Original | Odaily Planet Daily (@OdailyChina)

Author | Azuma (@azuma_eth)

$292 million, this is the total amount of rsETH funds stolen from Kelp DAO; $17.2 billion, this is the scale of funds that have flowed out of Aave since the incident.

Aave is watching the community's panic sentiment ferment for several consecutive days due to its extremely foolish crisis PR strategy, thereby losing its once greatest advantage in the lending track—hundreds of billions of dollars in deposited funds and the user mindset label of "the safest DeFi".

- Odaily Note: For background, please refer to "DeFi Hacked Again for $292 Million, Is Aave No Longer Safe?" and "The Tripartite Game Under the $290 Million Hole: Who Will Pay the Bill—Aave, L0, or Kelp?".

What Did Aave Do Wrong?

The details of the Kelp DAO hack need not be repeated; blaming Aave for why it granted rsETH such a high LTV is meaningless now. Here, I mainly want to discuss Aave's response strategy after the incident from the perspective of a long-term AAVE user.

First is the bad debt scale issue; Aave itself has done the math. Depending on the different handling of rsETH, there might be two possible bad debt scenarios—if the stolen loss is written off from all rsETH in circulation, it is expected to generate $123.7 million in bad debt; if the value of mainnet rsETH is protected and the loss is fully recorded in the mapped version of rsETH on Layer2, it is expected to generate $230.1 million in bad debt.

In either case, Aave has the capability to cover it with its reserves from Umbrella, the DAO treasury, and the team. I understand that Aave is unwilling to pay this money itself and wants the main responsible party, Kelp DAO, and the secondary responsible party, LayerZero, to contribute as much as possible. But the problem is that the other parties will think the same way—"Aave is so rich, the situation is so awkward, it should bear more." Therefore, in the short term, it is difficult for these three parties to reach a consensus, which implies that a solution that satisfies everyone is temporarily impossible.

But users cannot wait that long—Aave's yield levels have never been very competitive in the industry. Users who choose to deposit with Aave are all attracted by its reputation, security, and liquidity. However, the situation now is that in the most critical days after the incident, Aave consistently failed to give users some kind of bottom-line guarantee promise, but instead kept emphasizing "our code has no problems" and "how rsETH is accounted for is beyond Aave's control" to shift blame.

This is why panic sentiment kept fermenting within the community. Users tried every means to escape and avoid risk: those who could withdraw directly did so, and those who couldn't went to borrow from other pools first, causing the impact to gradually expand. So Aave's current situation is: on one hand, it faces continuous fund outflows; on the other hand, multiple pools are experiencing liquidity drying up due to utilization rates being maxed out.

This awkward situation could have been avoided (or at least not been this bad)... Since Aave can afford the money, why didn't it inject a dose of reassurance into the community from the beginning to prevent a bank run? At most, it's $230 million in bad debt (possibly less), and this money wouldn't necessarily be paid by Aave alone;后续 could continue to dispute with LayerZero and Kelp DAO.

Now, it's done. For the sake of a promised relief of at most $230 million, Aave watched $17.2 billion in deposited funds flow out (the number may continue to grow), and this doesn't even include the decline in AAVE's price these days... No matter how you calculate it, it's a huge loss.

What makes Aave even more uncomfortable is that the worse its situation becomes, the more relaxed opponents like LayerZero and Kelp DAO will be, because they will judge that Aave will be more motivated to solve the problem as soon as possible, which only puts Aave at a disadvantage in the game.

Having reached this point, Aave has brought this upon itself.

Behind Aave, Spark Is Watching Covetously

While Aave is suffering from headaches, the situation of its competitor Spark is booming and extremely positive. What is even more lamentable is that Spark is actually a competitor "personally incubated" by Aave.

Spark was originally a lending protocol forked and developed by Sky (formerly MakerDAO) based on the open-source code of Aave V3; both sides actually use the same underlying code logic. In return, there was once a profit-sharing agreement between Spark and Aave, but later Aave accused Spark of涉嫌 breaching the contract, and coupled with route differences, the two are now purely competitive.

Three months before the Kelp DAO theft, Spark had just removed support for rsETH (for details, please refer to "Same Day, Different Fate: Aave Embraces rsETH and Loses Nearly $200 Million, Spark Exits Unscathed"). You call it strategic conservatism or rigorous risk control, or even attribute it entirely to luck, but the result is that Spark was not affected at all in this incident—on this point alone, Spark can wantonly attack Aave's former "safest DeFi" label.

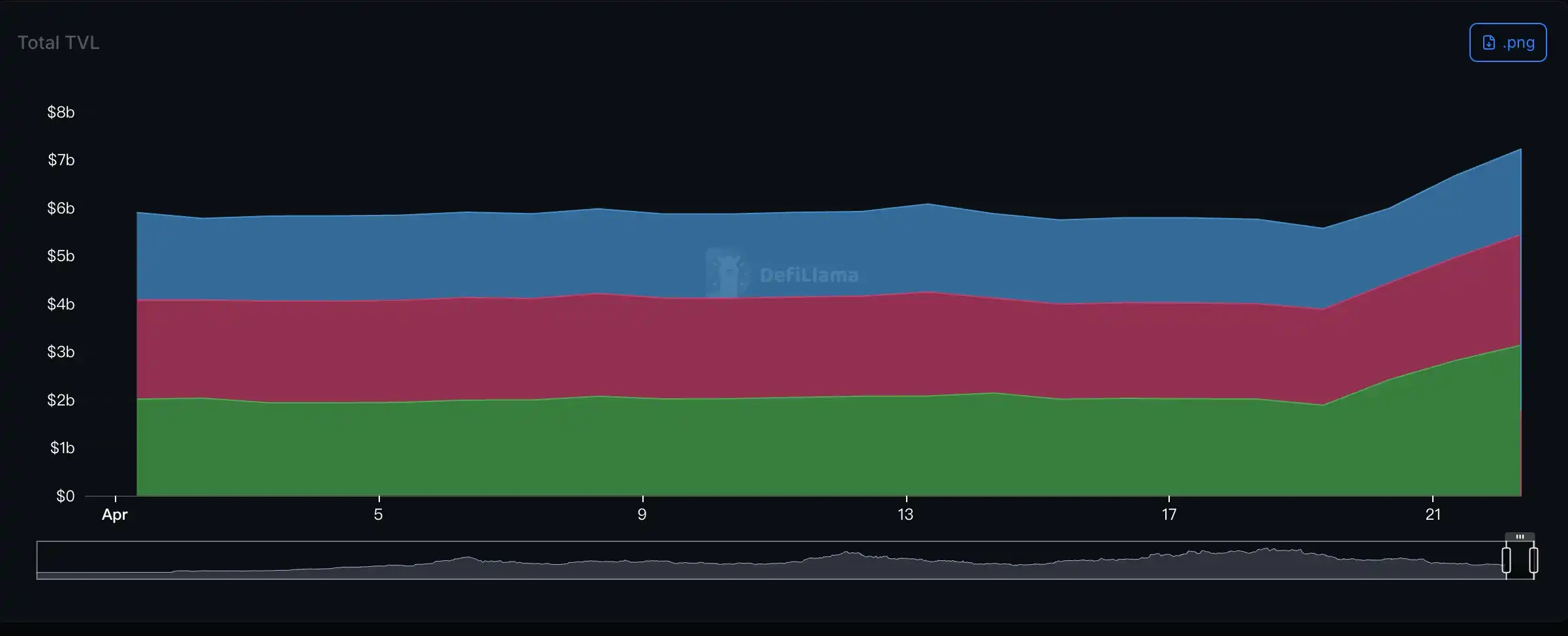

Thus, Spark became one of the safe havens for funds fleeing Aave. Since the incident, Spark's TVL has grown by nearly $2 billion (green part in the chart below). On the day of the incident, Justin Sun withdrew 53,665 ETH (worth $124 million) from Aave and subsequently deposited it into Spark. After continued accumulation in recent days, the total deposit has reached $1.3 billion—in the DeFi world, Brother Sun's operations are really something to learn.

On April 23, Upbit officially announced the launch of the Spark (SPK) Korean Won trading market. SPK, stimulated by this positive news, rose over 80% in a single day, significantly narrowing the market value gap between itself and AAVE.

Even Wang Chun, founder of F2Pool, lamented on X: "In the past year, I received 83.7 million SPK rewards from Spark and sold them on CoWSwap for 663 ETH and $1.4 million. Now I kind of regret it."

Spark clearly realizes that this is a perfect opportunity to seize market share from Aave's mouth. Since the incident, Spark's Strategy Lead, MonetSupply, has almost become the most frequent KOL speaking out on this matter, posting dozens of times a day. Although his发言 can indeed help the public understand what happened, it objectively also加剧 the panic sentiment surrounding Aave.

But this is the purest商业 competition; MonetSupply just made the most correct choice.

Aave Is Losing the Throne of DeFi Lending

In the early morning of April 24, perhaps realizing the严峻 situation, Aave founder Stani announced on X the launch of a relief plan called DeFi United. Cooperative participants include LayerZero, Ethena, ether.fi, Ink Foundation, Golem Foundation, Trydo, etc. Stani personally will also donate 5,000 ETH to solve the current problem.

But the funds have already flowed out, and user trust has been severely damaged. Relying solely on this belated statement, Aave will find it difficult to regain deposited funds and user trust in the short term.

The DeFi lending track has long presented a pattern of "one superpower, multiple great powers," with Aave一直以来 having seemingly extremely solid leading advantages. But now, Aave is拱手 surrendering the throne. Behind it, challengers are coming aggressively; besides the booming Spark, other opponents like Morpho and Jupiter Lend also hope to take a bite out of Aave's share.

Last year, Stani bought a five-story luxury house in London for approximately $30 million, one of the most expensive transactions in the UK's sluggish luxury real estate market in the past year. I don't know if there is something like a "jinx," but with precedents like Su Zhu and others, it seems that big shots who consume conspicuously within the circle always run into some倒霉事.

I can't guess what Stani is thinking right now in his five-story luxury house.