By: ChandlerZ, Foresight News

On June 25, Bitcoin officially broke below the $60,000 level, hitting an intraday low of $58,030, marking its lowest point since October 2024. ETH fell in sync to $1,519, SOL traded at $65.99, with major assets across the board under pressure.

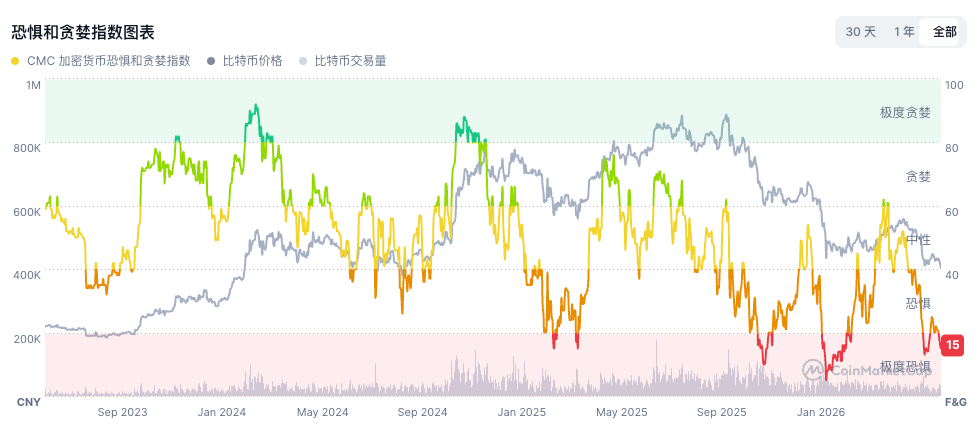

Data from Coinglass shows that over $1 billion in leveraged positions were liquidated in the past 24 hours, with long positions accounting for $788 million. The Fear & Greed Index dropped to 15, entering the Extreme Fear zone.

From its all-time high of $126,198 in October 2025, Bitcoin has now retreated more than 53%, with the bear market extending into its 8th month.

The bullish logic for Bitcoin over the past two years rested on two key pillars. First, the flywheel model represented by companies like Strategy continuously buying Bitcoin through securities financing. Second, the influx of large-scale institutional capital following the launch of US spot ETFs. These two channels together built the demand foundation for Bitcoin's last bull run. The current problem is that both pillars are simultaneously weakening.

Strategy's Financing Flywheel Continues to Lose Momentum

The most noteworthy variable in this decline is Strategy, the world's largest corporate holder of Bitcoin.

As of June 21, Strategy holds 847,363 bitcoins with an average cost basis of approximately $75,651, resulting in a paper loss exceeding $14.6 billion at current prices. Over the past few years, the company's core strategy has been to raise funds through issuing equity and preferred shares to continuously purchase Bitcoin. This cycle of "issuing securities, buying Bitcoin, pushing up the price, supporting the stock price, and issuing more securities" made it one of the most stable sources of institutional buying in the Bitcoin market and once propelled MSTR's stock price above $457 in 2024.

However, the key gears of this flywheel are slipping. In July 2025, Strategy completed a $2.5 billion IPO for a variable-rate preferred stock, STRC, designed to trade anchored to its $100 face value, with the company able to adjust the dividend rate monthly to maintain the peg. STRC was positioned as a financing product for the mass market, aiming to attract ordinary investors to participate indirectly in Bitcoin investment with lower volatility.

Since its debut, STRC has been consistently weak, falling to a historic low of about $75 on June 25, a 25% discount to its face value. According to its terms, if STRC falls below $95, it automatically triggers a 0.5% interest rate increase; its current annualized dividend yield has climbed to about 11.5%, increasing annual dividend expenses by approximately $53 million. The company's cash reserve is about $1.4 billion, sufficient to cover just over a year of dividend payments.

Andreja Cobeljic, Head of Derivatives Trading at Amina Bank, analyzed that while the direct cause of Bitcoin's current decline is a weakening market cycle, the deeper driver is the impact on the credibility of Strategy's strategy. If STRC continues to fail to return to its face value, Strategy's ability to raise funds through this channel to buy Bitcoin will be severely weakened, potentially cutting off what has been the most important incremental funding source for the Bitcoin market over the past two years.

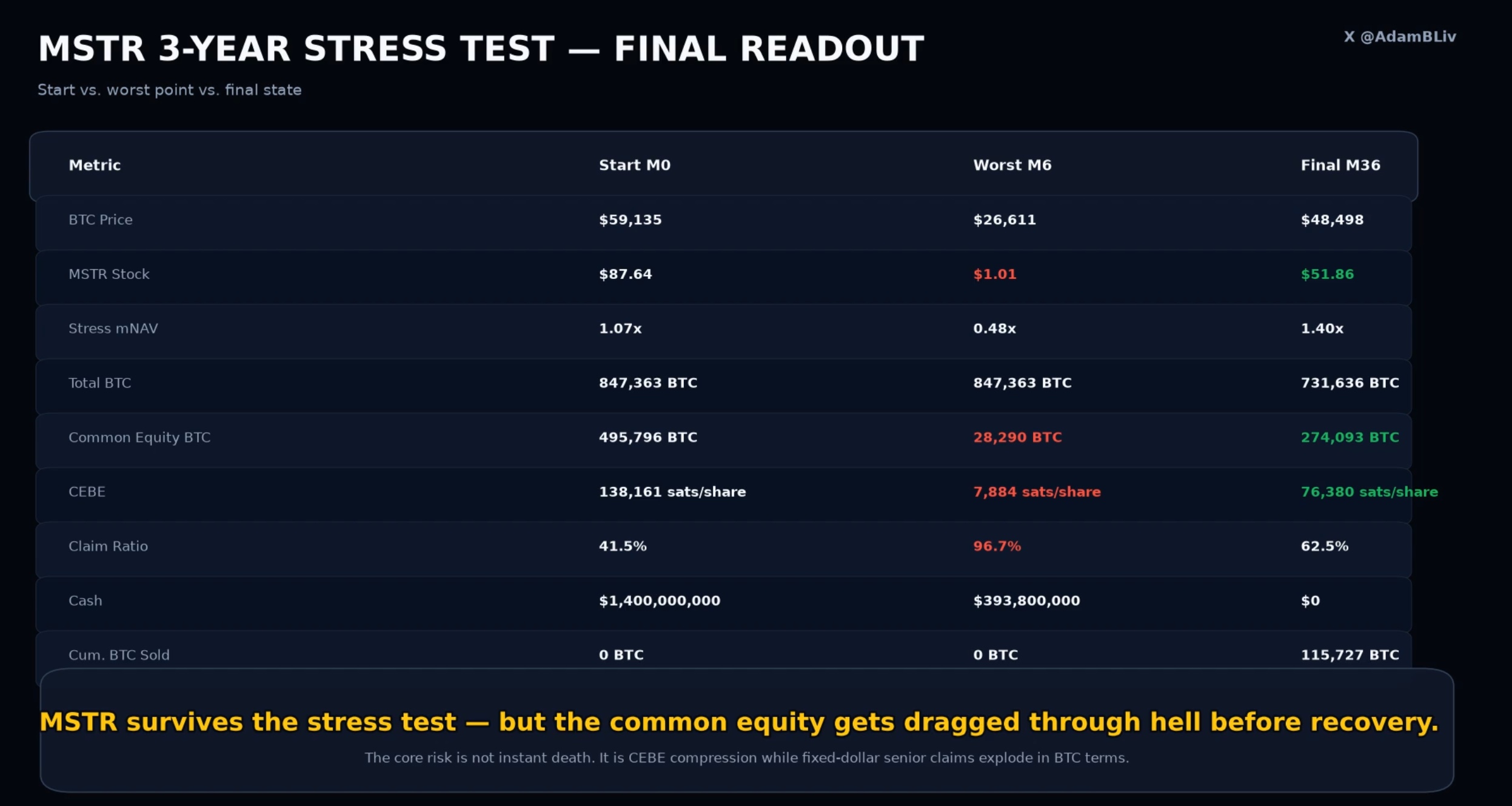

Analyst Adam Livingston conducted a three-year stress test on MSTR starting from current data, simulating an extreme scenario. The model assumes Bitcoin crashes 55% to $26,611 by month 6, while capital markets completely shut down, preventing Strategy from issuing new equity, new debt, or continuing to buy Bitcoin.

In this scenario, Strategy's priority debt structure quickly becomes perilous. Both preferred shares and bonds represent fixed-dollar claims; when the Bitcoin price collapses, their BTC-equivalent claims inflate dramatically. The model shows the BTC-equivalent claims of priority debt surging from 350,000 BTC to 819,000 BTC, accounting for 96.7% of total holdings and almost swallowing the entire Bitcoin inventory. The equity remaining for common shareholders collapses from 496,000 BTC to 28,000 BTC, with the MSTR stock price simulated to fall to $1.01. Meanwhile, monthly fixed expenses of $167.7 million (preferred dividends plus debt interest) continue to deplete cash. By month 9, cash runs out, forcing the company to start selling Bitcoin to service its debt obligations, cumulatively selling about 116,000 BTC over three years.

However, the model's conclusion is that Strategy survives. Assuming Bitcoin recovers to $48,498 in three years, the company would still hold 732,000 BTC, the MSTR stock price would return to $51.86, and the market-adjusted NAV (mNAV) ratio would recover to 1.40x. Livingston's assessment is that the real risk is not the "immediate bankruptcy" shouted by bears, but rather that priority debt, when measured in BTC, temporarily devours almost all common equity value during a price crash. Nevertheless, the model ultimately does not conclude with a "death spiral."

Institutional Retreat, Macro Tightening, Capital Shifts to AI

Strategy's issues are part of a larger picture of capital withdrawal.

US spot Bitcoin ETFs saw a single-day net outflow of $469 million on June 24, with BlackRock's IBIT accounting for $239 million, marking its fifth consecutive day of net outflows. Cumulative outflows for June total approximately $2.8 billion to $3.5 billion, constituting the most severe sustained capital flight since the products were approved in January 2024.

Bloomberg ETF analyst Eric Balchunas recently stated that Bitcoin's excessive reliance on the ETF and Strategy (MSTR) narratives should not be seen as the main value proposition for Bitcoin. He believes they should be the icing on the cake, not the whole cake. When Strategy's buying slows and the ETF channel simultaneously bleeds, Bitcoin's demand side loses its two most critical incremental sources.

Old money is leaving, and new money isn't coming in either, as the macro environment continues to tighten. The May PCE price index released on June 25 showed a year-over-year increase of 4.1%, the fastest pace in over three years. The Fed kept interest rates unchanged at 3.50%-3.75%, with expectations for a rate cut this year pushed further out. On the same day, US stocks initially rose but then fell. Apple announced global price hikes (up to $300) for multiple product lines due to memory chip shortages, causing its stock to plunge 5.1% and dragging the Nasdaq down from a 2.1% intraday gain to a loss of over 1%. Stubbornly high inflation implies persistently high funding costs, directly pressuring crypto assets that rely on liquidity expectations.

Deutsche Bank notes that a key difference in this downturn compared to previous cycles is the near absence of new retail buying, with institutional capital shifting en masse towards AI. On June 25, as Bitcoin fell below $60k and Apple tumbled, memory chip stocks rose across the board. Micron gained 8.6%, SanDisk rose 10.6%, and SK Hynix surged over 10% at one point on plans for a US listing. Capital made a directional choice between AI infrastructure and crypto assets.

Capital outflows, lack of new buy-side demand, and macro pressure all converged in the same week, culminating in a concentrated assault on the $60,000 support level.

~$10 Billion in Options Expire Today, Volatility May Persist

Beyond the aforementioned pressures, there is an immediate catalyst on June 26: Deribit will see approximately $10 billion in notional value of Bitcoin options expire, accounting for about 37% of current open interest. The put-to-call ratio is 0.83, indicating bullish bets still outnumber bearish ones. However, most call options are now out-of-the-money, while put options are concentrated in the $60,000-$65,000 and $70,000-$75,000 strike ranges, meaning bearish bets are more likely to be profitable.

Jean-David Pequignot, Chief Commercial Officer at Deribit, stated that this was an option structure positioned for mid-term higher prices and is now facing the test of declining spot prices.

Adam Haeems, Head of Asset Management at Tesseract Group, pointed out that quarter-end liquidity is typically thin, so prices might initially overshoot in either direction before mean-reverting after market makers hedge and close positions. However, a more significant test will arrive in the first week of July with quarterly contract settlements and leverage reductions.

![Assessing Sonic’s [S] 12% price drop and why more selling may be next](https://d1x7dwosqaosdj.cloudfront.net/images/2026-06/161e3d66eea4402796d2e6a66d93d453.jpg)