Author: Lex

Compiled by: Deep Tide TechFlow

Deep Tide Introduction: Coinbase and Robinhood both reported earnings below expectations last week, erasing $12 billion in market value. This exposes a fundamental issue with the exchange model: how to survive in a bear market when revenue is highly dependent on trading fees? Platforms like Revolut, which are payment-centric, are almost unaffected, with trading income accounting for only 15% of their revenue. This comparison reveals the underlying logic of competition among fintech platforms.

Cryptocurrency is in the depths of a bear market.

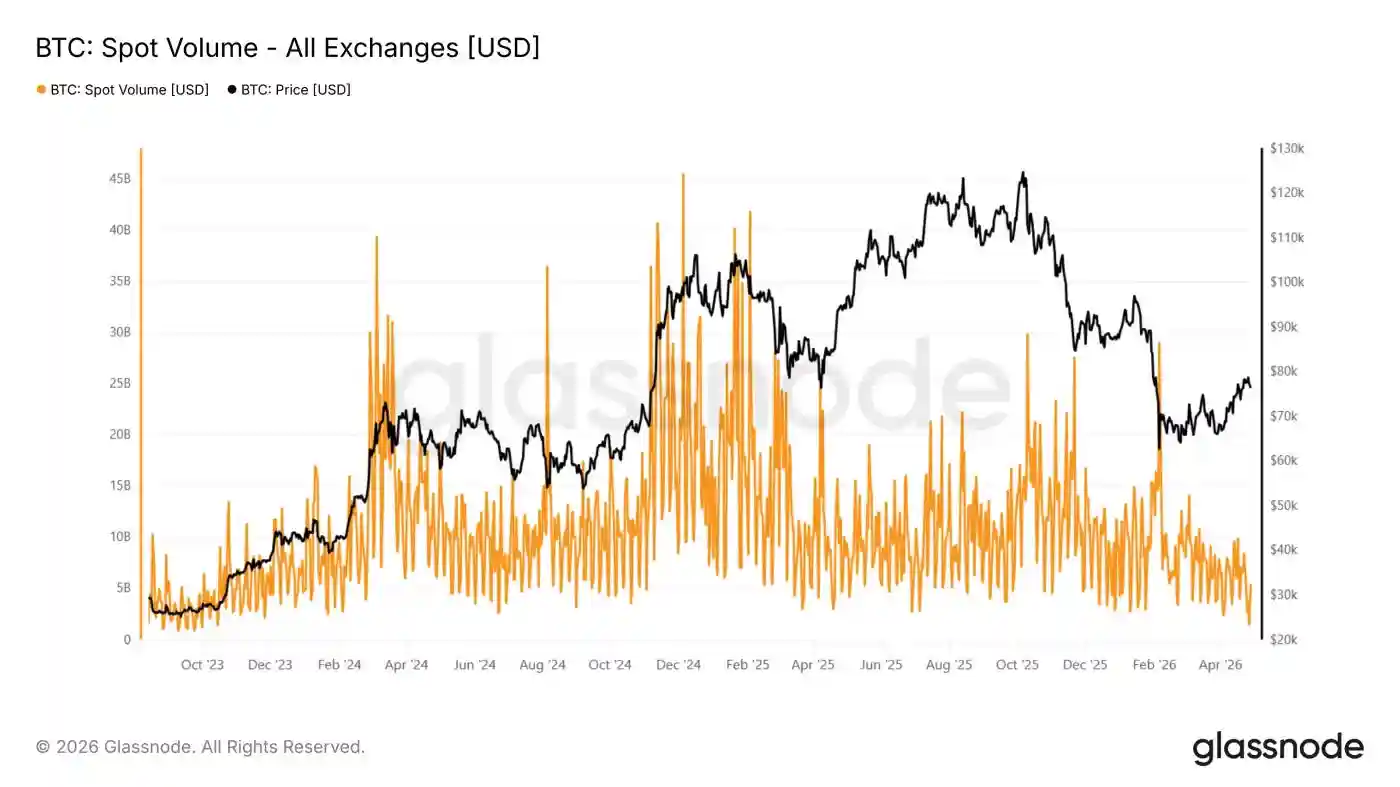

Bitcoin hovers around $80,000, down approximately 36% from its peak of $126,000 in October 2025. Spot trading volume on centralized exchanges has fallen to its lowest level since September 2019, down 44% year-over-year in the first quarter according to Coinbase data.

Some on-chain analysts believe the recent rebound from $60,000 may lack sustained momentum. This has been the longest bear market rally of the past two cycles, but it appears more technically than fundamentally driven. Open interest in derivatives (perpetual contracts) has risen, but spot activity is low, suggesting the rise is driven more by short liquidations and speculative position unwinding than persistent buying.

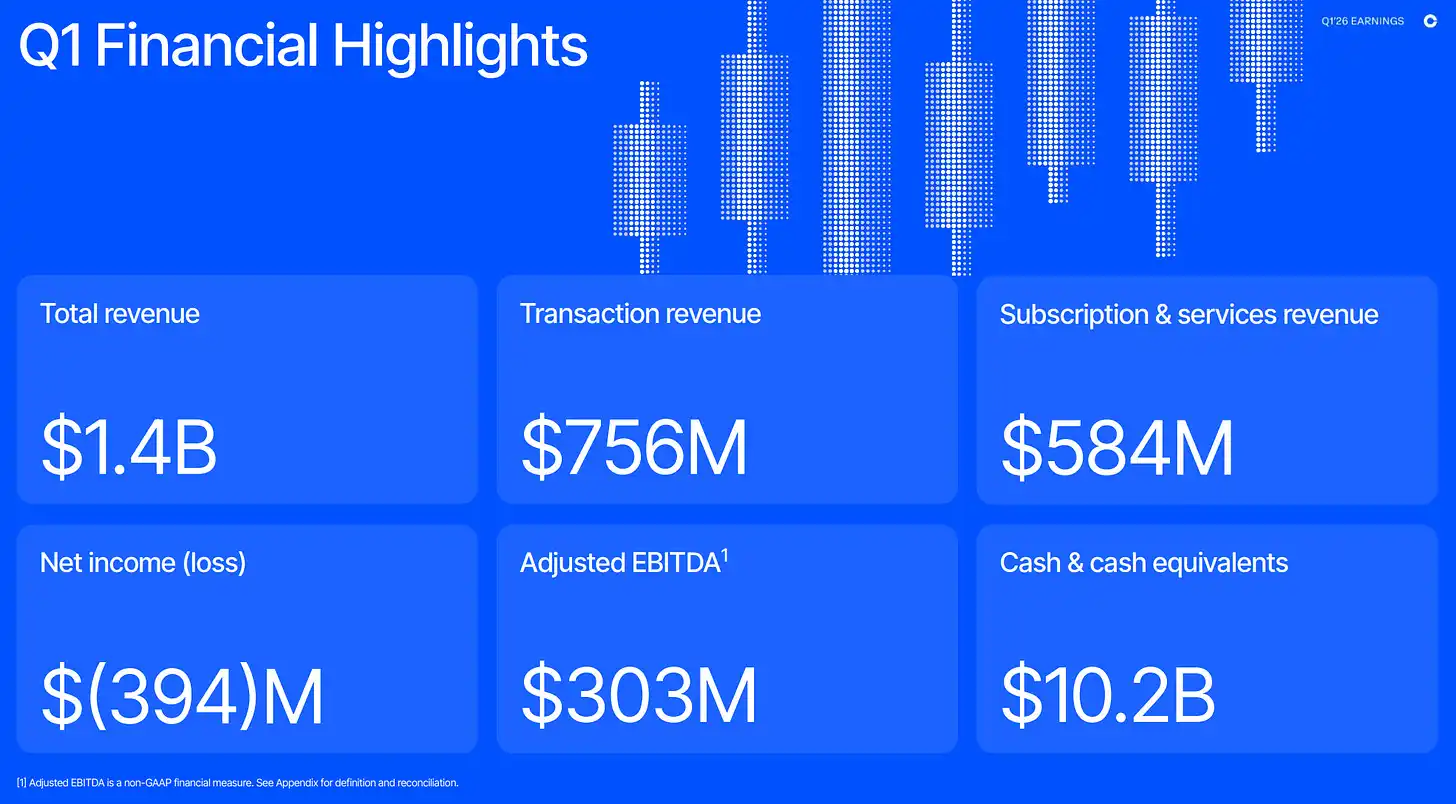

Decreased trading activity is eroding platform revenue. Coinbase's revenue fell 31% year-over-year to $1.41 billion, with a net loss of $394 million, compared to a profit of $66 million in the same period last year. Management also announced layoffs of 700 employees (about 14% of its workforce) the same week, citing both crypto cyclicality and a cost "reset for the AI era."

Trading business is at the center of the decline.

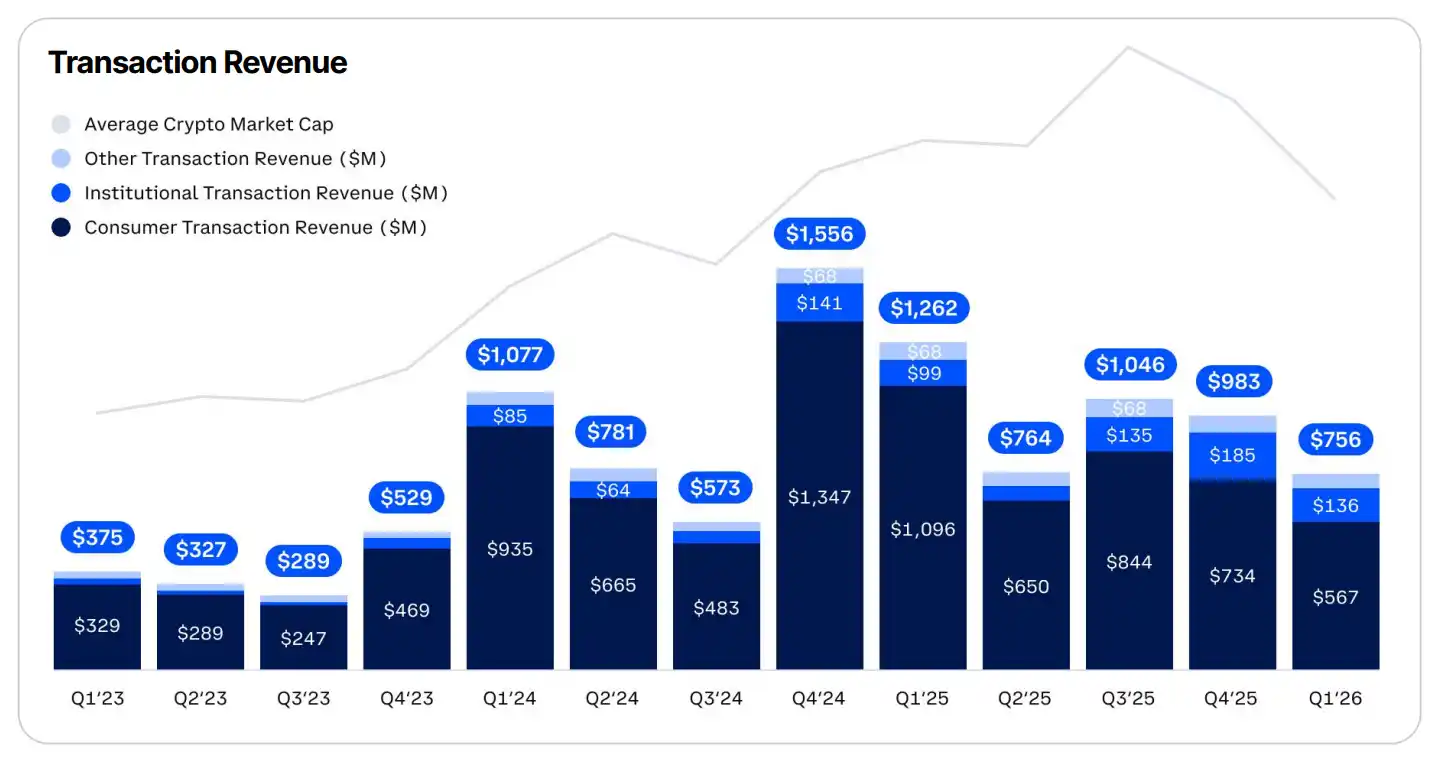

Transaction revenue accounted for 56% of total revenue in Q1, down 40% year-over-year. Consumer transaction revenue fell 48% to $567 million. Institutional transaction revenue actually grew during this period, but this was almost entirely due to the $4.3 billion acquisition of Deribit completed in August 2025; organic institutional trading volume actually fell 48%.

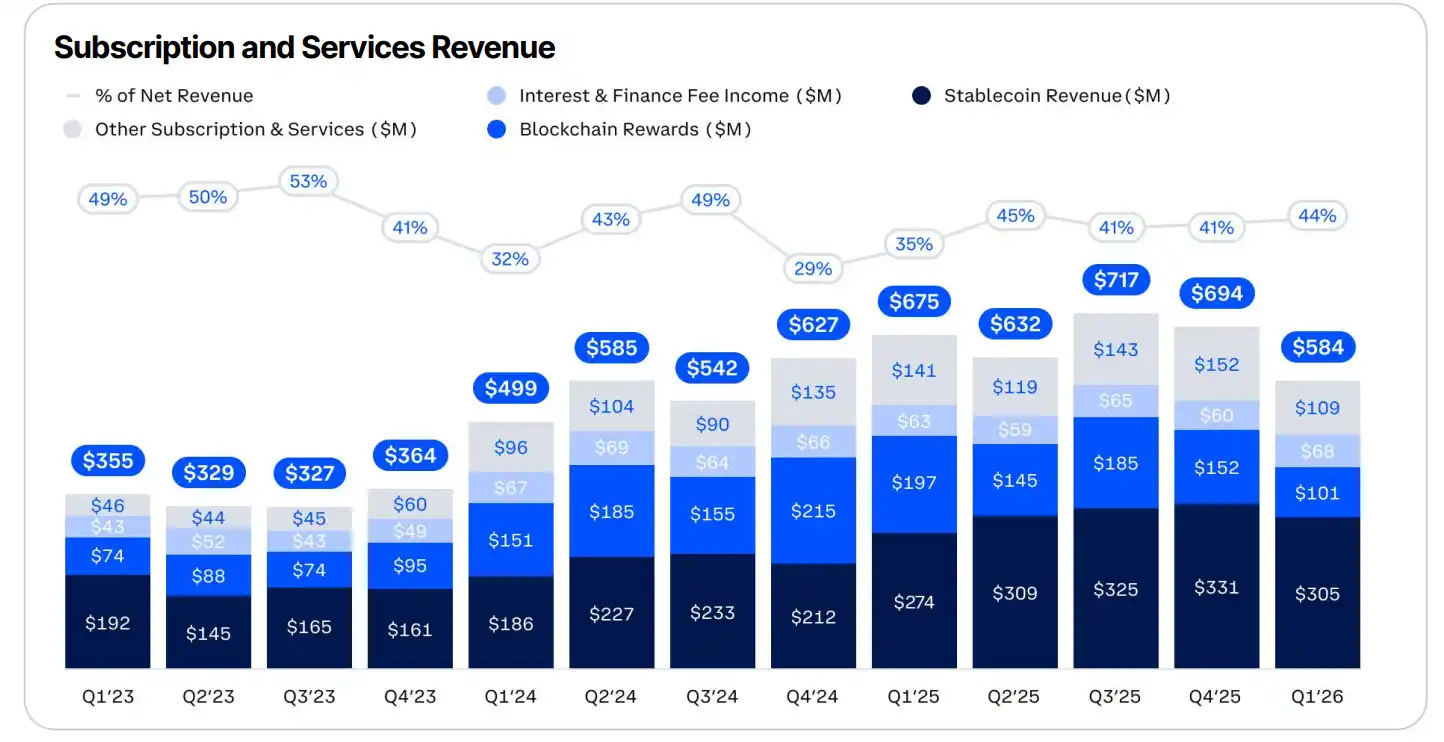

The remaining revenue comes from subscriptions and services, distributed across stablecoin revenue (interest earned from customer USDC balances via Coinbase's partnership with Circle), blockchain rewards, interest and financing fees, and other subscription products like Coinbase One.

This segment now accounts for 44% of total revenue, which management positions as a "durable buffer" against trading volatility. But this is somewhat misleading. Stablecoin revenue is the largest single item, accounting for 22% of net revenue, up 11% year-over-year, but it is also highly correlated with trading volume. Customers move into USDC to avoid volatility or rotate between assets, but reconfigure back into volatile assets once the market turns. This dynamic partly explains why the proportion of subscription and service revenue to total revenue has looked fairly steady over the past 3 years.

Meanwhile, Robinhood reported stronger numbers.

Revenue increased 15% year-over-year to $1.07 billion, with net profit of $350 million, but still missed analysts' revenue expectations. Like Coinbase, the miss was driven by crypto, with related transaction revenue falling 47% year-over-year to $134 million. Notably, this was the only major revenue line item to decline year-over-year.

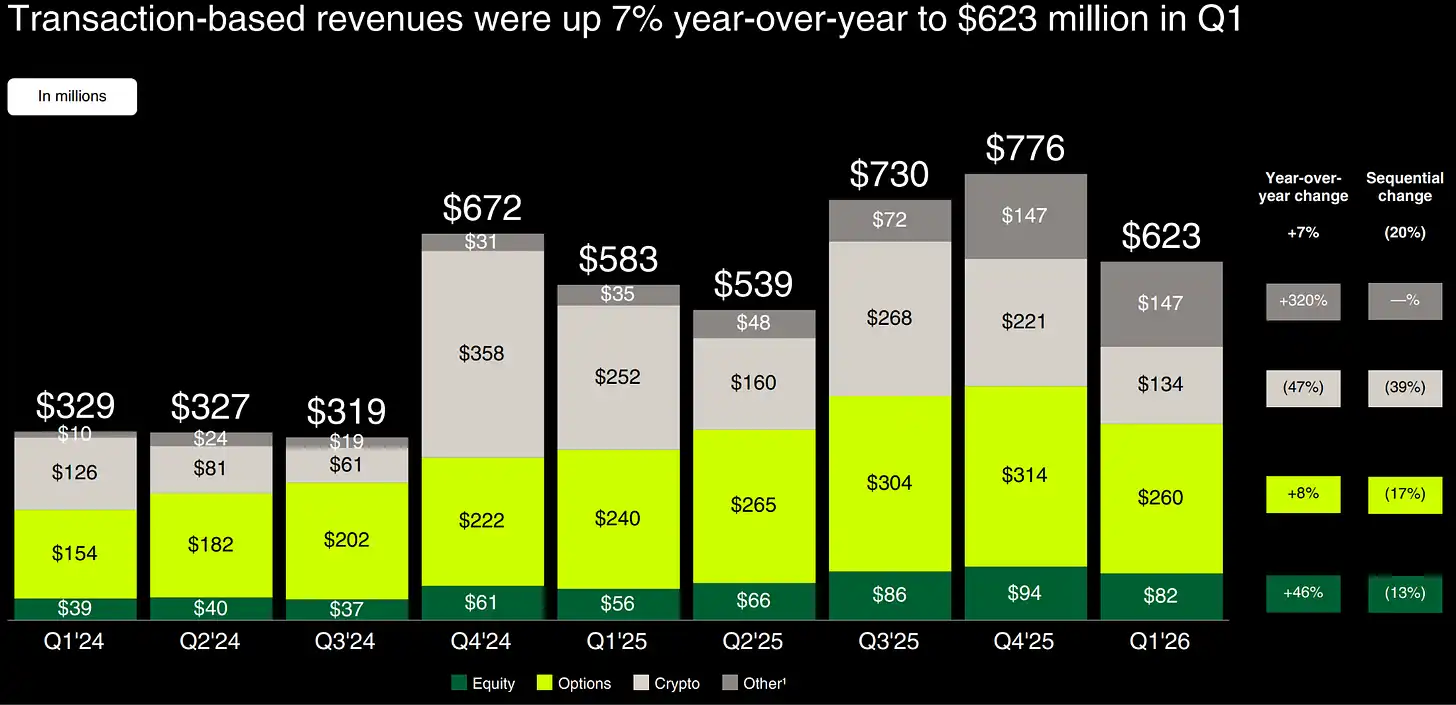

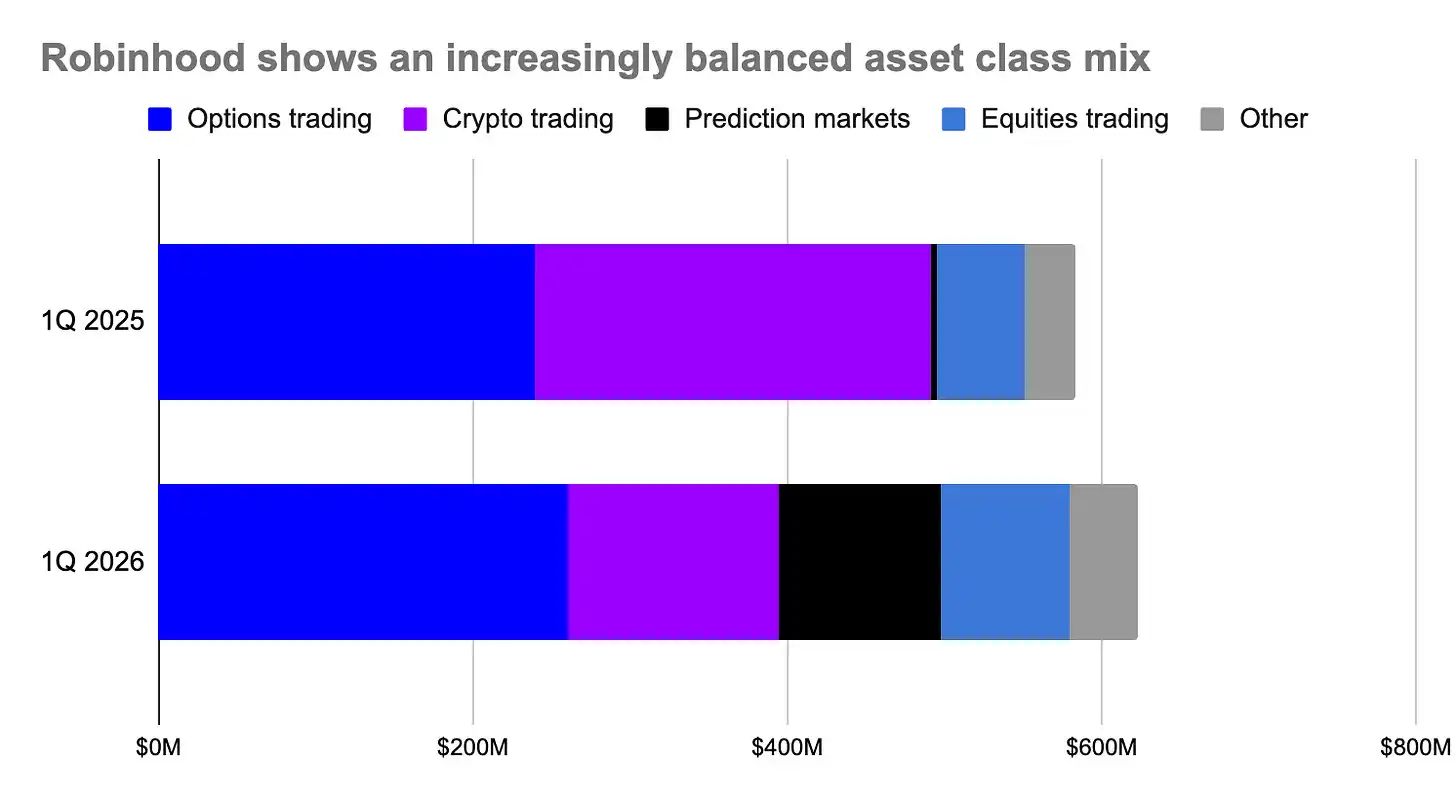

Trading still accounts for 58% of Robinhood's revenue, basically flat from a year ago. But due to the diversity of tradable asset classes, the company has performed better throughout the bear market. Total transaction revenue grew 7% year-over-year to $623 million, driven by a 320% surge in prediction market revenue via Robinhood's partnership with Kalshi, a 46% increase in stock revenue, and 8% growth in options.

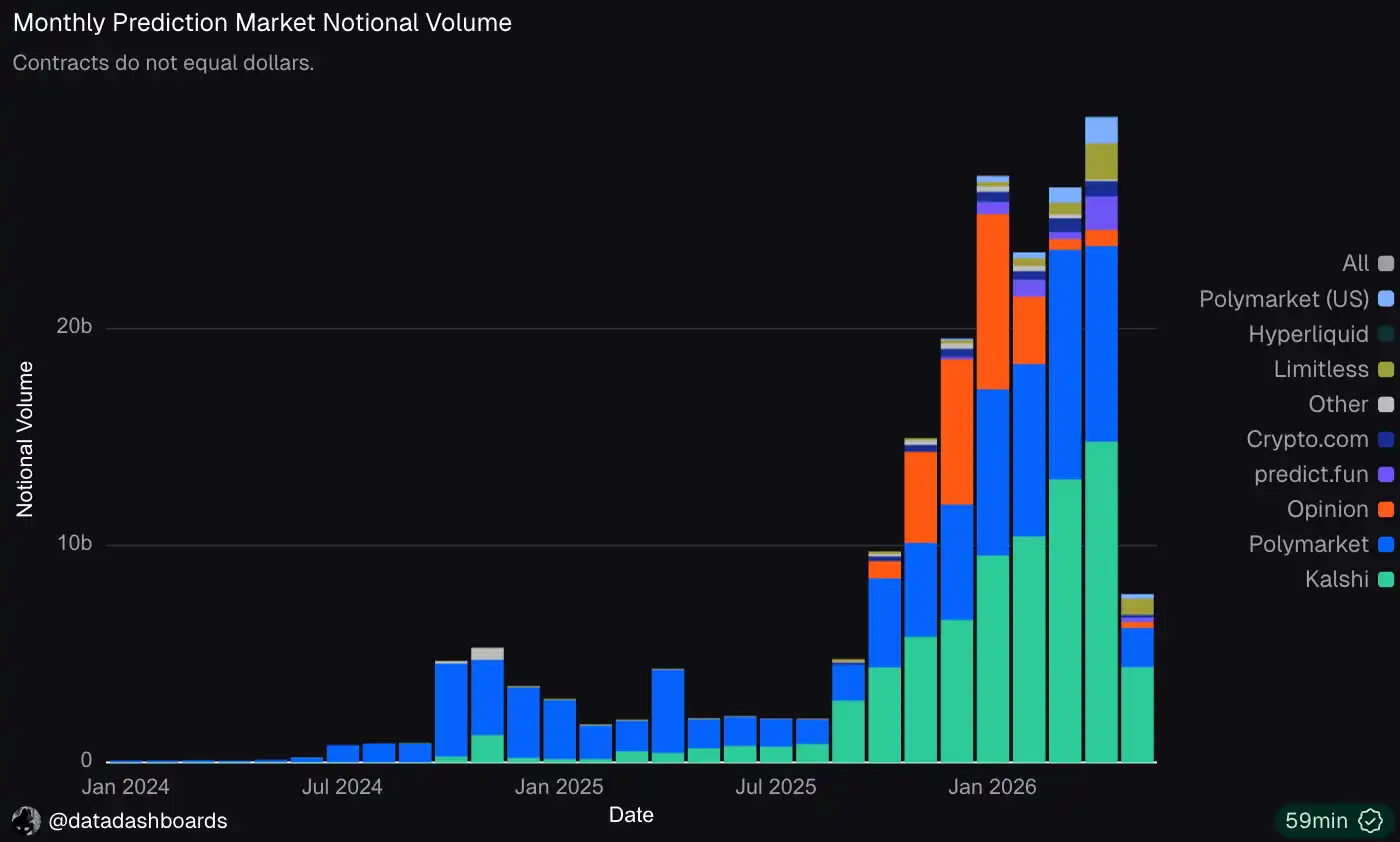

Derivatives like prediction markets and perpetual contracts have shown more resilience during downturns. Kalshi raised $1 billion last week at a $22 billion valuation, doubling its valuation in just 6 months and tripling its annualized trading volume to $178 billion.

Event-driven trading, like predictions, often focuses on sports, elections, and economic data, making it less sensitive to the broader market. But growth also stems from institutions starting to use it as a hedging tool during market volatility. There is an organic adoption tailwind masking the cyclicality.

Perpetual contracts show a similar pattern. As of the end of April, the total value of leveraged positions by traders on Hyperliquid (measured as "open interest") was $4.3 billion, having grown 9% over the past two months despite the general collapse in spot markets. While this metric is still down from the October peak, it is clearly performing better.

This is significant for trading platforms that have these features.

Prediction markets now account for 17% of Robinhood's total transaction revenue!

While it doesn't directly offer perpetual contracts, it does offer similar margin trading on stocks and crypto, and earns interest from it. In Q1 2026, margin interest revenue grew 75% year-over-year to $193 million, accounting for 18% of total revenue.

Coinbase is a latecomer to this shift. While it launched prediction markets and perpetual contracts for retail customers in January 2026, it hasn't yet had a material impact on its P&L. Consequently, the exchange has greater exposure to spot trading.

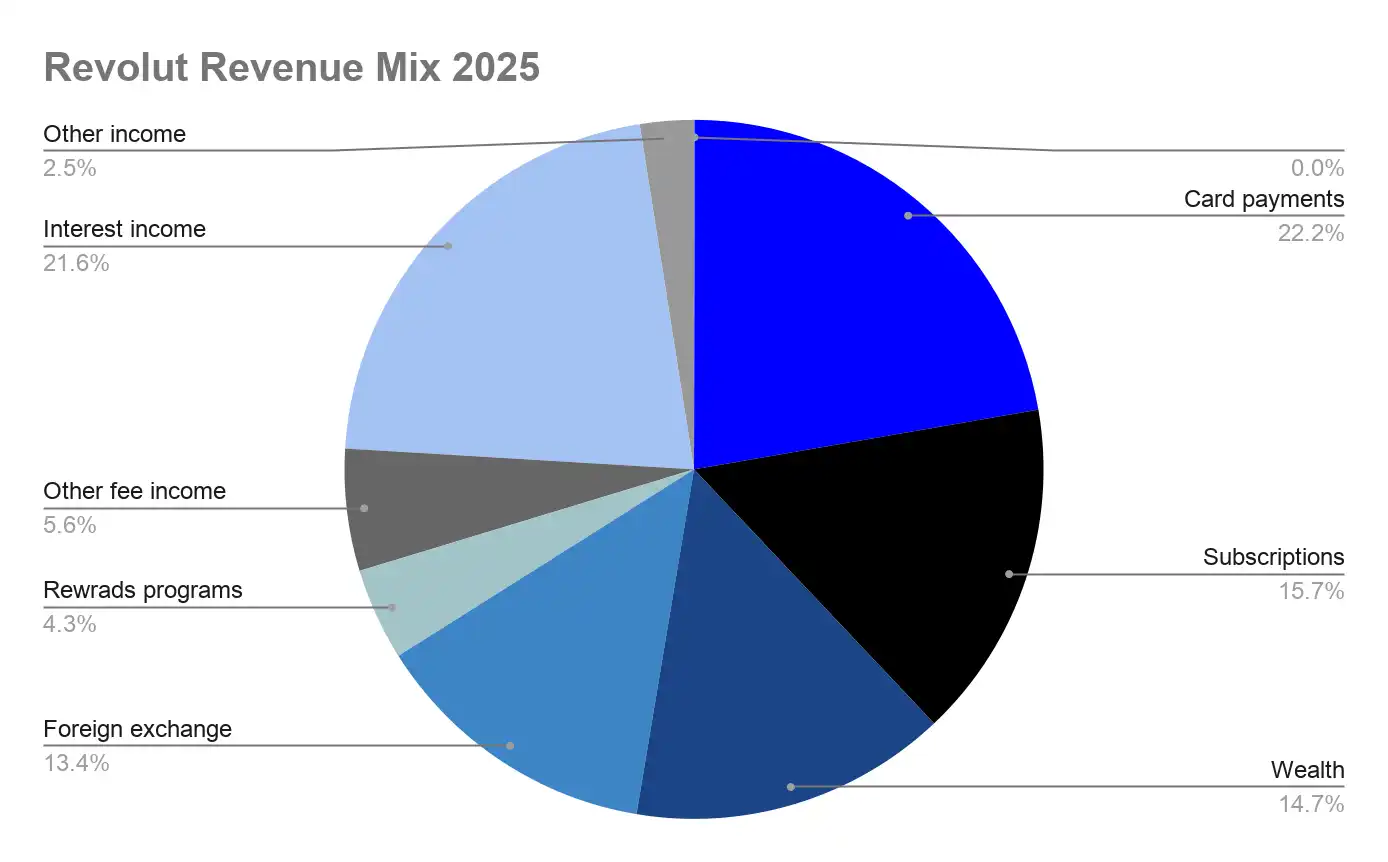

Fintech platforms centered on payments and banking, but with significant trading activity like Revolut, are much less affected. Revenue grew strongly by 45% to $6.1 billion in 2025, with a balanced distribution across major revenue streams, each accounting for 13-22% of total revenue.

Card interchange fees and interest income are the two largest items, each around $1.3 billion. Crypto trading, along with stocks and CFDs, falls under the Wealth segment, accounting for 15% of total revenue—a fraction of Robinhood's exposure and a sliver of Coinbase's.

Notably, Revolut's interest income is similar to Coinbase's stablecoin revenue, both monetizing idle customer balances. As of year-end, Revolut held 90% of its $68 billion customer balance in cash and treasury investments. But the behavior driving these balances is fundamentally different. Revolut's deposits grow with primary banking relationships and direct deposit growth (up 45% year-over-year), while Coinbase's USDC balances grow as willingness to trade declines. If the crypto market turns more bullish, Coinbase is more likely to see balances decline.

The challenge for trading-first platforms like Coinbase and Robinhood is whether they can meaningfully expand into adjacent financial products while being tightly linked to market cycles. Robinhood has shown that diversity in tradable asset classes, especially prediction markets and derivatives, can act as a hedge.

Coinbase is moving in a similar direction. The risk is that a prolonged bear market hinders their growth ability, while fintech competitors like Revolut, Nubank, and Cash App take a greater share of customer deposits.