The CLARITY Act’s landmark committee approval has sent Bitcoin sentiment soaring to its highest point in months.

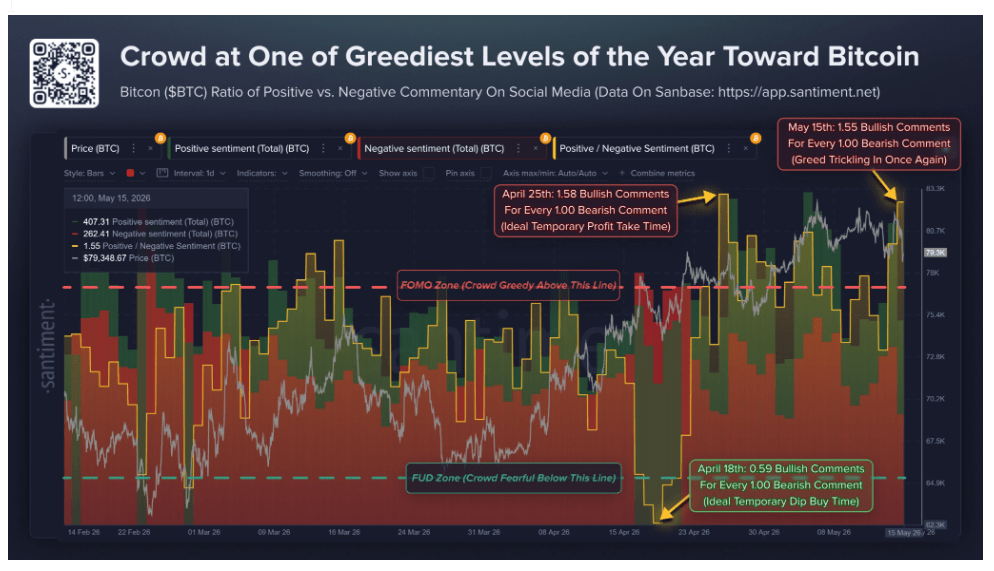

Data from Santiment shows that bullish Bitcoin commentary on social media has climbed to one of its greediest readings of the year, with 1.55 bullish comments for every 1.00 bearish comment. The on-chain data, however, indicates that the crowd may be getting ahead of itself.

Bitcoin Sentiment Points To Greed After CLARITY Act Vote

The passage of the Digital Asset Market Clarity Act through the Senate Banking Committee moved both price and crowd psychology simultaneously. The move came after the US Senate Banking Committee advanced the CLARITY Act in a 15-9 bipartisan vote, sending the important market-structure bill to the full Senate.

Interestingly, Santiment’s data shows that Bitcoin social sentiment has moved back into a FOMO zone. On May 15, Santiment’s social sentiment ratio for Bitcoin reached 1.55 bullish comments for every 1.00 bearish comment, placing it within a FOMO Zone.

That reading mirrors a prior peak recorded on April 25, when the ratio reached 1.58 bullish-to-bearish. Any time the ratio of positive to negative commentary on social media crosses this FOMO zone, then it is an ideal temporary profit-taking moment.

This does not mean Bitcoin has to crash because the crowd has turned optimistic. The same Santiment chart shows that the better contrarian setup came on April 18, when the bullish-to-bearish ratio dropped to 0.59. This was deep in the FUD Zone, before Bitcoin mounted a recovery.

Bitcoin Ratio Of Positive vs. Negative Commentary. Source: @SantimentData On X

CLARITY Act Still Bullish For Bitcoin In The Long Run

The caution around short-term sentiment does not cancel the long-term importance of the CLARITY Act. The bill is designed to create a clearer federal framework for digital assets, including a more defined division of authority between the Securities and Exchange Commission and the Commodity Futures Trading Commission.

The bill was championed by major crypto companies, including Coinbase, Circle, and Ripple, all of which have sought a degree of regulation for the crypto industry. Senior figures linked to these companies also reacted positively on social media after the Senate Banking Committee advanced the legislation.

Coinbase CEO Brian Armstrong, for instance, stated in a post on X: “looking forward to a bipartisan law that cements the US as the world’s crypto capital. Let’s get CLARITY done.”

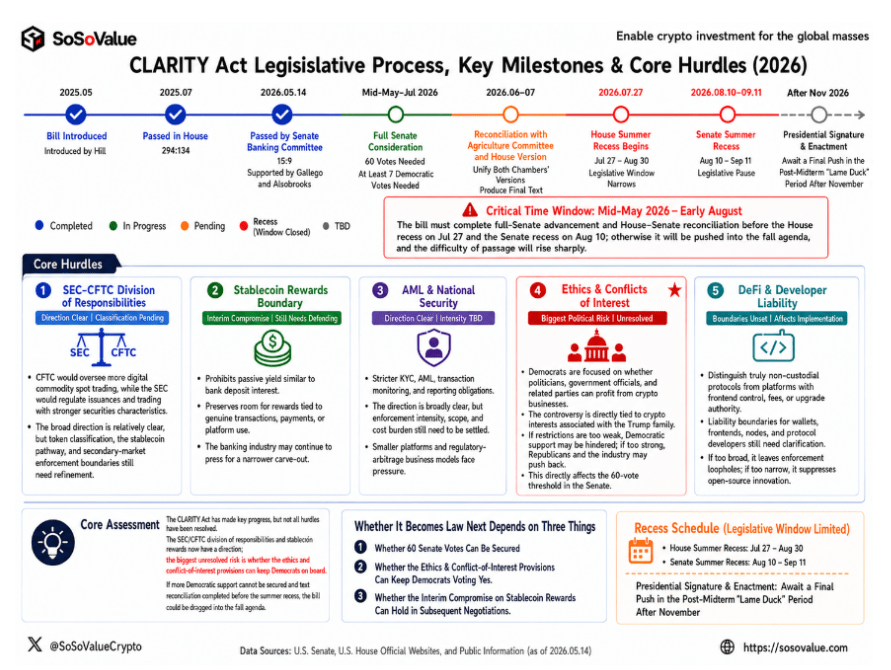

The bill still needs to be available for a vote from the full Senate, where 60 yes votes will be required. Projections from SoSoValue show a key window between mid-May and early August, with the House recess beginning July 27 and the Senate recess beginning August 10.

If lawmakers fail to complete full Senate consideration and reconciliation before that period, the bill could be pushed deeper into the fall agenda, and the difficulty of passage will rise significantly.

Clarity Act Legislative Process. Source: SoSoValue

Featured image from Unsplash, chart from TradingView