Author: Common Sense Investor (CSI)

Compiled by: Deep Tide TechFlow

Deep Tide Guide: With the dramatic changes in the macroeconomic environment in 2026, market logic is undergoing a profound shift. Veteran macro trader Common Sense Investor (CSI) presents a contrarian view: 2026 will be the year bonds outperform stocks.

Based on the U.S. government's heavy interest payment pressure, the deflationary signals released by gold, the extremely crowded bond short positions, and the imminent trade conflicts, the author believes that long-duration U.S. Treasuries (such as TLT) are at an inflection point with an "asymmetric game" advantage.

At a time when the market generally considers bonds "uninvestable," this article, through rigorous macro mathematical deduction, reveals why long bonds could become the highest-returning asset in 2026.

The main text is as follows:

Why I Am Overweight TLT and TMF — and Why Stocks Will Underperform in 2026

I do not write these words lightly: 2026 is destined to be the year bonds outperform stocks. This is not because bonds are "safe," but because macro mathematics, positioning, and policy constraints are converging in an unprecedented way—and this situation rarely ends with "Higher for Longer."

I have put my money where my mouth is.

TLT (20+ Year Treasury ETF) and TMF (3x Leveraged Long 20+ Year Treasury ETF) currently make up about 60% of my investment portfolio. This article compiles data from my recent posts, adds new macro context, and outlines a bullish scenario for long-duration bonds, especially TLT.

Core Arguments at a Glance:

-

Gold's Movement: Gold's historical performance does not signal sustained inflation—it signals deflation/deflation risk.

-

Fiscal Deficit: U.S. fiscal math is collapsing: approximately $1.2 trillion in annual interest expenses, and rising.

-

Issuance Structure: Treasury bond issuance is skewed short-term, quietly increasing systemic refinancing risk.

-

Short Squeeze: Long bonds are one of the most crowded short positions in the market.

-

Economic Indicators: Inflation data is cooling, sentiment is weak, labor market pressures are rising.

-

Geopolitics: Geopolitical and trade headlines are turning "risk-off," not "reflationary."

-

Policy Intervention: When something breaks, policy always turns to lowering long-end rates.

This combination has historically been rocket fuel for TLT.

Gold Is Not Always an Inflation Warning Bell

Whenever gold rises more than 200% in a short period, it signals not runaway inflation but economic stress, recession, and falling real rates (see Chart 1 below).

Historical experience shows:

-

The gold surge in the 1970s was followed by recession + disinflation.

-

The early 1980s surge was followed by a double-dip recession, breaking inflation.

-

The early 2000s gold rise foreshadowed the 2001 recession.

-

The 2008 breakout was followed by a deflationary shock.

Since 2020, gold has risen about 200% again. This pattern has never ended in lasting inflation.

When growth flips, gold acts more like a safe-haven asset.

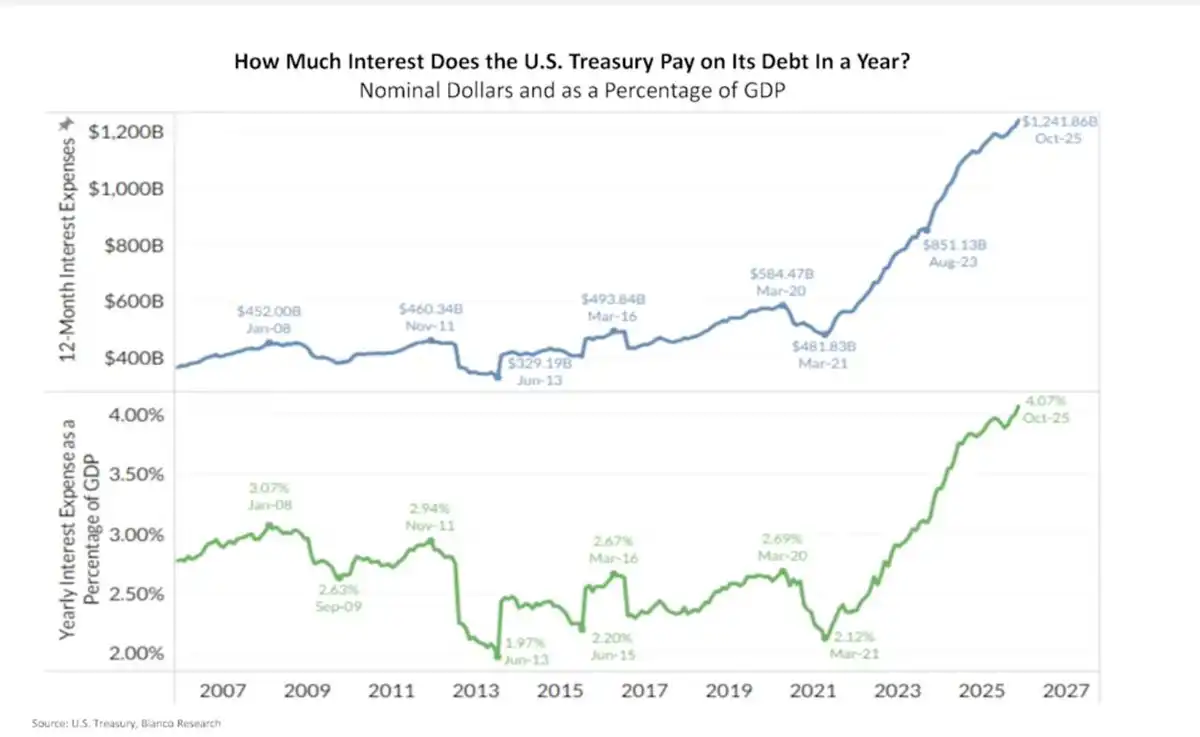

U.S. Interest Expenses Are Exploding Compounded

The U.S. currently has annual interest expenses of about $1.2 trillion, roughly 4% of GDP (see Chart 2 below).

This is no longer a theoretical issue. This is real money flowing out—and interest compounds rapidly when long-term yields stay high.

This is so-called "Fiscal Dominance":

-

High rates mean higher deficits

-

Higher deficits mean more debt issuance

-

More debt issuance leads to higher term premium

-

Higher term premium leads to higher interest expenses!

This doom loop won't resolve itself with "Higher for Longer." It must be resolved through policy intervention!

The Treasury's Short-Term Trap

To ease immediate pain, the Treasury has drastically cut long-bond issuance:

-

20/30-year bonds now make up only about 1.7% of total issuance (see Chart 3 below).

-

The rest is all pushed into short-term T-bills.

This doesn't solve the problem—it just kicks the can down the road:

-

Short-term debt constantly rolls over.

-

Refinancing will happen at future rates.

-

The market sees the risk and demands a higher term premium.

Ironically, this is why long-end yields stay high... and why they will collapse violently if growth cracks.

The Fed's Trump Card: Yield Curve Control

The Fed controls the short end, not the long end. When long-end yields:

-

Threaten economic growth

-

Trigger exploding fiscal costs

- <极="ltr" role="presentation">Disrupt asset markets

...the Fed has historically only done two things:

-

Buy long bonds (QE)

-

Cap yields (Yield Curve Control)

They won't act preemptively. They only act after stress appears.

Historical references:

-

2008–2014: 30-year yield fell from ~4.5% to ~2.2% → TLT surged +70%

-

2020: 30-year yield fell from ~2.4% to ~1.2% → TLT surged +40% in under 12 months

This isn't just theory—this has happened before!

Inflation Is Cooling, Economic Cracks Appearing

Recent data shows core inflation falling back to 2021 levels (see Chart 4).

-

CPI momentum is fading.

-

Consumer confidence is at a decade low.

-

Credit stress is building.

Labor market is starting to crack.

Markets are forward-looking. The bond market is already starting to smell this.

Extremely Crowded Short Positions

TLT's short interest is very high:

-

Approximately 144 million shares sold short.

-

Days to cover exceeds 4 days.

Crowded trades don't unwind slowly. They reverse violently—especially when the market narrative shifts.

And importantly:

"Shorts piled in AFTER the move, not before."

This is classic late-cycle behavior!

Smart Money Is Moving In

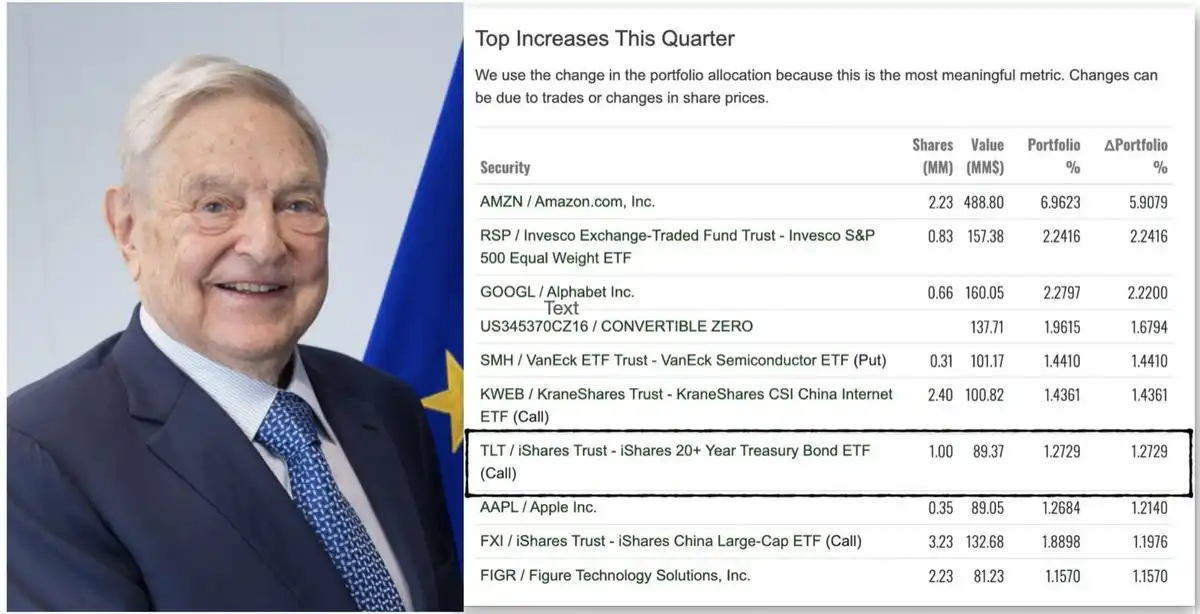

Recently, widely circulated 13F institutional holding reports showed a large fund's top quarterly additions included a significant number of TLT call options.

Regardless of who gets the credit, the message is simple: Sophisticated capital is starting to reposition for duration. Even George Soros's fund held TLT call options in the latest 13F disclosure.

Deflationary Shock from Tariff Frictions

The latest news is reinforcing the "risk-off" logic. President Trump announced new tariff threats targeting the Denmark/Greenland dispute, and European officials are now openly discussing freezing or suspending participation in the EU-US tariff agreement in response.

Trade friction will:

-

Hurt growth

-

Squeeze margins

-

Reduce demand

-

Push capital into bonds over stocks

This is not an inflationary impulse; it is a deflationary shock.

Valuation Mismatch: Stocks vs. Bonds

Today's stock pricing reflects:

-

Strong growth

-

Stable margins

-

Benign financing conditions

While bond pricing reflects:

-

Fiscal stress

-

Sticky inflation fears

-

Permanently high yields

If just one of these narratives is wrong, returns will diverge violently.

Long-duration bonds have "convexity"; stocks do not.

Upside Case Analysis for $TLT

TLT has:

-

An effective duration of ~15.5 years

-

You earn ~4.4–4.7% yield while you wait

Scenario Analysis:

-

If long-end yields fall 100 basis points (bps), TLT price return is +15–18%.

-

Fall 150 bps, TLT return is +25–30%.

-

Fall 200 bps (not extreme historically),意味着 it could surge +35–45% or more!

This doesn't include interest income, convexity bonuses, or the acceleration effect of short covering. This is why I see "asymmetric upside."

Conclusion

Honestly: After the carnage of 2022, I swore I'd never touch long bonds again. Watching duration assets get crushed was a deeply frustrating experience.

But the market doesn't care about your psychological trauma—it only cares about probabilities and prices.

When everyone agrees bonds are "uninvestable," when sentiment bottoms, when shorts pile up, when yields are high and growth risks are rising...

That's when I start buying!

-

TLT + TMF currently make up ~60% of my portfolio. I made 75% returns in the 2025 stock market and redeployed most of it into bond ETFs in November 2025.

-

I am "getting paid to wait" (earning over 4% yield).

-

My position is based on policy and growth shifts, not flimsy narratives.

2026 will finally be the "Year of the Bond."