Background: Escalating geopolitical risks, the crypto market has become a high-beta risk asset deeply embedded in the global macro cycle.

Quantitative Framework: The GPR index can be decomposed into "Threats" and "Acts," with negative effects primarily driven by "Threats".

Transmission Mechanisms: Risk Appetite Shift | Inflation and Rate Cut Concerns | Market Structure Amplification

Causes of High Beta: Strengthened Correlation with Risk Assets + High-Leverage Liquidation Cascades + Endogenous Liquidity Contraction

Outlook: Baseline Scenario - Volatile Recovery | Pessimistic Scenario - Double-Dip | Optimistic Scenario - High-Volatility Outperformance Rebound

Implication: Investors need to incorporate geopolitical risk into a unified macro framework, dynamically assessing its impact on risk premiums and liquidity.

I. Overview of Geopolitical Risk

- What does Geopolitical Risk mean?

Geopolitical risk is often perceived as the "impact of a sudden news event." However, a more accurate understanding is: it is a collection of events and expectations—escalation of war or conflict, terrorist attacks, sanctions and counter-sanctions, diplomatic confrontations, obstruction of key shipping lanes, escalation of trade frictions and tariffs, etc.—that collectively increase future uncertainty.

The key to geopolitical risk lies not in the event itself, but in the market's repricing of the probability of future paths. In other words, GPR is a "macro-level risk premium generator." It may not erupt every day, but as long as it rises, the market responds with higher discounts, stricter risk appetites, and tighter funding constraints.

- How to quantify Geopolitical Risk?

The Geopolitical Risk Index (GPR Index), compiled by US Federal Reserve economists Dario Caldara and Matteo Iacoviello, statistics the proportion of discussions on negative geopolitical events or threats in international newspapers and magazines since 1900, sourced from 10 major international newspapers.

The Geopolitical Risk Index is an indicator that measures changes in global geopolitical risk, typically used to assess the potential impact of political instability, conflict, war, policy changes, and other factors on the economy and markets of countries or regions. More importantly, this system breaks down risk into two more "tradable" components:

- Threats: The stage where risk is brewing but has not yet materialized—discourse such as threats, warnings, concerns, risks, tensions appears intensively. When threats rise, the market often first trades "probability" (expectations), manifested as rising panic indicators, strengthening gold/USD, and the emergence of oil price risk premiums;

- Acts: Risk has already occurred or escalated—the proportion of "factual" reports such as the start of war, escalation of conflict, execution of terrorist attacks increases. At this point, the market begins to trade "real shocks" (supply/demand/policy/growth), volatility is often more intense, and it is more likely to trigger cross-asset chain reactions.

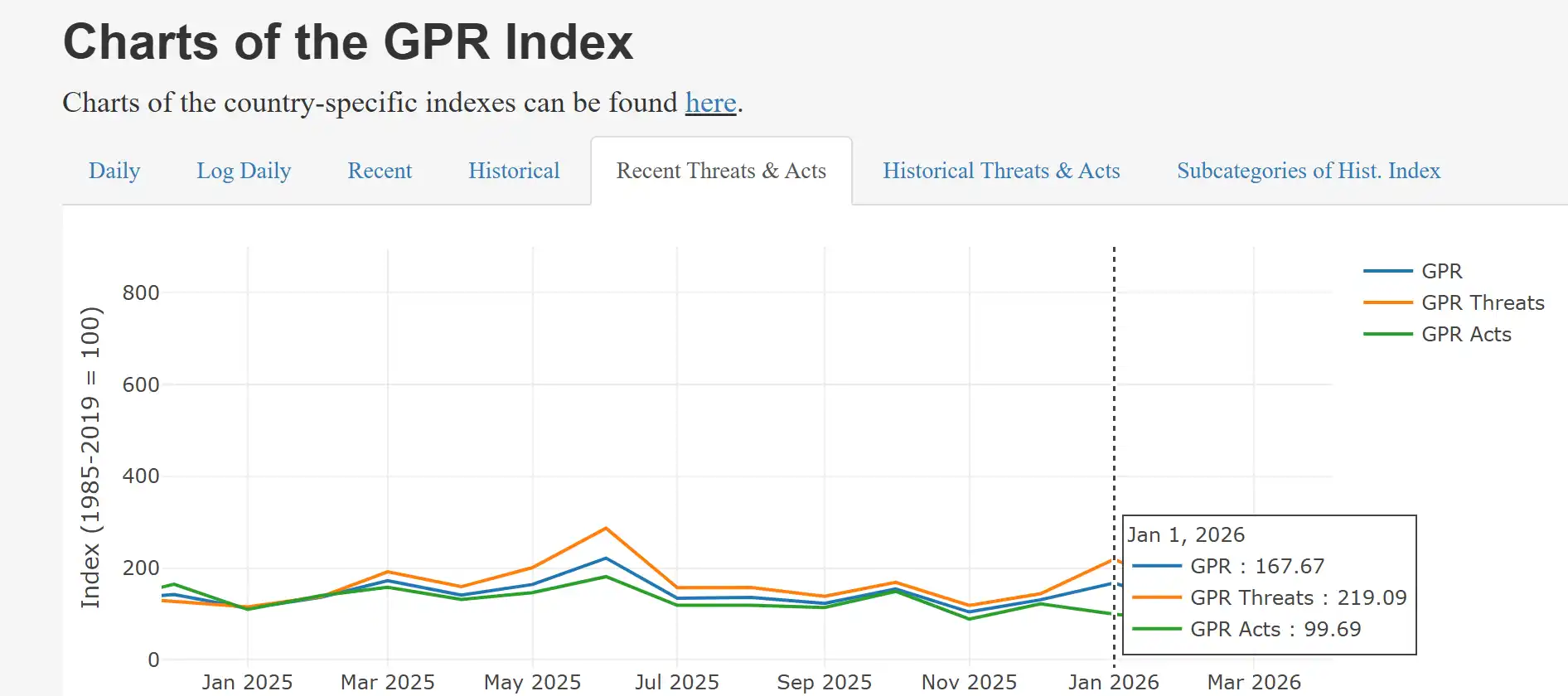

According to MacroMicro platform data, the global geopolitical risk "Threats" index rose significantly in January 2026, reading 219.09. When GPR rises, the market's first reaction is often to reduce risk exposure first, before discussing whether to buy the dip. This manifests as: increased volatility (VIX rise), risk asset pullbacks, and increased preference for safe-haven assets and cash-like assets.

Source: https://www.matteoiacoviello.com/gpr.htm

II. Impact and Transmission of Geopolitical Risk

The rise in geopolitical risk (GPR) does not directly cause crypto market volatility; it first increases macro uncertainty, which is then transmitted through multiple channels, ultimately forming intense co-movement in the crypto market. This is the inevitable result of macro stress being transmitted and amplified by market structure.

Rising GPR primarily works through the following four mechanisms: (1) Risk Appetite Shift: VIX rise, widening credit spreads, overall reduction in risk asset positions; (2) Energy and Commodity Shock: Rising gold, oil prices, rising inflation expectations; (3) Policy and Liquidity Repricing: Delayed rate cut expectations, stronger USD, rebound in long-term rates; (4) Market Structure Amplification: Thin weekend liquidity, high-leverage derivatives, forced liquidation cascades.

These mechanisms work together, causing the crypto market to exhibit "more violent" co-movement than the stock market.

- Risk Appetite Shift

Escalating geopolitical conflicts first trigger risk aversion. Safe-haven sentiment heats up in the stock market, the volatility indicator VIX rises, funds flow out of high-volatility assets, and转向 traditional safe-haven assets.

VIX (CBOE Volatility Index) is a core indicator measuring the expected volatility of US stocks over the next 30 days, calculated from S&P 500 index option prices, reflecting implied rather than historical realized volatility. Because it spikes sharply during market declines, it is called the "fear index." Its numerical range can intuitively reflect market sentiment: below 20 is stable and optimistic; 20-30 is cautious; above 30 is high panic; above 40 is extreme panic (common in major crises).

In March 2026, VIX has rapidly risen from about 14.50 at the beginning of the year to above 20, reflecting market panic over military conflict and energy supply chain disruptions. Gold, as a classic safe-haven asset, typically shows strong buying interest in the early stages of a geopolitical crisis. World Gold Council research shows that for every 100-point increase in the GPR index, the gold price rises by an average of about 2.5%. Spot gold is highly positively correlated with the GPR index, especially when sovereign credit risk or the situation deteriorates, its safe-haven value even surpasses traditional currencies.

- Inflation and Rate Cut Concerns

Escalating conflicts in regions like the Middle East often first impact oil prices and shipping expectations, pushing up inflation concerns, thereby forcing the market to lower rate cut expectations, creating sustained pressure on high-valuation, high-volatility assets.

The core driver of oil price volatility is supply disruption risk, not just sentiment. The safety of key channels like the Strait of Hormuz directly determines the level of "geopolitical premium." If the conflict becomes protracted, it will bring lasting inflationary pressures. If gold mainly reflects the safe-haven demand from financial system uncertainty, oil prices directly map the impact of conflict on real economy supply and inflation. As long as the market begins to worry about supply chains, sanctions and counter-sanctions, oil prices will be repriced.

Brent crude oil has risen sharply recently, with a monthly gain of over 20%. When geopolitical risk rises, energy price shocks and rising volatility often appear simultaneously, driving risk appetite shifts and liquidity repricing. Rising oil prices strengthen concerns about inflation stickiness, directly undermining the certainty of rate cuts. When market expectations shift from "easing is on the way" to "higher for longer" interest rates, crypto assets, as high-volatility, high-expectation varieties, often come under pressure first, especially during periods of thin liquidity.

Since the beginning of 2026, crude oil and VIX have shown a high positive correlation. Currently, both are rising simultaneously, meaning that soaring energy prices are directly driving market panic sentiment. Meanwhile, the price of BTC, seen as "digital gold," shows a clear negative correlation with VIX—the more panicked the market, the greater the selling pressure on Bitcoin. The reason behind this is that the pressure from rising oil prices has strengthened expectations of high interest rates, which is a double blow to high-risk assets (Bitcoin) and the stock market (as reflected by VIX performance).

- Characteristics of Crypto Market Structure

After macro pressure is transmitted to the crypto market through the first three routes, the crypto market's own structural issues will further amplify the impact. The structural characteristics of the crypto market determine that its volatility in risk events is often more intense than that of traditional risk assets:

- 24/7 All-Day Trading: Makes weekends the period most prone to amplification of macro shocks: traditional markets are closed, hedging tools are reduced, market depth becomes shallow;

- High Proportion of Derivatives and High Leverage: Price declines easily trigger margin calls and forced liquidations, forming "passive selling" cascades;

- Clear Liquidity Stratification: Uneven liquidity stratification is reflected in aspects such as large exchanges vs. small exchanges, spot vs. perpetual, mainstream coins vs. altcoins. When risk appetite contracts, liquidity quickly concentrates towards the top, and the decline of tail assets is more extreme.

It is these mechanisms that drive and determine the "high beta" attribute of the crypto market, driven by mechanisms rather than单纯 emotion.

It is worth noting that when conflicts are叠加 sanctions, capital controls, or restrictions on the banking system, cryptocurrencies may become a partial safe-haven tool due to their cross-border transfer and alternative settlement properties, providing buying support. In the early stages of the Russia-Ukraine war, there was active fiat trading and a significant increase in related demand. Although this path can provide short-term support, it usually cannot reverse the downward trend dominated by macro risk appetite, unless accompanied by stronger narratives such as long-term inflation or sovereign debt crises.

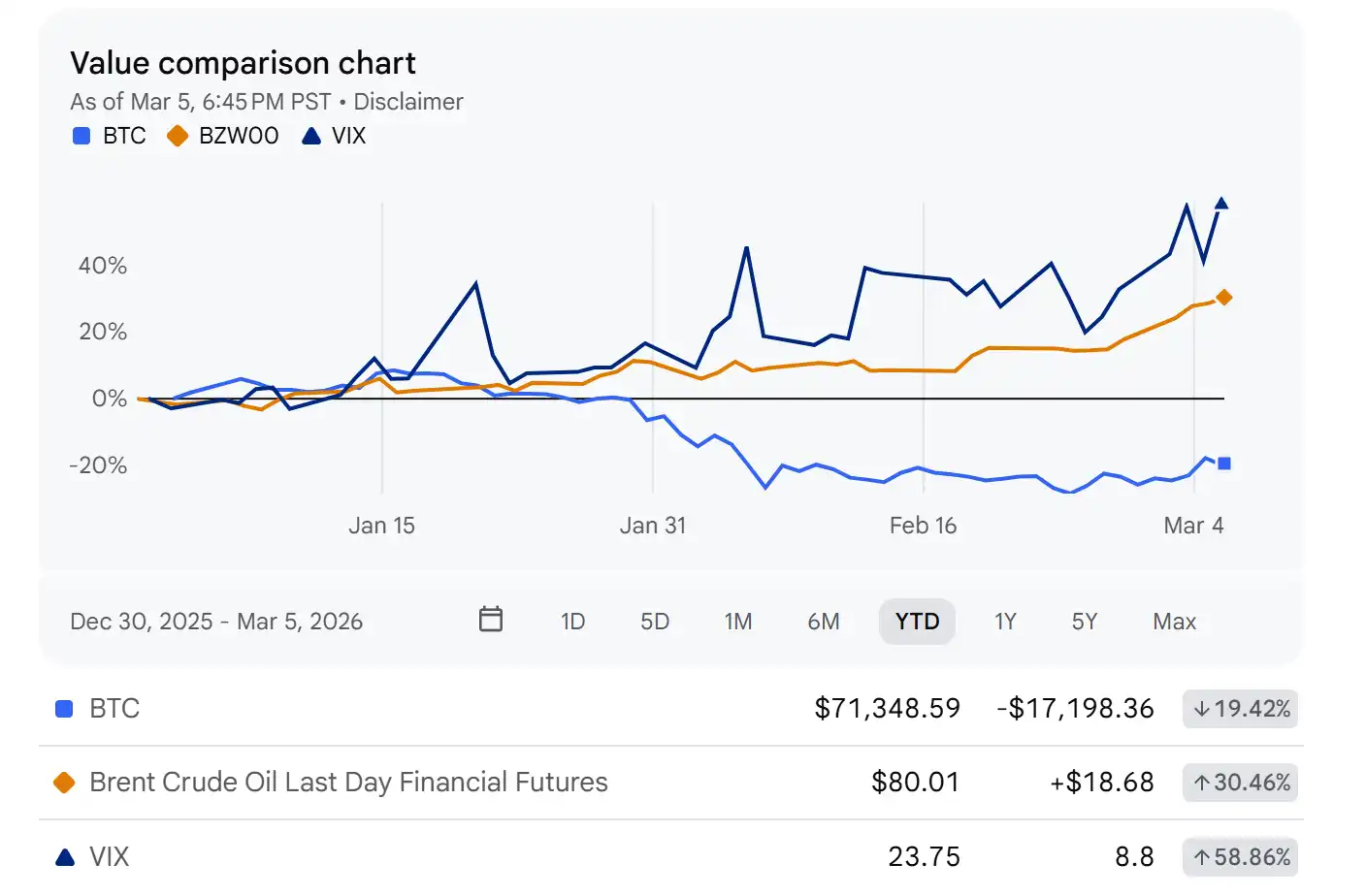

The chart below, drawn from Yahoo Finance, shows the 6-month trend. The blue filled area represents the CBOE Volatility Index (VIX), overlaid with the performance of Brent crude oil futures, gold, and Bitcoin for the same period. Entering 2026, as geopolitical risks continue to escalate, the VIX index has risen significantly,最新收于23.75 on March 6, 2026; Brent crude oil has rebounded strongly同步; Gold has risen significantly as a safe-haven asset;而 Bitcoin has experienced a sharp correction. This chart visually confirms that geopolitical risk is transmitted through the dual paths of "VIX surge + energy price surge." On one hand, it pushes up market volatility and inflation expectations; on the other hand, it causes high-beta risk assets like cryptocurrency to come under significant pressure.

Source: https://finance.yahoo.com/

III. Reasons for Crypto Assets' High Beta

Many people simplify BTC as "digital gold," but in most macro phases, it behaves more like a "high-volatility version of the Nasdaq." The reasons mainly come from three layers of structure: correlation-wise, it is incorporated into risk asset pricing; price discovery occurs more in derivatives; and the "endogenous liquidity cycle" composed of stablecoins and exchange margins.

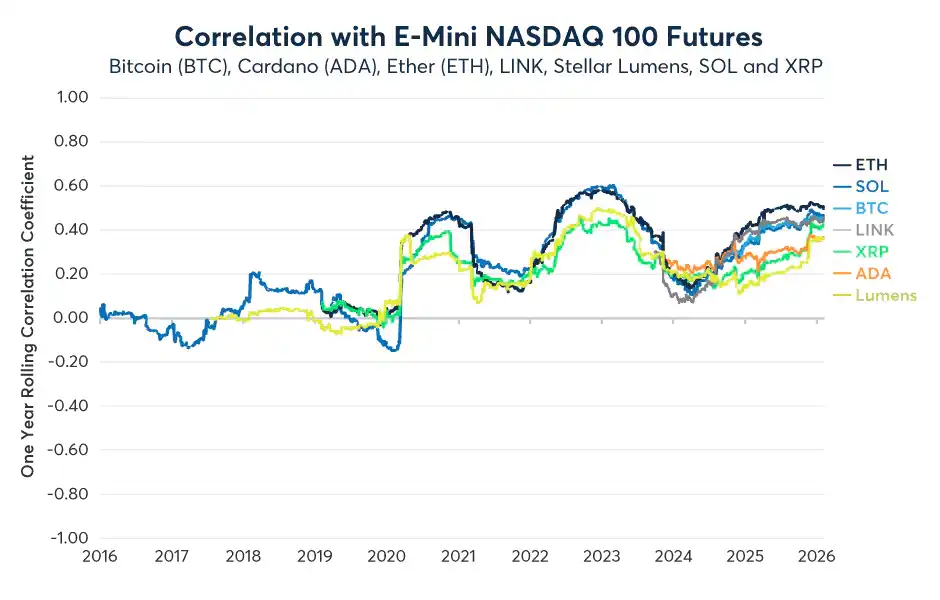

- Correlation with Risk Assets

Research from CME Group points out that since 2020, the correlation between crypto assets and the Nasdaq 100 has been positive for a long time, and in some phases of early 2025 and 2026, the rolling correlation can reach approximately +0.35 to +0.6 (clearly阶段性, not constant).

Source: https://www.cmegroup.com/insights/economic-research/

This means that once a macro shock triggers "risk assets reducing positions together" (war escalation, rising oil prices, delayed rate cut expectations), it is difficult for BTC to remain unharmed, and it even often falls faster. This is the first layer of "high beta".

- High Leverage Amplifies Volatility

The violent fluctuations in the crypto market are often not due to fundamentals changing drastically within 24 hours, but rather the funding rate—margin—liquidation chain accelerating "deleveraging".

In the "1011" crash event of 2025, over $19 billion in leveraged positions were liquidated within 24 hours, setting a record for the largest single-day liquidation in crypto history. At the same time, the open interest in perpetual contracts contracted significantly, indicating that "liquidation cascades" can push already fragile行情 into non-linear volatility.

- Endogenous Liquidity Mechanism

When macro tightening expectations heat up, stablecoin funds become more cautious, lending and margin conditions tighten simultaneously, and the market experiences "self-siphoning": available margin decreases → passive position reduction → price falls → collateral shrinks → further passive position reduction.

It can be seen that the crypto market, unlike traditional markets that mainly rely on central banks "turning on/off the tap," is more like a system that automatically contracts liquidity under pressure, thus更容易出现 sharp declines and sharp rebounds.

So is "digital gold" still valid? The historical peak of the rolling correlation between BTC and gold is limited, and it has fallen back to near 0 since 2024. Therefore, a more accurate framework is: under short-term shocks, BTC behaves more like a high-beta risk asset; in the medium to long term, only in structural scenarios such as capital controls, cross-border frictions, and sovereign credit concerns is BTC more likely to体现 the narrative advantage of being "cross-border transferable and non-dilutable".

IV. Subsequent Trend Outlook

The impact of geopolitics on crypto is essentially not about "whether war will benefit Bitcoin," but about how risk appetite and liquidity conditions change. While Middle East risks remain uncertain, we use a three-scenario framework to展望 possible paths—key triggers—corresponding trends.

- Baseline Scenario: Volatile Recovery

Assuming the conflict remains within a controllable range, key shipping and energy supplies do not experience long-term disruptions, oil prices fluctuate at high levels but do not surge失控ly; market concerns about secondary inflation ease, VIX gradually falls back, and rate cut expectations undergo "slow repair" after data confirmation.

In this environment, crypto, as a high-beta asset, often does not immediately走出 a one-sided trend but is more likely to走 a "range-bound oscillation + slow upward" recovery行情: supported below by falling risk premiums and bargain-hunting配置, capped above by still cautious macro conditions and the time needed for leverage recovery.

- Pessimistic Scenario: Double-Dip

If the conflict spills over to a wider range, substantial supply obstructions occur or shipping costs rise长期ly, oil prices continue to surge bringing inflation back, the market is forced to further delay rate cuts,甚至重新计价 higher real利率 paths, and risk assets overall face valuation downgrades.

At this time, crypto's triple amplifiers would叠加: falling together with risk assets + derivative deleveraging + endogenous liquidity contraction (margin/lending tightens simultaneously), more prone to a structure of "accelerated decline—weak rebound—re-breaking support," known as a double-dip.

- Optimistic Scenario: High-Volatility Outperformance Rebound

If the risk event cools down rapidly, oil prices fall back, VIX declines, and simultaneously the macro releases clearer easing signals, the market reaffirms the rate cut path, and risk appetite quickly repairs.

Crypto often exhibits弹性更强的超额反弹 in such phases: capital回流叠加 short covering, leverage重新打开, prices may走出 "sharp rise"行情. But be wary: crypto's structural characteristics determine that it often "rises fast and also pulls back fast,"容易 experiencing剧烈回吐 when sentiment overheats.

V. Implications and Summary

Crypto assets have been彻底 integrated into the global macro financial cycle, no longer an "independent narrative asset"游离于 mainstream之外, but a high-beta risk asset jointly influenced by oil prices, inflation expectations, interest rate paths, and volatility.

Three Implications

Implication 1: The real杀伤力 of geopolitical risk lies in the提前定价 of risk premiums by "Threats"

After the GPR index decomposes risk into "Threats" and "Acts," the effects are primarily driven by the former. This means the market often completes repricing through VIX surges, oil price premiums, and delayed rate cut expectations even before the conflict escalates,表现为 "expectation as reality".

Implication 2: The high-beta characteristic of the crypto market is the inevitable result of the dual effects of macro transmission and market structure

Risk appetite shifts, inflation and rate cut concerns, policy liquidity repricing, plus the四大 mechanisms of 24/7 trading, high-leverage liquidations, and endogenous liquidity contraction reinforce each other, causing crypto assets to fluctuate significantly more strongly than traditional markets under similar macro shocks. This is not driven by emotion but by mechanism.

Implication 3: The macroization of Bitcoin has become an irreversible structural trend

Bitcoin and US stocks have transformed into a long-term偏正 correlation, indicating that Bitcoin is increasingly being traded according to risk appetite assets. In the short term, it behaves more like a "high-volatility version of the Nasdaq"; in the medium to long term, only in scenarios of capital controls, sovereign credit crises, or intensified cross-border frictions will the属性 of "digital gold" truly manifest.

Conclusion

In the current environment of high interest rates + geopolitical conflict, Bitcoin's "digital gold"属性 is temporarily dominated by its high-beta risk属性. Investors who understand the transmission mechanisms of geopolitical risk will shift from passively承受波动 to actively seizing opportunities. Only by transforming geopolitical uncertainty into quantifiable risk premiums and liquidity signals, dynamically assessing its impact on asset allocation, can rational decisions be made in complex situations. The long-term value of the crypto market never lies in avoiding macro cycles, but in deeply understanding and utilizing them.

About Us

Hotcoin Research, as the core research institution of Hotcoin Exchange, is committed to transforming professional analysis into your practical weapon. We analyze market dynamics through "Weekly Insights" and "In-Depth Research Reports"; with the exclusive column "Hotcoin严选" (AI + expert双重筛选), we help you lock in potential assets and reduce trial-and-error costs. Every week, our researchers also interact with you face-to-face through live broadcasts, interpreting hot topics and predicting trends. We believe that warm companionship and professional guidance can help more investors navigate cycles and grasp the value opportunities of Web3.