Author: Michel Athayde

Can the Dual Currency Win Strategy Really Weather Bull and Bear Markets?

Using real market data from 2020-2026 for backtesting, we discovered:

Even with the same Dual Currency Win strategy, just by changing how the Calls are sold, the final profit difference can be nearly double.

The data tells us the problem isn't the strategy, it's human nature.

In the crypto market, the "Dual Currency Win" (Wheel Strategy) is often seen as a tool for collecting rent through bull and bear markets. But how do different underlying execution logics reshape long-term profit distribution?

To find the truth, we backtested Bitcoin and Ethereum over a complete bull-bear cycle from 2020-2026. In this sample, which includes crashes and an epic bull market, we compared two截然不同的双币赢玩法:

-

Standard Dual Currency Win (Rolling Strike): Follows the market. After taking delivery of the spot asset, each time a Covered Call is sold dynamically at 105% of the current price.

-

Break-even Type Dual Currency Win (Fixed Anchor): Anchors to cost. Once taking delivery at a high price, no matter how far the price falls, it stubbornly sells Calls at the "last delivery strike price," refusing to give up the chips until breaking even.

This is no longer a simple contest of "selling strategy vs. holding spot," but a deep test of "how trading psychology changes long-term profit distribution."

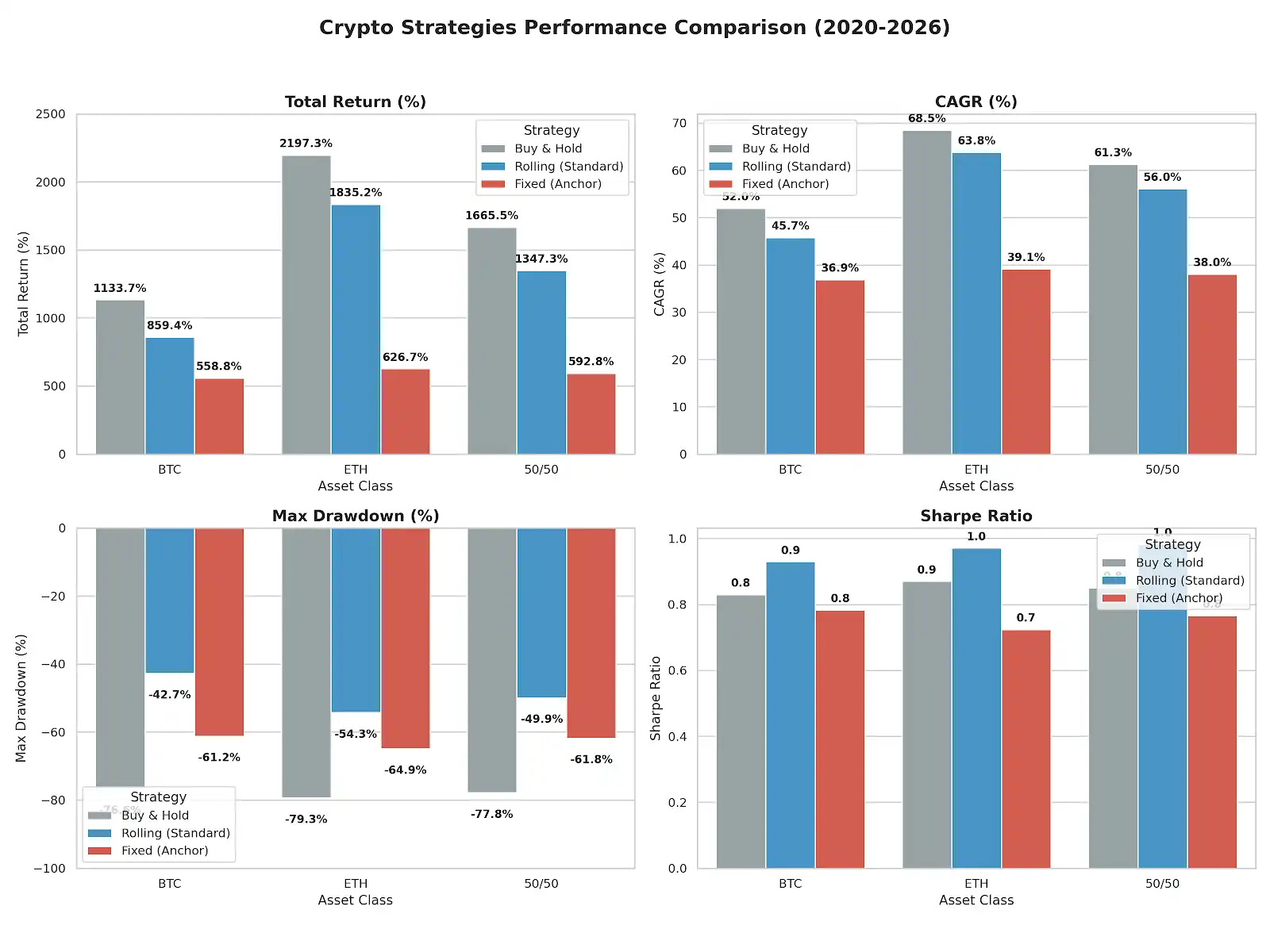

Core Data: Re-evaluating Risk and Return

(Note: Backtest span 2020-2026, Puts priced at 30% annualized, Calls at 25% annualized, 7-day cycles)

| Investment Strategy | Total Return | Annualized (CAGR) | Max Drawdown | Sharpe Ratio |

| BTC HODL (Buy & Hold) | +1133.73% | 51.95% | 0.83 | |

| BTC Standard (Rolling) | +859.43% | 45.72% | -42.74% | 0.929 |

| BTC Break-even (Fixed) | +558.81% | 36.88% | -61.19% | 0.783 |

| --- | --- | --- | --- | --- |

| ETH HODL (Buy & Hold) | +2197.31% | 68.52% | -79.30% | 0.87 |

| ETH Standard (Rolling) | +1835.21% | 63.78% | -54.27% | 0.971 |

| ETH Break-even (Fixed) | +626.74% | 39.13% | -64.87% | 0.724 |

| --- | --- | --- | --- | --- |

| 50/50 HODL Portfolio | +1665.52% | 61.30% | <极速赛车开奖网em data-index-in-node="0" data-path-to-node="11,9,3,0">-77.80% | 0.85 |

| 50/50 Standard Portfolio | +1347.32% | 56.05% | -49.90% | 0.983 |

| 50/50 Break-even Portfolio | +592.77% | 38.03% | -61.80% | 0.766 |

Faced with this real data, we need to re-examine two core propositions in trading.

The Risk-Return Balancing Act of the Standard Dual Currency Win

Many mistakenly believed the standard strategy would severely underperform in bull markets, but the data proves that with just a 5% upside buffer (spot price * 1.05), it exhibits极强的 risk-return balancing ability over a full cycle.

In the 50/50 portfolio, its Sharpe Ratio (0.983) thoroughly crushed buy-and-hold (0.85) and drastically compressed the nearly -78% abysmal drawdown to -49.9%.

Its advantage doesn't come from predicting the market, but from the mechanism of "continuously dynamically raising the strike price."

With every price change, the standard version relentlessly adjusts its target. Rolling本质上是在牛市中不断“重置成本”,而 Fixed Anchor 却是在不断“确认错误”. The standard version sacrifices a极小部分 of potential暴利上限,换取来了平滑资金曲线的巨大战略纵深.

"Anchoring to Cost" is the Most Expensive Psychological Placebo

The most thought-provoking part of the data is the comprehensive failure of the "Break-even (Fixed Anchor)" type. It fell far short of the standard version in both return and drawdown control.

This exposes the most common weakness in human trading psychology: Anchoring Effect. If you took delivery at a high of 60k, and stubbornly hang a Call at 60k when the price drops to 30k, you not only lose the "bleeding stop" ability of option premiums during the long bear market, but also risk having your chips called away at 60k during a V-shaped market reversal, completely missing the subsequent main upward浪.

The break-even strategy seems conservative, but it's actually using time to fight the trend. And in a trend-driven market, time is often on the side of the trend. Obsessing over "not selling at a loss" is ironically the fastest way to perfectly miss out on major cycle红利.

Conclusion

Markets are full of volatility, but data doesn't lie.

In trending assets like Bitcoin and Ethereum, the real risk is not drawdown, but being limited on the upside by your own psychological anchor.

The standard Dual Currency Win tells us:

As long as you keep adjusting dynamically and rolling continuously, a selling strategy can also coexist with the trend.

And the break-even strategy reminds us:

The market won't change direction because of your cost basis.

Discipline is far more important than breaking even.