Author: Artemis

Compiled by: Deep Tide TechFlow

Deep Tide Guide:

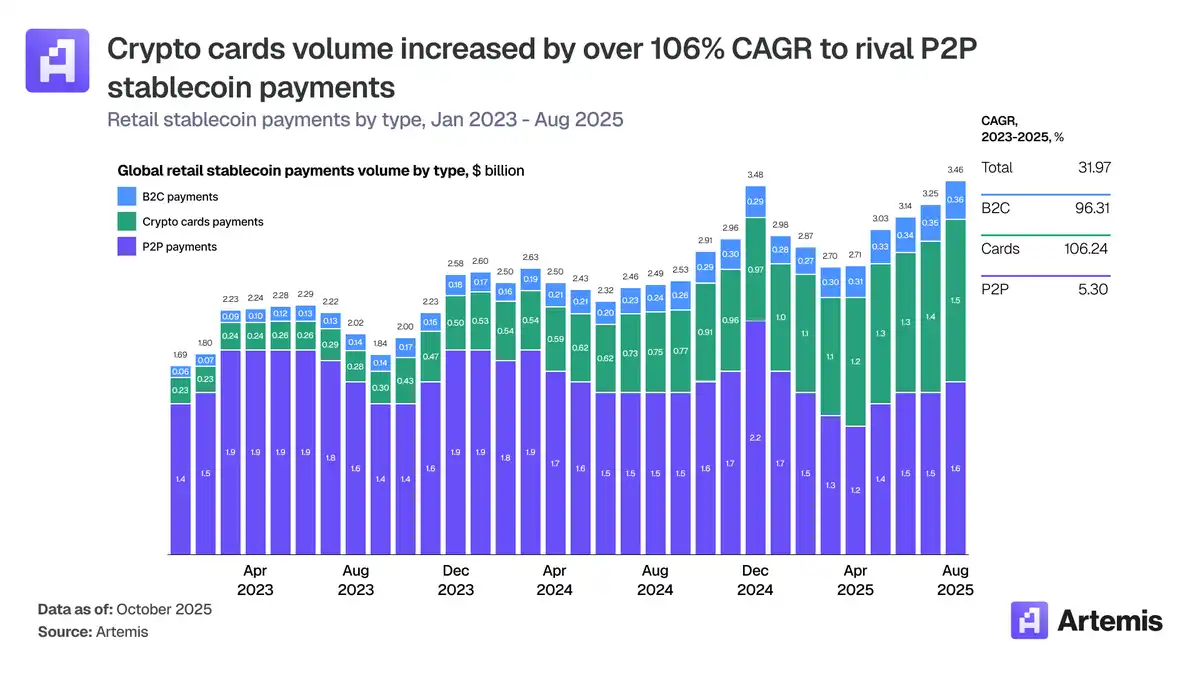

Crypto payments are undergoing a silent "great power shift." The latest research from Artemis shows that the crypto card market has surged from the fringes in early 2023 to a massive $18 billion annualized size, with monthly transaction volume increasing 15-fold in just two years.

This article deconstructs the three layers of the crypto payment stack and reveals a surprising figure: Visa accounts for over 90% of on-chain card transaction volume. More importantly, the industry is experiencing a structural shift towards "full-stack issuance." Companies like Rain and Reap are bypassing traditional banks by connecting directly to Visa, completely rewriting the economic model. From crypto-collateralized credit in India to daily stablecoin payments in Argentina, crypto cards are becoming key infrastructure for bringing digital dollars into the real world.

Full text as follows:

Big news: We just released the industry's most detailed research report on Crypto Cards.

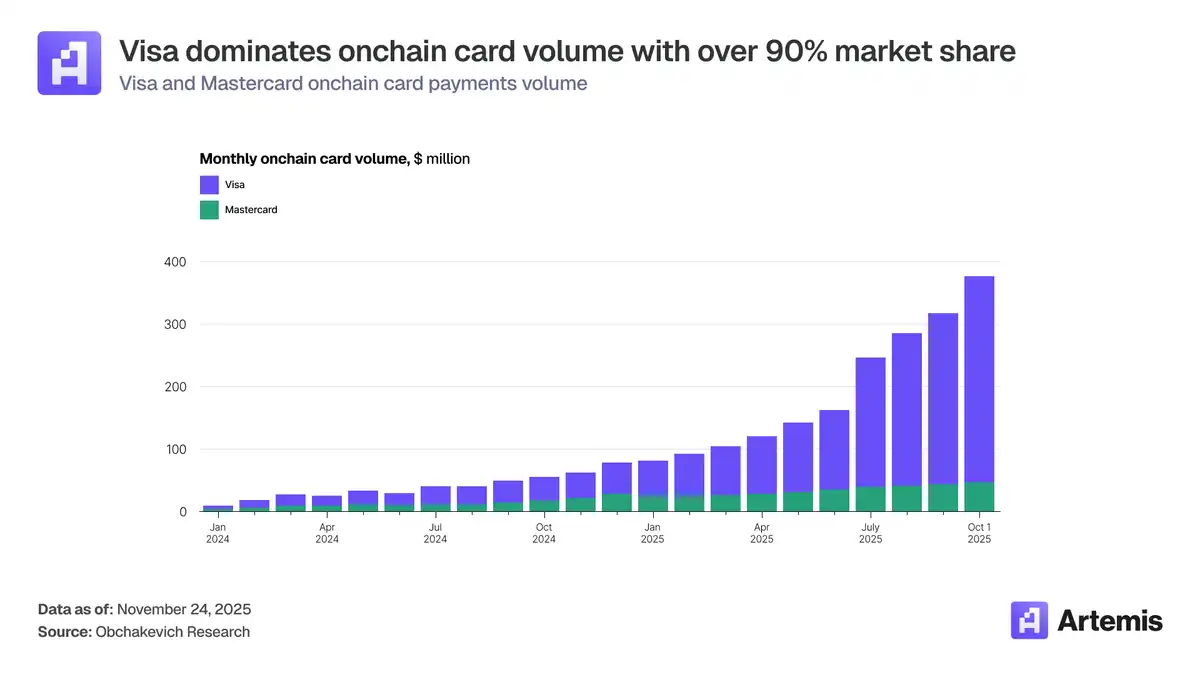

Not because it's a niche market, but because it has quietly grown into an $18 billion market. In early 2023, monthly transaction volume for crypto cards was only around $100 million. Today, that number has exceeded $1.5 billion.

To do this, we spent weeks digging deep into the data, the infrastructure, and the companies actually building this stack. Here are our key findings:

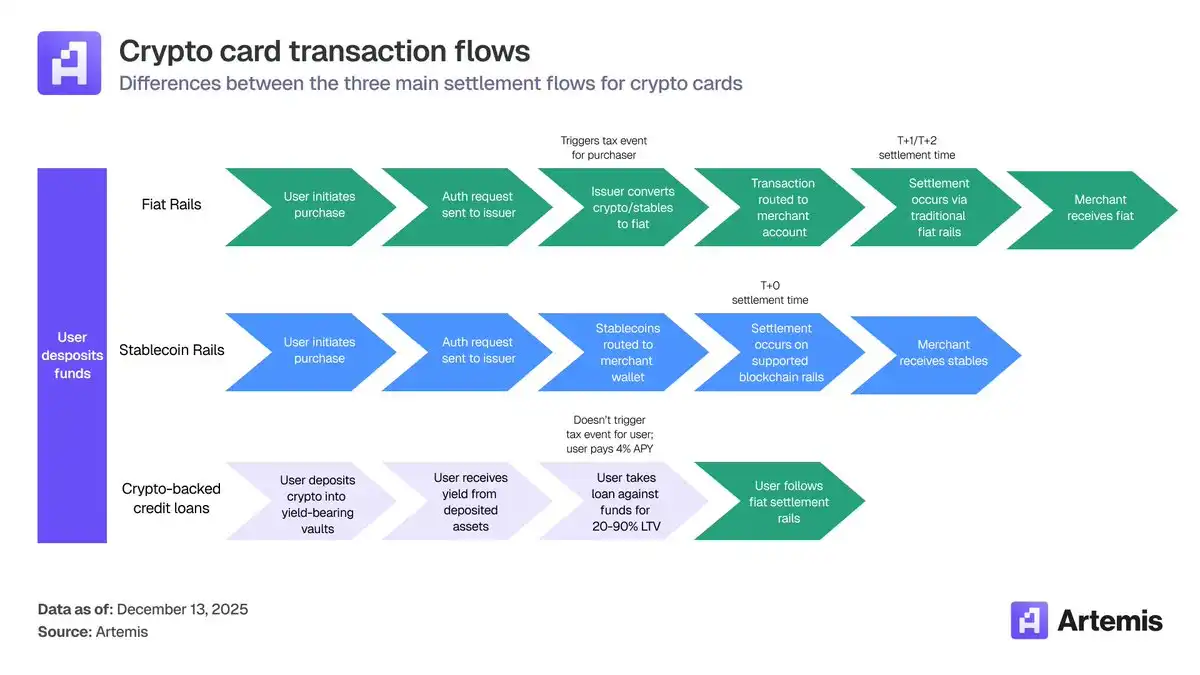

First, let's look at what's actually happening. Crypto cards aren't about replacing Visa or Mastercard; they're about leveraging them.

Stablecoins fund the transactions, and Cards provide the merchant acceptance environment.

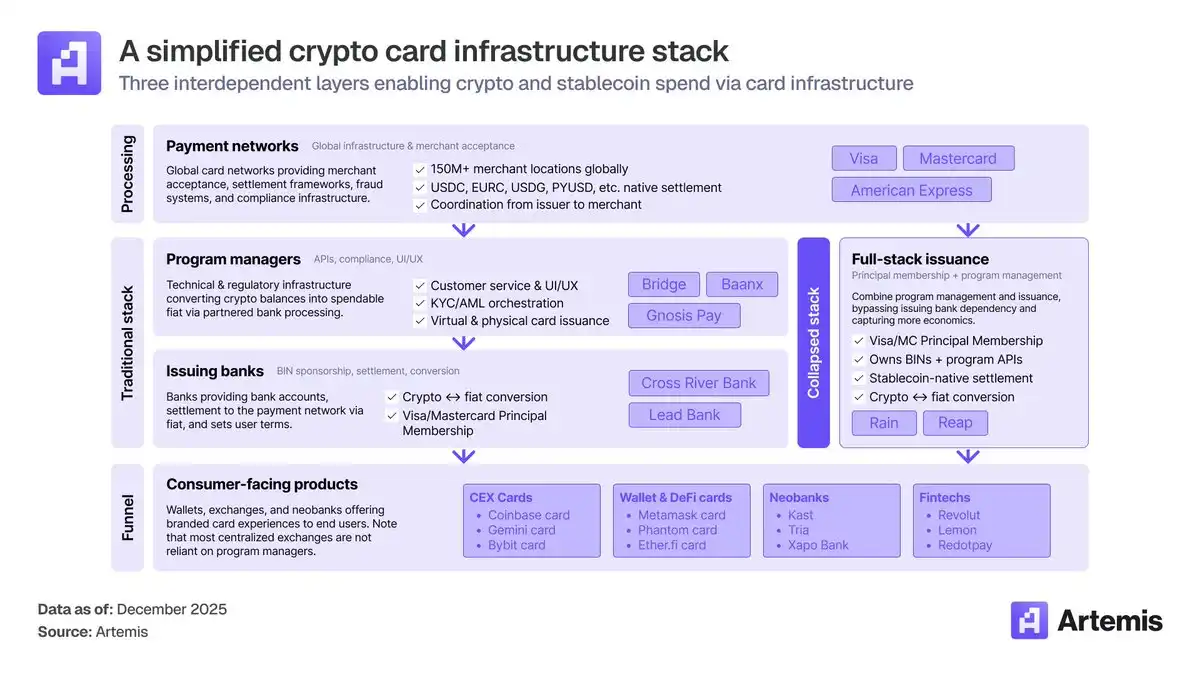

The stack is divided into 3 layers:

- Network Layer: Visa, Mastercard

- Issuers & Program Managers Layer: Baanx, Bridge, etc.

- Consumer Apps Layer: Wallets, Exchanges (e.g., MetaMask, Phantom)

This is precisely where the power struggle is most intense.

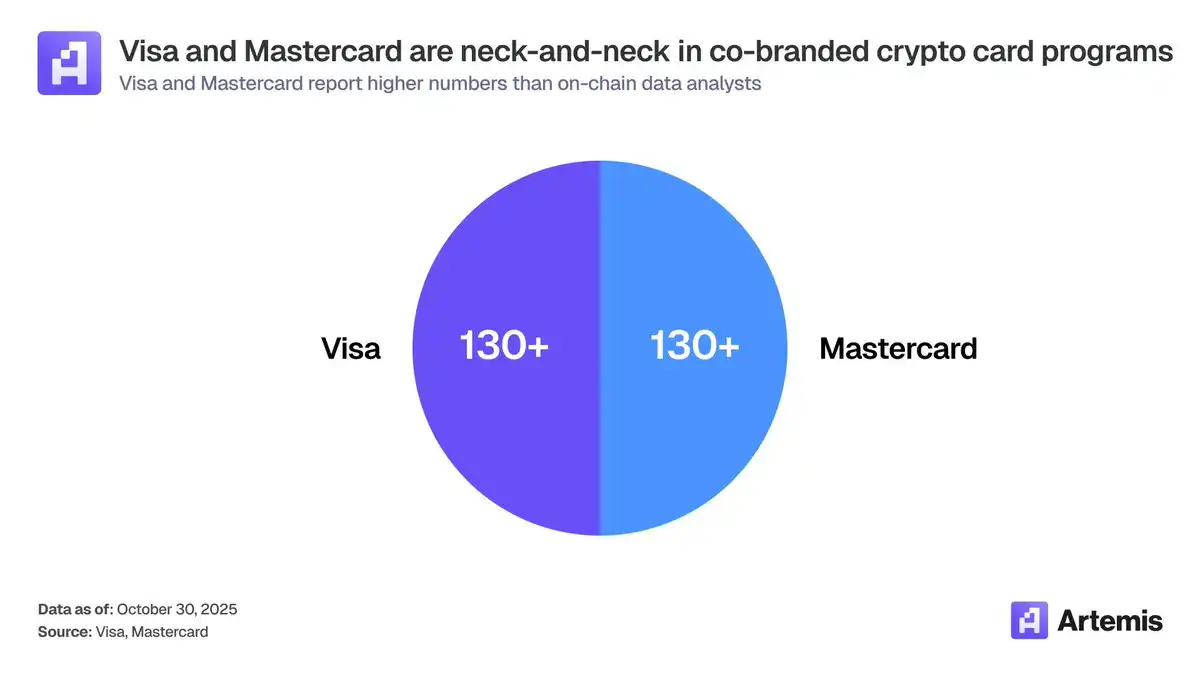

Although both Visa and Mastercard each have over 130 crypto partnerships...

Visa accounts for over 90% of on-chain card transaction volume. The reason lies in its early and deep partnerships with the Infrastructure Layer.

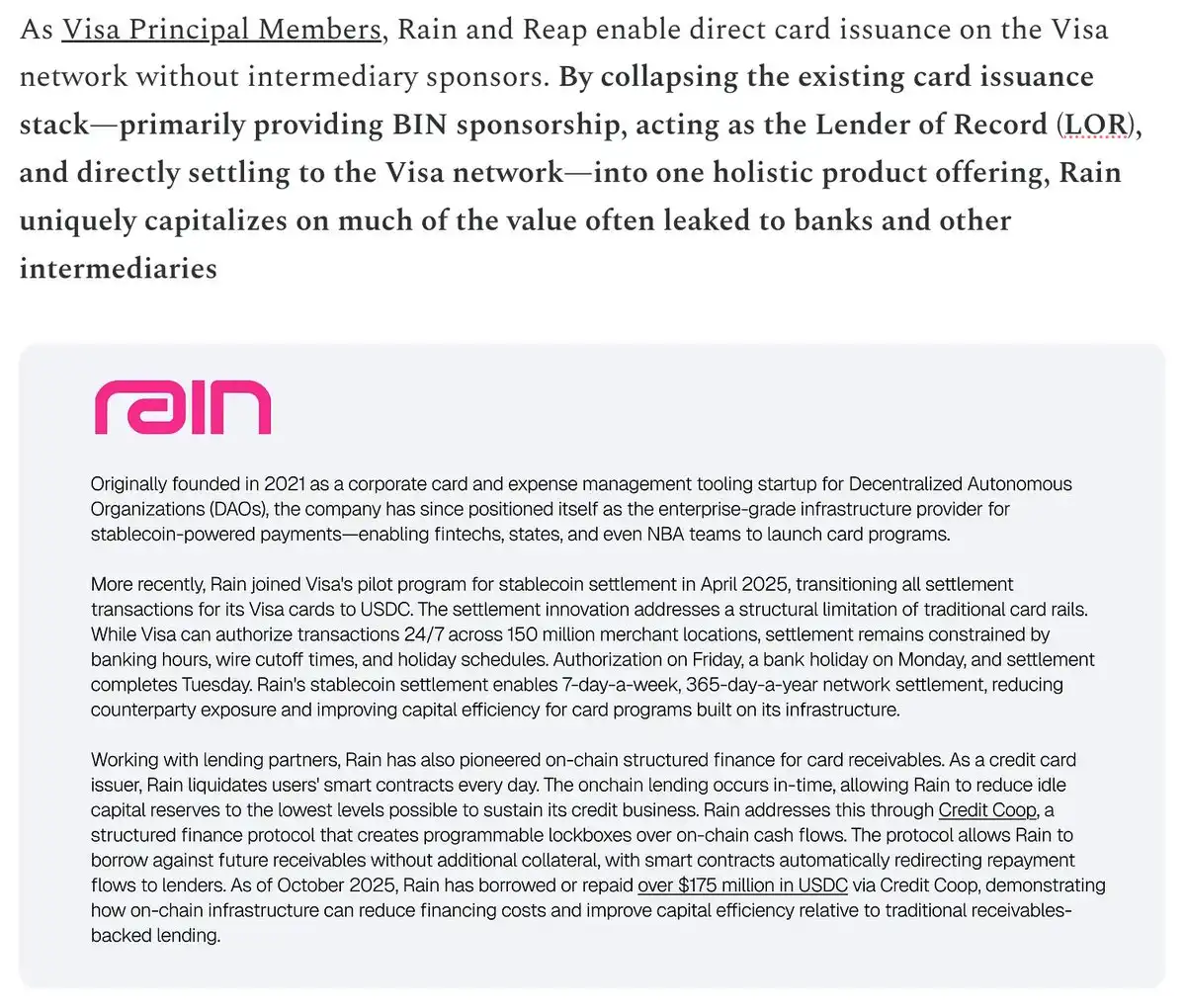

The biggest structural shift: Full-stack issuers.

Companies like Rain and Reap can now issue cards and settle directly as Visa Principal Members.

No sponsor bank needed. More control. Better economics.

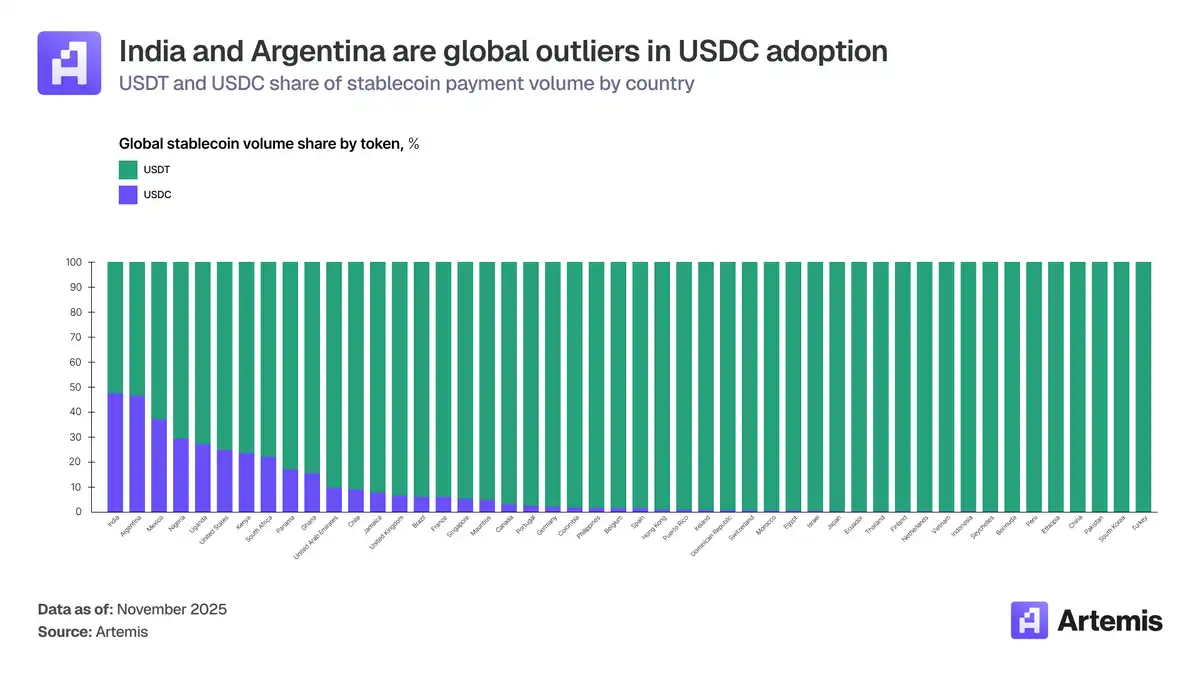

Geographic distribution reveals the real use cases. India: With $338 billion in cryptocurrency inflows. The opportunity here is crypto-collateralized credit (because UPI has already won in debit payments). Argentina: The practical application is stablecoin debit cards as an inflation hedge.

In developed markets, crypto cards don't solve a "critical need."

They target a new, high-value user base: those who already hold significant stablecoin balances and want to spend them.

Our view is simple: Stablecoins will continue to grow, and crypto cards will scale accordingly.

They are the infrastructure for bringing digital dollars into the real world.

This post is just the key highlights. Read the full report for the complete deep dive.