A White House meeting aimed at breaking the logjam over stablecoin rewards under pending crypto market structure legislation aka Clarity Act ended without a compromise, even as both banking and crypto participants described the session as “productive,” according to details shared by Crypto In America reporter Eleanor Terrett citing sources in the room.

The follow-up gathering, smaller than the first meeting last week, zoomed in on what has become the most combustible line item in the Clarity Act debate: whether, and under what constraints, crypto firms can offer “rewards” tied to stablecoin usage. The White House urged both sides to reach a deal by March 1, Terrett reported, though it remains unclear whether another meeting of this scale will occur before the end of the month.

Crypto Clarity Act Update

Terrett said banks and banking trade groups came prepared with a written handout titled “Yield and Interest Prohibition Principles,” framing “payment stablecoins” as payment instruments and pushing for a bright-line ban on consideration paid to holders.

“In the GENIUS Act, Congress specifically designed payment stablecoins to be payment instruments,” the document states. “Consistent with this design, market structure legislation should incorporate the following yield and interest prohibition principles to limit deposit outflows that reduce the availability of credit for communities.”

The handout’s core demand is sweeping: “No person may provide any form of financial or non-financial consideration to a payment stablecoin holder in connection with the payment stablecoin holder’s purchase, use, ownership, possession, custody, holding, or retention of a payment stablecoin.” It pairs that with a call for regulator enforcement authority and civil monetary penalties, anti-evasion language, and strict marketing and disclosure rules that would bar firms from implying rewards are “interest,” “risk-free,” or comparable to insured deposits.

One source highlighted a narrow shift in bank posture: the inclusion of “any proposed exemptions” language, which Terrett said was viewed as a concession because banks had previously been unwilling to discuss exemptions “with respect to offering rewards on a transaction-based basis at all.” Even so, the handout insists exemptions must be “extremely limited in scope” and must not “drive deposit flight that would undercut Main Street lending.”

Terrett reported that a major share of the discussion centered on “permissible activities”: the types of account behavior that could qualify a crypto firm to offer rewards. Crypto representatives want those definitions broad; banks want them narrowed. That framing captures the heart of the dispute: whether rewards can be designed as functional incentives for payments activity, or whether any such consideration is inherently deposit-like and therefore destabilizing for traditional funding models.

Ripple Chief Legal Officer Stuart Alderoty struck an optimistic tone after the session, writing via X: “Productive session at the White House today – compromise is in the air. Clear, bipartisan momentum remains behind sensible crypto market structure legislation. We should move now – while the window is still open – and deliver a real win for consumers and America.”

Dan Spuller, EVP of the Blockchain Association, described the meeting as a shift from general debate to “serious problem-solving,” while underscoring the gap that remains. “Stablecoin rewards were front and center,” he wrote. “Banks did not come to negotiate from the bill text, instead arriving with broad prohibitive principles, which remains a key disagreement.”

The meeting was led by Patrick Witt, Executive Director of the President’s Crypto Council, and included Senate Banking Committee staff, Terrett reported. Crypto-side attendees included Coinbase’s Paul Grewal, a16z’s Miles Jennings, Ripple’s Alderoty, Paxos’s Josh Rosner, Blockchain Association CEO Summer Mersinger, and Ji Kim of the Crypto Council. Banks represented included Goldman Sachs, JPMorgan, Bank of America, Wells Fargo, Citi, PNC Bank, and U.S. Bank, alongside trade groups including the Bank Policy Institute, the American Bankers Association, and ICBA.

Mersinger said the continued convenings signal momentum even without a deal. “Today’s second White House meeting reflects continued, meaningful momentum toward delivering bipartisan digital asset market structure legislation, and we’re encouraged by the progress being made as stakeholders remain constructively engaged on resolving outstanding issues,” she said. “We’re thankful to Patrick Witt and the Administration for their continued leadership and commitment to keeping this process moving forward.”

For now, the White House appears to be applying time pressure rather than dictating terms. Further discussions are expected “in the coming days,” Terrett reported, setting up a race to define “permissible activities” narrowly enough to satisfy banks, but broadly enough for crypto firms to preserve rewards as a competitive product feature before the March 1 target date.

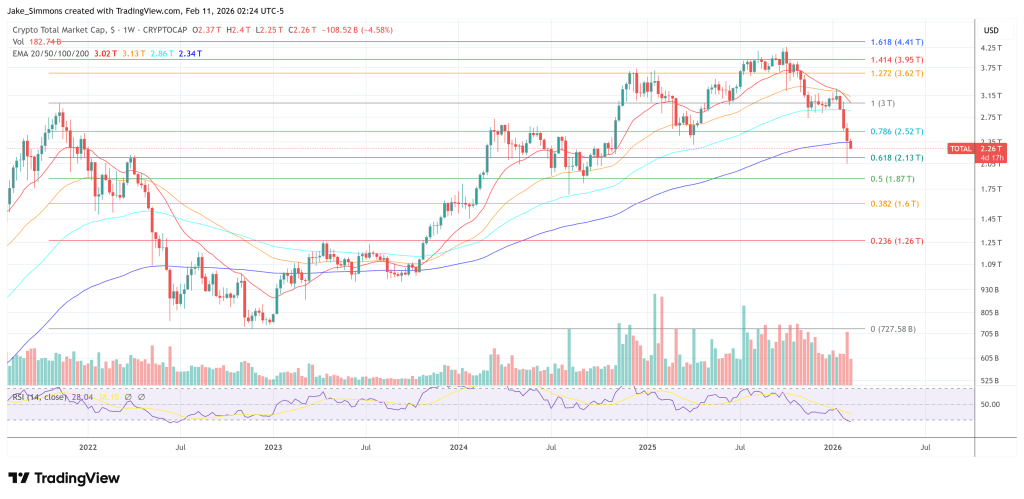

At press time, the total crypto market cap stood at $2.26 trillion.