Curry, Shenchao TechFlow

Shenchao Insights:

Strategy, which holds 847,000 Bitcoin, officially rewrote its four-year 'buy only, never sell' script on June 29 by launching a 'Digital Credit Capital Framework'. The new framework authorizes the sale of Bitcoin to raise up to $12.5 billion, establishes a $25.5 billion cash reserve, raises the STRC dividend rate to 12%, and authorizes up to $10 billion each for repurchasing its own securities. This comes against a backdrop where MSTR plunged 36% in eight days, the preferred stock STRC fell to about 24% below its face value, and the annual dividend obligation quadrupled in a year to $12 billion. For holders, this is a 'stop-loss plan', but whether it will work depends on the Bitcoin price.

Strategy (formerly MicroStrategy) has officially acknowledged that the flywheel of buying Bitcoin indefinitely by issuing preferred stock can no longer keep spinning.

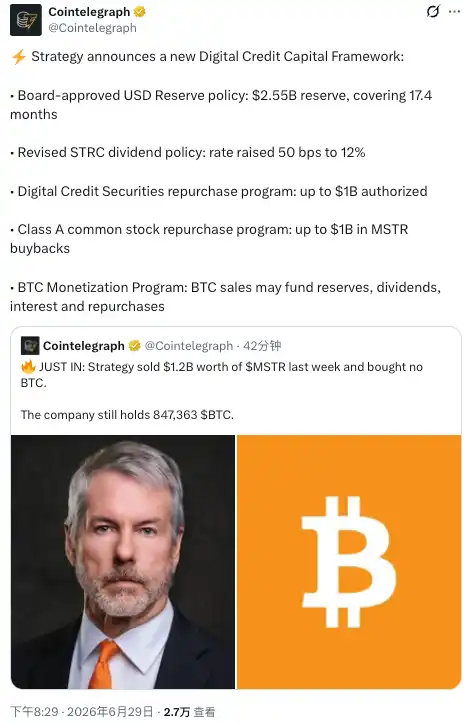

On June 29, the world's largest corporate Bitcoin holder announced the launch of a 'Digital Credit Capital Framework', introducing a comprehensive set of cash reserves, repurchase, and Bitcoin sale mechanisms to provide a safety net for its nearly out-of-control capital structure. The framework consists of five components: a USD reserve policy, a revised STRC dividend policy, a Digital Credit Securities Repurchase Plan, a Class A Common Stock Repurchase Plan, and a Bitcoin Monetization Plan.

The most impactful item is this: the company's board has authorized the sale of Bitcoin to raise up to $12.5 billion, to be used to supplement the cash reserve, pay preferred stock dividends and interest, or repurchase its own securities. For a company that built its faith on 'never selling Bitcoin', this is akin to officially laying down the institutional runway for selling.

Founder Michael Saylor's wording in the statement has already shifted from the past. He said Bitcoin remains the company's 'primary treasury reserve asset,' but immediately admitted: 'Digital credit requires liquidity, discipline, and proactive capital management.'

Translated, it means holding Bitcoin alone can no longer support the $1.2 billion annual dividend bill.

STRC Dividend Rate Soars to 12%, Preferred Stock Falling Below Par is the Trigger

To understand this framework, one must first see how passive Strategy's situation has become.

The company simultaneously announced it is raising the annual dividend rate for its variable-rate Series A Perpetual Preferred Stock STRC from approximately 11.5% by 50 basis points to 12.00%, effective for record dates on or after July 1. Superficially, this offers increased returns to investors, but the essence is being forced by the market—the STRC price has fallen to around $75-$76, a discount of about 24% from its $100 face value, hitting a record low.

STRC falling below par strikes at the heart of Strategy's financing model. This preferred stock was the company's 'money printer': continuously issuing new shares at or above face value to raise funds for buying Bitcoin. Once the price is deeply discounted, new preferred shares cannot be issued at a favorable price, and the entire financing flywheel jams. Julio Moreno, Head of Research at on-chain analytics firm CryptoQuant, calculated in a report on June 23: Strategy's annualized dividend obligation has skyrocketed from about $300 million at the beginning of the year to about $12 billion, quadrupling in one year, while the dividend coverage period shrank from over seven years to about 14 months. He directly advised the company to pause Bitcoin purchases and rebuild its cash reserve to about $28 billion first.

For preferred stock holders, a 12% coupon sounds attractive, but only if the company can pay. The new framework requires the USD reserve to cover at least 12 months of preferred stock dividend and interest obligations, effectively writing the ability to 'pay on time' into a hard constraint.

$25.5 Billion Cash Reserve: Shifting from 'HODLing' to 'HODLing Cash'

Strategy's cash reserve is visibly swelling, in the opposite direction of its past strategy.

According to the company's 8-K filing, as of June 28, the USD reserve balance was $25.5 billion, including anticipated cash proceeds from Class A common stock ATM offerings that have not yet settled. This number shows a significant jump compared to $1.4 billion on June 21 and $1.44 billion when it was initially established in early December 2025. Where is the money coming from? The answer is selling its own stock, not buying Bitcoin.

Operations over the past three weeks have already hinted at the pivot. In the week of June 22, the company bought only 520 Bitcoin for approximately $34.9 million, one-third of the previous week; during the same period, it sold 2.71 million shares of MSTR common stock, raising $335.5 million, but allocated less than 11% into Bitcoin, with the remainder all going to the cash reserve.

Cointelegraph posted on June 29 that Strategy sold $1.2 billion worth of MSTR shares last week and did not buy any Bitcoin. If accurate, this indicates that the intensity of selling shares to replenish cash is increasing (Note: The $1.2 billion weekly sale figure is significantly higher than previously disclosed weekly data and should be verified against the company's latest filing prior to publication). The company currently holds 847,363 Bitcoin with a weighted average cost of approximately $75,651 per coin.

The cost of shifting to 'HODLing cash' is dilution. Issuing new shares when the MSTR stock price is below its per-share Bitcoin Net Asset Value dilutes the amount of Bitcoin backing each share. MSTR fell to around $82 this week, approaching a two-year low of $81.81; the 'premium' that fueled the flywheel's operation no longer exists.

$10 Billion Each for Repurchases: Trying to Buy Back the Discount

The framework also hides two 'repurchase knives': the Digital Credit Securities Repurchase Plan and the Class A Common Stock Repurchase Plan, each with an authorization ceiling of up to $10 billion.

The logic isn't complicated. STRC and other preferred securities and MSTR common stock are trading at deep discounts. The company using cash (or proceeds from Bitcoin sales) to repurchase at low prices can theoretically narrow the discount and protect the price. Bitcoin critic Peter Schiff has repeatedly posted on X in recent days, saying Saylor's best option is to sell Bitcoin to repurchase shares and close the discount.

Now Strategy has written this suggestion into its formal framework, though Schiff simultaneously warned that forced Bitcoin sales could conversely crash the Bitcoin price, plunging the entire structure into a death spiral.

Whether the repurchases will work depends on how much cash the company has. For investors holding MSTR or preferred stock, the $10 billion authorization is just a ceiling, not a guarantee of full execution; the actual buying pace will depend on subsequent disclosures.

More Than Just Stopping the Bleeding: Legal Probes and Mounting Debt

This framework was hastily launched under multiple pressures; looking at financial numbers alone is insufficient.

On June 25, Rosen Law Firm disclosed it is investigating Strategy and Saylor, alleging they may have issued 'materially misleading information' to investors regarding Bitcoin holdings. The investigation covers all five of the company's securities: MSTR, STRF, STRC, STRK, and STRD. The probe is still in its early stages with no formal lawsuit yet, but the timing coincides with the continuous decline in stock price.

The debt situation is equally tight.

According to multiple media reports, Strategy's total debt on its balance sheet is about $8.2 billion. Since 2026, its cash reserve has shrunk by approximately 38%, and the company also conducted a debt buyback in May. With Bitcoin currently around $60,000, it has fallen below the cost basis of all Strategy's purchase batches from 2024 to 2026. Paper losses range between $10.6 billion and $14 billion (varies by source).

For investors on the sidelines, the key metric to watch now is the discount of the MSTR stock price relative to its per-share Bitcoin Net Asset Value. If the discount remains persistently deep, the ATM offering engine will stall. That is the outcome this framework truly aims to avoid—yet may not be able to prevent.