Author: Liu Honglin, Mankun Blockchain

The State Council has promulgated the "State Council Regulations on Outbound Investment," which will take effect from July 1, 2026.

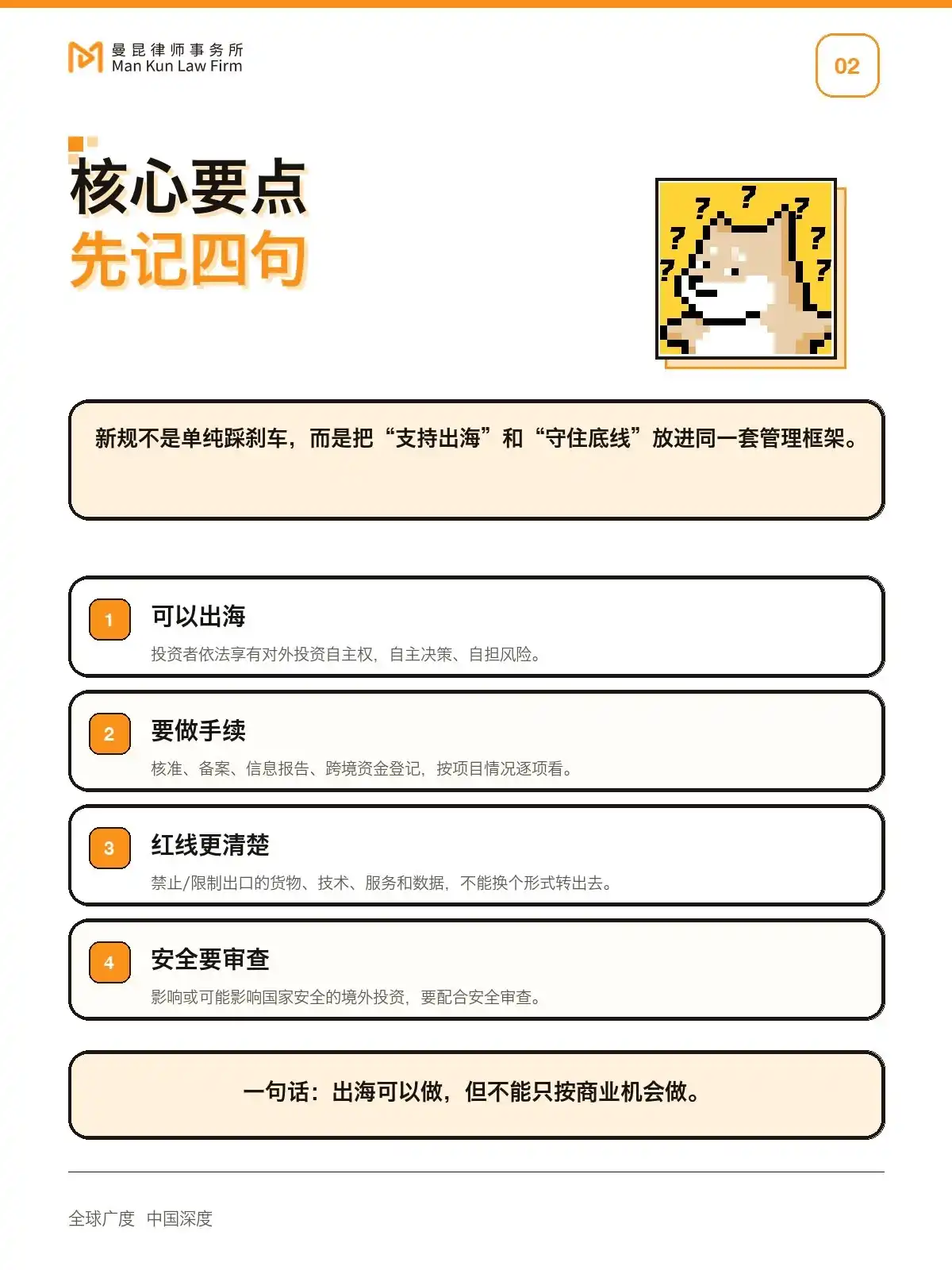

This is not simply a matter of "cannot go overseas."

More accurately, it serves as a reminder to enterprises and individuals: outbound investment must follow rules.

To understand this new regulation, keep the following points in mind first:

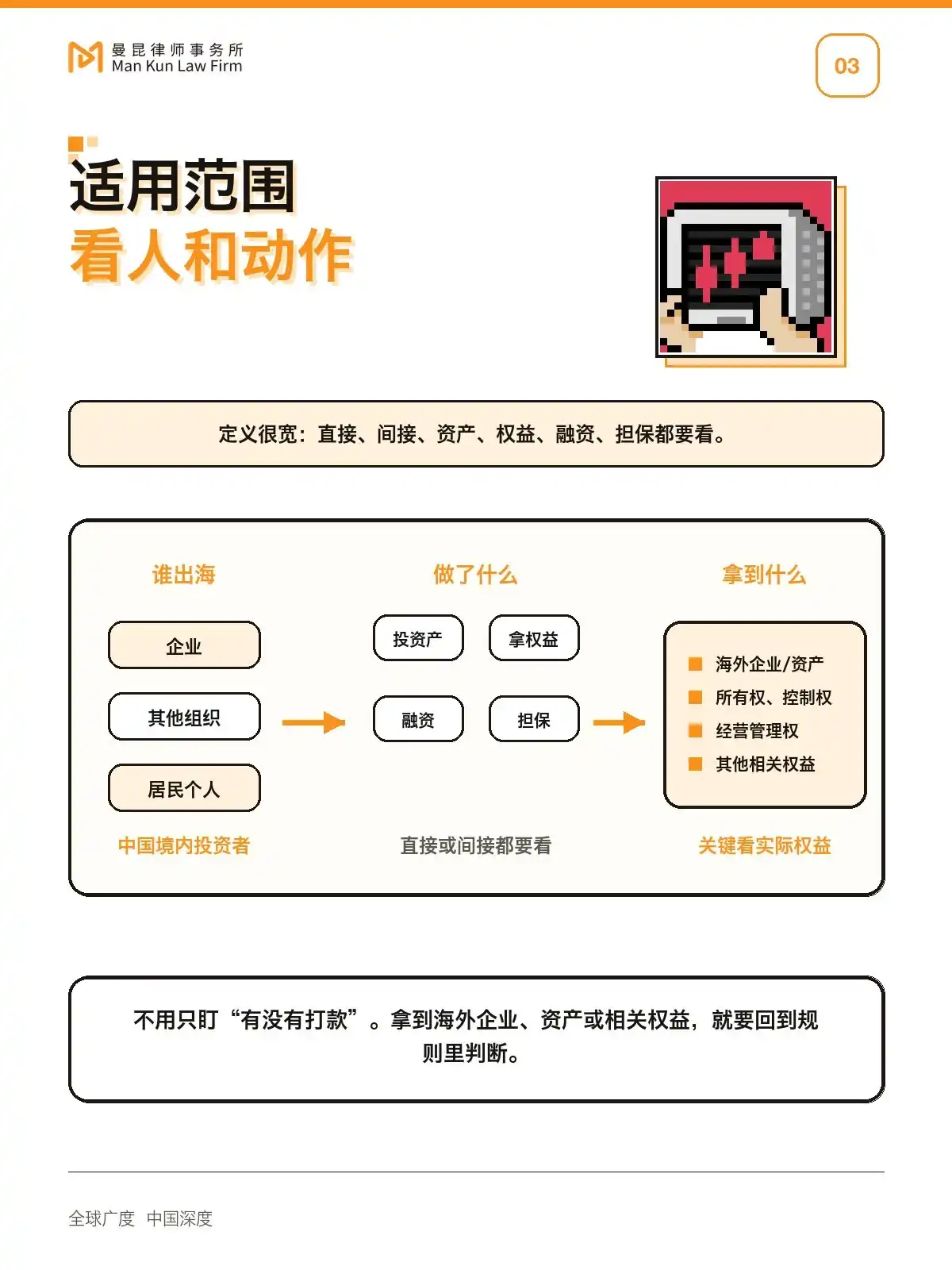

1️⃣ It's not just enterprises that are regulated. The scope of investors includes domestic enterprises, other organizations, and resident individuals.

2️⃣ It's not just about transferring money. Acquiring assets, obtaining equity rights, providing financing or guarantees, and directly or indirectly acquiring rights and interests related to overseas enterprises or assets all require assessment.

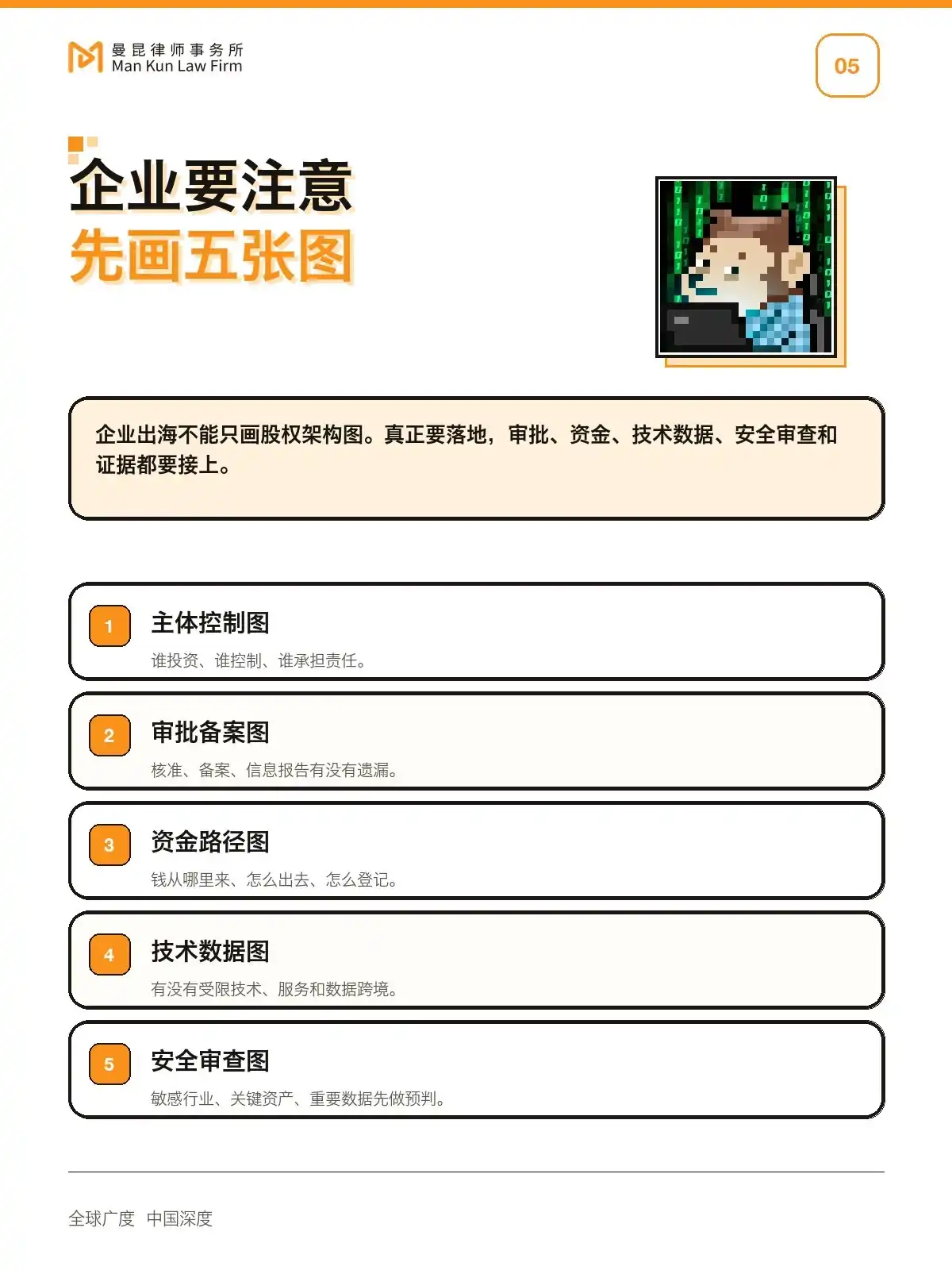

3️⃣ Enterprises shouldn't just draw equity structure charts. They also need to clearly chart the entities, approval/filing procedures, fund flow paths, technology, data, and security reviews.

4" Individuals shouldn't just look at returns. First, consider whether you are eligible to invest, how the funds will go out, what you are actually buying, and whom to turn to if something goes wrong.

5️⃣ The price of non-compliance is not light. Beyond fines, there may be restrictions on continuing outbound investment activities.

In a nutshell: Outbound investment is not prohibited, but it cannot be pursued solely based on commercial opportunities.

The above is for general information sharing only and does not constitute legal advice or investment recommendations.