Written by: Pink Brains

Compiled by: AididiaoJP, Foresight News

Over the past three years, we have collaborated with more than 35 leading DeFi projects, handling their marketing efforts. We discovered that the most effective marketing campaigns are not designed from the project's perspective, but from the user's perspective: how users discover a product, how they build trust, and how they genuinely get involved.

Note: Pink Brains is a marketing studio specializing in DeFi, providing services such as KOL marketing and content creation (threads, analysis) for DeFi projects.

The thinking behind most crypto marketing guides is: select KOLs, allocate budget, launch the campaign, track impressions.

We have completely reversed this process. Instead of starting with tactics, we first study user behavior: How do DeFi users discover new protocols? What convinces them to try? What makes them stay?

How Do DeFi Users Discover New Protocols?

Crypto users typically discover opportunities on Twitter (X) first, then verify data on platforms like DefiLlama, DeBank, Artemis, Token Terminal, Moni, review the protocol's official documentation, and finally consider depositing funds.

The discovery process is socially driven, while the decision-making process is data-driven.

The actual path usually looks like this:

A trusted account posts about a new perp DEX – this post rarely triggers an immediate deposit.

The user will first check the project's official account, browse posts and reviews from other KOLs, learn about data like trading volume, TVL, incentive programs, quickly skim documentation and guides, and finally deposit a small amount of test funds.

That X post merely introduced the protocol to the user. What truly drives the decision is the KOL's content and real data.

This is why X remains the core battlefield for DeFi: it's where narratives form, vulnerabilities are exposed in real-time, and founders and researchers debate fiercely in the comments.

The practical takeaway for protocol teams is: the goal in the discovery phase is not to chase virality, but to be mentioned by accounts already trusted by data-driven users, and for all the data to hold up when users go to check. A strong X mention paired with thin TVL or a weak audit page will not convert truly valuable users.

What Are DeFi Users Focusing on in 2026?

This year, DeFi users are primarily attracted by several clear themes:

- New DeFi trends (tokenization, perpetual contracts, RWA, pre-IPO perps, and the crypto × AI wave)

- Airdrops requiring real contribution but higher risk

- Yields backed by real revenue

- Value-capturing tokens directly linked to product usage

- New types of trading venues

The common thread is: verifiable mechanisms, not marketing fluff.

New Narratives: Perps, RWA, Crypto × AI

What people are trading is changing.

Hyperliquid's HIP-3 upgrade enabled permissionless perpetual listings, subsequently birthing over 100 RWA markets (stocks, commodities, indices, forex, even pre-IPO assets) with cumulative trading volume exceeding $130 billion. By the end of Q1 2026, RWA markets accounted for over 90% of HIP-3 open interest.

@Ostium (an RWA-focused perpetual DEX on Arbitrum) proposes the "perpification" theory: a perpetual contract only needs a price oracle and a liquidity pool, not a full tokenization stack. This brings exposure to traditional markets on-chain faster than tokenized spot assets.

@tradexyz and @ventuals are delving into commodities and forex on Hyperliquid; Trade.xyz's Cerebras pre-IPO perpetual contract almost perfectly "priced" the stock hours before its NASDAQ debut.

Another major narrative is crypto × AI. Users focus not on the narrative itself, but on agentic payments and token incentive mechanisms aligned with AI.

- @opentensor ($TAO) completed its first halving at the end of 2025, currently runs 120+ active subnets, and generates real revenue demand.

- @virtuals_io (VIRTUAL) reported over $4 billion in agent GDP and $60 million in protocol revenue in Q1 2026, deployed 17,000+ agents, and co-authored cross-chain agent commerce standards with the Ethereum Foundation.

- @NEAR Protocol and @AskVenice hold core positions in private inference and data sovereignty.

Additionally, early connections in the crypto × robotics field (like @xmaquina, Robotics Capital Markets) are emerging.

This sector is volatile and has many low-quality projects, but what users genuinely care about is the revenue and real usage of top projects.

Airdrops, But the Bar Has Been Raised Significantly

Airdrops remain a key driver, and most farmers are still looking for the next HYPE, but the era of easy money is over.

Projects now increasingly demand real contribution: sustained trading, providing real liquidity, creating educational content, etc. Sybil filtering is standard, and tokens are often immediately sold post-TGE.

Points programs value fees generated over locked capital; testnet rewards value sustained, qualitative participation over sheer transaction count.

Real Yield

Users can now clearly differentiate between "yield generated from real revenue" and "yield printed through inflation," showing a distinct preference for the former.

Real yield manifests in many forms, but only a few are meaningful: fees from economic activities like trading, lending, funding rates, liquidations; infrastructure usage fees; and RWA-backed yields.

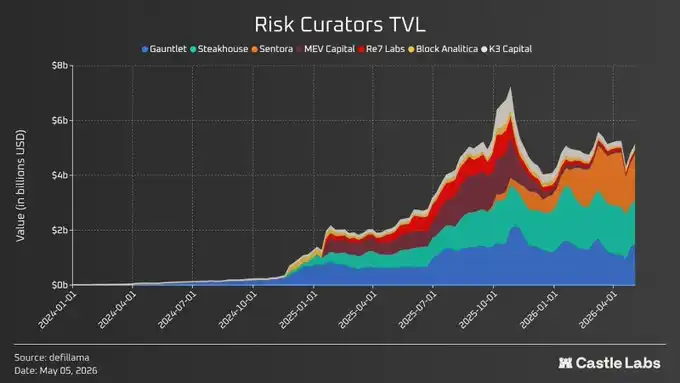

Yield trading platforms like @pendle_fi, and vaults operated by risk managers like @veda_labs, @gauntlet_xyz, @MEVCapital, @SteakhouseFi, as well as on-chain capital allocators like @sparkdotfi, have become primary gateways for capital deployment, funneling more liquidity into fixed-income strategies based on real yield sources.

For example, @ethena's sUSDe generates yield through delta-neutral basis trading, with supply nearing $5.8 billion.

@SkyEcosystem's sUSDS pays about 4-4.5% yield, backed by RWA collateral and stability fees – S&P even assigned its first-ever credit rating to a DeFi protocol, Sky.

The overall trend is moving from a market that "manufactures yield via inflation" to one that "imports and distributes yield from real sources."

Value-Capturing Tokenomics

Beyond yield, users increasingly favor tokens whose value is directly tied to product adoption – often via buybacks, buyback-and-burn, supply deflation, or protocol revenue sharing.

Hyperliquid's HYPE is a classic case: its Assistance Fund uses approximately 99% of trading fee revenue for open market buybacks, with cumulative buybacks exceeding $1.16 billion. Since TGE, 4.45% of the total supply has been bought back and burned.

Venice's VVV ties demand to staking AI inference compute, with part of the protocol revenue used to buy back and burn VVV. About 40% of the supply has been burned so far, with prices up 400% year-to-date.

Bittensor's TAO employs a Bitcoin-style halving mechanism, shifting from inflation to scarcity.

The pattern users look for is the same: the token must be tightly coupled with activity actually generated by the product, where increased activity adds value, not dilutes it.

New Types of Trading Venues

Finally, attention is diffusing to new types of trading venues:

- Prediction markets (Polymarket and Kalshi saw massive cumulative trading volume in 2025)

- Physical card and collectible trading markets

- Crypto-supported gamification (Crypto iGaming)

These are more speculative but bring real trading volume and revenue.

Logan Paul has publicly stated his portfolio contains no stocks, only Pokémon cards. The Pokémon card market size reached $75 billion in 2026 (less than $15 billion in 2016).

@Collector_Crypt (a card trading market on Solana) has surged to become the second-highest revenue dApp on Solana, with $1.9 million in daily revenue.

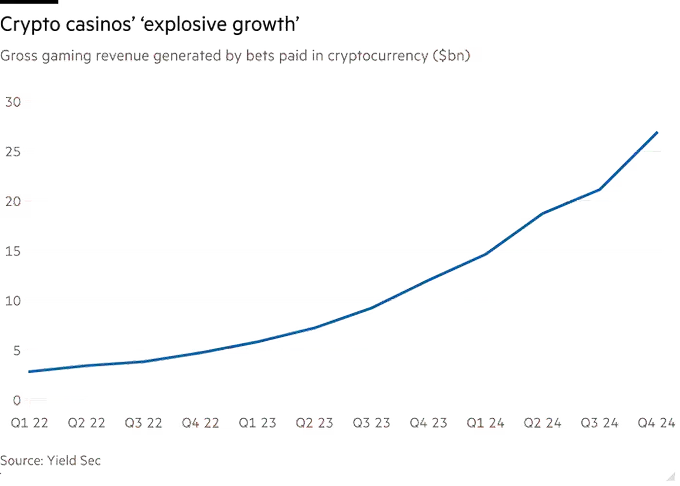

GameFi is outdated, but GambleFi is quietly booming. Crypto gambling revenue reached $81.4 billion in 2024, a 5x increase from 2022. Q1 2025 crypto betting volume alone was $26 billion, almost double year-over-year. Non-KYC, global reach, and provably fair mechanisms are driving a new wave of on-chain gamification.

Centralized crypto iGaming platforms like @Stake, @shufflecom, and provably fair on-chain iGaming platforms like @nardotbet, though rarely mentioned by DeFi KOLs, have very strong real transaction volumes.

The commonality in these fields: users can independently verify their appeal. Interest stems from the mechanisms themselves, not marketing language.

What Makes DeFi Users Stay?

DeFi users continue using a protocol when it is genuinely useful in real life, generates profit, and creates value for token holders. It must also remain reliable through market ups and downs.

The core difference lies in: protocols that retain capital do so through trust, distribution, and reliability, not temporary APY or TVL.

Real-World Use Cases

The strongest reason for users to stay is simple: the protocol is genuinely useful in daily life. Products like crypto cards, neobanks, vaults give users a reason to stay in the ecosystem beyond speculation.

Ether.fi Cash is a good example: users earn cashback while spending, while also earning staking yield. The specific rates matter less than the fact that "daily financial activity itself becomes a reason to stay in the ecosystem."

The same logic applies to crypto neobanks and capital allocators: they are embedded in users' regular financial habits, not just occasional destinations for yield farming.

Tokenomics Reflecting the Real Product

When a token truly captures the value generated by the product, users are more willing to stay, rather than relying on narratives.

The textbook case for 2026 is HYPE. Its Assistance Fund uses 99% of trading fee revenue for open market buybacks. The Bitwise CIO stated plainly: the token's design means platform activity growth directly benefits holders. This is a value loop users can personally verify, thus it sustains attention, not just short-term market attention at launch.

@AskVenice's VVV represents another specific model: staking VVV grants proportional daily AI inference compute on the platform, which can be locked to mint DIEM (representing $1 of API credit per day). Venice has burned over 42% of the initial supply and drastically cut inflation. Demand is entirely driven by real usage.

Airdrops and Incentives, But Not Just Talk

Airdrops can still bring users back, but the easy era is largely over. Projects increasingly reward real usage and strictly filter Sybils.

@monad skipped traditional points programs altogether, instead rewarding real contributors. Its testnet airdrop was based on 5 contributor tracks with strong anti-Sybil measures; ultimately, only 5,500 wallets were rewarded for community building, support, content creation, and ecosystem growth.

Points programs are still difficult to execute well. A recent example is MegaETH's Terminal program: launched with TGE in April 2026 as an 8-week reward campaign, it was terminated early just 3 weeks later (May 21).

Even well-designed programs struggle to convert short-term campaigns into long-term retained users.

How Can DeFi Projects Retain Users?

DeFi retention relies on four elements working together:

- A product experience good enough for daily use

- Responsive customer support

- Tokenomics aligned with community interests long-term

- Community building beyond TG and Discord (product experience, support, tokenomics, strategic community building)

Types of KOLs DeFi Projects Should Collaborate With

DeFi KOLs roughly fall into four categories: Educators, Content Creators, Airdrop Practitioners, and Vertical Experts.

Each is suitable for different stages of the user journey. Treating them as interchangeable "exposure tools" is a common and costly mistake.

What DeFi KOL Content Performs Best?

Top-performing DeFi content is usually specific and verifiable: on-chain credentials, step-by-step strategy breakdowns, balanced protocol analysis, and timely interpretations of vulnerabilities or new mechanisms.

Underperforming content is typically generic, undisclosed, or unverifiable.

Common Mistakes in DeFi KOL Marketing

- Using creators who don't understand the product

- Generic content (vague terms like "revolutionary," "game-changing")

- Audience mismatch

- Over-reliance on a few top KOLs (concentration risk)

- False exposure metrics

- One-off promotions instead of building long-term relationships

- Ignoring product readiness

Summary

The most effective DeFi marketing plans are those that truly mirror actual user behavior: discovery comes from trusted voices, interest comes from verifiable mechanisms, retention comes from strong tokenomics and product design, not just marketing speak.

Top-performing protocols don't rely solely on internal marketing. KOLs bring awareness, research validates the thesis, users share real results, and ultimately, persistent on-chain data proves the product's value far exceeds incentives.