Author: danny

“What should I do? I haven't made money from AI, it's too late if I don't get on board now.” This is probably the voice in your head when you opened this article.

NVIDIA has risen over tenfold in three years. The leading optical module company rose 17 times in one year. Every news article talks about AI. Colleagues are showing off their portfolios. Various social media platforms, Xiaohongshu, X, TIKTOK are all sharing “the next ten-bagger stock”.

You are uninvested. You are anxious. You open your account, finger hovering over the “Buy” button.

I want to ask you a question first—Why do you want to buy?

If your answer is “AI is a megatrend,” “some KOL is pumping it”—that's someone else's judgment, not yours;

If your answer is “my friend made money, I want to make money too”—that's envy, not investing;

dir="ltr">If your answer is “it'll be too late if I don't buy now”—that's FOMO, not analysis.Your real problem isn't 'being late'. Your problem is not having your own worldview.

Sounds abstract. Let me explain in a concrete way—why this problem is 100 times more important than “which stock to buy”.

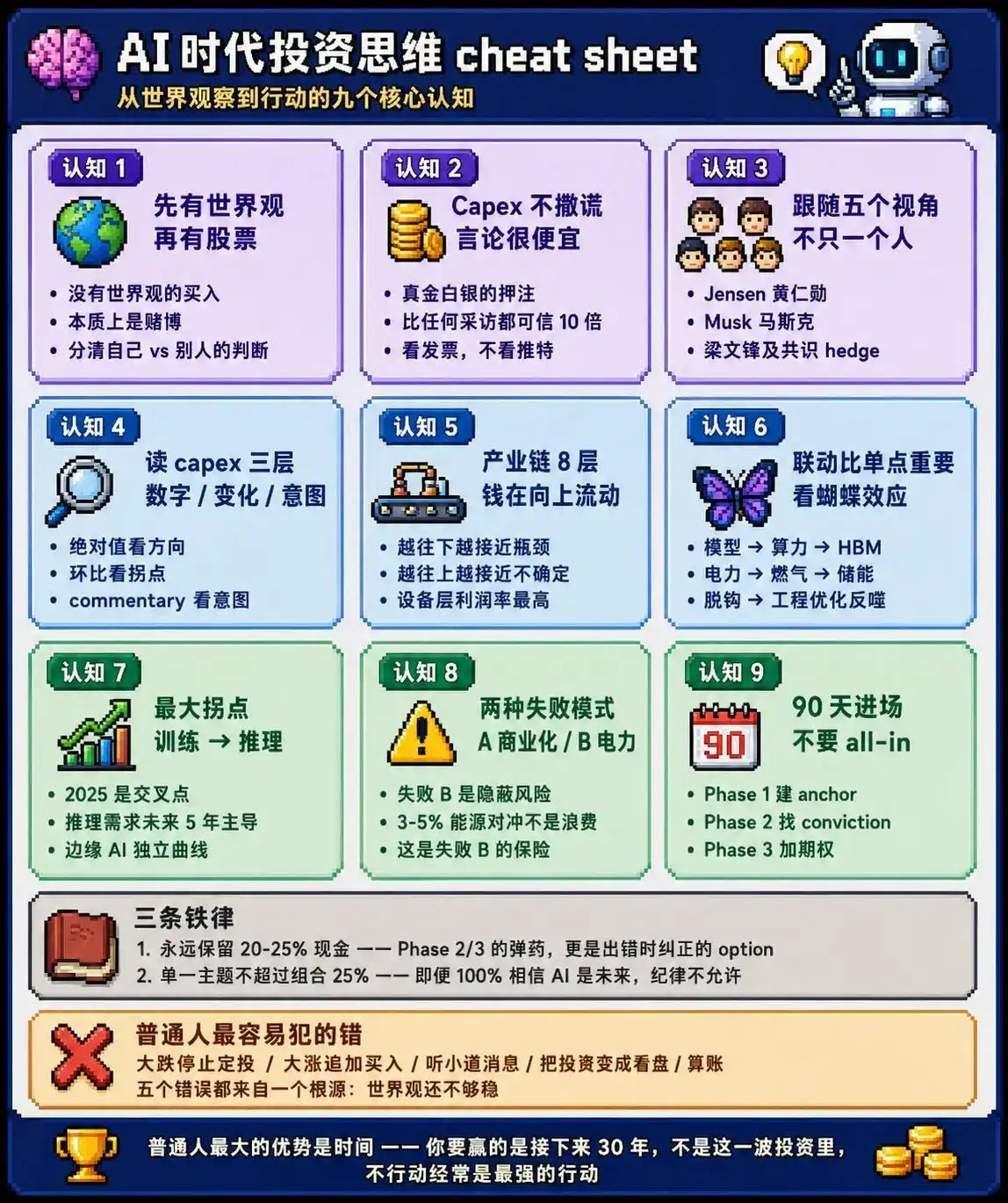

I. Where 99% of People Fail

Open any financial platform, all discussions revolve around one question: What to buy.

“Can NVIDIA still rise?” “Should I chase optical modules?” “What about the robotics sector?”

These questions themselves are wrong.

They assume one thing—you already know AI / Robotics / Optical Communications is the right direction. And this is precisely the part that should be independently thought through, but is skipped by 99% of people.

What's the price of skipping it?

When your judgment is right, you don't know why it was right—so you don't know when to exit.

You bought NVIDIA at $80 based on some KOL's recommendation. At $140, you couldn't bear to sell because you were “bullish long-term.” At $200, you wanted to add because “the momentum is strong.” At $150, you were confused, “the story is still there.” At $100, you panicked and sold, “was I wrong?”.

When your judgment is wrong, you don't know why it was wrong—so you'll keep losing until it's deep.

You bought some AI concept stock at $50. At $30, you didn't sell, “AI is a ten-year theme.” At $20, you added, “it's cheap now.” At $10, you gave up. That stock never returned to your cost basis.

The commonality of these two scenarios: You never had your own judgment framework. You just listened to different people and did different things at different times.

This is the cost of a rented worldview.

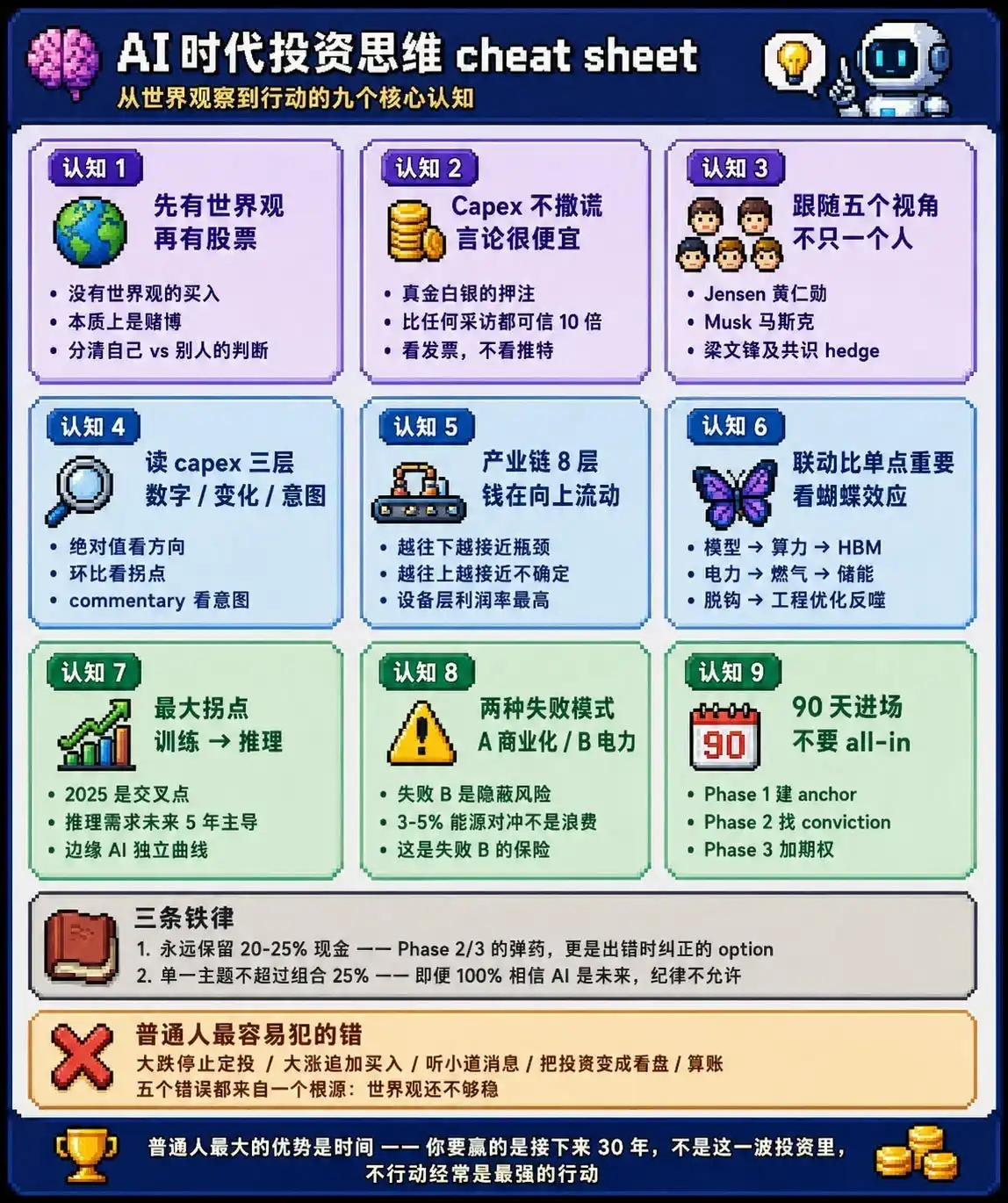

II. What is “Your Own Worldview”

Worldview is not reading news. Worldview is answering a few fundamental questions: (For example)

In the next 5-10 years, what will be the biggest changes in human society? Will the energy structure be reorganized? Will computing costs drop by another order of magnitude? Will the labor market be restructured?

Where are the physical constraints for these changes? Is there enough power? Enough minerals? Enough talent?

How will money flow? Who profits from it? Who is disrupted? Who is the real bottleneck?

When you can answer these questions, stock selection becomes simple—because you already know where money will flow, you just need to find the sluice gates on that river.

More importantly—When the market fluctuates, you won't panic, won't ask everyone for advice. Because your judgment doesn't depend on “will it rise or fall tomorrow,” but on “what the world will look like in 5 years.”

Buffett, Munger, Dalio can weather bull and bear markets, not because they are smarter, but because their worldview is built by themselves, not fed by the market.

III. Two Paths: Build vs. Follow

Path A: Build Your Own Worldview

Difficult. It requires extensive cross-disciplinary reading, tracking primary information sources, long-term independent thinking, accepting that 30% of your judgments will be wrong.

Most ordinary people don't have the time, energy, or knowledge base for this. That's okay—there's Path B.

Path B: Follow Those Who See the Farthest

The logic is simple: those who truly change the world see the trend 5-10 years earlier than everyone else. Their words and actions reveal their worldview. Following their money equals inheriting their judgment.

But 99% of people get this step wrong—you're not following their words, but their money.

Let me repeat, because it's important:

Talk is cheap. But Capex is expensive.

Elon Musk has said “FSD L5 next year” for eight years—that's talk. SpaceX spending $5.6B on gas turbines—that's capex.

Capex doesn't lie. When someone is willing to bet $5 billion on a certain direction, their real conviction in that direction is 10 times stronger than any interview, speech, or tweet.

This is the most critical yardstick for judging the worldview of leading figures.

Subscribe

IV. Five People Worth Tracking in the AI Commercialization Space

Not all CEOs' words are worth listening to. This article lists five individuals whose opinions represent different slices of the AI era's worldview. Together, they form a complete signal network.

Jensen Huang (NVIDIA) — The Shovel Seller's Perspective

All AI companies have to buy chips from him. He holds the most complete demand signals in the industry chain: the real curve of computing power demand, bottlenecks in which links, how capacity is allocated for the next 3 years.

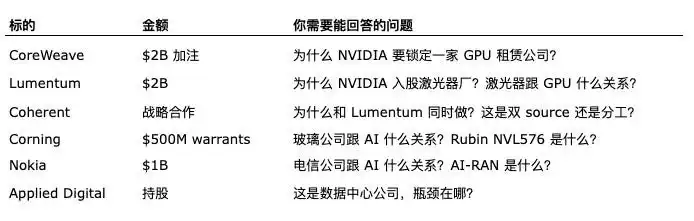

Listen to the GTC keynote (every March and October), watch the quarterly earnings calls. But most importantly, look at NVIDIA's balance sheet investments—CoreWeave, Lumentum, Coherent, Corning, Nokia—these are the real bottlenecks he identifies. He uses his own company's cash to tell you where the money is.

Elon Musk (Tesla / SpaceX / xAI) — The Capex Perspective

The most aggressive executor. Has real decision-making power across five fields simultaneously: autonomous driving, rockets, AI, energy storage, robotics.

A technique for listening to Musk: 70% of his words are talk, 100% of his actions are signals. “FSD L5 next year” for eight years is talk, but $5.6B buying gas turbines, $697M buying Megapacks, merging SpaceX and xAI—these capex decisions are his real worldview.

The right way: Ignore his Twitter noise, closely watch his invoices.

Sam Altman (OpenAI) — The Commercialization Perspective, with Bias

Represents the front line of AI application layer + commercialization. He interfaces with the largest enterprise clients daily, knows which use cases can truly generate revenue, where the real bottlenecks in model iteration are.

But one must be vigilant when listening to Altman—he is fundraising. His description of everything has elements of talking his book. How far is AGI, Stargate investment of five trillion—these are narrative crafting for the next round of funding pricing.

The right way: listen to the direction he points to, but discount his timelines by at least 50%.

Dario Amodei (Anthropic) — The Technologist's Perspective

The most serious “technologist + safety” faction in the AI industry. Anthropic can compete head-on with OpenAI on frontier models, but its voice is far smaller than its valuation—meaning Dario's speech has signal, no noise.

His long essays (“Machines of Loving Grace”, “On DeepSeek”) are among the few serious reflections in the AI era. He doesn't sell stories; he explains what he believes. Listening to Dario gets you closer to the truth than listening to Sam—because he has no need to hype.

How to track: Anthropic official blog, his long essays, occasional podcasts. He doesn't use Twitter—this in itself is a signal.

Wenfeng Liang (DeepSeek) — The Anti-Consensus Perspective

Represents the real technical depth of Chinese AI. DeepSeek-V3, R1 proved one thing: under constrained computing power, engineering optimization can approach the performance of closed-source models. This fact changes the entire cost curve of the AI industry chain. (Especially cost!!!)

Wenfeng Liang basically doesn't give interviews, doesn't use Twitter, doesn't do marketing. His worldview is hidden in DeepSeek's papers and model release notes—you have to read them, can't wait for the media to feed you.

Why still track him: He represents an anti-consensus but extremely important perspective—”AI doesn't necessarily require infinite computing power stacking.” If his direction proves true, the entire “AI = infinite capex” story needs to be re-evaluated.

His existence itself is a hedge for your portfolio—a reverse indicator reminding you “maybe NVIDIA's growth curve isn't that steep.”

Remember that time in early 2025 when DeepSeek-R1 was released? NVIDIA fell 17% in a single day, market cap evaporated six hundred billion dollars. If you only listened to Jensen and not to Wenfeng Liang, you had no idea why that drop happened. If you listened to both, you would understand: this was the market re-evaluating the training cost curve, a correction not a rupture—so you wouldn't panic sell.

The diversity of worldview determines whether you can stay calm when the unexpected happens.

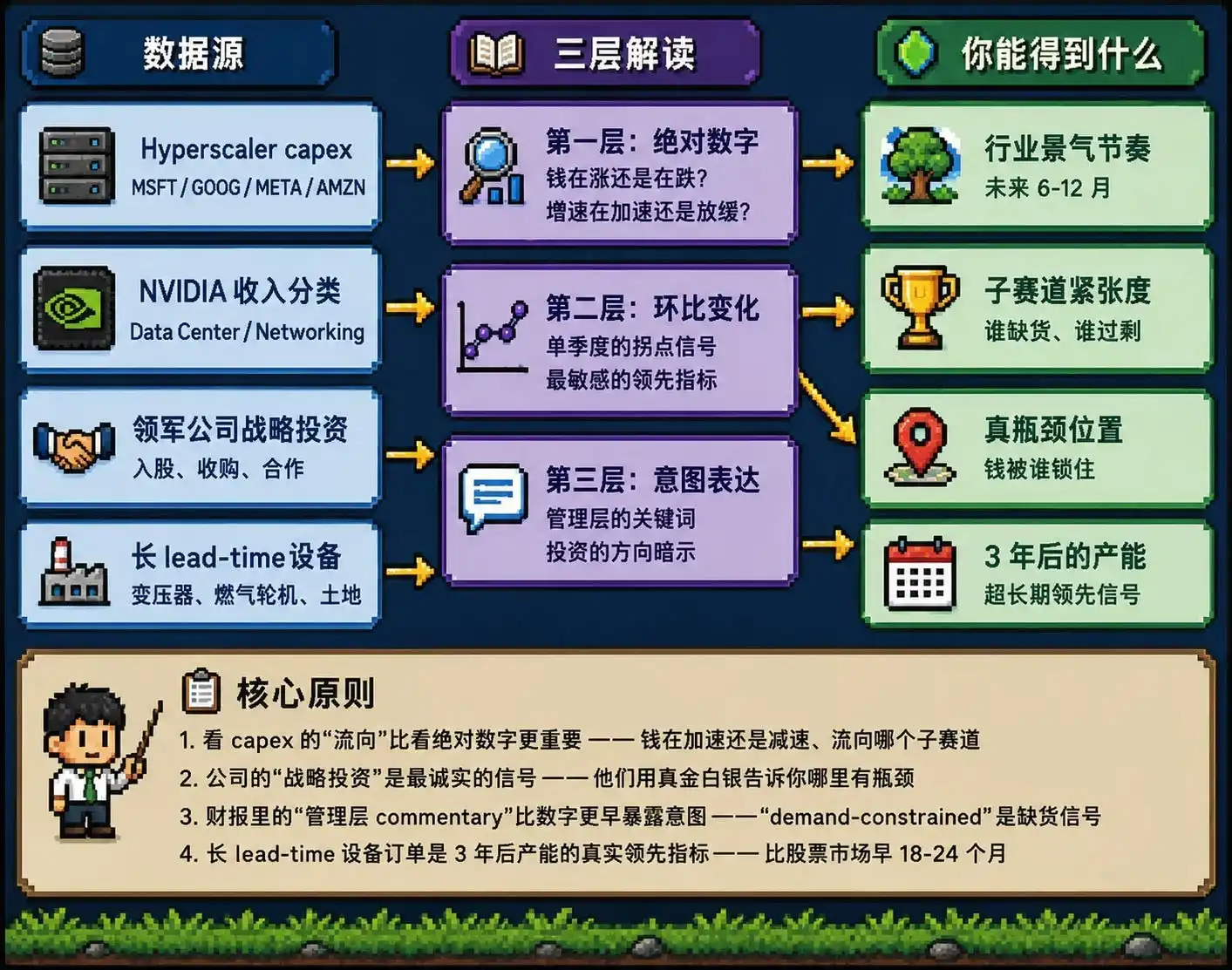

V. How to Specifically Read Capex

You might ask at this point: I understand the theory, but where exactly do I look for this capex thing? How do I read it?

This section is the real practical knowledge. I'll break down the method into actionable steps.

Category 1: Hyperscaler Quarterly Capex (The Most Important Signal Source)

Look at: The “Capital Expenditures” number in each quarterly earnings report + forward guidance given by management in the conference call.

Where to look:

-

Microsoft earnings disclosure → investor.microsoft.com

-

Google → abc.xyz/investor

-

Meta → investor.fb.com

-

Amazon → ir.aboutamazon.com

-

Oracle → investor.oracle.com

How to read the three layers of signals:

First layer: Bird's-eye view numbers Full-year 2024 hyperscaler total capex ~$250B, 2025 ~$320B, 2026 consensus expectation $400B+. Growing 25-30% annually.

This number itself tells you two things:

-

The tide of AI capital expenditure is still rising

-

The growth rate is slowing (from +60% in 2023 to +25% in 2026)

Note: Slowing does not equal ending. A market growing from $250B to $400B is still a huge pull for the supply chain—but you can't price it with the “exponential curve” expectations of 2023-2024 anymore.

Second layer: Sequential changes Is the single-quarter capex higher or lower than the previous quarter? This is the most sensitive indicator.

Example: Meta 2025 Q1 capex $20B → Q2 $23B → Q3 $27B — that's acceleration. If you see sequential change turn negative—alarm. That means the company is starting to throttle spending.

Third layer: Management commentary In the earnings conference call, management will be questioned by analysts “how is capex spent? Which direction?”—Their answers are real expressions of intent, because they have disclosure obligations to shareholders (though they will package it).

Key phrases to listen for:

-

“compute infrastructure” / “AI training” / “data center build” → AI capital expenditure

-

“land and shells” / “long-lived assets” → Data center civil construction (not GPU procurement, but land + building + power access)

-

“networking” → Optical modules, switches

-

“we are demand-constrained, not capacity-constrained” → Still supply-constrained

-

“we see signs of normalization” → Alarm, demand starting to soften

Category 2: NVIDIA Quarterly Revenue Breakdown (The Fastest Leading Indicator for the Industry Chain)

Look at: NVIDIA earnings report Data Center business revenue + Networking segment.

Why this is a gold signal: NVIDIA sells chips to all hyperscalers. Its datacenter revenue = the real landing of the “compute” portion of hyperscaler AI capex. If NVIDIA Q1 FY27 datacenter revenue is +92% YoY, that means hyperscalers' AI spending actually materialized—not guidance, but revenue.

Networking segment is a more hidden goldmine: NVIDIA Q1 FY27 networking +199% YoY, reaching $15B single quarter—annualized $60B+. This number is larger than all sell-side analyst predictions for the “AI networking market TAM”.

What does this mean?

-

The demand for the entire optical module / switch / interconnect industry chain is underestimated

-

Upstream supply chain (optical components, connectors, PCB) should be tighter than market expectations

-

You can infer the sub-sector prosperity 12 months later from this number

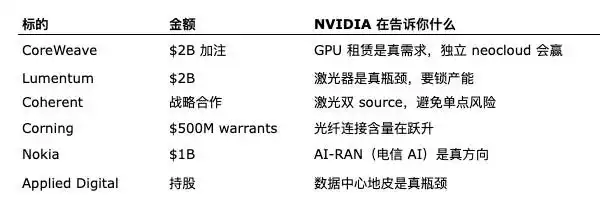

Category 3: Leading Companies' “Balance Sheet Investments” (Strongest Signal)

This is a signal completely ignored by most retail investors.

A CEO's words may have bias, earnings numbers are lagging indicators. But when a company uses its own cash to invest in another company—this is the strongest expression of belief in the future.

NVIDIA's investment targets in the past 12 months:

Is it a bit complex? Or rather, have no clue? If you connect their industry chain relationships, does it become slightly clearer?

The same method applies to:

-

Which AI startups did Microsoft acquire? Who did they invest in besides OpenAI?

-

Google's acquisition list (what does Character.AI's back license indicate?)

-

Changes in Tesla's supplier payments in which areas?

How to find this data:

-

Company 10-K / 20-F annual reports have the “Investments and Advances” appendix

-

SEC 13D/G filings (mandatory disclosure for holdings exceeding 5%)

-

PitchBook, Crunchbase (paid)

-

Companies' news release sections (public strategic partnerships will be announced)

Category 4: Leading Indicators—Power, Land, Long Lead Time Equipment

This is the most hidden but earliest signal.

Why important: Chips can be bought, but delivery cycles for power, land, transformers, gas turbines are 3-7 years. So orders for these long-lead-time resources reflect capacity 3 years later.

Look at:

-

“interconnection queue” data from US grid companies like ERCOT / PJM / MISO (publicly available data on data center applications for grid connection)

-

Backlog data from GE Vernova, Siemens Energy, Mitsubishi Heavy Industries

-

Transformer orders from ABB, Hitachi Energy, Eaton

-

Specific data center site selections and power configurations publicly disclosed by xAI / Stargate / Meta

These signals often appear 12-24 months before chip sales boom. If you see ERCOT queue grow 200% for 2026, that means a large number of data centers will come online around 2028, corresponding chip demand in 2027-2028.

VI. The Full Map of the AI Industry Chain (Structural Understanding)

Just knowing “where the money is” isn't enough. You need to know how this money flows along the industry chain.

Let me map out the AI industry chain from the bottom to the top. This isn't to make you remember every layer, but to understand “where value is created and allocated.”

Tier 0: Raw Materials & Substrates

Power: Nuclear, Natural Gas, Geothermal, Energy Storage Materials: Silicon, Copper, Rare Earth, Gallium, Indium, Indium Phosphide (InP), Thin-Film Lithium Niobate (TFLN) Typical Players: Cameco (Uranium), Williams Companies (Natural Gas Pipelines), AXTI (InP Substrate), Soitec (SOI Substrate), NGK (TFLN)

Economic Characteristics:

-

Capital intensive, slow capacity adjustment (2-5 years)

-

Strong commodity attributes, pricing power from geography or tech patents

-

The “transmission end” of the AI cycle—prosperity lags upstream by 12-24 months

Tier 1: Wafer Foundry & Substrate Processing

Logic Chip Foundry: TSMC, Samsung Foundry, Intel Compound Semiconductor: Win Semi (GaAs/InP), Tower Semiconductor (Silicon Photonics) Memory Manufacturing: SK Hynix, Samsung Memory, Micron Substrate Processing: Shin-Etsu, SUMCO

Economic Characteristics:

-

Oligopoly (TSMC is basically exclusive below 3nm)

-

Extremely high capital expenditure (one fab $100-300B)

-

The “throat” of the entire AI revolution—everyone has to place orders here

Tier 2: Chip Design

GPU: NVIDIA, AMD ASIC: Broadcom (designs for Google TPU / Meta MTIA), Marvell (for Amazon) Networking Chips: Broadcom (Tomahawk), NVIDIA (Spectrum-X) HBM Controller: Marvell, Astera Labs, Credo CPU: Intel, AMD, ARM architecture (Apple / Apple Silicon)

Economic Characteristics:

-

Extremely high profit margins (NVIDIA gross margin 75%)

-

But diverging—hyperscaler self-developed ASICs are taking NVIDIA's share

-

Design capability is the real moat, relatively less capital intensive

Tier 3: Advanced Packaging & Testing

CoWoS Packaging: TSMC (exclusive capacity) Testing Equipment: KLA, Applied Materials, Onto Innovation Hybrid Bonding (Key Tech for HBM4): BESI, ASMPT Silicon Photonics Testing: MSSCORP

Economic Characteristics:

-

Equipment companies are “unlockers of capacity constraints”

-

Extremely high profit margins (BESI gross margin 60%+)

-

A severely underestimated segment—most retail investors don't know this layer exists

Tier 4: Optical Interconnect & Networking

Lasers: Lumentum, Coherent, Sivers Modulators: HyperLight (TFLN), traditional players Optical Modules: Zhongji Innolight, Eoptolink, Coherent Fiber Connections: Corning, Foci Network Switches: Arista, Cisco, Juniper, NVIDIA Spectrum-X

Economic Characteristics:

-

When GPU clusters exceed 100k units, interconnect cost accounts for 15-25% of total system cost

-

One of the fastest-growing sub-segments in the AI industry chain

Tier 5: Servers & System Integration

ODM / EMS: Foxconn, Quanta, Wistron, Inventec, Supermicro Liquid Cooling: Vertiv, Boyd, Asetek, Auras Power Supply: Delta Electronics, Lite-On

Economic Characteristics:

-

Low gross margin (5-10%) but large volume

-

Liquid cooling is a new growth sub-segment (significantly higher margin than traditional air cooling)

Tier 6: Data Center Infrastructure

Data Center Operations: Equinix, Digital Realty Neocloud: CoreWeave, Nebius, Lambda Power + Cooling + Network Support: Too many players

Economic Characteristics:

-

This is the biggest destination of hyperscalers' own capex

-

Neocloud is a new species that emerged in 2024-2026—independent rental of GPU computing power to AI companies

Tier 7: Models & Applications

Frontier Models: OpenAI, Anthropic, Google DeepMind, xAI, Meta, DeepSeek Application Layer: Microsoft Copilot, Cursor, Perplexity, various vertical AI SaaS

Economic Characteristics:

-

The most watched layer by the market, but winners are undecided

-

Business models still being explored (subscription, API, agent fee)

-

The layer with the highest risk and most uncertain return

VII. Interlinkages Within the Industry Chain

Just knowing the industry chain layers isn't enough. You need to understand how changes in one layer transmit to other layers—this is the cognition most easily overlooked by ordinary investors.

Let me give a few concrete transmission chain examples:

Linkage 1: Model Layer → Compute Layer → Storage Layer

Trigger Event: OpenAI releases GPT-5 (assuming 10 trillion parameters needed)

Transmission Chain:

-

Training Compute Demand: From GPT-4's ~25,000 H100 cards → GPT-5 estimated to need 100,000+ B200/Rubin cards

-

NVIDIA Benefits: Datacenter revenue accelerates

-

HBM Demand Soars: Each B200 paired with 192GB HBM3E, 100k cards = ~20PB HBM

-

SK Hynix / Samsung / Micron Benefit: HBM prices rise

-

HBM4 Accelerated: Customers pressure Samsung / SK Hynix to accelerate HBM4 mass production

-

BESI Benefits: HBM4 requires hybrid bonding, BESI equipment orders soar

-

InP / TFLN Benefits: Because a 100k GPU cluster must use optical interconnect, corresponding upstream material demand

This is why when an OpenAI launch ignites stock prices, it's not just NVIDIA—but also upstream segments like BESI, Lumentum, AXTI.

Linkage 2: Power Bottleneck → Data Center Site Changes → Regional Beneficiaries

Trigger Event: US transformer delivery lead times extend from 50 weeks to 130 weeks

Transmission Chain:

-

Data Center Construction Delays: Projects originally planned for 2026 launch postponed to 2028

-

Bypassing the Grid: Hyperscalers start using mobile gas turbines (Solar Turbines / Capstone)

-

Natural Gas Demand Grows: Williams Companies, Kinder Morgan benefit

-

Energy Storage Steps In: Tesla Megapack, Sungrow, Fluence sell to data centers

-

Nuclear Option Revalued: Cameco (Uranium), Constellation Energy (Nuclear operations) surge

-

Site Selection Concentrates Near Natural Gas Sources: Texas, Appalachia, North Dakota become new data center corridors

This is why power shortages let you find “energy stocks + storage stocks” opportunities within the AI theme.

Linkage 3: China-US Decoupling → Supply Chain Dual-Tracking → Regional Player Divergence

Trigger Event: US restricts Nvidia H20 exports to China

Transmission Chain:

-

Chinese Cloud Providers Forced to Self-Develop: Alibaba, ByteDance, Tencent, Baidu accelerate domestic chip procurement

-

Huawei Ascend Benefits: Orders surge

-

Chinese Semiconductor Equipment Chain Benefits: AMEC, Naura, etc.

-

Chinese Model Companies like DeepSeek Benefit: Computing power constraints instead spur engineering optimization

-

DeepSeek-R1 Released → NVIDIA Falls 17%: Because market worries “compute demand curve not that steep”

-

In Turn Drives NVIDIA to Find New Growth in Middle East, India: HUMAIN, IndiaAI projects

This is why geopolitics is not an external variable for the AI theme—it's one of the biggest internal variables for the AI theme.

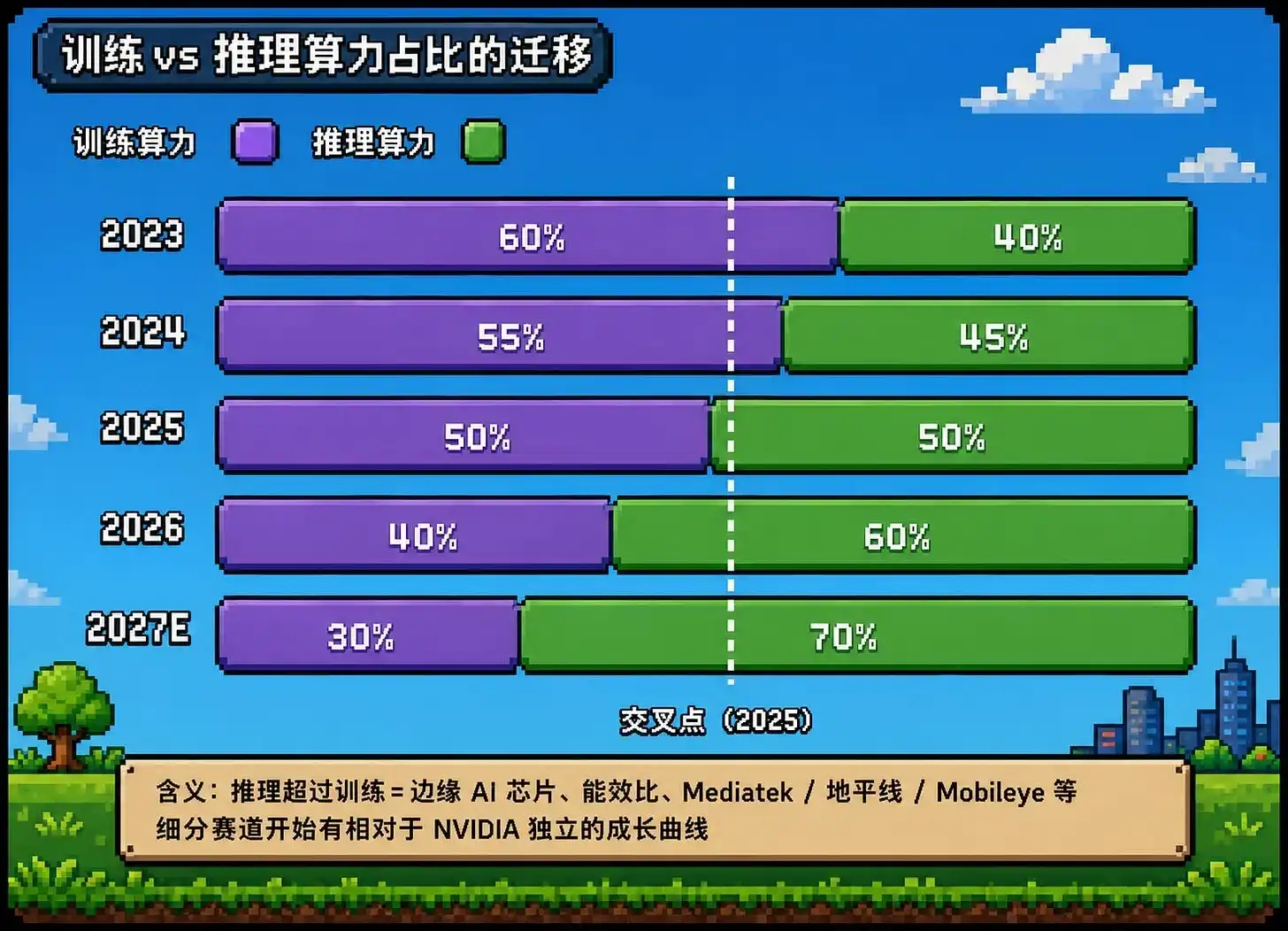

Linkage 4: The Generation Shift from Training → Inference

Trigger Event: reasoning models (o1, Claude reasoning, DeepSeek-R1) become mainstream

Transmission Chain:

-

Inference Token Consumption Explodes: Single query from 500 tokens → 50,000 tokens (100x)

-

Inference Compute Demand > Training Compute Demand: From 4:6 in 2024 → predicted 7:3 in 2027

-

Edge AI Chips: Diffusion from datacenter to terminals (phones, cars, robots)

-

MediaTek, Horizon Robotics, Mobileye Benefit

-

Energy Efficiency Becomes More Important: GaN, SiC power semiconductor demand grows

-

NVIDIA's “Inference-Optimized” product line (Blackwell Ultra, Rubin Inference) becomes more profitable than training products

This is the most important industry chain inflection for 2025-2027—most investors are still looking at AI through the “training compute” framework, but the real money is shifting to inference. (You can have your AI help you reason)

VIII. The “Worldview” Deduced from Listed Companies' Capex

When you start following capex flows, you'll find money flowing to a few clear directions:

AI Chips—The marginal cost of intelligence is declining, but total demand grows faster, so total chip volume continues to expand. But winners aren't just NVIDIA. Broadcom via ASICs takes hyperscaler self-development orders, TSMC is the fab for all players.

Memory—The larger the AI model, the more HBM demand. GPUs without HBM are crippled. HBM is structurally in short supply, SK Hynix, Samsung, Micron three oligopolies, expansion cycle 18-24 months.

Optical Interconnect—When GPU count exceeds 1 million units, the physical limit of copper interconnect is breached, must use optics. Corning is the relatively safest bet—large-cap + truly benefits.

Robotics—The cost structure of physical labor is being rewritten. But this market is far from mature, Tesla Optimus already postponed twice. It's still too early, wait until 2027 to see mass production data.

Energy—This is the most underestimated direction. AI is not a software revolution, it's an energy consumption revolution. A large data center consumes power equivalent to a medium-sized city. The US grid cannot bear expected AI demand, transformer queue 5 years, gas turbine queue 7 years. So what's happening is hyperscalers bypassing the grid, self-building gas turbines + storage + future small nuclear.

These five directions above, each deduced from capex flows, not from news. This is judgment built upon worldview.

After talking so much about capex, industry chains, hedging, you might think: How should I judge when I see daily news, Twitter, a CEO says something?

Here's an actionable judgment process for you.

IX. A Training You Can Act on Immediately

After all this theory, here's a practice you can do tonight.

Practice: List all NVIDIA's investment targets in the past 12 months, and explain why.

I'll list them for you:

Can't explain clearly → You don't have a worldview yet, this is the homework for your next month Can explain clearly → You have started looking at the world through capital flows

This list you can explain yourself is more important than any stock recommendation. It doesn't tell you “what to buy,” it's training you “how to see.”

X. From Worldview to Action

Good—you've built a worldview. Now the question: How to implement?

A counterintuitive answer: The clearer the worldview, the slower the action actually is. (Don't believe it? Look at Buffett.)

Why? Because you're no longer driven by FOMO. You know AI is a 10-year story—entering 3 months, 6 months, even 12 months late is not important on a 10-year scale. You don't need to win this wave, you need to win the next 30 years.

Step 1: First solve the basic financial structure

Before thinking “what to buy,” answer three questions first:

-

Do you have an emergency fund for 6 months of living expenses?

-

Have you repaid high-interest debt (credit cards, consumer loans)?

-

Have you bought insurance?

Investing in stocks without solving these three problems is waiting to be stopped out.

Step 2: Decide the allocation ratio for your investment strategy

Conservative 10%, Balanced 15%, Aggressive 25%.

Don't exceed 25%. Even if you 100% believe AI is the future—risk management doesn't allow a single theme to exceed a quarter of your portfolio. This isn't pessimism, it's discipline.

Step 3: Choose the participation method

For 80% of ordinary people, the correct answer is broad-based index ETFs (QQQ, SPY, VOO). (Data also proves this)

In Nasdaq 100, NVIDIA, Microsoft, Google, Meta, Amazon, Apple together account for over 40%—they are all core beneficiaries of the AI theme. Buying QQQ equals automatically overweighting AI, while diversifying single-stock risk.

For 15% of people—thematic ETFs (AIQ, SOXX). Volatility is 2-3 times that of broad-based, but more diversified than single stocks.

For 5% of people—individual stocks. The list is extremely short, like NVIDIA, Microsoft, Google, Meta, TSLA, Broadcom, TSMC, etc. (The above is not investment advice, do your own research)

Don't expand to “upstream small-cap high-payoff.” That's for professionals, not for you.

Step 4: Enter in batches

If you decide to invest 100k into AI—don't buy it all in one go today.

Divide over 6-12 months, fixed amount monthly.

You don't know if today is a high or low point. If you buy over 12 months, during a 20% market drop you're still buying consistently—your average cost will be significantly lower than a one-time purchase.

Boring strategies are often profitable strategies. Exciting strategies are often losing strategies.

Step 5: Write down the rules

Before entering, write down three rules, print and post on the wall, or set as phone wallpaper:

-

I will start monthly DCA of [amount] on [date], for [number of months]

-

I will not change the plan due to short-term volatility—whether up 20% or down 20%, continue DCA

-

I will evaluate whether to adjust after [3 years / exceeds 30% of portfolio / urgent need for money]

You must know: The rational judgment you can write today will likely be overridden by emotions when the market fluctuates violently. And this rule printed on the wall is the contract between you and your future out-of-control self.

XI. Mistakes You Will Definitely Make in the Next 12 Months

Mistake 1: Stop DCA when the market crashes. On the day it drops -15%, your instinct is “stop quickly.” Wrong—this is precisely when you should keep buying.

Mistake 2: Double down on buying when the market soars. After three months of gains, think “speed up progress”—this is chasing highs.

Mistake 3: Turn “investing” into “watching the screen.” Start checking your account ten times a day after starting DCA—you've already slid from investor to gambler. Uninstall the app, check only once a month.

Mistake 4: Listen to rumors and add positions. Group recommends “must rise tenfold”—99% wrong, 1% you can't distinguish. Except for your list, ignore everything.

Mistake 5: Calculate the account. Newbies love to calculate “how much I made.” Paper profits before selling are not yours. Don't calculate for 5 years.

These five mistakes all stem from the same root—your worldview is not stable enough.

If you truly believe AI is a 10-year theme, a 20% drop won't panic you (you might even be happy for cheap chips). If your judgment is rented, a 5% drop makes you doubt life.

The stability of worldview determines the stability of your execution.

XII. Finally, Why Do You Want to Buy?

Back to the opening question—Why do you want to buy?

If after reading this you can give an answer that is your own, then today you are closer to the truth than 95% of retail investors.

Not because you are smarter than them. Because you are willing to slow down, first think clearly why, then do what.

Remember, the smallest gap between ordinary people and large institutions, professional traders, IQ150 is time. You and they alike only have 24 hours a day. Everyone equally needs to wait the same amount of time to see the fruit ripen.

Institutions face quarterly performance pressure, client redemption pressure, outperforming peers pressure daily. They must trade daily, must time, must chase themes.

You don't have to.

DCA into global indices for 30 years yields ~8-10% compound return—already beating 80% of actively managed funds.

You research nothing, analyze nothing, just mechanically execute—your long-term return exceeds most professional investors.

Then why do you still risk buying AI individual stocks?

Because we all want to feel we “participated in the era.” Because we all fear missing obvious opportunities like NVIDIA. Because our instinct tells us “inaction is failure.”

But in investing, ‘inaction’ is often the strongest action.

-

First have worldview, then have stocks. Buying without worldview is essentially gambling.

-

Follow capex, not words. How much real money one is willing to spend determines their true belief in the future.

-

Money is not for rushing to invest. Opportunities will always come, but principal only once.

You must know, AI won't crash because of you; AI won't be irrelevant to you because you entered three months late—but once your principal goes all-in at the wrong time, it may take five years to break even.

Those five years are your most expensive price.

Suggest you print this and post it on the wall:

Epilogue

These days many people ask, what to buy? How to open an account?

I always say: Really, don't rush to open an account and buy stocks.

Do one thing tonight: Find a piece of paper, write “Why I believe AI is the main theme for the next 10 years”—in your own words, at least 500 words.

Can't write it—you don't have a worldview yet, don't invest yet. Can write it—your worldview withstands this simple test, you can start executing.

Believe me, this one piece of paper is more important than buying any stock today.

Because it's the beginning of your independent investment thinking.

It will accompany you for the next 30 years—and 30 years of compounding is what you can truly win from this era.

Take your time. Get the first step right.