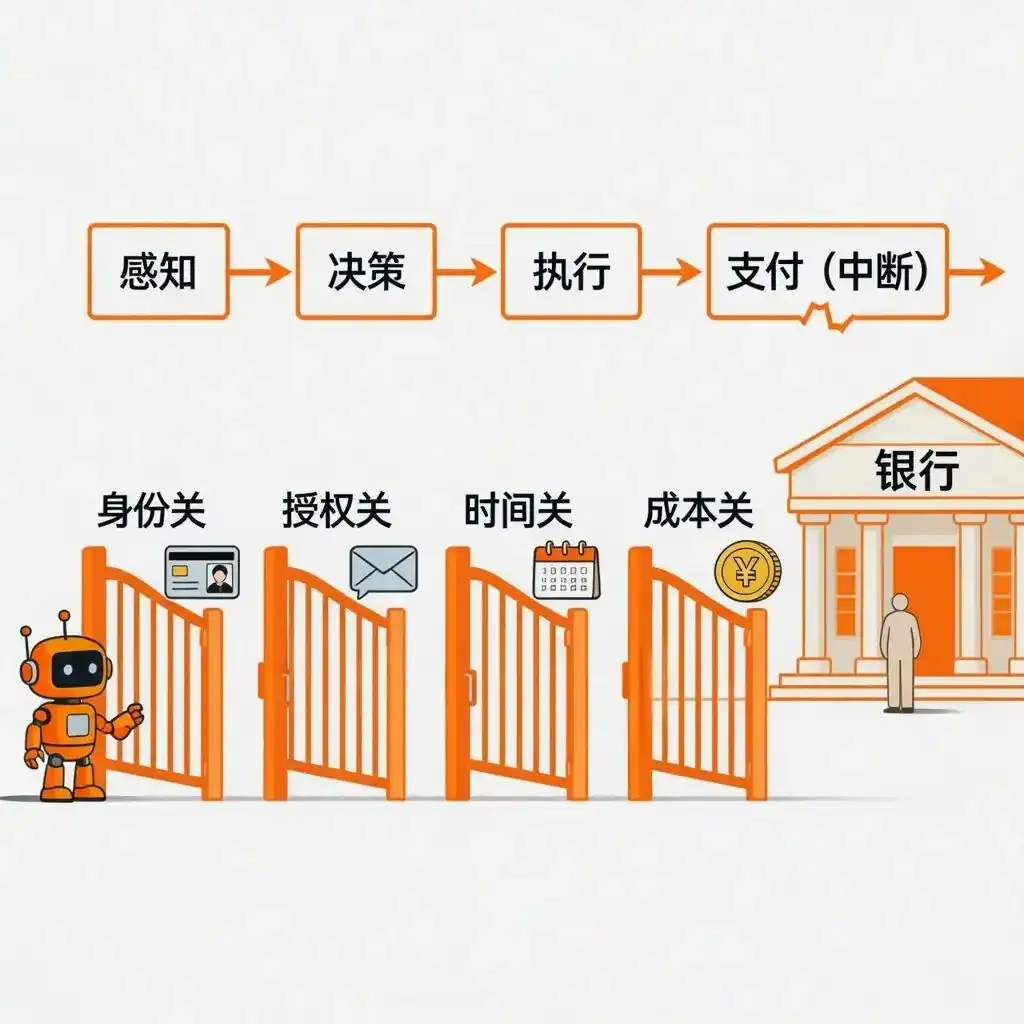

Generative AI is evolving from "chatbots" into capable AI Agents that can get things done on their own. A practical problem emerges: How do these silicon-based "employees" receive payments and make payments? The traditional banking system – requiring real-name authentication, manual authorization, and corporate accounts – is inherently incompatible with AI Agents.

A rapidly emerging answer is: building a native "currency layer" for AI using stablecoins (like USDC, USDT, and interest-bearing stablecoins). This article will dissect the practical implementations in this field by leading companies such as Coinbase, Circle, and Stripe, while also discussing the associated compliance and security risks.

The technical infrastructure is ready, but how to effectively drive adoption remains a significant challenge.

I. The "Payment Disconnect" Hindering AI Agent Commercialization

Today's AI Agents are already quite capable: booking flights, writing code, calling APIs... But they hit a wall at the "payment" step. Traditional payment systems are designed for humans – requiring ID cards, verification codes, weekday operations, and relatively high transaction fees. These are all obstacles for Agents.

Specifically, the traditional payment system presents four major hurdles for Agents:

- Identity Hurdle: Opening a bank account or getting a credit card requires ID, facial recognition, or bank statements – things an Agent simply doesn't have.

- Authorization Hurdle: Payments often require SMS verification codes, manual confirmation clicks, or 3D Secure authentication. Agents can't receive SMS or click buttons.

- Time Hurdle: Banks process transfers only on weekdays during business hours, while Agents need to work 24/7.

- Cost Hurdle: Fixed fees per transaction (e.g., 30 cents minimum for credit cards) make models like per-use fees of $0.001 economically unviable. Yet, this is precisely the kind of micropayment, high-frequency billing model (e.g., per API call, per usage) that Agent economic activity requires.

A more fundamental issue is that the entire payment system was never designed for "program-to-program" direct transfers. Even between two tech companies, the flow often is: Agent generates order → emails a human → human approves → human logs into online banking to transfer → counterparty's finance reconciles. The Agent can only handle the first steps and final recording; the core action of "moving money from A to B" requires human intervention.

Current Attempts: Mimicking Humans, Not Creating New Accounts for Agents

The industry has made many attempts, but they essentially involve making Agents "pretend to be human":

- Virtual Credit Cards + APIs: Agents call Stripe or similar interfaces to pay, but these are still tied to a human's identity and card. Once risk control flags unusual activity (too fast, strange amounts), it requires human verification.

- Robotic Process Automation (RPA): Making Agents click on online banking pages like a human. If the bank's website updates, CAPTCHAs change from numbers to sliders, or an extra verification step is added, the script breaks.

- Delegated Payments: A human pre-approves a spending limit for the Agent, who can spend within it. But approving the limit, renewing it, and auditing still require human action.

The common flaw of these solutions: Agents don't have their own accounts; they can only "live in borrowed shells." Their autonomy can be revoked at any time by the bank or platform.

Why Stablecoins Are a Better Solution: Giving Agents a Native "Wallet"

For Agents to truly manage money autonomously, they need a programmable, human-identity-free, 24/7 operating, fully auditable, and value-stable monetary system. Stablecoins happen to provide exactly that:

- Programmable: Payments can be coded directly, executing automatically when conditions are met, without a human pressing a button.

- Permissionless: Agents can generate their own wallet addresses without queuing at a bank to open an account.

- 24/7 Operation: No weekends, holidays, or closing times.

- Transparent Ledger: Every transfer is on the blockchain, visible to all, facilitating audits.

- Value Stability: Unlike Bitcoin or Ethereum with their high volatility, suitable for pricing and long-term settlement.

Stablecoins aren't absolutely safe either. Fiat-collateralized ones like USDC and USDT rely on centralized custodians and audits, and have experienced brief depegs historically; purely algorithmic stablecoins have proven unreliable. The stablecoins discussed here primarily refer to regulated, mainstream, fiat-collateralized stablecoins.

II. Who is Building for Payment-Enabled Agents?

The direction is clear, but who is laying the groundwork? Over the past year and a half, leading companies like Coinbase, Circle, and Stripe have moved beyond conceptual discussions, launching usable tools and protocols. Each has chosen a different angle: some focus on Agent wallets and payment rails, others solve cross-chain settlement, and others bridge fiat and stablecoins.

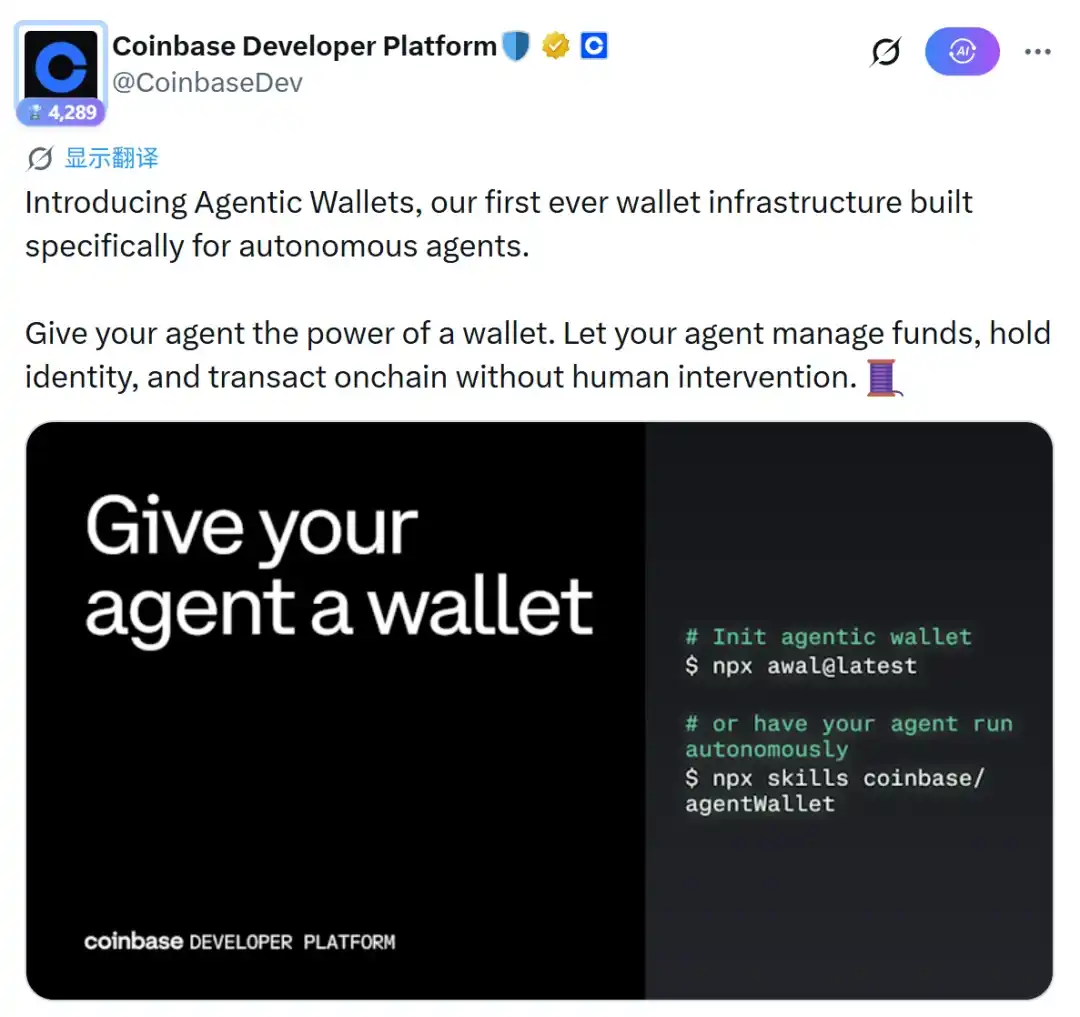

Coinbase: Base Chain + AgentKit Tool Suite

Coinbase's AgentKit is a developer toolkit enabling AI Agents with on-chain wallets and payment capabilities. In February 2026, they launched Agentic Wallets, built-in with five core functions: identity authentication, storing funds, making payments, trading, and earning interest. Underlying this is the x402 protocol, co-developed with Cloudflare, specifically designed for "machine-to-machine" payments.

By early 2026, this protocol had processed over 50 million transactions. Security-wise, Agentic Wallets support setting limits like "maximum spend per session" or "maximum per transaction."

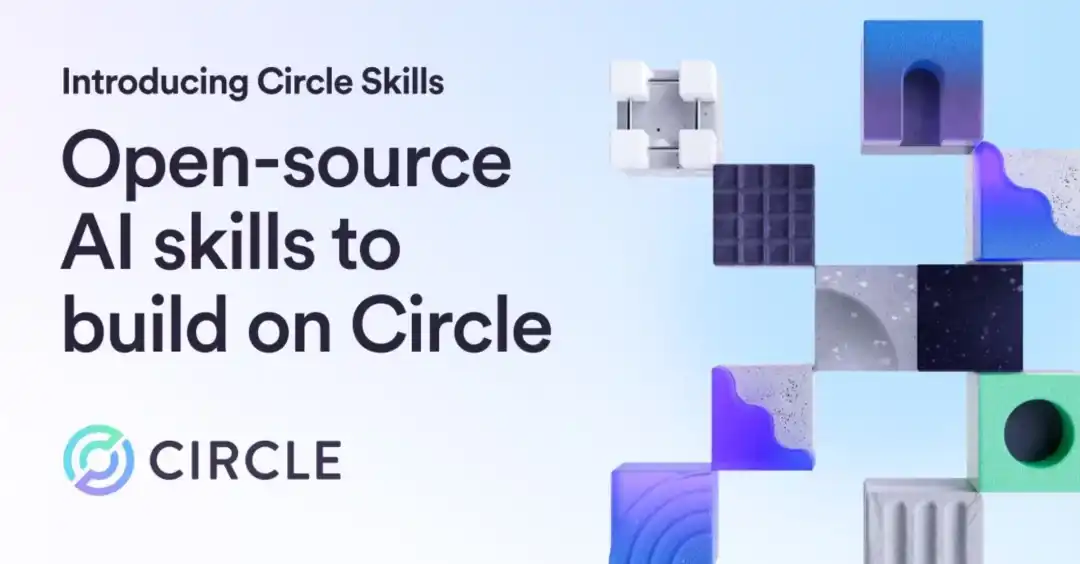

Circle: CCTP Cross-Chain Protocol + AgentStack

Circle's CCTP (Cross-Chain Transfer Protocol) solves the problem of securely transferring USDC across different blockchains. It employs a "burn-and-mint" mechanism, avoiding reliance on third-party bridges, making it inherently more secure and compliant. Building on this, Circle launched AgentStack in 2025, containing: Agent wallets (supporting gasless transactions), CCTP, Gateway for micropayments (supporting as low as $0.000001), and an Agent services marketplace.

CCTP added a Hooks feature, allowing AI Agents to attach business information during cross-chain transfers, enabling one-click operations like "automatically deposit or invest upon cross-chain receipt."

In March 2026, Circle further launched the Circle Skills open-source library, enabling AI Agents (like Claude) to autonomously decide: when to use CCTP and when to use Gateway micropayments.

Stripe: Stablecoin API, Bridging Traditional Commerce and On-Chain World

Stripe officially launched its stablecoin API in 2025 and, through the acquisition of stablecoin infrastructure company Bridge, built a compliant bridge from traditional commerce to the on-chain ecosystem. In October of the same year, Stripe launched stablecoin subscription payments, initially supporting USDC subscriptions on Base and Polygon chains. They wrote smart contracts to solve the hassle of "needing manual signature for each payment" – users can save a wallet as a payment method, authorizing automatic periodic deductions.

Stripe handles backend ledger and KYC/AML compliance monitoring, shielding users from underlying blockchain complexities like private key management and gas fees. When AI Agents need to transact with traditional merchants, Stripe provides a legal and compliant channel for USD exchange and settlement.

Beyond the "big three," some traditional internet giants are also beginning to explore this space:

- AWS + Stripe + Coinbase (May 2026): A tri-party collaboration launched USDC-based payment infrastructure, enabling AI Agents to pay for digital services like cloud services and API calls. Amazon Bedrock's AgentCore Payments serves as the payment layer, settling on the Base chain in about 200 milliseconds at a cost of less than 1 cent per transaction. Stripe implemented its own MPP (Machine Payment Protocol), supporting "streaming payments" – real-time deductions based on computing power or token consumption per second. On the same day, Stripe and Tempo released the MPP open standard, and Visa announced support.

- Google + Coinbase (September 2025): Jointly launched the Agent Payments Protocol (AP2), integrating Google's Agent-to-Agent communication framework (A2A) with Coinbase's x402 payment rail, enabling Agents to complete the full cycle of "negotiate price → pay → issue receipt." Initial partners included ServiceNow, Salesforce, PwC, Shopee, and Worldpay.

- Virtuals Protocol + Ethereum Foundation (March 2026): Jointly proposed ERC-8183 (Agentic Commerce), an on-chain commercial settlement standard specifically for AI Agents. Its core is the concept of a "Job": a smart contract locks funds between the client, provider, and arbiter, settling according to a state machine of "create → fund → deliver → complete/reject/expire."

III. Typical Use Cases for the Silicon-Based Economy

With the above infrastructure, if AI Agents truly have their own stablecoin wallets – capable of receiving and sending payments, cross-chain operations, and earning interest – they are no longer isolated tools but can form a self-operating micro-economy. Here, we analyze use cases that have seen partial implementation in the short term and are most likely to realize the value of a silicon-based economy.

Use Case 1: DeFi Yield Optimization – Letting Agents "Make Money Breed Money"

In traditional finance, idle cash in checking accounts earns minimal interest. In the DeFi world, stablecoin holders can deposit funds into lending protocols (like Aave, Morpho, Compound) to earn yield. The problem is that interest rates across different protocols and chains are constantly changing, making it difficult for humans to monitor and rebalance frequently. This is precisely where AI Agents excel.

Take the Walbi platform: it processed 187,000 transactions autonomously initiated by AI Agents over 14 weeks, involving 9,500 unique Agents – with zero human intervention. Agents automatically scan lending rates across chains, calculate net profits after gas fees, and move funds from low-yield pools to high-yield ones. Consider ZENITH's approach: deploying independent AI Agents on major public chains like Ethereum, Arbitrum, Optimism, and Base, each managing DeFi protocols (Aave, Morpho, Compound, etc.) on its chain. Once an Agent detects a significant interest rate differential between chains that can cover cross-chain costs, it transfers funds via protocols like CCTP.

Why are Agents essential for such tasks? Manual human operation faces three difficulties: 1) tracking rate changes across multiple protocols is data-intensive; 2) cross-chain operations are cumbersome, requiring manual signatures for each; 3) high-frequency rebalancing incurs prohibitive fees and time costs. AI Agents paired with stablecoins enable 24/7 monitoring, millisecond-level response, automatic execution, and fully traceable, auditable transactions.

Use Case 2: Ultra-Micropayments – Unlocking the Long-Tail "Pay-Per-Use" Economy

Traditional payment systems have fixed fees per transaction (e.g., 30 cents minimum for credit cards), making micropayments (like $0.001) economically unfeasible. Yet for AI services (billing per API call, per generated image, per query volume), micropayments are the most natural pricing model. The low fees and support for tiny denominations inherent in stablecoins make micropayments viable again.

The x402 protocol co-developed by Coinbase and Cloudflare embeds payment directly into HTTP requests. When a client accesses a paywalled API, the server returns a 402 status code (Payment Required) with a payment request (e.g., "Please pay 0.001 USDC"). The client's built-in Agent wallet pays automatically, granting access to the data or service – by early 2026, this protocol had processed over 50 million transactions. Typical scenarios include: API paywalls, pay-per-access high-value datasets, and real-time market data subscriptions.

Circle's Gateway Nanopayments goes further, designed specifically for high-frequency, minuscule transactions, supporting USDC transfers as low as $0.000001, with the recipient paying no gas fees. The underlying principle is "batch settlement + state channels": multiple micropayments are aggregated off-chain, with only the net amount settled on-chain. This enables Agents to pay in real-time for every API call, every megabyte of storage, every second of compute, with near-zero fees. Without micropayments, AI Agent commercialization is limited to subscription packages or prepaid models. With it, Agents can meter usage as precisely as utilities, and collaboration between Agents (e.g., Agent A paying Agent B fractions of a cent per model inference) can occur with minimal friction.

Use Case 3: From "Idle Funds" to "Auto-Yield" – Advanced Practices with Yield-Bearing Stablecoins

In traditional finance, money in corporate checking accounts earns little to no interest. To invest, humans must research products, sign agreements, manually transfer funds – a cumbersome and time-sensitive process many SMEs simply forgo. Stablecoins combined with AI Agents fundamentally overturn this logic.

When an Agent holds yield-bearing stablecoins (like aUSDC, sDAI, eUSD), the wallet balance automatically accumulates yield – these stablecoins are essentially deposit receipts for DeFi protocols, with interest reflected in the token's rising exchange rate. Agents can "earn interest by doing nothing." More crucially, a well-designed yield-management Agent can automatically switch between different yield-bearing assets, achieving "yield while maintaining payment liquidity."

A February 2026 example is Ymax's yield orchestration platform: users sign once to authorize, and the Agent automatically allocates funds across multiple vaults like Morpho, Aave, Compound, rebalancing based on real-time rates, with yield accruing by the second, all hands-off. Another, aarnaFinance, offers AI-managed vaults integrating over twenty on-chain yield sources (lending, staking, vault strategies), with Agents dynamically constructing portfolios, achieving 8-12% annual yield in stablecoin terms. For comparison: traditional bank savings accounts typically yield below 0.5%, and USD money market funds around 4-5%.

For AI Agents, yield-earning capability isn't just an add-on; it may change the underlying economic logic: a self-yielding Agent could use interest to cover its operating costs (gas fees, API call fees), even accumulating capital for more complex tasks. The Agent is no longer a "cost center" but a "self-sustaining" micro-economy. When billions of such Agents run simultaneously, they could spawn a novel, entirely program-driven financial sub-market.

IV. Necessary Challenges for Scaling Adoption

Infrastructure exists, use cases are proven, but hold the celebration – without overcoming these hurdles, mass commercial adoption remains distant.

Private Key Management and Security

A major flaw in many current AI Agent wallet designs: directly handing private keys or API credentials to the Agent. If subjected to a "prompt injection attack" (e.g., a malicious actor tricking the Agent via input), the private key could be leaked. Auditing firm Sherlock lists "malicious third-party skills," "indirect prompt injection," "credential exposure," and "poor wallet permission design" as the top security risks for Web3 Agents in 2026. On-chain transactions are irreversible; one wrong signature can mean permanent loss.

A real-life lesson: In the February 2026 Owockibot incident, an autonomous AI Agent leaked its hot wallet private key in multiple places, forcing the project team to sever the Agent's internet and crypto operation permissions. The founder admitted: "I severely underestimated the security difficulty of this project and must re-architect from a security-first perspective."

Currently explored solutions include:

- Isolated Signing Layer: The Agent can propose "I want to pay X amount to Y," but the actual signing occurs in a separate hardware security module or custody layer.

- MetaMask Smart Account Approach: Agents can initiate transactions but never access private keys. Fine-grained permissions are managed via ERC-4337 smart accounts and ERC-7710 delegation authorizations.

Compliance and Regulatory Gaps

Traditional KYC needs to evolve into "Know Your Agent" (KYA), but legally, such a category doesn't exist. Agents are not legal entities; they cannot own assets, sign contracts, or bear liability. Who is responsible if an Agent sends money to the wrong place or is hijacked by a hacker? This question remains unanswered. Consider cross-border fund monitoring – the high-frequency, complex transfers between multiple Agents present technical and legal blanks for Anti-Money Laundering (AML), tax, and compliance oversight. Circle's AgentStack includes spending limits and black/white lists, but cross-border Agent payments easily enter regulatory gray areas. Stripe's stablecoin API is currently only available to US businesses. Liability attribution is equally murky: Agentic Wallets rely on user-set limits, but if the Agent errs, is the user or developer liable? The AP2 protocol runs some compliance checks (like Travel Rule, sanction screening) before transfers, but this is nascent.

Technical Risks and AI Intent Accuracy

Smart contract vulnerabilities don't vanish just because an AI controls the funds. AI-managed pools remain susceptible to flash loan attacks, oracle manipulation, and no protocols are specifically designed to defend against malicious Agents. More thorny is AI intent deviation. Even if wallets and payment rails are secure, how to ensure an Agent executing complex, multi-step financial tasks truly follows the user's intent? Auditing firm Sherlock highlighted a key issue: a prompt can "guide" an Agent's behavior, but guidance isn't control. Errors can arise in many ways – model reasoning errors, external information pollution, malicious third-party skill injection... each could cause irreversible fund loss. The industry's research on safety boundaries and verification mechanisms for "intent-driven execution" is currently far from sufficient.

Conclusion and Outlook

The deep integration of AI Agents and stablecoins is fundamentally altering the settlement architecture of global digital commerce. Infrastructure built by companies like Coinbase, Circle, and Stripe has already closed the loop from "Agent → cross-chain → fiat world," elevating stablecoins from "speculative tools" to the "native wallets of the silicon-based economy."

In the short term, private key management and security are the biggest roadblocks. Expect more hardware-isolated signing solutions and smart account authorization standards. Compliance-wise, some regions (like the EU under MiCA) may pilot KYA (Know Your Agent) frameworks.

From a medium-to-long-term perspective, those who can seamlessly integrate yield-bearing assets, provide user-friendly cross-chain hooks, and meet multi-Agent micropayment needs are poised to become the key infrastructure for the next-generation internet economy. Simultaneously, AI intent verification mechanisms (like formal verification, zero-knowledge proof-based intent proofs) are expected to mature, reducing "signing error" risks.

In this economy, Agents can earn, spend, invest, and settle contracts with other Agents autonomously. Humans are no longer approvers for every transaction but rather system designers and boundary setters. This is both exhilarating and disquieting. And the starting point for all this is the infrastructure重构 happening today.

Ultimately, the real question is no longer "Is it technically possible?" but rather, are we ready to embrace an on-chain economy comprised of hundreds of millions of self-operating AI Agents?