Author: Max.s

Original Title: War, Weekends, and Locked Liquidity: How RWA is Reshaping Global Trading Time from the Iran Airstrike Incident

On February 28, 2026 (Saturday), air raid sirens in the Middle East pierced the tranquility of global geopolitics. The United States and Israel launched a meticulously planned large-scale airstrike on targets within Iran.

The timing of this military operation, like an extremely precise surgical strike, was reflected not only in the physical coordinates of the tactical attack but also in the grasp of the "time coordinates" of the global financial markets. Choosing to launch the surprise attack during the weekend, when traditional Western financial markets are closed, was deeply significant: it maximally prevented the immediate spread of panic in the stock and foreign exchange markets, while also giving governments and central banks a full 48-hour buffer period to intervene and guide market expectations.

However, in this deliberately created "trading vacuum," global capital did not sit idly by. When the CME (Chicago Mercantile Exchange) gold and crude oil futures boards froze at Friday's closing prices, and the buy/sell buttons for various ETFs were grayed out by the system, real undercurrents were surging in another never-sleeping network. Cryptocurrency gold tokens represented by XAUT (Tether Gold) and PAXG (PAX Gold) experienced a trading peak on blockchain networks like Ethereum.

This is not just a game of geopolitical chess; it is a stress test about "liquidity privilege." The airstrike incident, in an extremely extreme way, declared to all traditional financial practitioners: traditional financial infrastructure based on T+1 or T+2 settlement, limited to working days and fixed trading hours, is being left behind by the times. The tokenization of real-world assets (RWA) and the completion of 24/7 trading settlement through digital assets are no longer social experiments by geeks but an inevitable trend in the global capital's fight for pricing power and trading Alpha.

From the perspective of quantitative trading and hedge funds, the core of risk management lies in the accessibility of hedging tools. After the airstrike on February 28, the risk exposure of macro hedge funds skyrocketed instantly. In theory, crude oil and gold are the preferred safe-haven hedging targets. But on that Saturday morning, tens of thousands of financial institutions and professional traders became "liquidity prisoners."

The infrastructure of traditional financial markets is built on the industrial era's schedule. Although electronic trading has been popularized for decades, the underlying clearing and settlement systems (such as DTCC, Euroclear systems, and the SWIFT network) still heavily rely on the batch processing of centralized institutions and banking hours. When a black swan event occurs outside trading hours, the reaction mechanism of traditional markets is completely frozen. Investors can only watch information spread at the speed of light while capital flows are trapped like insects in amber, unable to move.

This "deliberate avoidance of trading days" strike essentially compresses all market volatility and gap risk into the few short minutes of Monday's opening. For quantitative market makers and high-frequency trading institutions, this kind of discontinuous hedging gap risk is fatal. During the highly information-asymmetric and liquidity-dry Monday opening phase, it is extremely easy to trigger a chain reaction of long squeezes or short blow-ups.

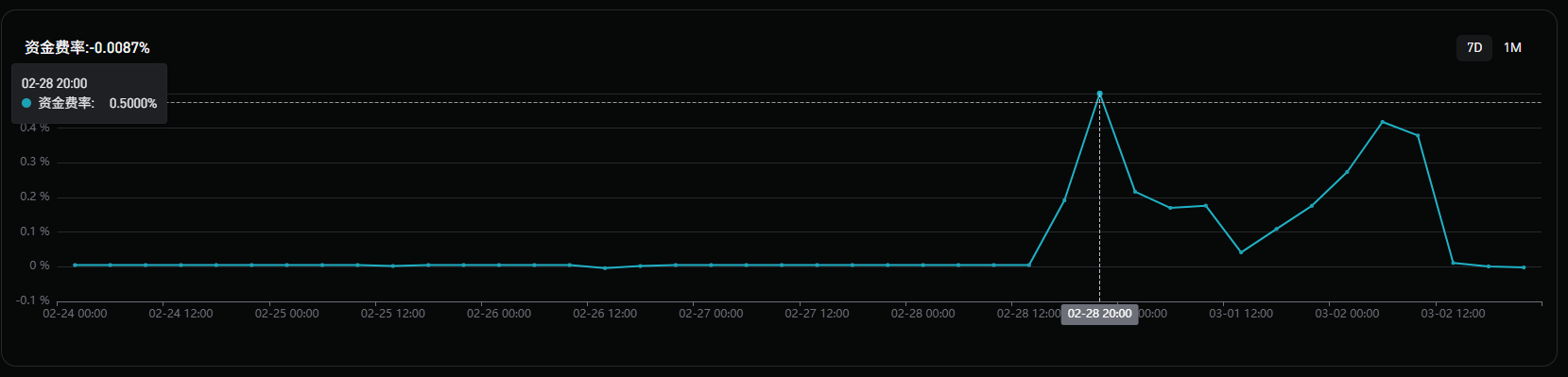

In contrast, the cryptocurrency market demonstrated a dimension-reducing resilience. Within minutes of the news of the February 28 attack spreading, capital rapidly flowed into crypto liquidity pools. XAUT and PAXG trading pairs on major centralized crypto exchanges absorbed a massive level of safe-haven demand. As shown in the chart, the funding rate (longs pay shorts) reached 0.5% on February 28.

We can clearly see this smooth and steep value growth curve from the on-chain data: no market close, no trading halts, no opening gap uncertainty. The price of on-chain gold tokens followed every update from the front-line battle reports, performing continuous pricing in milliseconds. Before the CME opened on Monday, the price of on-chain XAUT had already completed sufficient price discovery.

This brings about a highly disruptive financial phenomenon: the pricing power of traditional commodities, for the first time in history during a major geopolitical crisis, temporarily shifted to the digital asset market.

When the Asian early trading session opened on March 2 (Monday), traditional gold spot and futures markets surged at the open. Over that weekend, XAUT was no longer a shadow asset of GLD (SPDR Gold ETF) or COMEX gold futures. Instead, on-chain tokens, in a sense, became the "price oracle" for Wall Street's Monday opening. Sharp arbitrageurs used this 48-hour time difference to build sufficient positions on-chain and, at the moment the traditional market opened on Monday, arbitraged the high basis to narrow the price gap between the two worlds.

The weekend's gold token trading frenzy revealed the most core value proposition of RWA assets: the expansion of the time dimension of liquidity.

In previous narratives, people often focused the advantages of RWA on lowering thresholds, fractionalizing ownership, or improving transparency. But for professional financial practitioners, the greatest appeal of RWA lies in the T+0 underlying logic of "settlement equals clearing" and the 7x24x365 non-stop operation mechanism.

Imagine if what broke out on the weekend was not a Middle East airstrike, but a sovereign debt default of a certain country, the collapse of a major bank, or an unexpected emergency central bank interest rate cut. Traditional institutions could only passively bear huge exposure risks before the Monday open. However, if government bonds, foreign exchange, and even core stock indices achieved deep tokenization and established sufficient liquidity pools on the blockchain, institutional investors could immediately use smart contracts to complete risk hedging and asset swaps the moment the risk occurs.

In this event, not only gold but also the exchange network between stablecoins and crypto-native assets acted as a super highway for capital safe havens. In the traditional financial system, cross-border, cross-institution fund transfers require complex correspondent bank confirmations and multiple compliance reviews, taking days to complete. On-chain, hundreds of millions of dollars in hedging positions can be atomically swapped within one block time (12 seconds for Ethereum), with no counterparty default risk.

For Wall Street, the weekend at the end of February 2026 was a profound research and education experience. Previously, many traditional institutions took a wait-and-see attitude towards the rise of RWA protocols like BlackRock's launch of BUIDL (tokenized treasury fund) and Ondo Finance, considering it just a gimmick to attract existing crypto funds. But the airstrike incident proved that in the face of extreme black swans, the liquidity premium provided by tokenized assets is a hardcore Alpha that no excellent quantitative model can replace.

Quantitative funds will no longer be satisfied with the trading interfaces provided by CME or Nasdaq; they will massively connect APIs to on-chain DEXs and RWA trading pools with institutional-grade compliance systems. To capture "non-synchronous trading opportunities" during weekends and holidays, building cross-border arbitrage models spanning TradFi and DeFi will become standard configuration for top hedge funds.

When brokers and market-making institutions realize that a large amount of trading demand and commission profits are leaking to blockchain networks on weekends, the drive for profit will force them to actively become liquidity providers for on-chain assets. In the future, large market makers like Jane Street and Jump Trading will not only make markets for ETFs on weekdays but will also inject liquidity into 24/7 RWA asset pools on weekends.

Starting with highly standardized commodities like gold and crude oil, gradually spreading to short-term treasury bonds, high-quality corporate bonds, and even US stock indices. The载体 of financial assets will completely migrate from the ledgers of trust companies and clearinghouses to distributed ledgers. No more T+2 capital occupation, no more weekend anxiety about selling for safety on Friday afternoon; global capital will truly achieve seamless circulation in physical time and space.

"Money never sleeps" was once one of Wall Street's most famous slogans, but the reality is that traditional Wall Street not only sleeps but also takes weekends and public holidays. The artillery fire on February 28, 2026, proved in a cruel way that in the face of an increasingly complex and unpredictable global macro environment, fragmented trading time and locked liquidity are themselves the greatest systemic risks.

The price discovery process led by digital assets like XAUT this weekend sounded the death knell for the traditional clearing system. RWA is not just about moving real-world assets onto the blockchain; it is about using code to reconstruct the time rules of financial operation. For quantitative analysts, traders, and financial engineers, the future battlefield is no longer limited to the trading screen for 5 days a week, 8 hours a day. Whoever masters the trading and settlement infrastructure of 24/7 digital assets first will be able to grasp the throat of the global market on the next unexpected black swan night.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush