Author: Claude, Deep Chao TechFlow

Deep Chao Introduction: The Q1 2026 earnings season for tech giants reveals a new phenomenon: while AI helps companies freeze hiring and cut positions, its own token consumption and GPU depreciation are inversely eroding gross margins. Shopify's subscription business gross margin is being suppressed by LLM costs, with about a quarter of Roblox's full-year margin guidance downgrade directly attributed to incremental AI investments. The combined AI capital expenditures of Amazon, Meta, Microsoft, and Google will reach $725 billion in 2026, a 77% year-over-year increase. For the first time, the two ends of the AI dividend—labor savings and compute consumption—are being accounted for on the same balance sheet in the same quarter, with the latter clearly larger.

The first-quarter earnings season is applying a corrective patch to the simplistic narrative of 'AI replacing labor.'

While a group of tech companies report successes in hiring freezes and accelerated product iteration, they are forced to explain a more棘手 question to investors: soaring AI chip depreciation and unpredictable token consumption are inversely eating up the money saved from layoffs.

Shopify President Harley Finkelstein stated at the May 5, 2026 earnings call that AI now handles over 50% of the company's code writing and helped Shopify deliver over 300 products and features while keeping headcount flat. However, in the same call, management also acknowledged that the gross margin of subscription solutions is being partially offset by large language model (LLM) costs, and this dynamic will persist.

Shopify: The LLM Cost Black Hole Behind an 80% Gross Margin

Shopify's Q1 subscription solutions gross margin was 80%, flat year-over-year, but the cost of maintaining this figure is changing.

According to Shopify's 10-Q filing with the SEC, subscription solutions costs grew 20% year-over-year in Q1 2026, reaching $148 million, compared to $123 million in the same period last year. Cloud and infrastructure costs (including AI-related usage) increased by $22 million as a single line item, being the primary driver of cost expansion. Shopify CFO Jeff Hoffmeister said on the earnings call that scale effects and support efficiency improvements were "partially offset by increased LLM costs, primarily driven by merchant usage of Sidekick, and we expect this dynamic to continue."

Sidekick is Shopify's AI assistant embedded in the platform. Its weekly active shops grew 385% year-over-year this quarter. Merchants used Sidekick to create over 12,000 custom apps this quarter, up more than 200% sequentially, with nearly half of Shopify Flows being AI-generated. AI-driven store traffic grew 8x year-over-year, and orders from AI search grew nearly 13x year-over-year.

But this explosion in usage means exponential growth in AI inference calls. Every interaction a merchant has with Sidekick, every proactive suggestion generated by the Pulse feature, corresponds to a token bill paid to upstream model providers.

Shopify explained the books for "internal AI" and "external AI" separately to investors: using AI internally for coding and controlling personnel expenses is a victory in the "cost game," while providing AI products externally to merchants is a strategic choice to "deeply tie infrastructure costs to merchant usage." Finkelstein summarized this logic on the earnings call as "AI is a structural advantage, not just a cost."

Roblox: One-Quarter of Margin Downgrade Directly from AI

Roblox CFO Naveen Chopra explicitly disclosed at the Q1 2026 earnings call on April 30 that about one-quarter of the full-year margin downgrade relative to prior guidance stems from incremental AI investment and adjustments to DevEx (Developer Exchange) for U.S. users aged 18 and above.

Roblox currently runs over 400 AI models on its own and cloud GPUs, processing 1.5 million inference calls per second, covering scenarios like discovery recommendations, communication safety, marketplace recommendations, and 3D generation.

Management is attempting to slice through inference costs via business model adjustments. Roblox Co-founder and CEO David Baszucki said on the earnings call that the company's upcoming "Roblox Reality" project, a technology capable of running 2K real-time photorealistic video models at 60Hz, will not be offered for free. "This will use cloud compute resources. We will have some form of subscription or payment mechanism, so we believe we can offset the costs on the real-time inference side," Baszucki explained.

Chopra added that the company's 2026 capital expenditure guidance remains unchanged, relying primarily on deploying GPUs in its own data centers to meet inference demand for the year, while some training tasks will still use the cloud. Roblox previously disclosed that by migrating some AI inference workloads from third-party clouds to its own data centers by the end of 2025, it had already achieved a 10x efficiency improvement in specific workloads like safety review and content discovery.

However, Roblox's quarterly full-year guidance includes multiple pressures: the aforementioned incremental AI investment, deleveraging of fixed costs due to lower-than-expected bookings scale, and the DevEx rate increase for 18+ adult content creators to 37.8%, ultimately triggering a market repricing of its full-year margin.

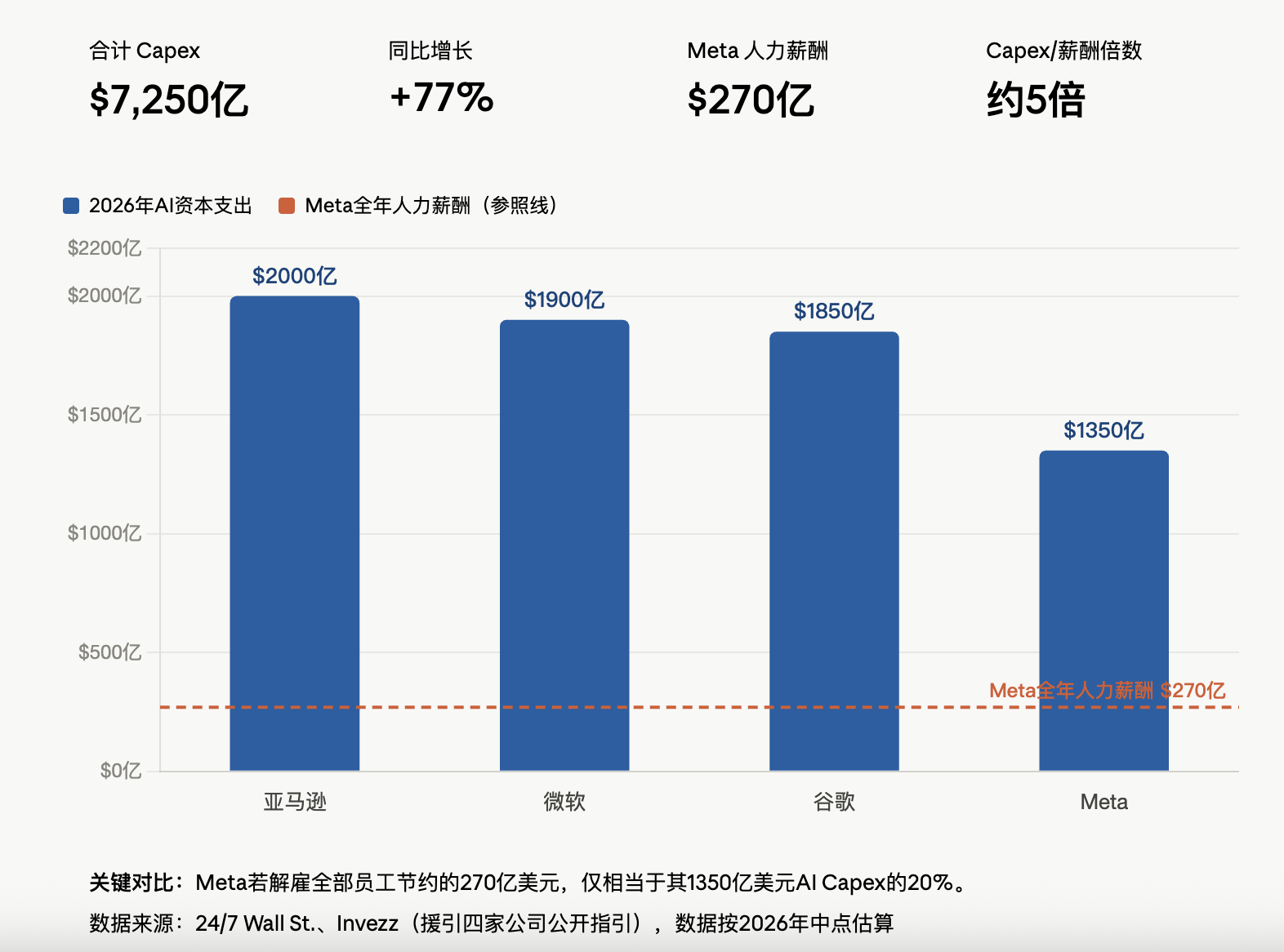

Industry Ledger: $725 Billion Capex vs. $2.7 Billion Salary Savings

The micro cases of Shopify and Roblox sit within a larger macro structural imbalance.

According to data cited by 24/7 Wall St., the combined AI capital expenditures of Amazon, Meta, Microsoft, and Google will reach $725 billion in 2026, a 77% year-over-year increase. Among them, Meta's full-year capex guidance is between $125 billion and $145 billion, meaning a daily expenditure of $370 million on data center construction; Microsoft's 2026 calendar year capex is $190 billion, with Amazon committing $200 billion.

This calculation is quite disproportionate compared to personnel expenses. Meta's total human compensation—all wages, benefits, stock-based compensation—amounts to approximately $27 billion. Even if Meta fired all its employees tomorrow, the savings would be less than one-fifth of its 2026 infrastructure expenditure.

Wedbush Securities analyst Dan Ives estimated in an April 25 research note that Meta's upcoming layoff of 8,000 people could free up about $2.4 billion in annual operating expenses, only offsetting about 12% of the incremental depreciation drag expected in 2026. In other words, for every dollar of financial pressure from AI compute expenditure, nearly ten dollars of human cost savings would be needed to fully offset it.

Meta CFO Susan Li positioned Meta's headcount reduction on the Q4 2025 earnings call as "building a leaner operating model to help offset the massive investments we are making." This statement clearly characterizes layoffs as a financial tool for AI capital expenditure, not a byproduct of productivity gains.

Victory for Model Providers, Dilemma for the Application Layer

The biggest beneficiaries of this ledger博弈 are the underlying model and compute suppliers. Microsoft Cloud gross margin held at 69% under the pressure of AI infrastructure expansion; OpenAI's gross margin is externally estimated at around 50%, Anthropic's at around 60%. Nvidia continued to report a gross margin level of about 70% in fiscal year 2026.

Application-layer companies, especially SaaS players that both consume AI and package AI capabilities into subscription products for sale, are facing a new financial structure: revenue is highly correlated with AI usage intensity, but the cost curve is dictated by upstream model provider pricing, and every model upgrade can bring new token consumption.

In his analysis of AI gross margins, Tanay Jaipuria points out that although the inference cost for a single model is declining at 80%-90% annually, the price of frontier models remains stable or even rises. If application-layer companies insist on calling the strongest model for every request, their Cost of Goods Sold (COGS) is effectively being led by the model providers' price cards.

Shopify's response is to position AI products as a strategic gateway deeply binding traffic and merchants, making the growth in inference costs a proxy indicator for "platform embed depth." Roblox's solution is to strip high-end AI experiences out of the free tier, forcing users to pay for inference costs. Behind both paths lies the same consensus: purely covering AI compute bills with savings from layoffs simply doesn't add up mathematically.