Arthur Hayes, co-founder and former CEO of crypto exchange BitMEX, argued in a Substack essay published Friday that the Federal Reserve’s new “reserve management purchases” (RMP) program is effectively a rebranded form of quantitative easing.

Hayes argues that by buying short-term Treasury bills and recycling liquidity through money markets, the Fed is effectively financing government spending while avoiding the political stigma of quantitative easing, even as officials frame the program as a technical liquidity operation.

“The RMP is a thinly disguised way for the Fed to cash the government’s checks. This is highly inflationary from both a financial and real goods/services perspective,” he wrote.

Hayes said policies like RMP expand fiat liquidity and, in his view, favor scarce assets such as Bitcoin, gold and silver.

I love QE because it means money printing, and thankfully I own financial assets like gold, gold/silver mining stocks, and Bitcoin that rise faster than the pace of fiat money creation.

At the same time, he warned that people without assets are harmed, as money creation erodes purchasing power, weakens wages relative to prices and shifts wealth toward asset holders.

“Unfortunately, in the here and now for most of humanity, money printing destroys their dignity as productive humans,” he wrote. “When the government intentionally debases the currency, it destroys the link between energy inputs and economic outputs.”

Related: Bitcoin rebounds on Japan rate hike as Arthur Hayes sees dollar at 200 yen

Polymarket points to pause after December rate cut

On Dec. 10, the Federal Open Market Committee (FOMC) cut interest rates by 25 basis points and announced purchases of short-term Treasury securities, a move Fed Chair Jerome Powell said was “solely for the purpose of maintaining an ample supply of reserves” and separate from the stance of monetary policy.

The Fed said the purchases would initially total about $40 billion in the first month and could remain elevated for several months to ease near-term pressures in money markets, particularly around seasonal fluctuations such as tax payments.

Despite the interest rate cut and the announcement of short-term Treasury purchases, analysts said mixed signals from Powell were likely to dampen a sustained Bitcoin rally until the rate-cutting cycle resumes in 2026.

The price of Bitcoin was about $92,695 on Dec. 10, according to Yahoo Finance data. It is was trading around $87,300 at time of writing.

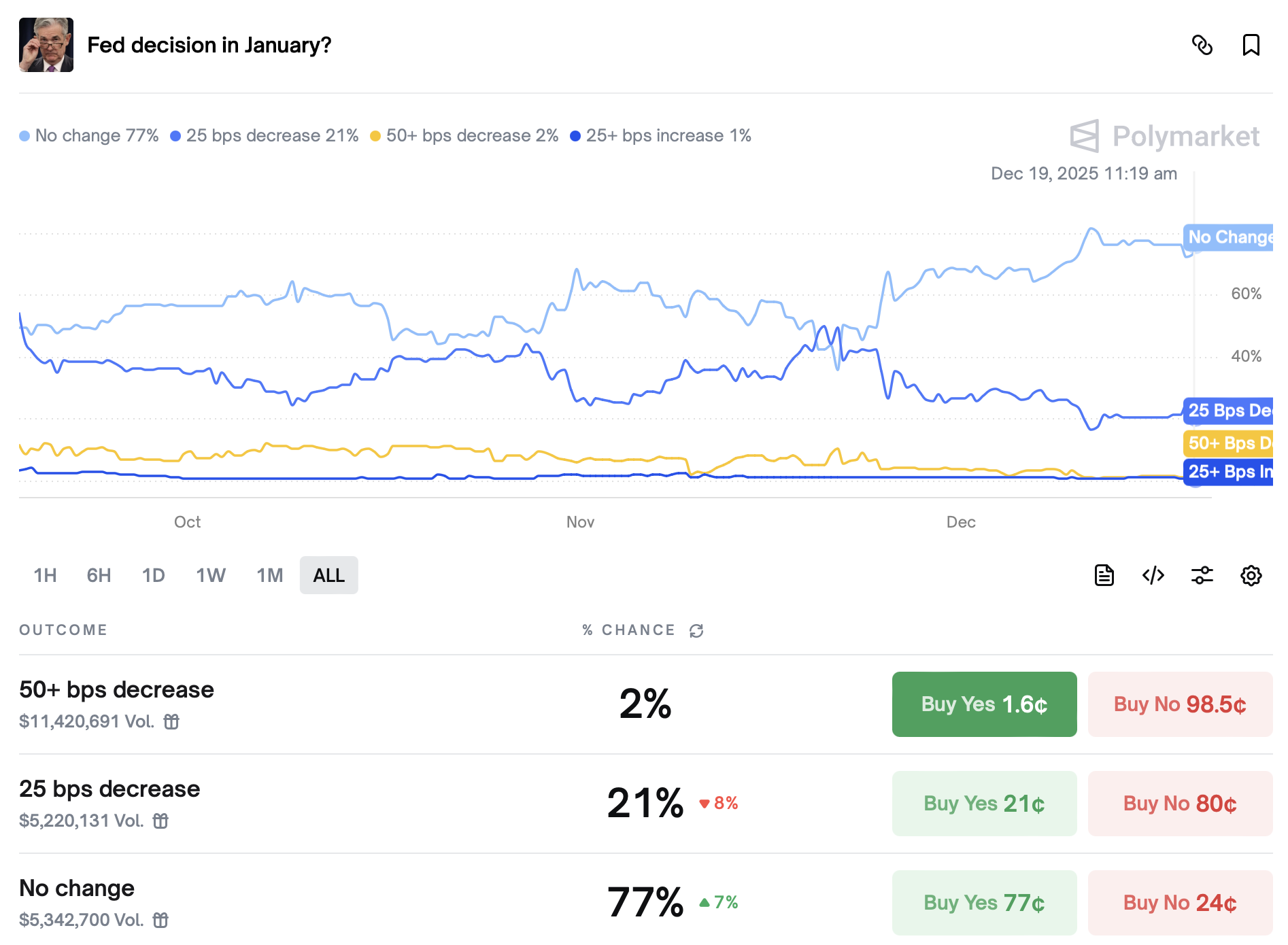

At the time of writing, Polymarket traders were overwhelmingly pricing in no change to Fed policy in January, with the probability of rates staying unchanged at about 77%, while odds of another 25 basis point cut sit near 21% and larger moves are viewed as highly unlikely.

Powell’s term is set to expire in May 2026. US President Donald Trump, who has publicly pushed for the next Fed chair to pursue aggressive interest rate cuts, is preparing to interview finalists to succeed him, with National Economic Council Director Kevin Hassett widely viewed as the frontrunner.

Magazine: Big questions: Would Bitcoin survive a 10-year power outage?