On January 14th, a bill aimed at establishing regulations for the U.S. crypto market—the CLARITY Act—is set for a crucial vote in the Senate Banking Committee. On the eve of this potential breakthrough for the industry, Brian Armstrong, founder and CEO of Coinbase, announced that the company would completely withdraw its support for the bill, stating that "a bad bill is worse than no bill."

The news immediately sent shockwaves through the industry. But what was truly surprising was that almost all other major players in the industry stood on the opposite side of Coinbase.

Chris Dixon, a partner at venture capital giant a16z, believed "now is the time to push forward"; Brad Garlinghouse, CEO of payments giant Ripple, stated that "clarity beats chaos"; Arjun Sethi, co-CEO of rival exchange Kraken, bluntly said "this is a test of political resolve"; even the non-profit organization Coin Center, known for its defense of decentralization principles, stated that the bill was "basically correct on developer protection."

On one side was the undisputed leader of the industry; on the other were the leader's former important allies. This was no longer the old story of the crypto industry fighting against Washington regulators, but a civil war erupting within the industry itself.

The Isolated Coinbase

Why was Coinbase isolated by the others?

The answer is simple: because almost all other major participants, based on their respective business interests and survival philosophies, judged this imperfect bill to be the best option at present.

First, a16z. As Silicon Valley's most prestigious crypto investment firm, a16z's portfolio spans almost all crypto sectors. For them, the most fatal issue is not the strictness of specific clauses, but the persistent regulatory uncertainty.

A clear legal framework, even with flaws, can provide fertile ground for the entire ecosystem they invest in. Chris Dixon's position represents the consensus among investors: regulatory certainty is more important than a perfect bill.

Second, the exchange Kraken. As one of Coinbase's most direct competitors, Kraken is actively preparing for an IPO.

Regulatory endorsement from Congress would significantly boost its valuation in the public market. In comparison, the bill's restrictions on stablecoin yields have a much smaller financial impact on Kraken than on Coinbase. Trading a controllable short-term business loss for the long-term huge benefits of going public is a no-brainer for Kraken.

Then there's payments giant Ripple. Its CEO, Brad Garlinghouse, summarized his stance in six words: "clarity beats chaos." Behind this lies Ripple's years-long legal battle with the SEC, costing hundreds of millions of dollars.

For a company exhausted by regulatory battles, any form of peace is a victory. Even an imperfect bill is far better than endless consumption in court.

Finally, the advocacy organization Coin Center. As a non-profit, their stance is the least driven by commercial interests. Their core demand for years has been to ensure software developers are not incorrectly classified as "money transmitters" and subjected to excessive regulation.

This bill fully incorporates their advocated Blockchain Regulatory Certainty Act (BRCA), legally protecting developers. With the core goal achieved, other details can be compromised. Their support represents the approval of the industry's "fundamentalists."

When VCs, exchanges, payment companies, and advocacy organizations all stand on the same side, Coinbase's position appears particularly glaring.

So the question is, if the entire industry sees a path forward, what does Coinbase see that makes it willing to cause an industry split to stop it?

Business Model Determines Stance

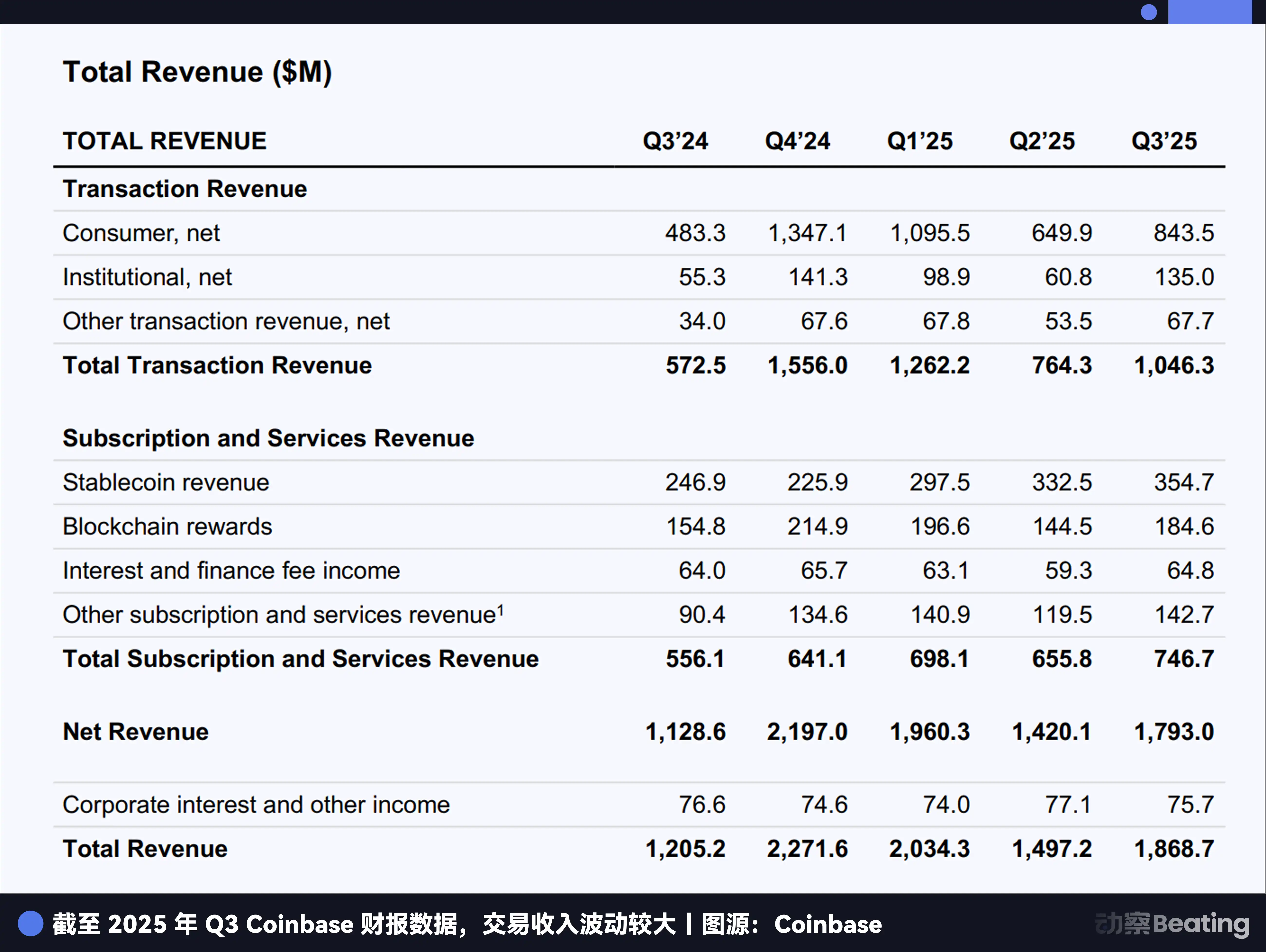

The answer lies in Coinbase's financial statements, in a $1.4 billion hole.

To understand Armstrong's move to overturn the table, one must first understand Coinbase's survival anxiety. For a long time, a significant portion of Coinbase's revenue has relied on cryptocurrency trading fees.

The fragility of this model was exposed during the crypto winter: profits were abundant during bull markets, but revenue plummeted during bear markets, even leading to quarterly losses. The company had to find new, more stable revenue sources.

Stablecoin yield is the second growth curve Coinbase found.

Its business model is not complicated: users hold the USD-pegged stablecoin USDC on the Coinbase platform, and Coinbase lends these idle funds out through DeFi protocols (like Morpho) to earn interest, then returns part of the earnings to users as rewards. According to data on Coinbase's website, regular users can get a 3.5% annualized yield, while paid members can get up to 4.5%.

According to Coinbase's Q3 2025 earnings report, its "Interest and Financing Income" reached $355 million, most of which came from stablecoin business. Based on this, this business contributed approximately $1.4 billion in revenue to Coinbase in 2025, accounting for an increasingly large share of its total revenue. In a bear market with sluggish trading volume, this stable and substantial cash flow is Coinbase's lifeline.

And a newly added clause in the CLARITY Act precisely targets Coinbase's Achilles' heel. The clause stipulates that stablecoin issuers or affiliated parties cannot pay yields for users' "Static Holdings," but are allowed to pay yields for "Activities and Transactions."

This means that the practice of users simply holding USDC in their Coinbase accounts to earn interest will be prohibited. This is a fatal blow to Coinbase. If the bill passes, this $1.4 billion revenue could shrink significantly or even vanish.

Beyond this, the various issues Armstrong listed on social media seem more like a battle over market structure: the draft could effectively block the path for tokenized stocks/securities, set higher barriers for DeFi, make user financial data more accessible to regulators, and weaken the CFTC's role in the spot market.

The stablecoin yield ban is just the most直观 (intuitive) and immediately damaging blow to Coinbase.

Different interests lead to different choices.

Kraken's stablecoin business is much smaller than Coinbase's, allowing it to trade short-term loss for the long-term value of an IPO; Ripple's core is payments, where regulatory clarity trumps everything; a16z's chessboard is the entire ecosystem, and the得失 (gains and losses) of a single project don't affect the overall situation. Coinbase sees a cliff, while other companies see a bridge.

However, there is a third party in this game: traditional banking.

The American Bankers Association (ABA) and the Bank Policy Institute (BPI) argue that allowing stablecoin yields will lead to trillions of dollars in deposits flowing out of the traditional banking system, posing an existential threat to thousands of community banks.

Back in July 2025, the stablecoin genius bill had already passed, explicitly allowing "third parties and affiliated parties" of stablecoins to pay yields, leaving legal room for Coinbase's model. But in the 7 months since, the banking industry launched a powerful lobbying offensive, ultimately successfully adding the "Static Holdings" ban to the CLARITY Act.

Banks don't fear the 3.5% yield; they fear losing deposit pricing power. When users can freely choose to keep funds in banks or crypto platforms, the banks' decades-long low-interest monopoly ends. This is the essence of the conflict.

So, faced with such complex interest博弈 (game theory), why did only Armstrong choose the most drastic approach?

Two Survival Philosophies

This is not just a conflict of commercial interests, but a collision of two截然不同 (completely different) survival philosophies. One is Silicon Valley-style idealism and non-compromise, the other is Washington-style pragmatism and gradual reform.

Brian Armstrong represents the former. This is not the first time he has publicly clashed with regulators. As early as 2023, when the SEC sued Coinbase for illegally operating a securities exchange, Armstrong publicly criticized the SEC for its "inconsistent stance" and revealed that Coinbase had held over 30 meetings with regulators, repeatedly requesting clear rules but never getting a response.

His stance has been consistent: support regulation, but firmly oppose "bad regulation." In his view, accepting a bill with fundamental flaws is more dangerous than having no bill for now. Because once a law is made, it will be extremely difficult to change it in the future. Accepting a bill that strangles the core business model for short-term certainty is like drinking poison to quench thirst.

Armstrong's logic is: fight now at all costs; it's painful, but it preserves the possibility of争取 (fighting for) better rules in the future. Compromising now means permanently abandoning the stablecoin yield battlefield. In this war concerning the company's future, compromise is surrender.

Other leaders in the crypto industry, however, have shown a截然不同 (completely different) pragmatic philosophy. They understand the rules of the game in Washington: legislation is the art of compromise, and perfection is the enemy of good.

Kraken's CEO Sethi believes the important thing is to first establish a legal framework, giving the industry legitimate social status, and then gradually improve it through continuous lobbying and participation. Survival first, development later.

Ripple's CEO Garlinghouse places certainty above all else. Years of litigation have taught him that struggling in legal quagmires is a company's huge消耗 (drain). An imperfect peace is far better than a perfect war.

a16z's Dixon looks from the strategic height of global competition, believing that if the US delays legislation due to internal quarrels, it will only hand over its position as the center of global financial innovation to Singapore, Dubai, or Hong Kong.

Armstrong is still fighting a Washington battle the Silicon Valley way, while others have already learned the language of Washington.

One is the principled坚守 (adherence) of "rather be a shattered vessel of jade than an unbroken piece of pottery," the other is the realistic consideration of "where there is life, there is hope." Which is wiser? Until time gives us the answer, no one can say for sure. But one thing is certain: both choices come with heavy costs.

The Cost of Civil War

What is the real cost of this civil war ignited by Coinbase?

First, it causes political分裂 (division) within the crypto industry.

According to a Politico report, Senate Banking Committee Chairman Tim Scott's decision to delay the vote was made precisely when Coinbase defected at the last minute and support votes for the bill among bipartisan senators were still uncertain. Coinbase's move, while not the sole reason, was undoubtedly a key factor pushing the entire effort into chaos.

If the bill ultimately fails because of this, other companies might partly blame Coinbase, believing it acted for its own selfish interests, affecting the entire industry's progress.

More seriously, this public infighting greatly weakens the crypto industry's collective bargaining power in Washington.

When lawmakers see the industry cannot even form a unified voice, they become confused and frustrated. A divided industry will be no match for powerful traditional financial lobbying groups.

Second, it exposes the困境 (dilemma) of regulation in the digital age.

The CLARITY Act attempts to walk a tightrope between encouraging innovation and preventing risk, but this balance point can hardly satisfy everyone. For Coinbase, the bill regulates too tightly; for traditional banks, it is too loose; for other crypto companies, it might be just right.

The dilemma of regulation is that it tries to set boundaries for never-satisfied desires. Every time a rule lands, it's just the beginning of the next game.

But the most important cost is that this civil war shakes the foundation of the crypto industry.

What exactly is the crypto industry? A social experiment about decentralization and individual freedom, or a business about asset appreciation and wealth creation? A revolution against the existing financial system, or a supplement and improvement to it?

Armstrong's决绝 (resoluteness) and the compromise of others in the industry together outline the industry's current true face: a contradictory entity constantly oscillating between ideal and reality, revolution and commerce.