On May 28th, Murata Manufacturing, the world's largest passive component manufacturer, surged 12.36% on the Tokyo Stock Exchange, briefly hitting its daily price limit during the session. It closed at 8,787 yen, marking a new all-time high on a split-adjusted basis. Two months ago, we analyzed Murata's 15-35% price hike on MLCCs (Multilayer Ceramic Capacitors) for AI servers, explaining how this sub-millimeter capacitor is stirring up the AI computing supply chain. This time, what's worth unpacking is not the capacitor, but Murata's stock itself.

Because if you look at Murata's latest earnings report, you'll find a stark contrast: its performance is actually quite flat, yet its stock price has doubled over the past year.

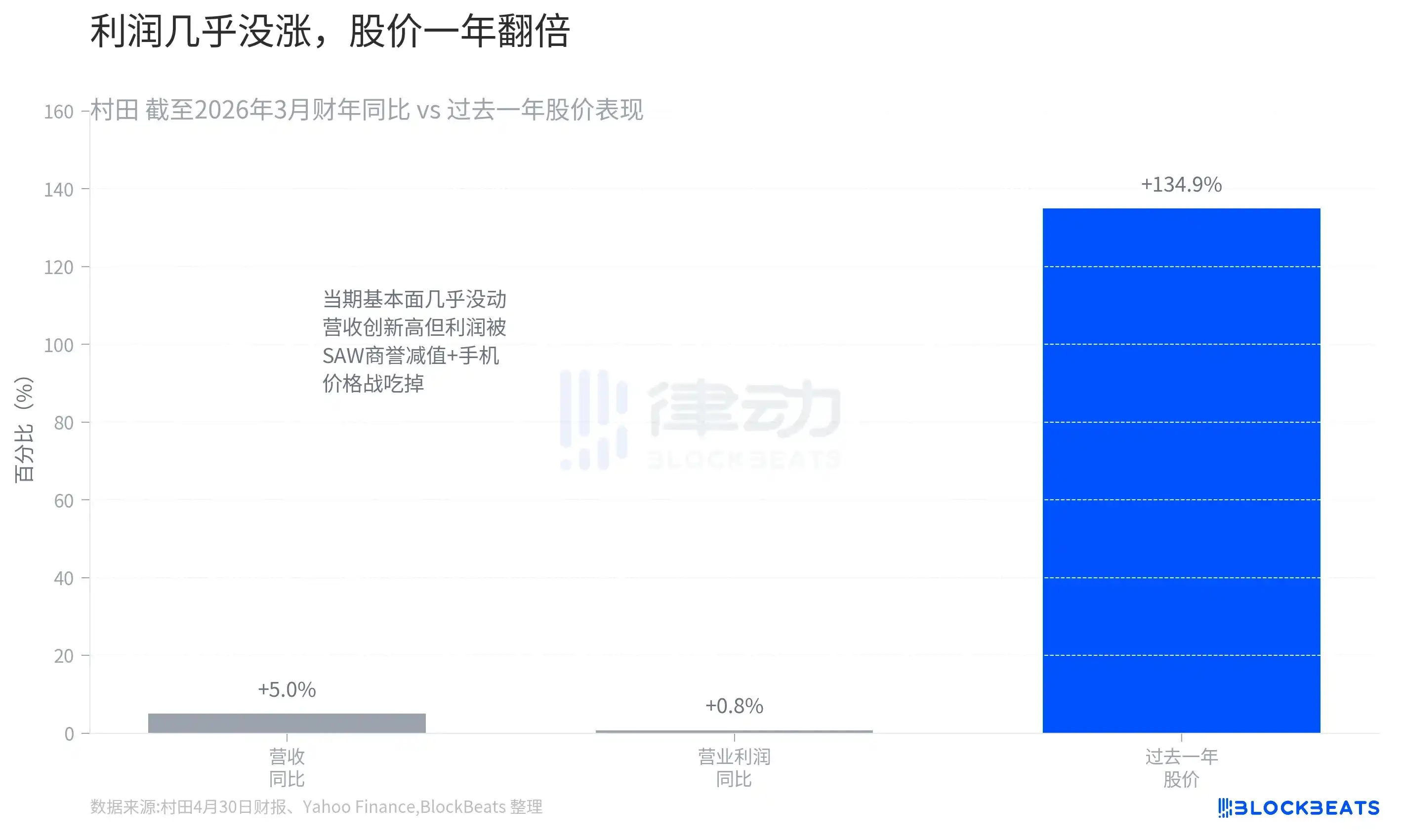

According to Murata's April 30th earnings report for the fiscal year ending March 2026, the company's revenue reached a record high of 1.83 trillion yen, but grew only 5.0% year-over-year. Operating profit was 281.8 billion yen, increasing a mere 0.8% YoY, essentially stagnating. Two factors dragged down profits: a goodwill impairment related to its SAW (Surface Acoustic Wave) filter business, and continued price wars in mature applications like smartphones. In other words, no matter how bright the AI segment shines, it's only making up for the losses in the mature businesses.

Yet during the same period, Murata's stock price rose approximately 134.9% over the past year (according to Yahoo Finance data), recently breaking above the 9,000 yen level. Its market capitalization has surged to around the 17 trillion yen level, pushing its P/E ratio to about 75 times. The market valuing a passive component maker with zero current profit growth at a 75 P/E ratio can only mean one thing: the buyers don't care about this year's profits—they are betting on the story ahead.

The real catalyst was a briefing

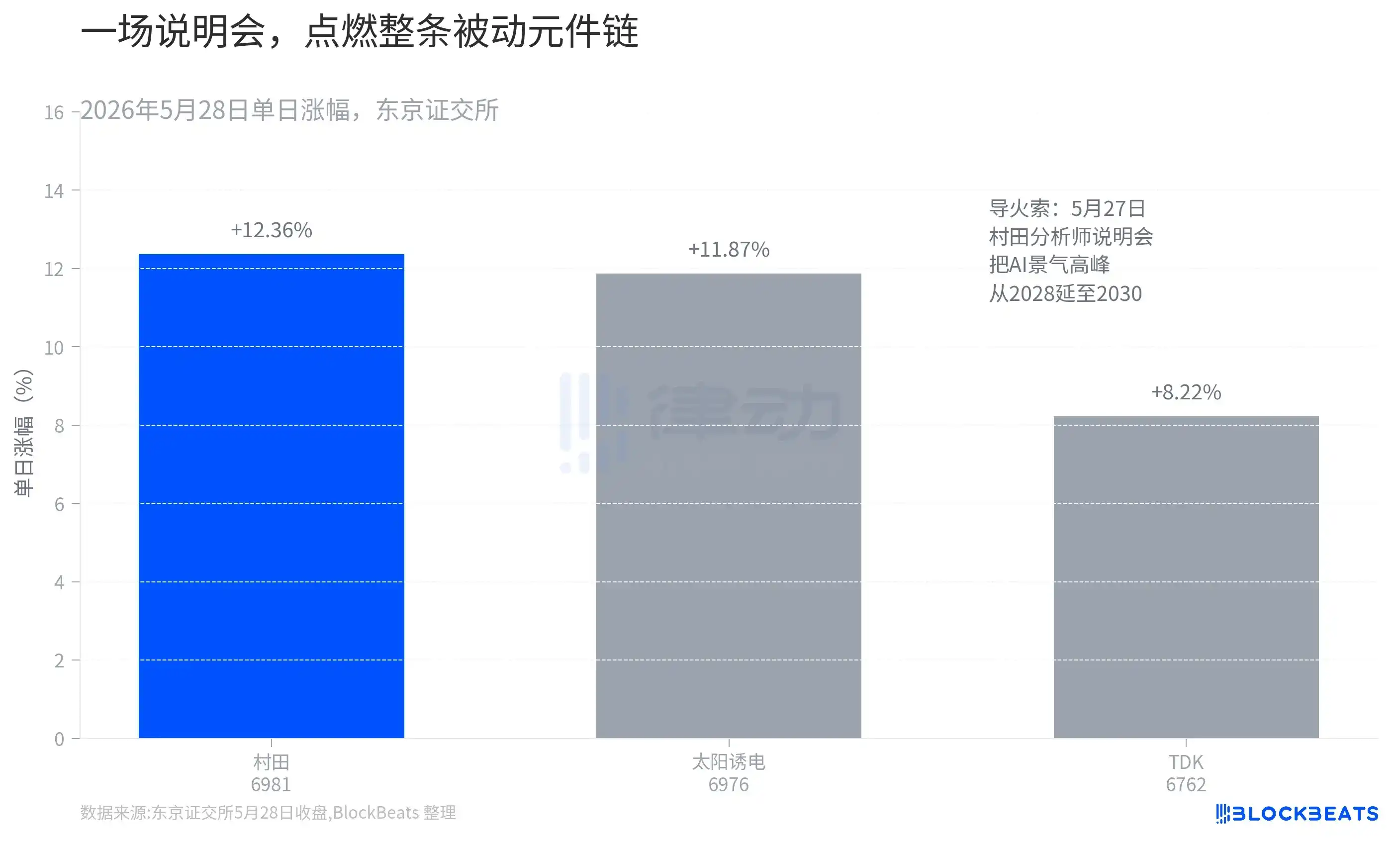

The trigger for this surge wasn't a price increase or the earnings report, but a small meeting for securities analysts held by Murata on May 27th.

According to content from the meeting cited by investment blogger kabuya66, Murata's management delivered two key statements. The first was an upward revision of the expected AI investment peak from "around 2028" to "likely continuing until around 2030." For a capital-intensive component manufacturer that plans production based on orders, an extra two years of robust demand cycle means order backlogs will continue to accumulate, making investments in capacity expansion more certain to pay off. The second statement was more direct: customers now prioritize securing volume over price, with demand being roughly double the available capacity. This means downstream players are scrambling for supply regardless of cost, just to get their hands on the components.

The impact of these statements was evident in the next day's trading. While Murata jumped 12.36%, peers Taiyo Yuden rose 11.87% and TDK climbed 8.22% (based on Tokyo Stock Exchange closing data). A single briefing from the industry leader led to a re-rating not just of one stock, but of the entire passive component chain. That day, the Nikkei 225 index also closed above 66,000 points for the first time, with the MLCC sector being one of the leading gainers.

What the market is buying is the "next year" pillar

The reason the briefing ignited such a rally is that it clarified Murata's potential profit elasticity for the coming year.

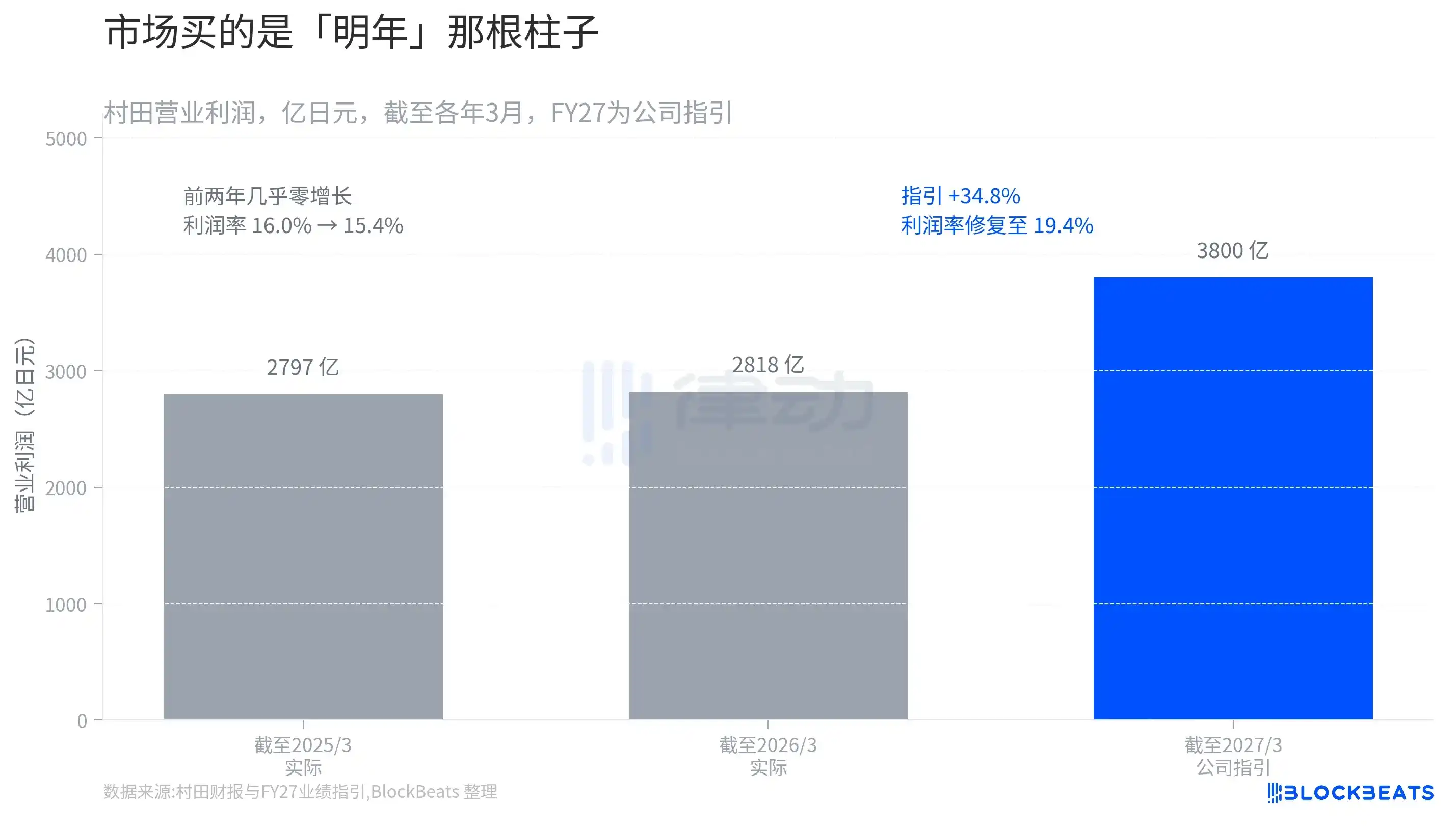

Visualize Murata's operating profit as three pillars, and the story becomes clear. For the fiscal years ending March 2025 (279.7 billion yen) and March 2026 (281.8 billion yen), profit was nearly flat for two consecutive years, with the operating margin also declining from 16.0% to 15.4%. However, Murata's guidance for the current fiscal year (ending March 2027) is an operating profit of 380 billion yen, a sharp 34.8% increase year-over-year, with the margin rebounding to 19.4%.

All the growth is locked into that rightmost pillar. The market is now buying not the past two years of flat performance, but this yet-to-be-realized guidance pillar. Supporting evidence comes from orders: according to a Nikkei Veritas survey, among listed companies with a market cap over 50 billion yen and expected profits this fiscal year, Murata ranked first in the growth rate of its order backlog last fiscal year. The order backlog directly translates to future revenue, providing the confidence behind that guidance pillar. Murata also announced a share buyback plan of up to 150 billion yen, aiming to repurchase 75 million shares, or 4.12% of its outstanding stock. Management's commitment of real money is an implicit admission that the current price isn't considered expensive.

What supports this pillar is AI revenue set to double again

Where does the 34.8% profit growth come from? The answer lies primarily in one segment.

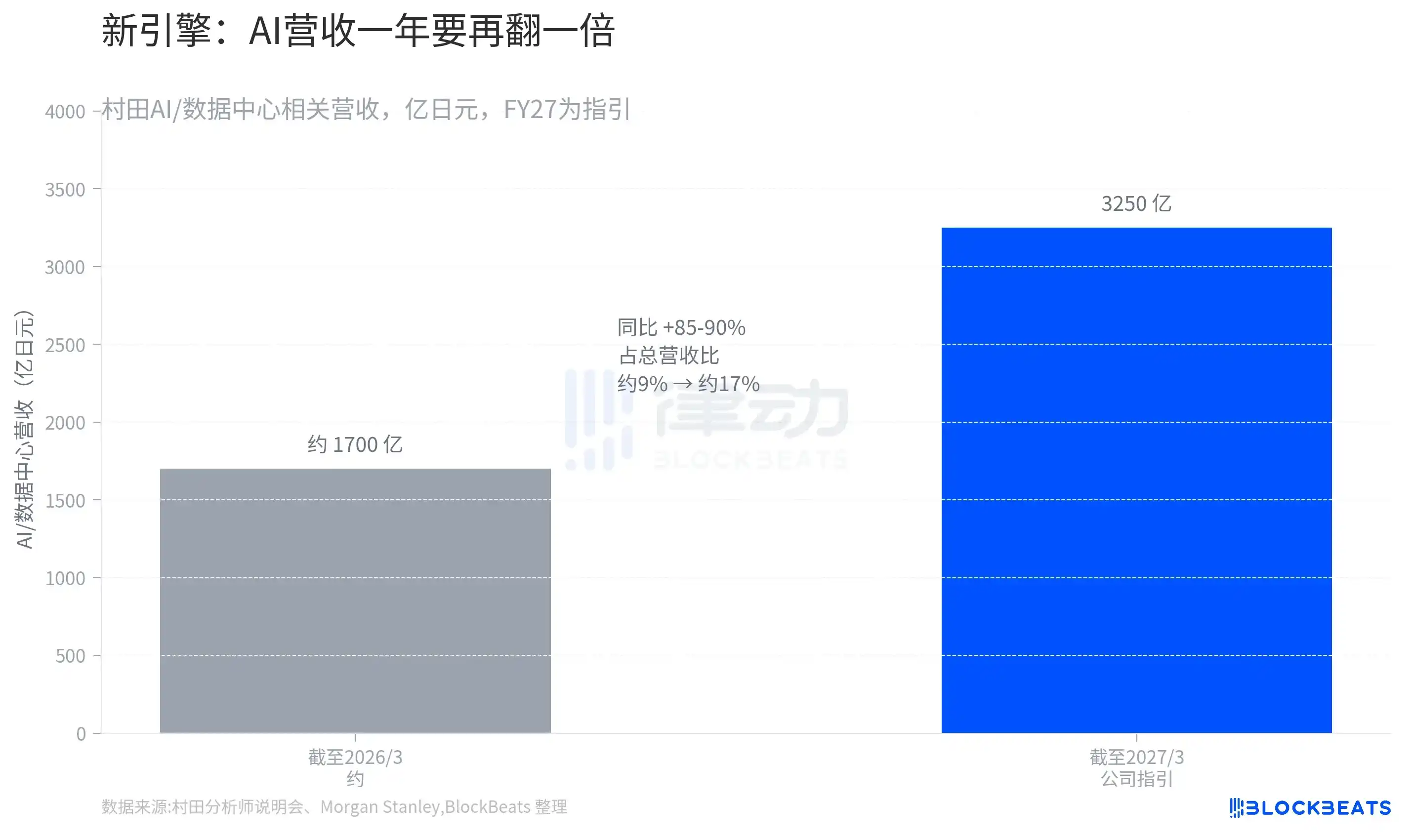

According to data from Murata's briefing, the company's AI/data center-related revenue is projected to jump from about 170 billion yen last fiscal year to a guided 325 billion yen this fiscal year, an increase of 85-90%. This segment's contribution to total revenue will rise from roughly 9% to about 17%. In other words, within a year, AI will grow from a minor part of Murata's revenue to a pillar accounting for nearly one-fifth of the total.

More crucial is the "quality" of this growth. According to analysis by Morgan Stanley MUFG Securities, this round of AI revenue growth for Murata is not primarily driven by price hikes on existing MLCC products, but by product mix upgrades—an increased proportion of cutting-edge products with smaller sizes and higher capacitance values, which pushes up the average selling price (ASP). Murata holds over a 70% share in the advanced-grade MLCCs required for AI servers, with almost no competitors able to keep pace. This means its price increases are not cyclical "price hikes due to short supply," but structural "higher prices because only we can make them." The market's willingness to assign a 75 P/E ratio is precisely pricing in this perceived sustainable pricing power.

Of course, the flip side of buying expectations to a record high is that expectations have already run ahead. Murata's President, Norio Nakajima, himself acknowledged the possibility that some customer demand forecasts might be "on the optimistic side." If the pace of AI investment slows, or if quarterly guidance subsequently falls short of expectations, this high valuation also carries the risk of a rapid correction. For high-multiple stocks, "not good enough" can be the best reason to sell.

Murata is still the same capacitor maker it was. What's changed is the yardstick the market uses to measure it: from a "destined for price declines" cyclical component manufacturer to an "AI picks-and-shovels" supplier with constrained supply and strong pricing power.