Author: Long Yue

Source: Wall Street News

Investors generally believe that quantum computing is still in the realm of science fiction, but Barclays' latest research report points out that this "too early" misconception might cause you to miss the most critical trend in the next 12 months.

According to Wind Trading Desk news, Barclays' analyst team recently released a research report titled "Quantum Computing: Correcting the Biggest Misconception Among Investors".

The core logic of the report is very straightforward: Wall Street underestimates the speed of technological breakthroughs and completely misunderstands the relationship between quantum and classical computing power (like NVIDIA). Barclays believes we are on the eve of transitioning from a "lab toy" to a "commercial tool".

Misconception 1: Quantum Computing is "Too Early"

Barclays' first correction is: Don't treat quantum computing as a purely long-term theme that "won't yield results for another decade."

The current market consensus is that perfectly functioning "Fault-Tolerant Quantum Computing" (FTQC) won't arrive until after 2030. This is correct, but Barclays reminds investors not to ignore the intermediate "tipping points".

Barclays points out that 2026 to 2027 will be the industry's watershed moment, when "Quantum Advantage" will be achieved.

More importantly is "how to define advantage". Barclays believes that "advantage is only proven when a system targets 100 logical qubits". It also cautions that any "claim of advantage" needs to be backed by "strong technical evidence", otherwise it's more like marketing than an inflection point.

"We expect major announcements within the next 12 months...... Quantum advantage will be proven when a system can stably run 100 logical qubits."

This is like the Wright brothers' first flight; although it couldn't carry passengers (commercialization), it proved that airplanes were better than horse-drawn carriages (quantum advantage). Once this signal appears, the valuation logic in the capital markets will be instantly reshaped.

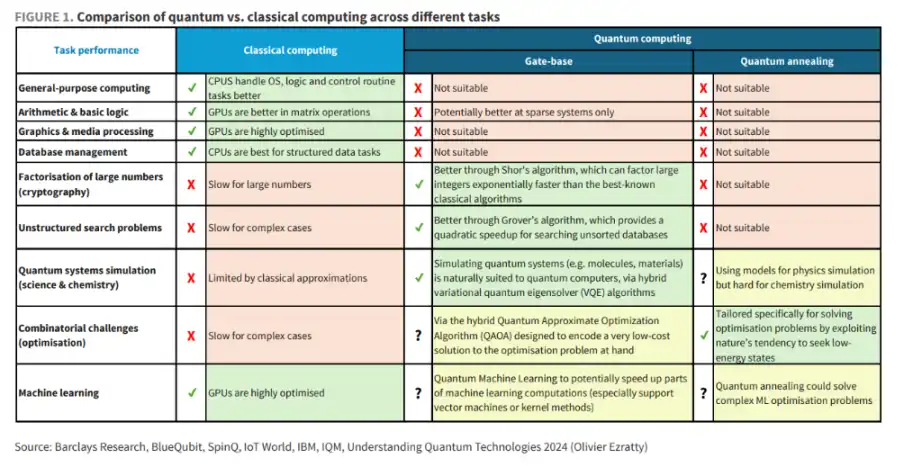

Misconception 2: Quantum will replace classical computing, so NVIDIA is finished?

This is the market's biggest cognitive bias. The report points out that many people think quantum computers are so powerful they will replace current CPUs and GPUs. Barclays refutes this: it's not a replacement relationship, but a "strongest assistant" relationship.

"Quantum computers will not replace classical computers as general-purpose machines, but will complement them."

The core logic behind this lies in "error correction": Qubits are very fragile and unstable (prone to errors). To make them work properly, an extremely powerful classical computing system is needed to monitor and correct them in real-time.

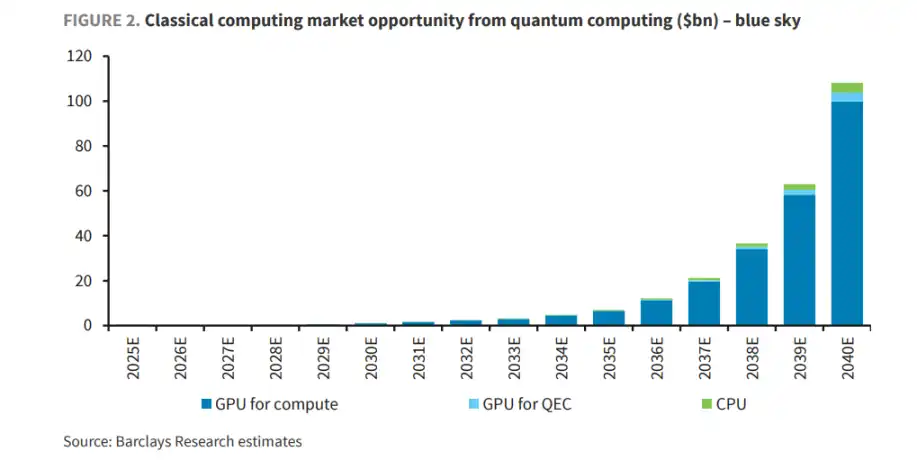

Barclays' research reveals a startling data relationship:

"Each logical qubit may require one GPU for error correction and control."

What does this mean? If you build a quantum computer with 1000 logical qubits, you would need to purchase 500 to 2000 GPUs to support it.

This is no longer competition, but symbiosis. The stronger the quantum computer, the more explosive the demand for chips from NVIDIA and AMD becomes. Barclays calculates that this "derived demand" could bring over $100 billion in incremental value to the classical computing market by 2040 in a blue-sky scenario.

Misconception 3: Quantum hardware is all similar, like buying a lottery ticket?

The truth about this misconception is that the field has already diverged, with clear strengths and weaknesses.

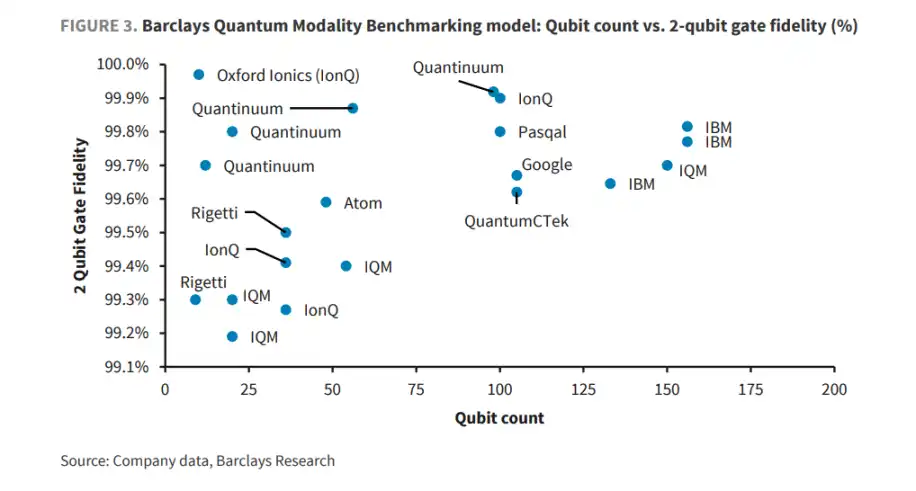

Quantum hardware approaches are not singular. Barclays categorizes mainstream physical qubit paths into electronic (superconducting, electron spin), atomic (trapped ions, neutral atoms), and photonic, among others, noting that their pros and cons stem from trade-offs between speed, accuracy, coherence time, external infrastructure (cryogenics, lasers, vacuum), and scalability.

Using a "quantum benchmarking model," Barclays highlights key points in the currently chaotic hardware landscape:

- Current "Accuracy King" — Trapped Ions: Represented by companies like Quantinuum and IonQ. Their advantage is accuracy, low error rates, and relatively mature technology.

- Future "Mass Production Dark Horse" — Silicon Spin: The direction Intel is pursuing. Although performance is modest now, it can leverage existing semiconductor fabs for manufacturing. Once breakthroughs occur, it's the easiest to mass-produce.

- Winning by Numbers — Neutral Atoms: Have a natural advantage in stacking large numbers of qubits.

Barclays concludes:

"Our testing indicates trapped ions are currently in the lead...... but the scalability of silicon spin warrants long-term attention."

Misconception 4: Encryption is about to be broken?

Regarding the panic that "quantum computers will crack bank passwords tomorrow," Barclays pours cold water on the idea: Think again, the computing power isn't there yet.

Cracking current RSA encryption requires thousands of perfect logical qubits, while humanity's top devices currently have only a few dozen. Barclays states bluntly:

"Quantum computers are not yet powerful enough...... modern encryption standards are not yet under threat."

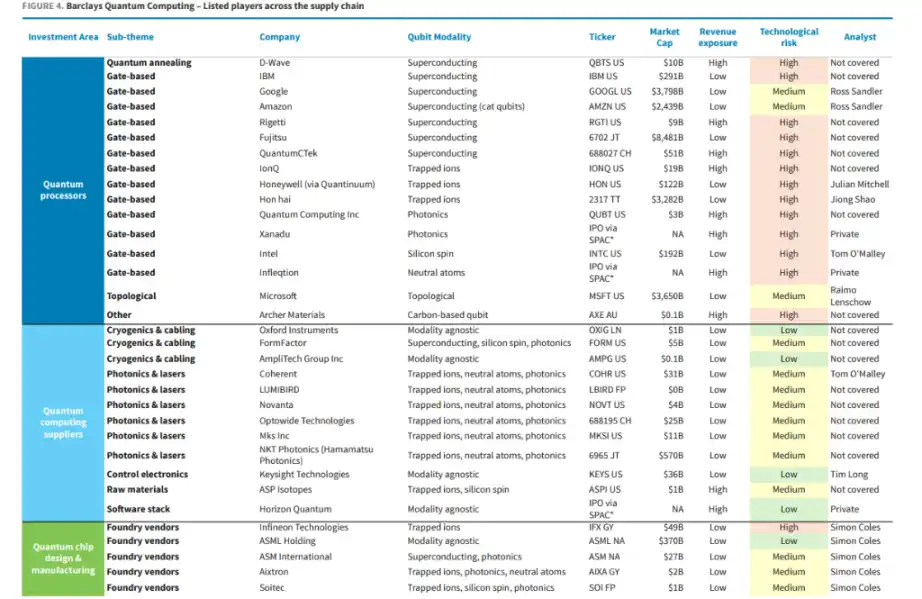

Misconception 5: The quantum theme has "only two or three companies worth investing in"

The market often perceives investment targets in this field as scarce, limited to a few well-known companies. But Barclays梳理 (sorted through) the entire industry chain, identifying 45 listed companies and over 80 private enterprises. They are mainly distributed across four areas:

1) Quantum Processors (system sales or QCaaS cloud access)

2) Quantum Supply Chain (cryogenics, lasers/optics, control electronics, materials, etc.)

3) Quantum Chip Design and Manufacturing (overlap with traditional semiconductor manufacturing)

4) Ecosystem Enablers (cloud, data center infrastructure, quantum simulators, quantum-classical integration: GPU/CPU/servers, etc.)

The framework provided by the report leans more towards "risk pricing": short-term often correspond to "higher revenue exposure" paired with "higher technical risk". It roughly categorizes technical risk as high (single approach), medium (few approaches), low (approach agnostic) based on whether the business model is tied to a single approach.

This also explains why the quantum narrative easily "focuses solely on pure quantum hardware stocks": their revenue exposure is most direct, but path uncertainty is also greatest; whereas the supply chain, semiconductor equipment & EDA, cloud & data centers, and hybrid integration segments might better transmit the "quantum progress → capital expenditure and supporting demand" linkage.