Author: Gu Yu, ChainCatcher

Last week, the severe backlash from BackPack was still vivid in everyone's minds, and today, another decentralized perpetual contract trading protocol, edgeX, is facing a tidal wave of criticism.

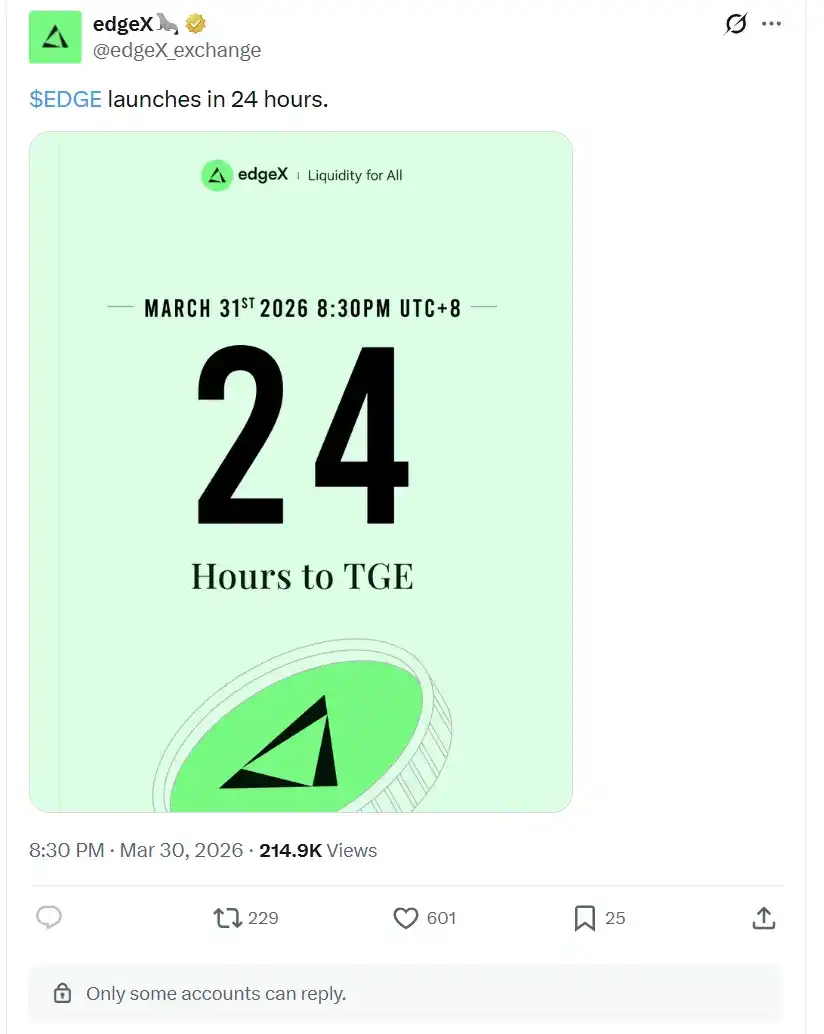

This morning, edgeX officially announced the website to check and claim the token airdrop, with plans to list on exchanges tonight. As a project incubated by Amber Group and strategically invested in by Circle Ventures this year, edgeX was once highly anticipated by airdrop hunters.

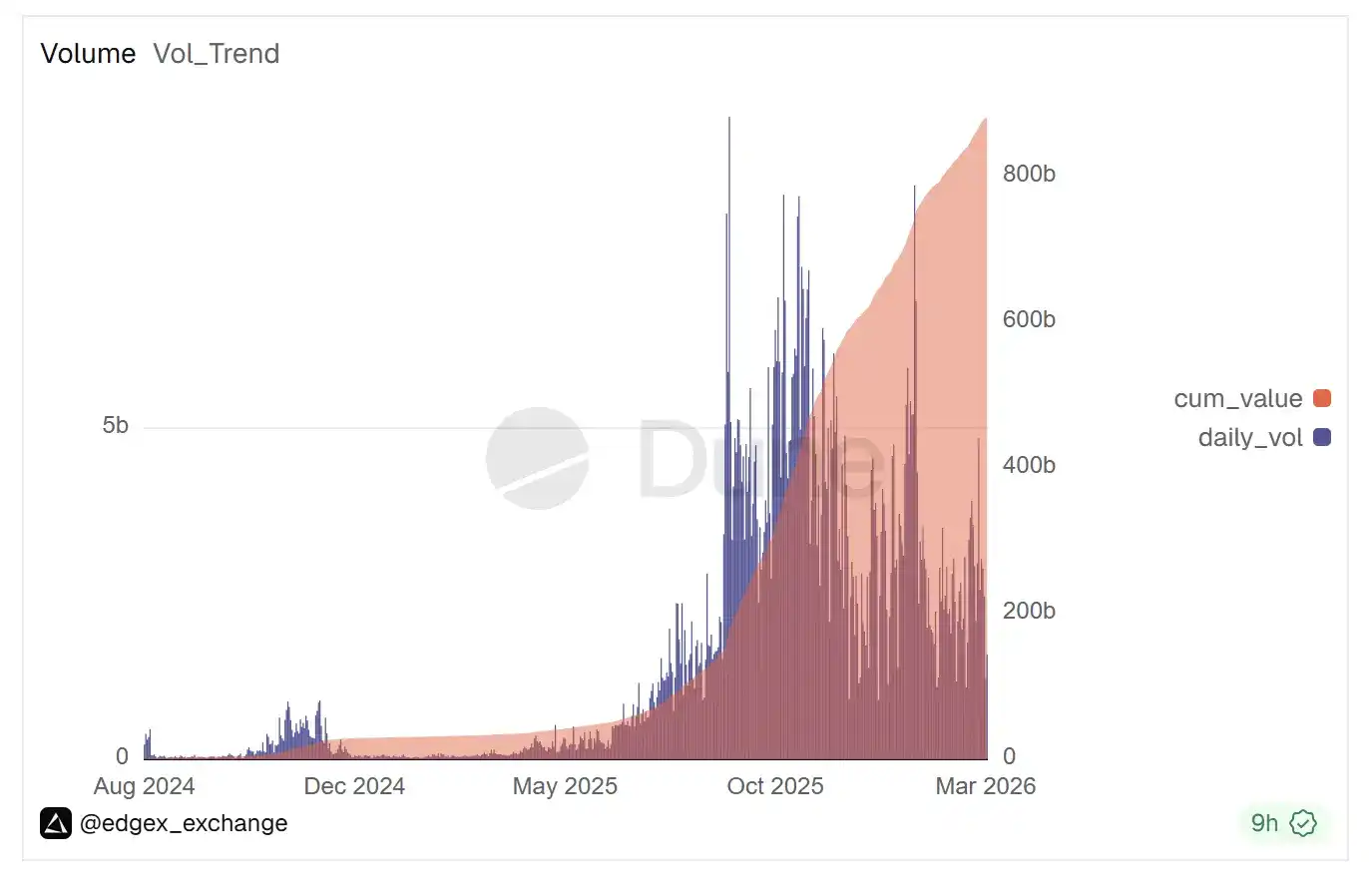

Since August 2025, edgeX's trading volume has entered a period of rapid growth. To date, it has accumulated over 470,000 user addresses, a total trading volume exceeding $87.7 billion, and a current Total Value Locked (TVL) of over $360 million. Furthermore, edgeX has generated over $180 million in fee revenue from these trades.

The edgeX team had previously promised the community that they would absolutely not screen for Sybil attacks—'if you have points, you get tokens'—which was a source of confidence for many edgeX users. However, what no one anticipated was that while edgeX indeed did not remove Sybil accounts this time, they manipulated the "points weighting" instead.

Based on community feedback, many users earned the same number of points through trading but received different amounts of airdropped tokens. Some users received 4 tokens per point on average, some only received 0.5 tokens per point, while others received 11 tokens per point. In response, the project team merely stated that points from different sources indeed had different weights.

Even calculating at the rate of 11 tokens per point, their current value is only about $5.5. In contrast, the secondary market price for edgeX points last year was $30-40, resulting in significant losses for secondary market buyers of these points.

What's worse, several KOLs, including He Bi, exposed that the edgeX project team engaged in a 'rat warehouse' situation (insider trading/preferential allocation), where multiple linked addresses with low points collectively received a quarter of the total airdropped tokens.

As community质疑声四起质疑 (questioning) grew louder, edgeX directly disabled comments on its X (formerly Twitter) account, attempting to suppress the spread of negative comments, but it was already too late.

"Why did they change rules arbitrarily, resulting in different rights for the same points? Why delete posts, kick people out, and suppress discussion? Because a project that from the very start intended to rely on wash trading to inflate data, hype valuations with stories, and coordinate with market maker groups for利益输送 (benefit transfer/insider profiteering) fundamentally cannot respect users, nor can it respect the community," said well-known KOL Ice Frog in an X post.

Ice Frog also stated that the most egregious aspect of edgeX is that it wasn't aimed at building a project from the beginning, but rather at setting up a scheme (a scam/plot), attempting to use manipulation and收割 (harvesting/exploitation) to destroy this industry.

Undoubtedly, this "post-rules" handling directly shatters the core premise of user trust in airdrop mechanisms—predictability. Once users cannot evaluate returns based on公开规则 (public rules), the so-called "points farming strategy" loses its博弈基础 (gaming foundation). One after another, large-scale "反向撸毛" (reverse airdrop/being rugged) and "作恶" (malicious acts) events continue to impact user confidence.

In fact, a significant portion of the trading volume and user activity on many yet-to-launch-token DeFi protocols comes from airdrop expectations. The seemingly massive community size and trading volume are built on this foundation. Once such projects complete their token launches and lose the appeal of potential收益 (returns/yields) for users, the false prosperity will quickly crumble. Once the expected returns from trading for airdrops are no longer certain or even become negative, the overall activity of the entire DeFi market could significantly decline.

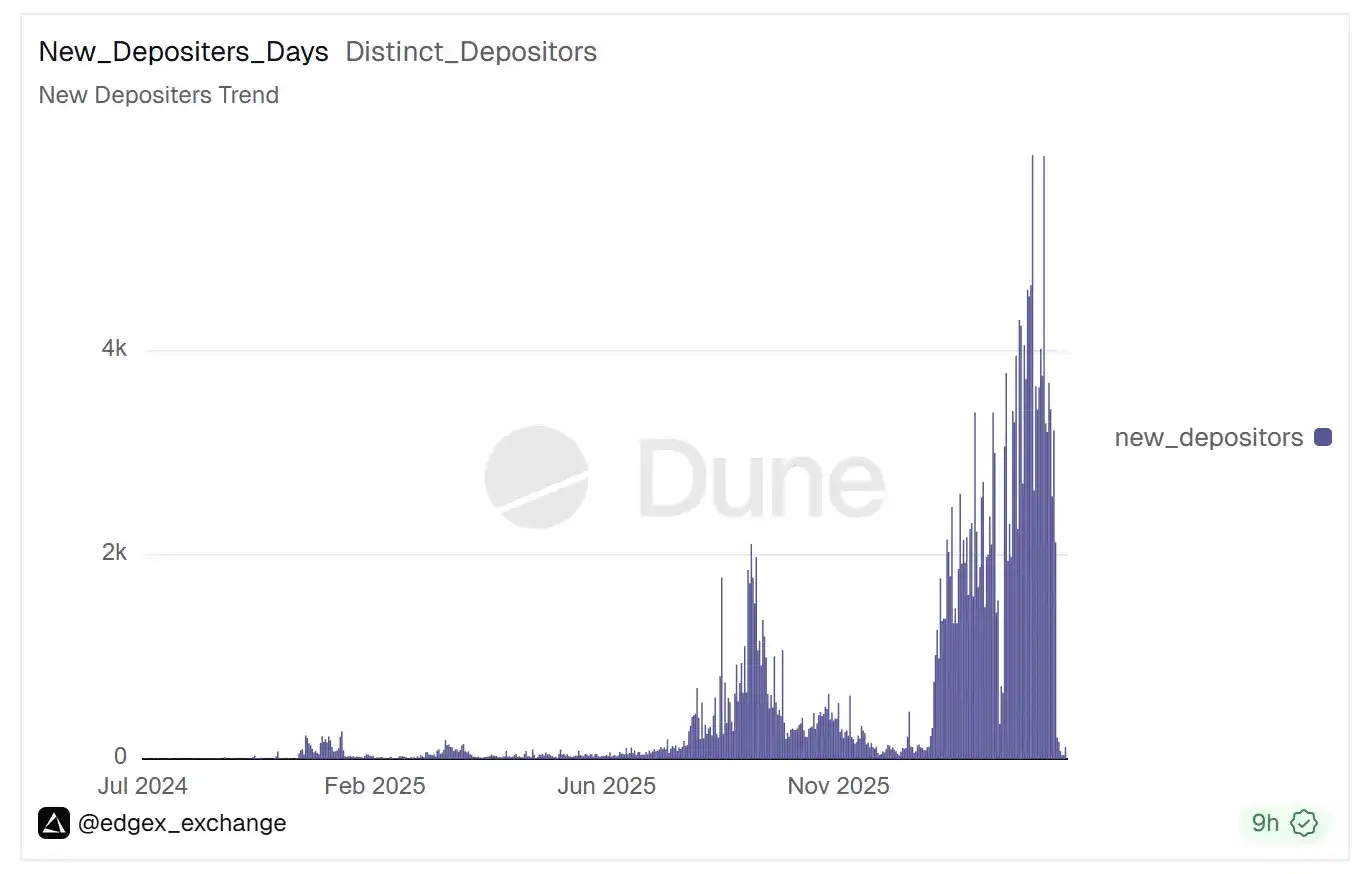

Taking edgeX as an example, in the days following the conclusion of the airdrop snapshot for this project, the number of new depositing users per day plummeted from over 2,000 to fewer than 50.

After the edgeX反向撸毛 (rug pull), what remains for the market is a series of question marks: How many people will continue to believe in "getting rich through airdrops"? As反向撸毛 (getting rugged) becomes the new normal and large numbers of airdrop hunters leave, will DeFi's trading activity and user stickiness continue to decrease?

When "反向撸毛" (reverse airdrops/rug pulls) evolve from isolated incidents into an industry consensus, the myth of getting rich through airdrops may have come to an end. For participants in the post-airdrop era, protecting the cash flow in hand might be more important than chasing those hard-to-verify "airdrop expectations."