectations, short-term profit-taking and leveraged fund stampedes, and silver's strong speculative nature amplifying fluctuations. The next Fed Chair, Warsh, is expected to make "balance sheet reduction and interest rate cuts" the core of policy, potentially leading to a steepening yield curve. Under this expectation, profit-taking occurred in the "weak dollar trade," but overall U.S. stock market volatility was limited. High-growth industries like AI are expected to benefit from subsequent rate cuts, and the financial industry is also likely to benefit.

A-Share View for February: Short-term Correction Pressure, Spring Rally Not Over

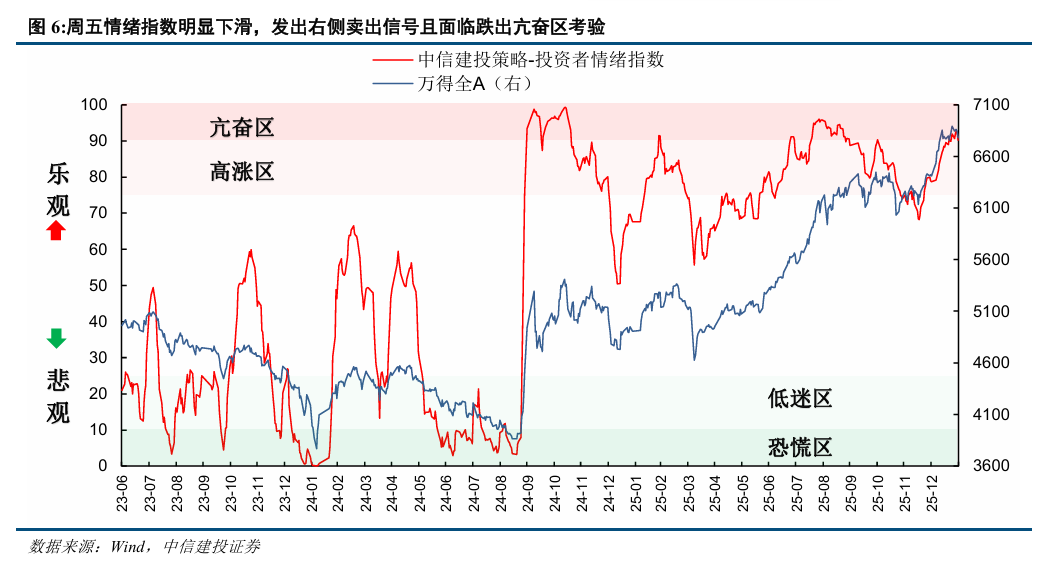

On January 30th, due to sharp volatility in international precious metal prices and recent large-scale selling pressure in A-share broad-based ETFs leading to liquidity stress, the sentiment index showed a significant decline, issuing a right-side sell signal and facing the test of falling out of the exuberance zone. Considering the seasonal effect of rising risk-off sentiment and a declining sentiment index before the Spring Festival, we expect the market to face short-term sentiment cooling and index correction pressure. Comprehensively considering the current market incremental funds and various sub-indicators of the sentiment index, we anticipate limited adjustment space for the All-Share Index, with stabilization expected before the Spring Festival and a new round of upward movement around the Spring Festival.

We are optimistic about the continuation of the Spring rally. Incremental funds in the first quarter are relatively ample. As the broad-based ETF sell-off gradually ends, market incremental funds are expected to improve significantly. Meanwhile, there have been many recent policy positives (new strategic investment system regulations) and industry catalysts (national capacity electricity price policy introduced, frequent highlights in AI large models). Seasonally, February typically has a high win rate and good赚钱效应 (money-making effect).

Long-term Adherence to the "Technology + Resources" Dual Main Theme, Short-term Style Switching Accelerates

We remain optimistic about the "Technology + Resources" dual main theme in the long term. Short-term market style rotation is accelerating. The technology sector has already experienced corrections and will subsequently benefit from the ample liquidity and high risk appetite of the Spring rally. Policy dividends like the strategic investment system, the introduction of the national capacity electricity price policy, and industry catalysts like AI large models will also support the rise of the technology growth style. The financial sector and midstream manufacturing, which have seen significant declines, are also expected to experience a rebound.

Comprehensively considering industry景气 (prosperity), industry catalysts, and external influences, key sectors for recent allocation include: Power Equipment (energy storage, UHV, photovoltaics, solid-state batteries, etc.), Non-Bank Finance, Banking, AI (optical communication, storage, etc.), Coal Power, Home Appliances, Automobiles, Steel, etc.

Behind the Gold and Silver Turmoil: Profit-Taking in the "Weak Dollar Trade"

On Friday, the A-share market experienced significant volatility, with major indices fluctuating over 2%. The Shenzhen Component Index fluctuated by 2.57%, the Shanghai Composite Index by 2.12%, and the Wind All-A Index by 2.34%. The market closed lower overall, with the Shanghai Composite Index, Shenzhen Component Index, and CSI 300 falling by 0.96%, 0.66%, and 1.00% respectively. The core driving factors were the heavy slump in the non-ferrous metals sector triggered by sharp volatility in international precious metal prices, combined with rising risk-off sentiment and the withdrawal of leveraged funds, collectively leading to intensified market fluctuations.

Why have international precious metal prices been so volatile recently? How will this further affect the market? We attempt a brief analysis as follows:

Shift in Expectations, Precious Metals from Soaring to Plunging

We believe the reasons for the recent sharp volatility in international precious metal prices are as follows, with the Fed Chair nomination shattering market dovish expectations being the core reason.

Shift in Fed Policy Expectations Drives Dollar Strength: The U.S. President nominated "hawkish" figure Kevin Warsh as Fed Chair. His policy inclination towards "balance sheet reduction + rate cuts" shattered market dovish expectations, pushing the U.S. dollar index higher rapidly. The attractiveness of dollar-denominated precious metals decreased, directly suppressing prices. Additionally, weakened market expectations for a Fed rate cut in March further reinforced short-term bearish sentiment.

Short-term Profit-Taking and Leveraged Fund Stampede: Precious metal prices surged rapidly in January 2026, with gold accumulating gains of over 30% and silver 60%, technically entering severely overbought territory (gold RSI hit a 40-year peak). Speculative funds that entered early had strong profit-taking需求 (demand), coupled with programmatic stop-loss triggers from leveraged funds, triggering chain selling.

Silver's Strong Speculative Nature Leads to More Violent Fluctuations: Silver, having both financial and industrial attributes, fluctuates more violently. On one hand, demand爆发 (explosion) in areas like photovoltaics, new energy vehicles, and AI data centers, with inventories dropping to a decade low; on the other hand, high prices stimulate industrial技术替代 (technical substitution) (e.g., copper for silver), raising market concerns about demand sustainability, exacerbating price fluctuations. Simultaneously, the silver market is smaller than gold's, not a traditional asset allocation category, with more speculative funds, especially leveraged funds, further加剧 (intensifying) silver price volatility.

Can the "Weak Dollar Trade" Continue?

The recent significant rise in prices of gold, silver, even copper, aluminum, and crude oil is essentially a集中体现 (concentrated manifestation) of the "weak dollar trade." In the long term, it reflects distrust in U.S. fiscal discipline and the dollar monetary system. The medium-term logic stems from the impact of "purchasing Greenland" on the U.S. alliance system and the new动向 (trend) of European capital "selling the U.S." The short term was triggered by the Fed Chair transition and Trump's statement that he is not worried about dollar depreciation. Trump even hinted he could manipulate the dollar exchange rate, saying: "I can make it go up and down like a yo-yo." (News source: First Financial News)

Therefore, we saw the U.S. dollar index accelerate its decline since late January, quickly falling from 99.37 on the 16th to 95.77 on the 27th, the lowest level since March 2022. Global funds eagerly engaged in the "weak dollar trade," going long on precious metals and other physical assets,演绎 (playing out) this long-term trend expected to unfold over decades to its extreme within a week, immediately followed by a backlash.

The turning point came on local time January 30th, when U.S. President Trump finally announced the next Fed Chair nominee: former Fed Governor Kevin Warsh. Warsh has long been known for his hawkish stance but changed his tune last year, echoing Trump's calls for significant rate cuts, which was seen as key to his nomination. For the market, due to Warsh's long-standing hawkish stance, investors believe he is more capable than other Fed Chair candidates of maintaining Fed independence, which significantly changed previous market expectations of a rapid decline in the dollar index. Global "weak dollar trade" quickly took profits, leading to dollar strength and a sharp fall in precious metals.

How Will Warsh Change the Fed?

After a brief period of预期混乱 (expectation confusion), we must focus on a key question: How will Warsh change Fed policy, and what impact will this have on the market?

In 2006, Warsh was nominated by President George W. Bush and served as a Fed Governor, becoming the youngest Governor in Fed history. During his tenure, which coincided with the global financial crisis, he used his previous experience working on Wall Street to help then-Fed Chair Ben Bernanke联系 (contact) Wall Street financial institutions. In 2010, when the Fed launched the second round of quantitative easing (QE), Warsh expressed opposition. He resigned from the Fed in March 2011.

In the 14 years since leaving the Fed, Warsh has become a critic of the institution. He particularly criticized Powell's monetary policy. Warsh's criticisms of the Fed mainly include: First, the Fed's role has become increasingly broad, even venturing into areas of national governance and social value shaping, leading to "mission drift." He believes the Fed's over-expanded role weakens the important and justified claim of "monetary policy independence." Second, since 2008, the Fed has become the largest buyer of U.S. Treasury bonds, with a balance sheet that is too large at $7 trillion, distorting (扭曲) the market. He believes that after the crisis ended, the Fed should "retreat to its original boundaries."

Warsh's Policy Core: Balance Sheet Reduction + Rate Cuts

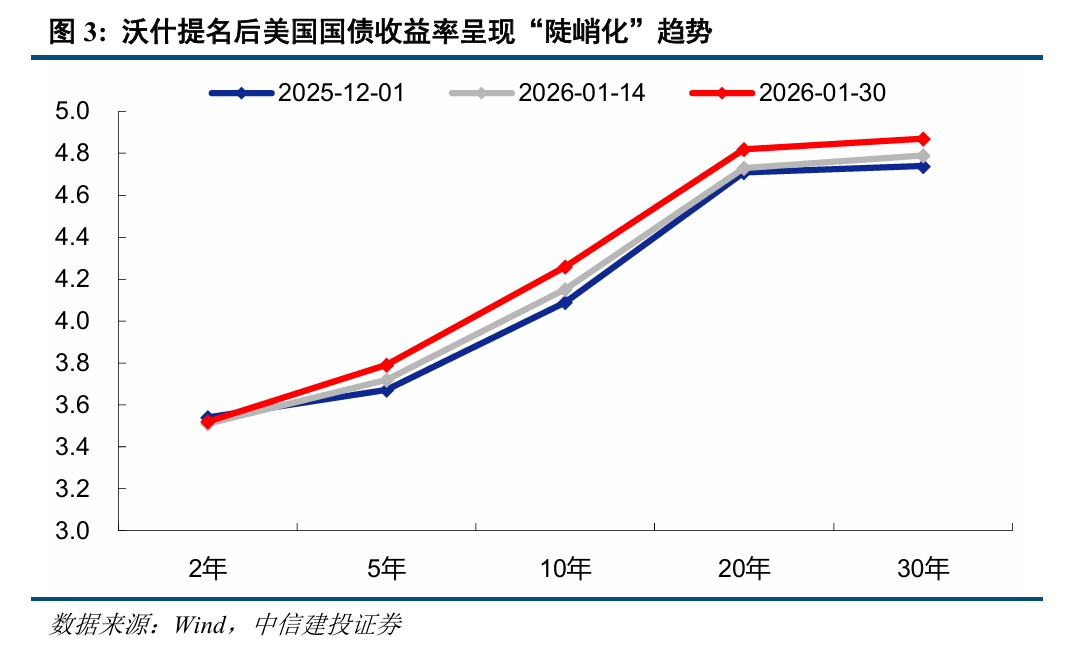

Balance sheet reduction is the core of Warsh's policy. He has明确 (clearly) set reforming the Fed's $6.6 trillion balance sheet as a core goal. Warsh believes the Fed's asset size is too large and should establish a new coordination mechanism with the Treasury to reduce the Fed's direct impact on the money market. This alleviated investor concerns about dollar weakness and also led to the recent sharp decline in non-ferrous metals. If the balance sheet reduction policy is implemented, overseas dollar liquidity may tighten, and the dollar may experience阶段性走强 (periodic strengthening). Additionally, balance sheet reduction will affect the demand for U.S. Treasuries, causing market disturbances. In the long run, balance sheet reduction may eliminate the "Fed put"—the psychological reliance that the Fed will stop tightening and turn to easing (救市 rescue the market) when the market falls sharply. This could allow risk to return to risk itself, meaning risk assets may fall significantly when fundamentals deteriorate. Simultaneously, balance sheet reduction raises long-term interest rates, which could also limit government debt expansion and economic bubbles.

Rate cuts are another major policy direction for Warsh, which would meet Trump's demands and also echo Warsh's recent criticisms of Powell's monetary policy. According to reports around midday Friday, January 30th, Trump stated in his White House office that Warsh would lower rates without White House pressure. Trump said Warsh did not promise him rate cuts, but he "certainly wants to cut rates." However, unlike Trump's goal of大幅降息 (significant rate cuts) to stimulate the economy and boost midterm election prospects, Warsh's rate cut policy is not aimed at stimulating demand but is more supply-side oriented. Its core purpose should be to reduce the burden on various entities, including the government, and encourage productive investment (rather than financial speculation).

Warsh's Policy Impact: Yield Curve Steepening

Unlike the current market's accustomed "flood irrigation" (大水漫灌), Warsh's policy combination of "balance sheet reduction + rate cuts" may lead to yield curve steepening and "liquidity stratification." The main impacts are:

Profit-taking in the "weak dollar trade," panic selling in non-ferrous metals in the short term, and potential limitation of long-term upside space.

Balance sheet reduction is expected to significantly push down U.S. inflation levels.

Funds flow out of junk assets and financial空转 (idling) into实体产业 (real industries). Financing costs rise for highly indebted economies, while economies with high growth potential receive fund青睐 (favor).

Market volatility increases, risk returns.

Although non-ferrous metals fell sharply, overall U.S. stock market fluctuations were limited. High-growth industries like AI are expected to benefit from subsequent rate cut policies.

Yield curve steepening benefits the financial industry (especially banks benefiting from rising net interest margins).

The benefits for technology growth and the financial industry may affect China's A-share and Hong Kong markets through the global linkage of yield curves.

Challenges Facing Warsh:

Warsh still needs approval from the U.S. Senate before officially taking office, which may face some uncertainty, though总体有限 (generally limited).

Warsh needs to simultaneously meet Trump's expectation of Fed obedience to his will and the market's expectation of the Fed maintaining policy independence.

Interest rate decisions are voted on by the 12 members of the monetary policy committee (FOMC). Although the Fed Chair has significant influence, they do not have unilateral decision-making power. Warsh's past public sharp criticisms of Fed leadership may face trust tests among new colleagues.

Warsh has承诺 (promised) to clearly break this tradition—completely rethinking the Fed's asset holdings, policy framework, economic role, and relationship with the executive branch. In fact, to achieve the "balance sheet reduction + rate cuts" policy combination, Warsh also needs to adjust the Fed's current monetary policy rules and monetary policy implementation framework and obtain majority agreement from the members of the monetary policy committee.

Warsh's policy reversed the current weak dollar expectation, which aligns with Bassent's strong dollar policy倾向 (inclination) (and also aligns with Wall Street interests given both their Wall Street backgrounds), but seems to背离 (deviate from) Trump's weak dollar policy.

Need to assess the impact of Trump reshaping the global trade landscape, judge the profound changes人工智能 (AI) brings to productivity and the labor market, and simultaneously respond to the冲击 (impact) the rise of digital assets may have on the banking regulatory system.

A-Share View for February: Short-term Correction Pressure, Spring Rally Not Over

Sentiment Cooling Issues Right-Side Sell Signal, Market Faces Short-term Correction Pressure

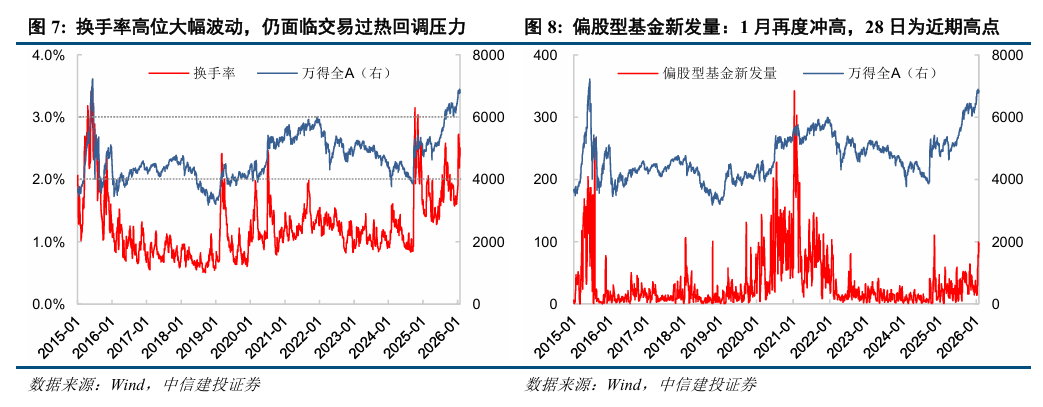

Our constructed and continuously tracked investor sentiment index shows: Market sentiment升温 (warmed up) rapidly after the New Year, quickly rising from below 80 at the end of last year to above 88 mid-month. The "stability as the priority" policy orientation, while抑制 (curbing) the "crazy rise" trend in stock prices, still showed高涨 (high) investor sentiment through ample incremental funds. The Wind All-A Index also remained high. By January 20th, the sentiment index broke through 90 again into the exuberance zone,之后 (after which) it basically fluctuated narrowly in the 90-93 range, reflecting the tug-of-war between the market's internal impulse for "accelerating冲刺顶峰 (rushing to the peak)" and regulatory "active降温 (cooling)." On January 30th, due to sharp volatility in international precious metal prices and recent large-scale selling pressure in A-share broad-based ETFs leading to liquidity stress, the sentiment index showed a significant decline, issuing a right-side sell signal and facing the test of falling out of the exuberance zone. Considering the seasonal effect of rising risk-off sentiment and a declining sentiment index before the Spring Festival, we expect the market to face short-term sentiment cooling and index correction pressure.

Some sentiment sub-indicators also提示 (indicate) short-term market correction pressure. For example, the turnover rate continues to fluctuate at highs above 2%, indicating the current market is still overheated in trading, suggesting a high possibility of subsequent correction. Equity fund issuance also surged again recently, reaching a recent high on the 28th; this indicator often corresponds to阶段性高点 (stage highs) in the market. However, other sub-indicators reflecting market strength/weakness levels, such as above MA60 and overbought/oversold, have already fallen from highs, indicating limited overall subsequent A-share adjustment pressure. (Details in "Active Cooling After the New Year Surge, What's the Market Sentiment? — Market Sentiment Tracking January Report")

Comprehensively considering the current market incremental funds and various sub-indicators of the sentiment index, we anticipate limited adjustment space for the All-Share Index, with stabilization expected before the Spring Festival and a new round of upward movement around the Spring Festival.

Will the Broad-Based ETF Sell-off Continue?

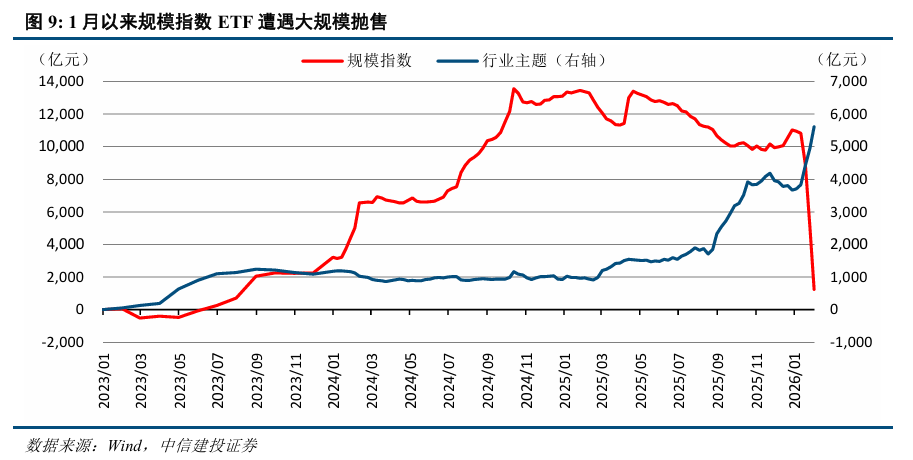

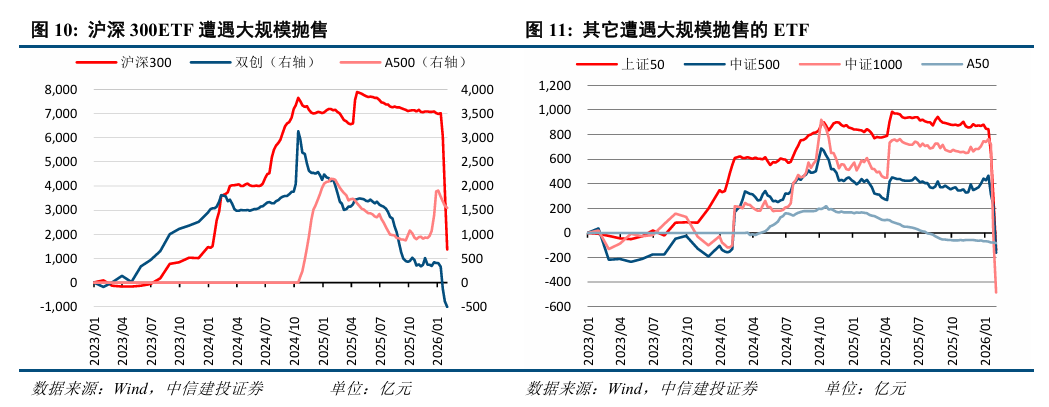

On January 15th, the China Securities Regulatory Commission (CSRC) held its 2026 System Work Conference, proposing "Adhere to stability as the priority, timely conduct countercyclical adjustment." Subsequently, major broad-market index ETFs experienced large-scale sell-offs,抑制 (curbing) the market's upward冲刺顶峰 (rush to the peak) momentum, and market sentiment gradually cooled. According to our monitoring of major market ETF products, recent selling focused on CSI 300, CSI 1000, SSE 50, and CSI 500 ETFs. STAR Market 50 and ChiNext ETFs also experienced small-scale selling.

If we focus on the recent动向 (movements) of ETFs held by Central Huijin, we can see that approximately 53-66% of the CSI 300 ETF shares held by Huijin recently (January 15-29) decreased, about 73-91% of the CSI 1000 ETF shares held by Huijin decreased, and the reduction比例 (proportion) for the SSE STAR Market 50 ETF甚至高达 (even reached) 94%. The estimated capital outflow scale is about 913.4 billion yuan.

Will the broad-based ETF sell-off continue? We believe the scale of broad-based ETF selling next week is expected to decrease significantly or even stop completely. The reasons are: 1) According to our monitoring data, market sentiment has明显降温 (noticeably cooled), and the previous ETF selling's effect on tightening market liquidity has begun to show; 2) The sharp volatility in international gold and silver prices, the阶段性转折 (stage turning point) in global weak dollar expectations, rising market risk-off and wait-and-see sentiment, coupled with the approaching Spring Festival, further increasing capital risk-off意愿 (willingness), means continued cooling is no longer necessary; 3) Huijin's ETF scale has already been reduced by about 60%, and a certain scale of ETFs仍需保留 (still needs to be retained) as subsequent调控工具 (regulation tools). Therefore, for the A-share market, although it still faces short-term sentiment cooling and correction pressure,随着 (as) ETF selling stops, the market is expected to stabilize and accumulate energy for the next upward move.

Optimistic About the Continuation of the Spring Rally

Although facing correction pressure in the short term, we are still optimistic about the continuation of the Spring rally for three reasons:

Ample Incremental Funds: In the earlier in-depth专题 (special report) "资金护航, 景气为纲 — 2026年A股资金面展望(下)" (Funds Escort, Prosperity as the Guideline — 2026 A-Share Capital Outlook (Part 2)), we pointed out that this year will see a wave of time deposit maturities, with about 45 trillion yuan in time deposits集中到期 (concentrated maturing), especially in the first quarter, making it the time点 (point) with the most ample incremental funds for the year. As the broad-based ETF sell-off gradually ends, market incremental funds are expected to improve significantly.

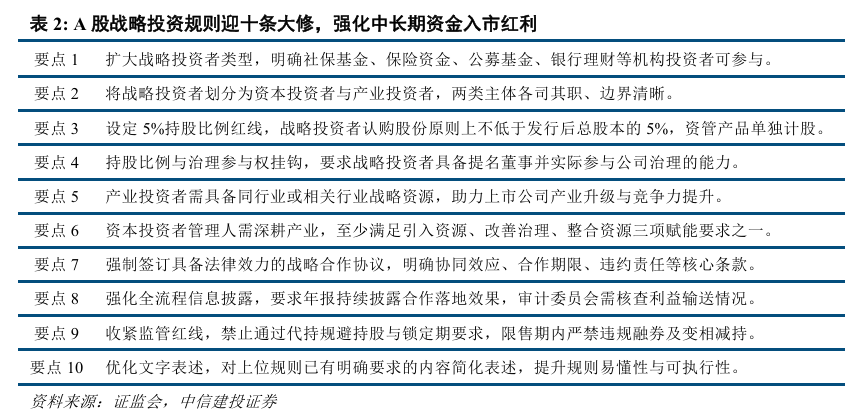

Many Policy Positives and Industry Catalysts: On January 30th, the CSRC solicited public opinions on amendments to the "Securities and Futures Law Applicability Opinion No. 18". This revision本质上 (essentially) is a systematic improvement of the strategic investment system. By clarifying the scope of subjects, shareholding requirements, empowerment responsibilities, disclosure obligations, and regulatory bottom lines, it opens channels for medium-to-long-term funds to enter the market while preventing system abuse through strict regulation. The new system is a major positive for attracting medium-to-long-term funds to deeply participate in listed company operations and industrial upgrade, is expected to activate A-share M&A and restructuring, and boost market risk appetite. Additionally, the national capacity electricity price policy was introduced, completing the final piece of the energy storage puzzle. Recent AI large model热点频出 (hot topics frequent): Silicon Valley's Clawdbot became popular from overseas to domestic, becoming the most notable AI爆款 (blockbuster) at the beginning of 2026. Domestic AI large models like DeepSeek-OCR2, Kimi K2.5, Alibaba's Qwen3-Max-Thinking, etc.,纷纷放出大招 (released major moves one after another).

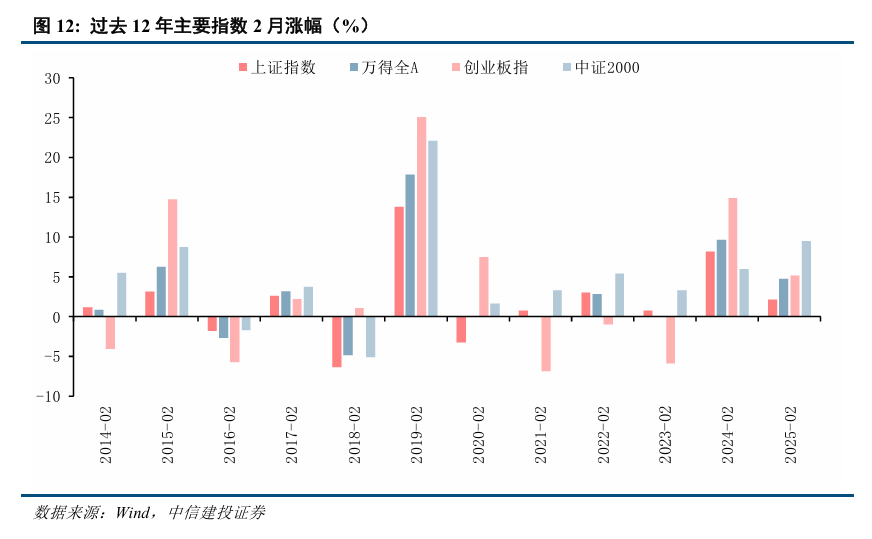

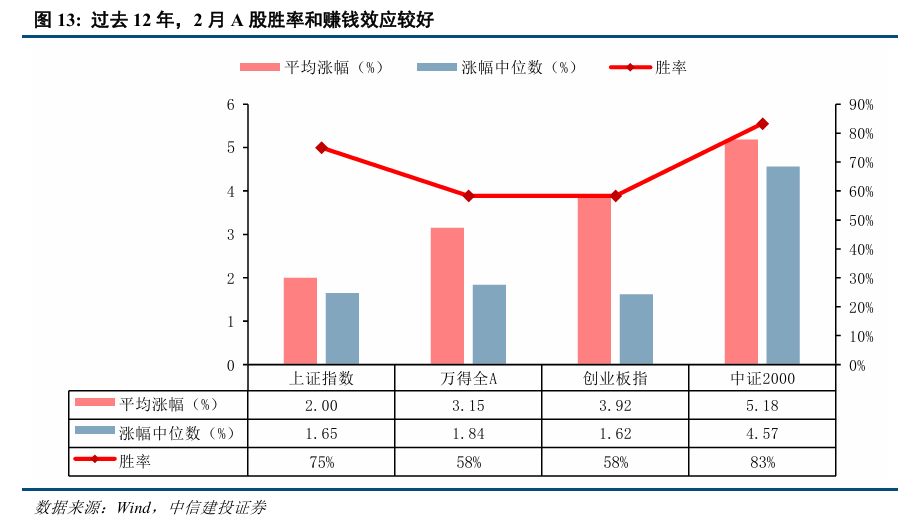

Seasonally, February Typically Has High Win Rate, Good Money-Making Effect: We统计 (statistics) of the February performance of major indices over the past 12 years show that the win rates for the Shanghai Composite Index and CSI 2000 in February are 75% and 83% respectively. The win rates for the Wind All-A Index and ChiNext Index also reached 58%. In terms of average gains, small and mid-cap styles and technology growth styles outperform. The average gains for the CSI 2000 and ChiNext Index are 5.18% and 3.92% respectively. The average gains for the Shanghai Composite Index and Wind All-A Index also reach 2.00% and 3.15%. Overall, February, as a key period for the Spring rally (post-Spring Festival, pre-Two Sessions), often sees高涨 (high) investor enthusiasm for going long. Combined with the current bull market atmosphere, the market is expected to usher in a new round of upward movement after the Spring Festival.

Long-term Adherence to the "Technology + Resources" Dual Main Theme, Short-term Style Switching Accelerates

In our November 2026 A-Share Strategy Outlook "Slow Bull New Journey: Game the Present, Layout the Future," we stated that 2026 A-shares enter a key period of景气验证 (prosperity verification), with intensified industry style rotation. We were optimistic about the technology growth main theme, while resources were likely to become a new main theme direction after technology. Recently, the "Technology + Resources" dual main theme characteristic has been obvious, with style rotation accelerating: From late December, technology sectors represented by commercial aerospace strengthened rapidly, leading the A-shares;随着 (As) the CSRC's "countercyclical adjustment," technology热点 (hot spots) adjusted, and funds turned to cyclical products represented by non-ferrous metals and chemicals. Sectors like home appliances, automobiles, and photovoltaics fell significantly amid concerns about rising raw material costs; however, with the recent sharp volatility in international precious metal prices, funds turned back to the technology growth style on Friday, and cyclical sectors experienced a sharp decline. Looking ahead, we continue to be optimistic about the long-term performance of the "Technology + Resources" dual main themes. Short-term fund flows are simultaneously affected by景气 (prosperity) (e.g., annual report performance previews), industry catalysts, and the external environment.

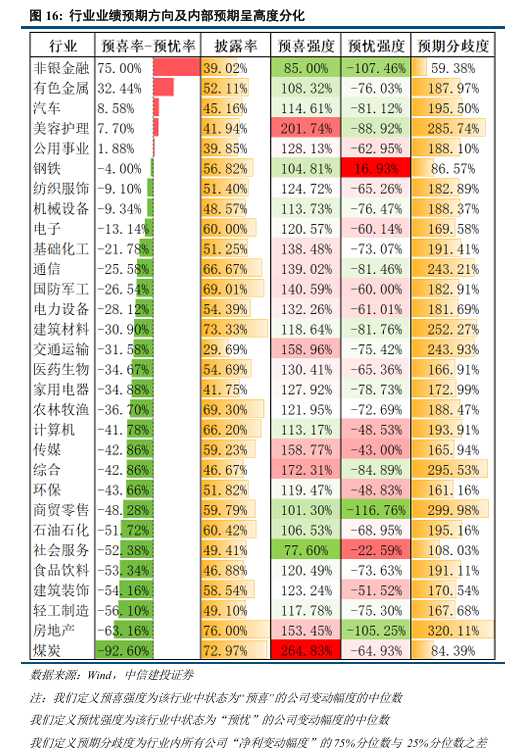

Annual Report Performance Preview Situation: Significant Industry Divergence, High景气度 (Prosperity) in Non-Bank Finance, Non-Ferrous Metals, Automobiles

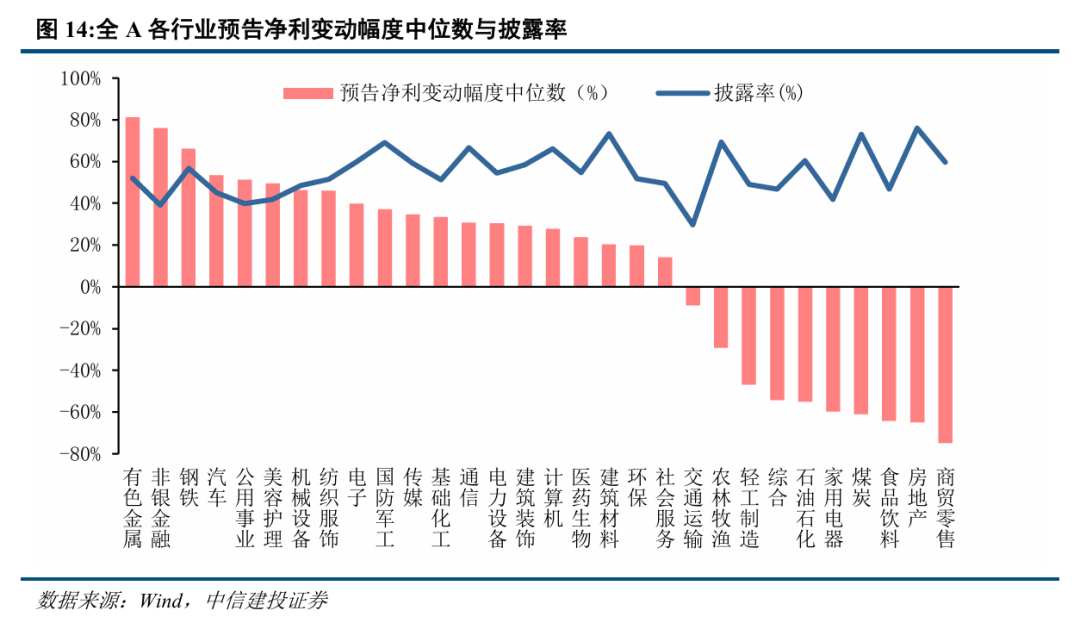

As of January 31, 2026, the disclosure of 2025 annual report performance previews for A-share listed companies is basically complete. Judging from the overall performance of the currently disclosed samples, the median change in预告净利润 (previewed net profit) for all A-shares reached 29%, showing a温和修复 (moderate recovery) in corporate profitability. In terms of profit scale, if the arithmetic average of the upper and lower limits of the previewed net profit is used to estimate the current period's归母净利润 (net profit attributable to parent company), the average profit scale of the disclosed companies is about 52.3 million yuan. The data indicates that although the macro environment remains challenging, the profit中枢 (center) has shown an improving trend.

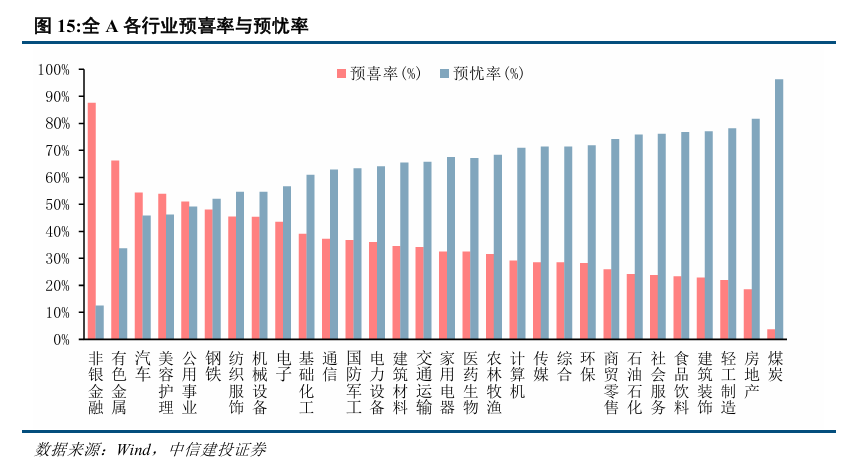

Industry景气 (prosperity) shows significant divergence, with resources and finance leading while domestic demand承压 (under pressure). The distribution of业绩修正 (earnings revisions) and growth industries shows obvious aggregation effects: The non-ferrous metals industry leads the entire industry with a median previewed net profit change of 81%, and its预喜率 (positive预告 rate) is as high as 66%, reflecting the strong溢价能力 (pricing power) of upstream resources amidst price fluctuations. The non-bank financial industry follows closely, with a median previewed net profit change of 76%, and its预喜率 reaches an absolute high of 88%, confirming the positive boost from the capital market回暖 (recovery) on asset allocation and related business profits. In contrast, the real estate, commercial retail, and food and beverage industries have median previewed net profit changes of -60% or below, and their预忧率 (negative预告 rate)均超过 (all exceed) 70%, indicating that consumption-side and traditional industries like real estate still await修复 (recovery).

Overall, non-ferrous metals, non-bank finance, steel, automobiles, public utilities, beauty care, machinery equipment, and textiles & apparel have the highest median net profit change, all exceeding 45%, with non-ferrous metals, non-bank finance, steel, and public utilities exceeding market expectations较多 (by a lot). Technology industries like electronics, communications, computers, media, power equipment, and pharmaceuticals also have median net profit changes exceeding 23%, continuing their rapid growth trend.

Performance Confirms Market Main Themes, Sector Leaders Have Their Own Highlights.

Industry expectations are明显异质性 (clearly heterogeneous). Prosperous directions combine high growth with low divergence, while pressured areas face deep adjustments and预期混沌 (expectation chaos). Observing the overall bias and internal structure of each industry's performance previews, each industry has its own characteristics under the overall业绩预期方向 (earnings expectation direction). Industries like non-bank finance and non-ferrous metals not only have significant net optimistic expectations, but the median previewed net profit growth for their预喜 companies also reaches 85% and 108% respectively, while the预期分歧度 (expectation divergence degree) is at relatively low levels of 59% and 188%, indicating their optimistic expectations have strong profit support and internal consensus. On the other hand, most industries show net pessimistic expectations, with real estate and coal having the deepest net pessimism. Notably, the internal structures of some net pessimistic industries differ significantly: For example, the national defense军工 (military industry) and power equipment industries have relatively温和 (moderate) median净利润调整 (net profit adjustments) for their预忧 companies, and expectation divergence is lower than many other net pessimistic industries; although the steel industry's overall expectations are not optimistic,预忧企业 (companies with negative previews) show strong net profit increases, indicating a盈利修复势头 (profit recovery momentum); while industries like commercial retail and real estate face both deep net profit adjustments and extremely high expectation divergence.

Industry Catalysts: New Energy, AI Welcome Positive News

National Capacity Electricity Price Policy Introduced, Power System Takes Key Step Towards High-Proportion New Energy Transition

The National Development and Reform Commission (NDRC) and the National Energy Administration (NEA) recently jointly issued the "Notice on Improving the Generation-Side Capacity Electricity Price Mechanism," formally introducing the national capacity electricity price policy. We believe this marks the transition of China's electricity market from a "single energy pricing" system to a multi-dimensional value system of "energy + capacity + auxiliary services." The policy, by clarifying the capacity compensation mechanism for调节性电源 (adjustable power sources) like coal power and new energy storage, not only guarantees the recovery of fixed costs for traditional power sources but also, for the first time at the national level, establishes the system value of new energy storage, providing a stable income source for the energy storage industry and taking a key step towards a high-proportion new energy transition for the power system.

Energy Storage Industry Accelerates Expansion: The national unified capacity mechanism breaks local pilot differences. Domestic energy storage industry chain demand in 2026 is expected to experience爆发 (an explosion), with leading companies particularly benefiting from growing long-duration energy storage demand.

Power System Value Restructuring: The policy首次 (for the first time) prices "reliable capacity" as an independent commodity. The capacity electricity price provides safety assurance for high-proportion new energy grid integration and will promote the协同发展 (synergistic development) of new energy and adjustable resources.

Coal Power Transformation Deepens: The capacity electricity price guides coal power from "base load operation" to "peak shaving and frequency regulation," increasing demand for unit flexibility改造 (retrofitting). Thermal power companies with location advantages see enhanced profit stability.

AI Large Models Have Frequent Highlights

The AI large model field recently exhibits a dual-drive characteristic of "technological architecture innovation and accelerated scenario落地 (landing)." Internationally, Clawdbot (later renamed Moltbot) redefined the AI Agent form with a "local-first +反向控制 (reverse control)" architecture; domestically, Alibaba's Qwen3-Max-Thinking achieved推理性能跃升 (reasoning performance leap) with trillion参数规模 (parameter scale) and test-time extension technology,性能媲美 (performance comparable to) GPT-5.2 and Gemini 3 Pro; DeepSeek-OCR2 broke through complex document understanding bottlenecks through a因果流查询机制 (causal flow query mechanism); Kimi K2.5 enhanced long-text processing and Agent集群协作 (cluster collaboration) capabilities. Overall, lightweight, localization, and scenarioization become the main lines of technological evolution. The open-source ecosystem and commercial落地 form a positive循环 (cycle), pushing AI from "dialogue interaction" to "autonomous action."

External Influence: "Weak Dollar Trade" Pauses, Which Sectors Benefit?

With Warsh's nomination as the new Fed Chair, profit-taking occurred in the "weak dollar trade," the U.S. dollar index rose, and the yield curve steepened. Which sectors benefit the most?

Finance (Banks): If Warsh's policy combination of "balance sheet reduction + rate cuts" is implemented, it will steepen the U.S. Treasury yield curve and also affect global yield curves. For A-shares and Hong Kong stocks, the financial sector, especially banks, will benefit from rising net interest margins, improving profit expectations.

Midstream Manufacturing (Home Appliances, Automobiles, Photovoltaics): Recently, midstream manufacturing sectors like home appliances, automobiles, and photovoltaics have all seen significant declines. One possible reason is investor concern that upstream raw material prices (e.g., copper, silver) rose大幅度 (sharply) without significant improvement in downstream demand, impacting sector毛利率 (gross profit margins). With the sharp decline in the non-ferrous metals sector on Friday, this concern is expected to significantly ease, benefiting the return of related sector stock prices to reasonable levels.

Overall, we remain optimistic about the "Technology + Resources" dual main theme in the long term. Short-term market style rotation is accelerating. The technology sector has already experienced corrections and will subsequently benefit from the ample liquidity and high risk appetite of the Spring rally. Policy dividends like the strategic investment system, the introduction of the national capacity electricity price policy, and industry catalysts like AI large models will also support the rise of the technology growth style. The financial sector and midstream manufacturing, which have seen significant declines, are also expected to experience a rebound. Comprehensively considering industry景气 (prosperity), industry catalysts, and external influences, key sectors for recent allocation include: Power Equipment (energy storage, UHV, photovoltaics, solid-state batteries, etc.), Non-Bank Finance, Banking, AI (optical communication, storage, etc.), Coal Power, Home Appliances, Automobiles, Steel, etc.

Domestic Demand Support Policy Effects Lower Than Expected. If subsequent domestic real estate sales, investment, and other data are slow to recover, inflation remains低迷 (sluggish), consumption does not see a significant boost, and corporate profit growth continues to decline, ultimately disproving economic recovery, then the overall market trend will face pressure, and overly optimistic pricing expectations will face修正 (correction).

Sino-US Strategic Game Intensification Risk. Be vigilant against the risk of the Sino-US strategic game expanding in scope and intensifying. For example, strategic博弈 (game) spreading from trade to technology, critical resources, finance, shipping, logistics, military, and other areas, leading to全方位战略冲突 (comprehensive strategic conflict), which could affect normal economic activities and simultaneously impact the equity market.

U.S. Stock Market Volatility Exceeds Expectations. If the U.S. economy deteriorates beyond expectations, or the Fed's easing efforts fall short of expectations, it could lead to significant fluctuations in the U.S. stock market, which would also have spillover effects on domestic market sentiment and risk appetite.