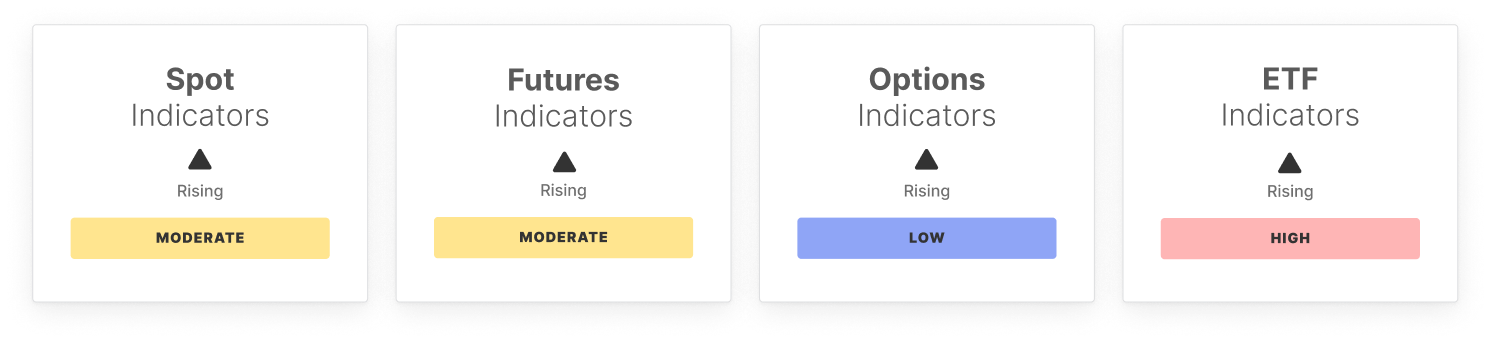

Spot conditions show early signs of improvement. Trading volume has lifted modestly, while the net buy–sell imbalance has broken above its upper statistical band, signalling a clear reduction in sell-side pressure. Despite this, spot demand remains fragile and uneven.

Derivatives positioning is mixed. Futures open interest has edged higher, reflecting a cautious rebuild in speculative engagement, while funding rates have cooled sharply, indicating reduced long-side urgency. Perpetual CVD remains negative, highlighting ongoing sell-side activity in leveraged markets.

Options markets continue to price elevated uncertainty. Options open interest has risen, while the volatility spread sits near the upper end of its historical range, signalling implied volatility remains elevated relative to realised levels. Downside protection demand remains persistent.

US spot ETF flows have reversed sharply into strong inflows, moving beyond statistical extremes and signalling renewed institutional accumulation. ETF trading volumes have risen alongside this shift, though elevated holder profitability raises near-term profit-taking risk.

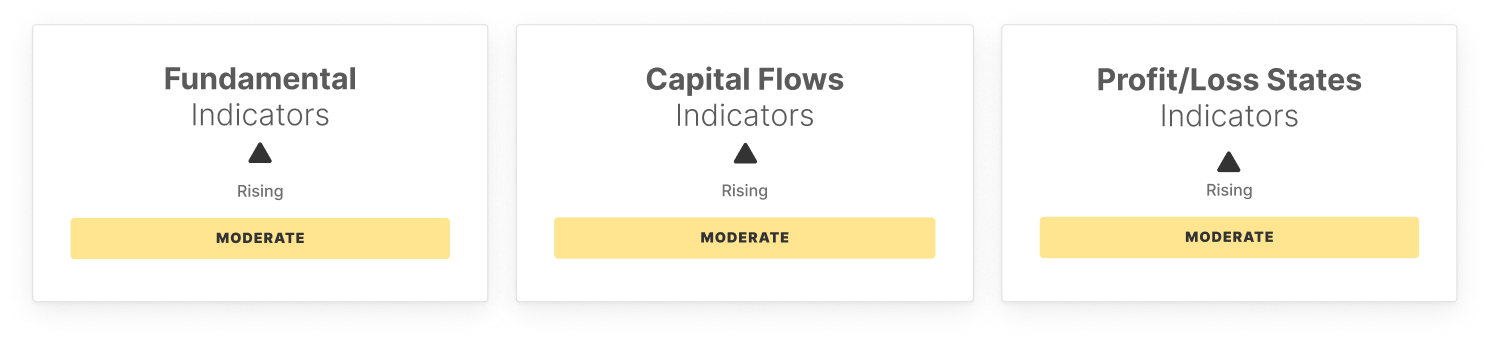

On-chain activity is stabilising. Active addresses remain subdued but are improving, while transfer volume continues to trend higher. Network fees have lifted modestly, and elevated short-term holder supply keeps the market sensitive to price moves.

Overall, Bitcoin remains in consolidation, but internal conditions are improving. While defensive positioning persists, strengthening buy-side dynamics and renewed institutional interest suggest a gradual rebuild toward a more constructive market structure.

Off-Chain Indicators

On-Chain Indicators

🔗 Access the full report in PDF

Don't miss it!

Smart market intelligence, straight to your inbox.

Subscribe now- Follow us and reach out on X

- Join our Telegram channel

- For on-chain metrics, dashboards, and alerts, visit Glassnode Studio

Disclaimer: This report does not provide any investment advice. All data is provided for information and educational purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.

Exchange balances presented are derived from Glassnode’s comprehensive database of address labels, which are amassed through both officially published exchange information and proprietary clustering algorithms. While we strive to ensure the utmost accuracy in representing exchange balances, it is important to note that these figures might not always encapsulate the entirety of an exchange’s reserves, particularly when exchanges refrain from disclosing their official addresses. We urge users to exercise caution and discretion when utilizing these metrics. Glassnode shall not be held responsible for any discrepancies or potential inaccuracies.

Please read our Transparency Notice when using exchange data.