Crypto heads into the week of March 2 with five clear catalysts on deck: a worsening US-Iran conflict under President Donald Trump, a privacy-focused Bitcoin wrapper from Starknet, Polygon’s March 4 agentic-payments gas upgrade, Avalanche’s new incentive round, and Friday’s US jobs report.

Crypto Watchlist For This Week

Bitcoin is still the biggest macro watch this week, but the setup has already changed. The initial war shock over the weekend pushed BTC down toward $63,000, yet that move did not hold. The token rebounded as high as $68,196 on Sunday and was back around $65,807 by European Monday morning, while broader reporting showed traders were already reassessing whether the conflict would become a lasting macro shock or a violent but temporary headline event.

Oil followed a similar pattern: Brent briefly surged to $82.37 before giving back part of the move and easing back into the upper-$70s, which matters because crypto traders are now watching inflation risk and rate expectations more than the initial geopolitical headline itself.

What matters now is not simply that Washington and Tehran are in open conflict, but that the political signals are mixed. Trump has said he is willing to talk to Iran’s “new leadership,” while the White House has also made clear that military operations are continuing.

At the same time, AP’s live coverage says Iranian leaders are publicly rejecting negotiations. For markets, that creates a more nuanced watch item than a straight risk-off story: if diplomacy starts to look credible and oil keeps fading from its highs, Bitcoin’s rebound may hold; if the war widens and energy markets tighten again, crypto is likely to trade under macro pressure first and narrative second.

On the product side, Starknet is preparing to roll out strkBTC, a wrapped Bitcoin asset issued on Starknet and redeemable for native BTC, with optional shielding for balances and transfers. The design matters because Starknet is not pitching privacy as mandatory. In its own words, “Privacy is available when needed. Transparency remains available when required for compliance.”

Polygon’s catalyst lands on March 4, when the Lisovo/LisovoPro hardfork is scheduled around block 83,756,500, with implementation of PIP-82 included in the release. The proposal would recycle up to $1 million in gas base fees spent on agentic-commerce transactions, a direct subsidy aimed at machine-to-machine payments. Polygon’s own proposal says the chain has attracted 20.3% of x402 transactions and 10.4% of total volume since the start of the year.

Avalanche’s watch item is the Retro9000 C-Chain Round, which starts on March 2 and draws from the Foundation’s $40 million Retro9000 funding pool. The key shift is methodological. Avalanche says the program is moving from rewarding who built to rewarding what gets used, with projects ranked by AVAX burned through smart-contract activity and the top 40 becoming eligible for rewards.

The cleanest scheduled macro event arrives on Friday, March 6, when the Bureau of Labor Statistics releases the February US employment report at 8:30 a.m. ET. Reuters expects payroll growth of 60,000 after January’s 130,000 gain, making the release an important test of whether the prior month was a false signal or the start of a firmer labor backdrop. For crypto, that report matters because it can quickly reset rate-cut expectations just as markets are trying to price geopolitical stress.

This leaves crypto focused mainly on macro. If Middle East risk keeps oil, the dollar and broader risk sentiment in motion, Bitcoin and the wider altcoin market could remain exposed to sharp headline-driven swings. But if US-Iran tensions cool, Friday’s jobs report may become the next major trigger, with markets likely to judge it through one question above all: whether it strengthens or weakens the case for Fed easing.

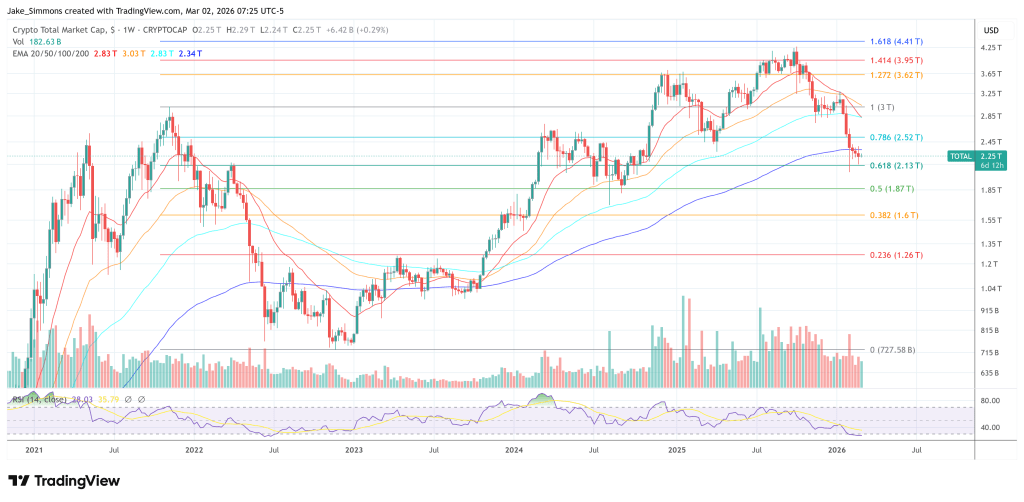

At press time, the total crypto market cap stood at $2.25 trillion.