Author: Campbell, Macro Analyst

Compiled by: Yuliya, PANews

Editor's Note: Recently, the US stock market's memory chip sector has become the main theme of the technology rally, with companies like Micron Technology, SK Hynix, and SanDisk continuing to surge. At the same time, debates about whether AI has entered a bubble phase have heated up again. Opinions in the market are divided: Dan Niles, a renowned chip analyst from the internet bubble era, believes the current AI development is closer to the mid-stage sprint of internet infrastructure construction in 1997, not the tail end of the bubble in 1999. He points out that the rise of AI agents is driving a sharp increase in computing power demand; although chip stock valuations are high in the short term, they still have long-term potential. Hedge fund legend Paul Tudor Jones also predicts that the AI bull market is currently about 50% to 60% complete and might last another one to two years. In contrast, Michael Burry, the inspiration for the protagonist of *The Big Short*, has issued a warning, seeing strong similarities between the current market and the pre-crash period of the 2000 internet bubble.

Amidst the intertwining of狂热 and担忧, with big names holding opposing views, if a bubble truly exists, how should we actually respond? The author of this article shares a hands-on guide on "how to short a bubble" based on personal experience. Below is the original article:

To be honest, I don't know if we are in a bubble right now. I'm not even sure if that's a knowable question. I know about as much as you do: the AI revolution is real.

Even though I gave up my professional investing career to go long, and have been writing about it for the past three years, I still feel like I'm not long enough. I look around like you do, see people getting incredibly rich just by stringing tokens together for AI apps (or going all-in on those infrastructure projects providing蒜力 for generating these tokens), and it gives me chills and fills me with envy. This then triggers a feedback loop where I can't tell if my view is being colored by jealousy, or if the jealousy is telling me something I already know: "Keep going long."

To some extent, I really feel like "the future is here, and we need massive amounts of computing power", so you really do want to buy these assets.

I don't think software stocks have performed all that well, and the market is selling them off, so there's not much fat to trim there.

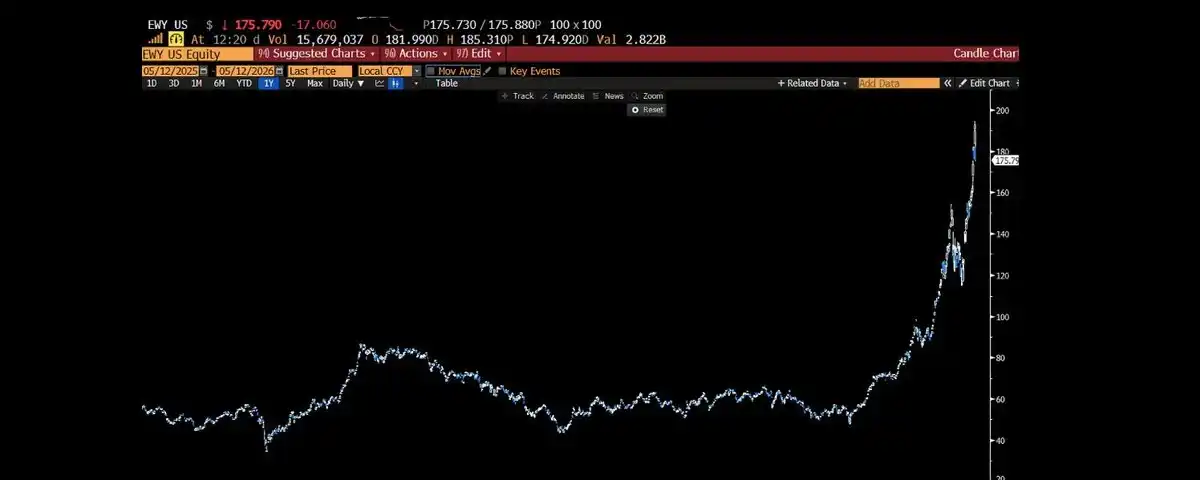

Like you, I've also noticed the extremely low valuations of South Korean stocks and am intrigued by the opening up of their market, which is clearly tied to the recent stock market surge.

I was also surprised by the quiet easing of the supplementary leverage ratio (eSLR), where banks and funds are allowed to hold less regulatory capital to buy US Treasuries. It's classic money printing in sheep's clothing.

-

I can imagine a day when interest rates rise enough to pull the plug on this "liquidity party," but that day is not here yet.

-

I can also imagine war ending the party; the violent swings there shook me out of the uptrend, so who knows what the future holds.

-

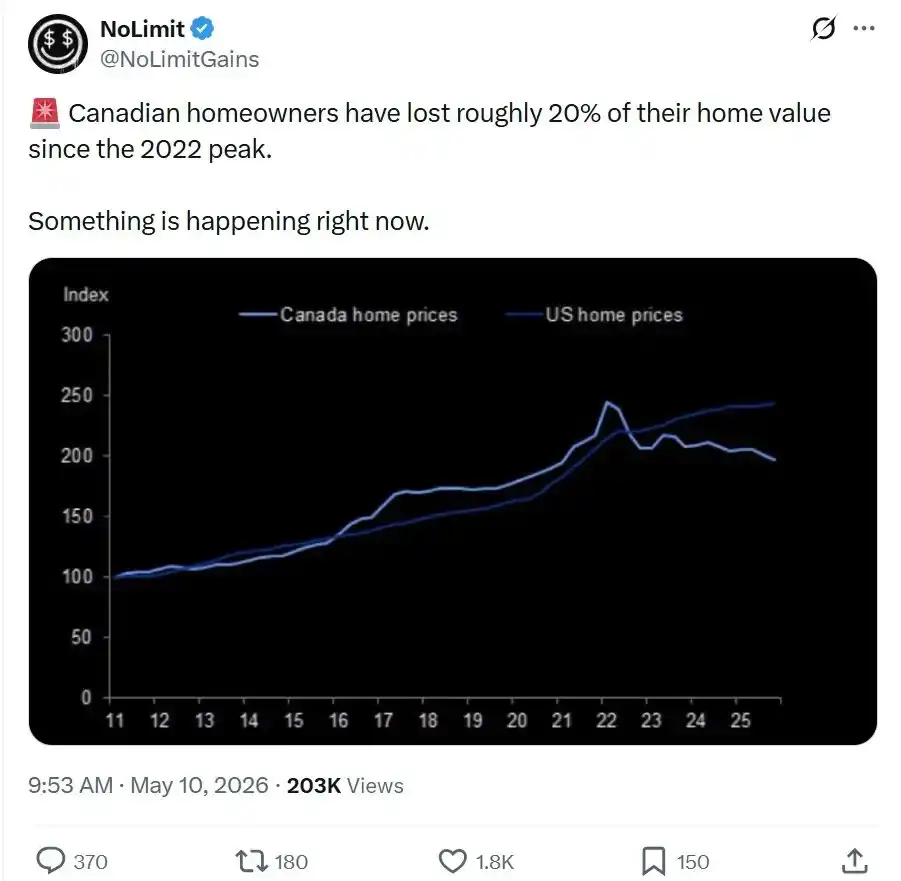

I can also imagine that Canadian bank stocks with price-to-book ratios as high as 3x and low volatility are a fantastic short opportunity, but I can't write a good article with actionable干货 for you because of a lack of trading channels and sufficiently long-dated options.

Frankly, there's a lot more I can't say explicitly here. This doesn't change my fundamental view on the trend, but it greatly limits the people and things I can discuss here. If you know Andreesen's "It's Time to Build" thesis, you'll know that my cautious, worrying personality注定 I'll never become a billionaire.

But there's one thing I know how to do. It's also a little bit of Alpha I can give you. We're not going to discuss today whether we are in a bubble, but rather, if you want to, how you should go about shorting a bubble.

Why Is Shorting a Bubble So Difficult?

What is a bubble? If something looks like a bubble, sounds like a bubble, moves like a parabola shooting to the sky, and requires ever-higher expectations and leverage to sustain price increases, then it's a bubble.

Why are bubbles so hard to short?

The problem is, the easiest things to short are those where negative fundamentals gradually become known to the public, then they grind down and finally collapse. You might face a short squeeze along the way (forcing shorts to buy to cover, causing a surge), but that反而 provides a good opportunity to add to your short, because this thing is eventually going to zero.

But shorting a bubble is an entirely different matter. When an asset price rises insanely in an unsustainable manner, your short risk exposure放大 exponentially as the price goes up.

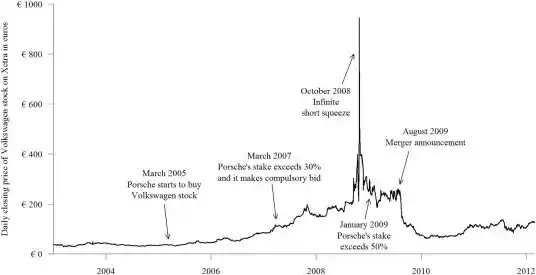

Just ask the people who shorted Porsche and Volkswagen in 2008.

Ask the people who shorted GameStop.

Or ask the people who shorted that unknown shoe company a few weeks ago that somehow turned into an AI company and crushed all shorts.

If a long sells, they simply sit in cash. But if a short sells, it means they must buy back tomorrow to cover their position and settle. If you can make their bill quintuple, they will have double the incentive to cover, sometimes at any cost.

Another reason bubbles are hard to short is that the very features that make them look so exciting—"explosive volatility! Awesome!"—make their options ridiculously expensive.

If it goes up 10% daily, the annualized volatility is 160. For options with volatility of 160, buying a call today could cost you half the stock price. Because the hedging value from actual volatility is so high, these options are practically unusable for directional bets.

So, we are left with the following few paths.

The only ways to short a bubble are:

a) Find the "Wedge"—find something external that can pop the bubble.

b) Short the "Victims"—bet on things related to the bubble that will fall into an abyss.

c) Wait for "Confirmation"—wait for the trend and charts to truly break down.

The rest of this article will be examples of each method.

A) Finding the Wedge

The first method to short a bubble is to not directly short the bubble itself.

You need to find the thing that will pop the bubble. Then you buy it to protect your portfolio from the bubble bursting.

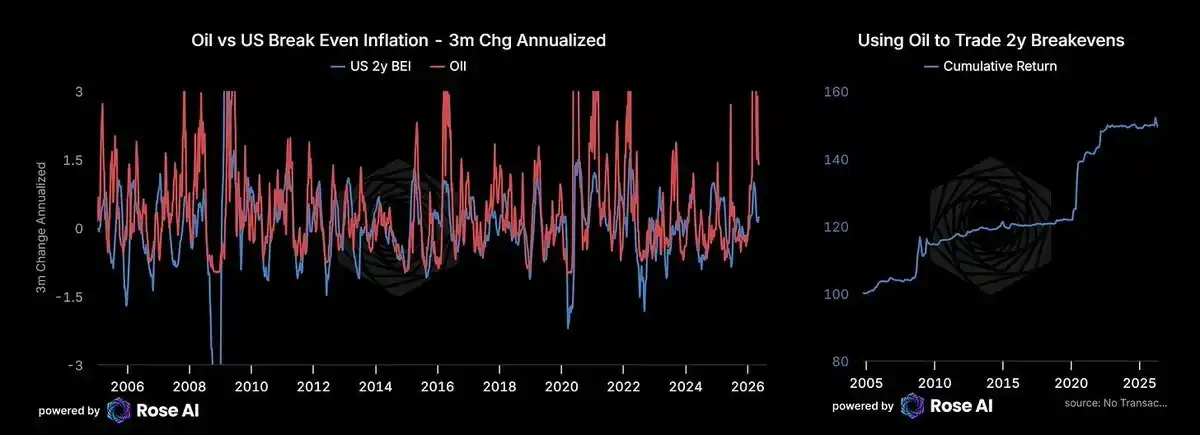

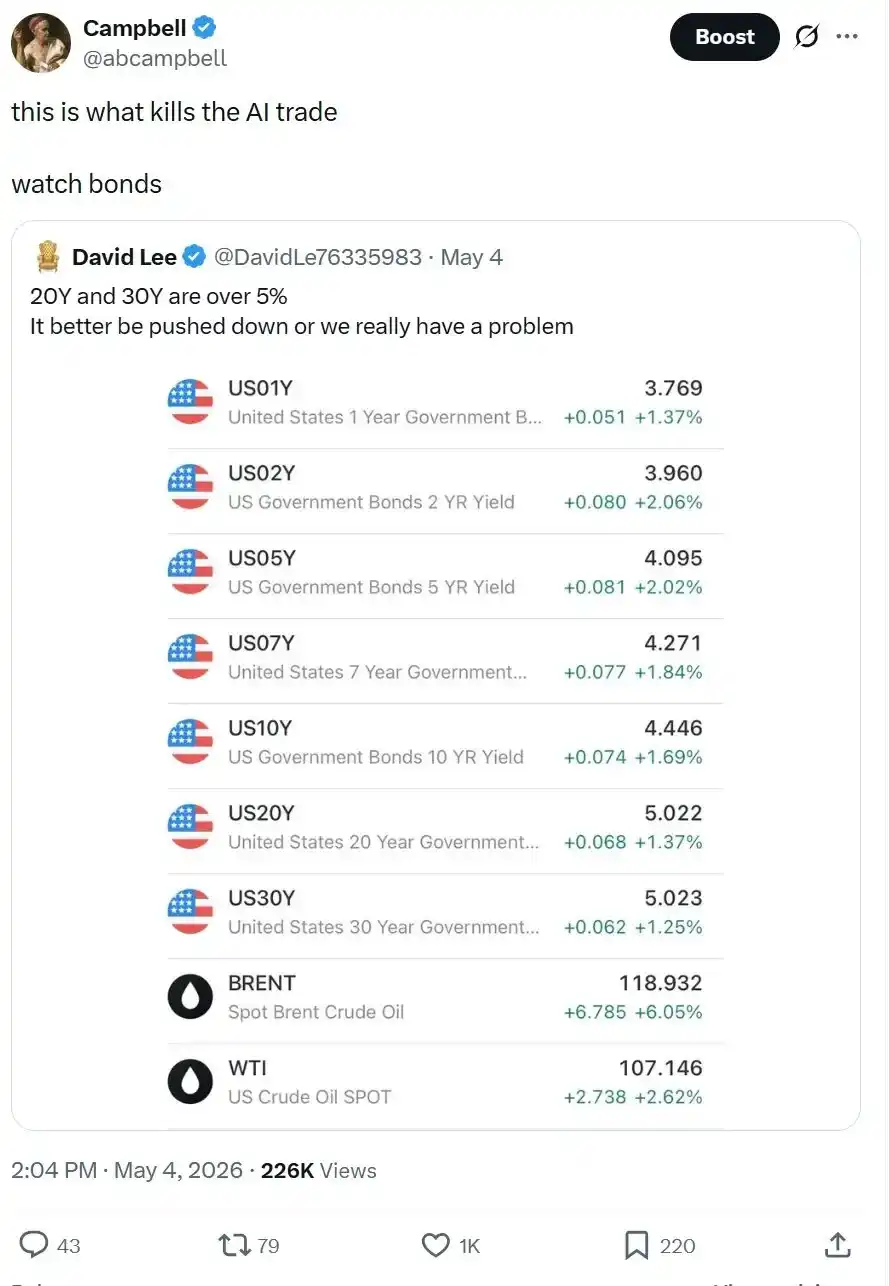

We started doing exactly that today, right before the CPI data confirmed what we already knew. Inflation is re-accelerating.

Interest rates are likely to rise too. As it turns out, just as Bob Prince used to say, there is a bond hiding inside stocks.

This is the "wedge." You don't short the bubble; you go long the trend that will kill the bubble. If AI is the bubble, then interest rates are the wedge that pops it.

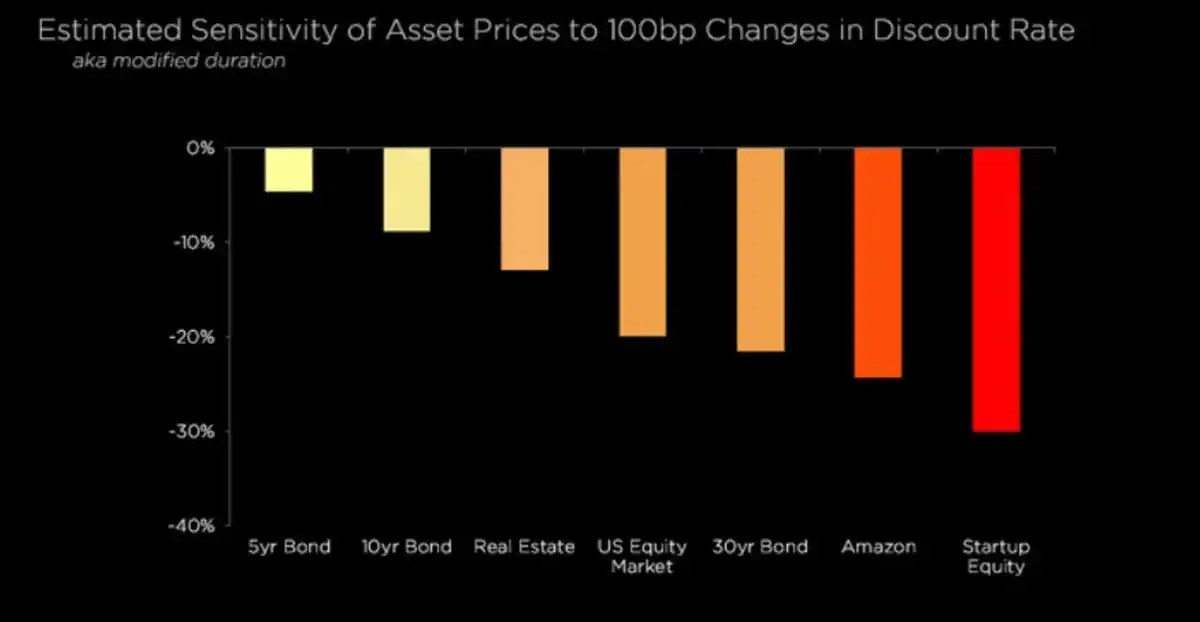

All assets with ridiculously high valuations are essentially disguised ultra-long-duration assets. When the discount rate (interest rate) rises, the present value of those wonderful future expectations gets heavily discounted, and stocks propped up by fantasies of 2030 cash flows get brought back to earth.

The core principle is: In every bubble, there are things that must depend on the bubble to survive. If the bubble just pauses for a moment, the weakest links will break. You are not betting that the market mania will end; you are betting that the weakest links cannot survive a market pause.

The beauty of the "wedge" strategy is you don't need precise timing. The bubble doesn't even need to pop; it just needs to stop accelerating for a quarter, and the highly levered junk starts to break.

Where is the "wedge" now? I'll tell you what I'm watching. Those Canadian banks with price-to-book ratios of 3x, holding "negative amortization" mortgages (where payments don't even cover interest, and the shortfall gets added to principal, like interest-capitalizing PIK loans), facing a housing market that makes 2007 US real estate look downright restrained.

I can't get the options I want on these banks, but I'm watching. Then broadly in credit, we wrote in "Watching Credit" that private credit feels like a "roach motel," reflecting loosening lending standards overall. Money goes in and doesn't come out. When the bubble pauses, the book value of these assets doesn't change because no one forces them to revalue. Until the day they have to face reality.

B) Shorting the Victims

The second method to short a bubble is to find things that will go down with the bubble, the assets adjacent to the bubble.

Evergrande is a great example. You didn't need to short Chinese bank stocks—that would have just cost you money for a decade. You needed the developer with insane leverage,极度依赖 pre-sales, that would explode if the Chinese property market just slowed a little. The bubble could keep inflating, but Evergrande couldn't last.

You look for "negative convexity" (things that fall faster and harder as they decline). You can't short the thing going parabolic itself; that's fighting double the upward momentum.

But look at its neighbor; maybe its options aren't trading at 70 vol.

Think back to airlines pre-pandemic. They weren't in a bubble themselves, but faced极度 asymmetric risk, so they fell viciously. Puts were priced richly but not ridiculously. You could still buy wings. So we did. It seems obvious in hindsight, but the "bubble" then was the blind optimism that "everything is fine."

Think back to financials in 07/08. You didn't need to directly short housing (frankly, directly shorting housing was extremely difficult and technical, though if you could find CDS, good for you). You just needed to short Bank of America.

The core principle is: Bubbles create correlations that only manifest during a crash. The options market usually only prices in this correlation when disaster strikes. Your job is to find the "victims" with cheap options, destined to be dragged down by the bubble asset with expensive options.

Who are the "victims" right now? Honestly, I haven't pinpointed them yet.

C) Waiting for Confirmation

The third method requires the most discipline, which is why most people mess it up.

That is: Wait.

I know, waiting is agony. Sometimes you see something shooting straight up, and you just can't help yourself. But again, you absolutely do not want to get run over by a train at full speed.

So you wait for the confirmation signal. What does it look like?

It's usually a combination of:

-

Fundamentals starting to deteriorate;

-

Buying drying up, market sentiment exhausted;

-

Trendline decisively broken.

Not a small pullback, but a decisive break. The kind where something that was going up nicely suddenly slices through a beautiful support line, and everyone starts screenshotting and sharing it on Twitter. We saw this break in silver earlier this January (don't look now, it's back up; we'll talk about that in a future article).

Depending on the timeframe you look at, the chart tells a completely different story.

The single most central truth right now about AI is that the only thing deteriorating is: Too much of its cash flow is promised far into the future.

The problem is you have to discount those future promises with today's rate. If inflation picks up and policymakers are forced to tighten (imagine if oil goes to $150-$200/barrel, they will), the net present value (NPV) of a lot of these assets shrinks massively. It's the same thing we wrote about with the bond bubble in 2021.

The other thing to watch is correlation. When what used to work perfectly suddenly stops working, when it suddenly becomes sensitive to factors it used to easily ignore, be careful. We may be seeing that today.

Practical Application and Summary

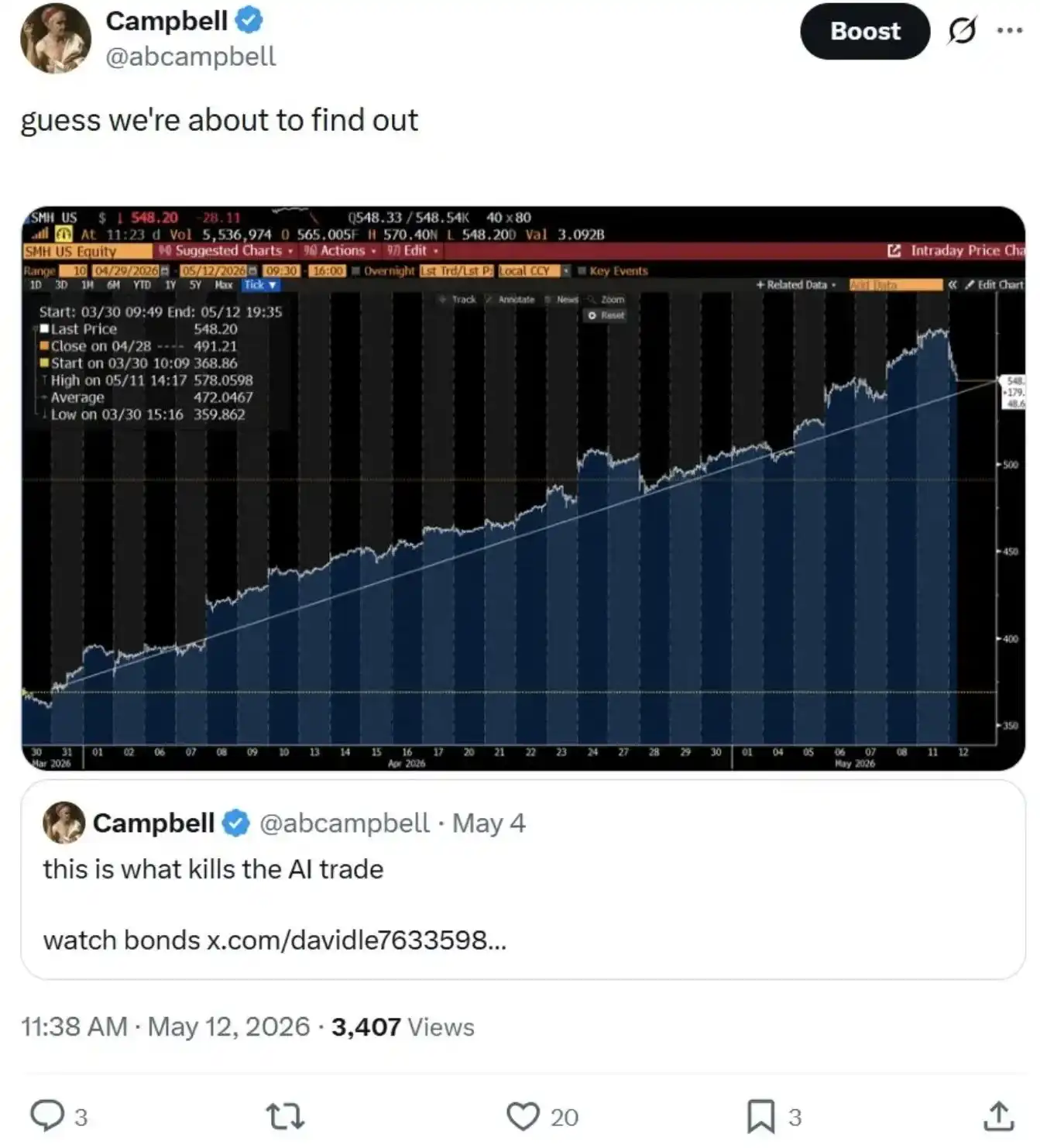

What did I do today? (Beijing time early May 13th) I had some hedges on before the market plunge, but not enough. I shorted another 5% of the S&P 500 (SPX) and 10% of high-yield bonds (HYG), then bought a little more short-dated put spreads. Then I stepped away, came back, and it was bad.

What did I actually do? I didn't short semiconductors because the core fundamental demand is still there, and the uptrend isn't broken. But I did short more bonds, this time directly buying put spreads on US Treasuries. If the trendline holds and the market bounces, I'll consider it cheap insurance for my "wedge" strategy, no big deal. If the trendline doesn't hold, I have cash, I have protection, and then, only then, will I go big on specific shorts. Oh, and I sold 5% of my Canadian bank stocks.

Hedge, find the wedge, wait for confirmation, go big.

Look, I don't know if we are in a bubble right now. This rally could be in the 4th inning (probably not, the price action is already too intense), or it could be in the 9th (I doubt it; that requires seeing demand for these underlying算力 tokens get destroyed, and I don't see signs of that yet). All I know is that the feeling of "inevitability" that AI gives me feels eerily similar to when I was in high school in 1999, putting together my first internet stock portfolio. Yes, those stocks eventually came back, and Amazon emerged from them. If you held until today, the IRR would be in the teens.

But I also haven't forgotten the brutal crash.

So, if you've read to the end of this rambling essay, you might feel nervous. If you feel nervous, the answer is definitely not to short the thing going vertical. The answer is: Find the wedge, buy puts on the victims, and then wait like hell for the confirmation signal before going big.

In the meantime, never fight the market trend. Never short the thing going parabolic.