Author: Eddie Xin, Chief Analyst at OSL Group

"They were fcking us the whole time".

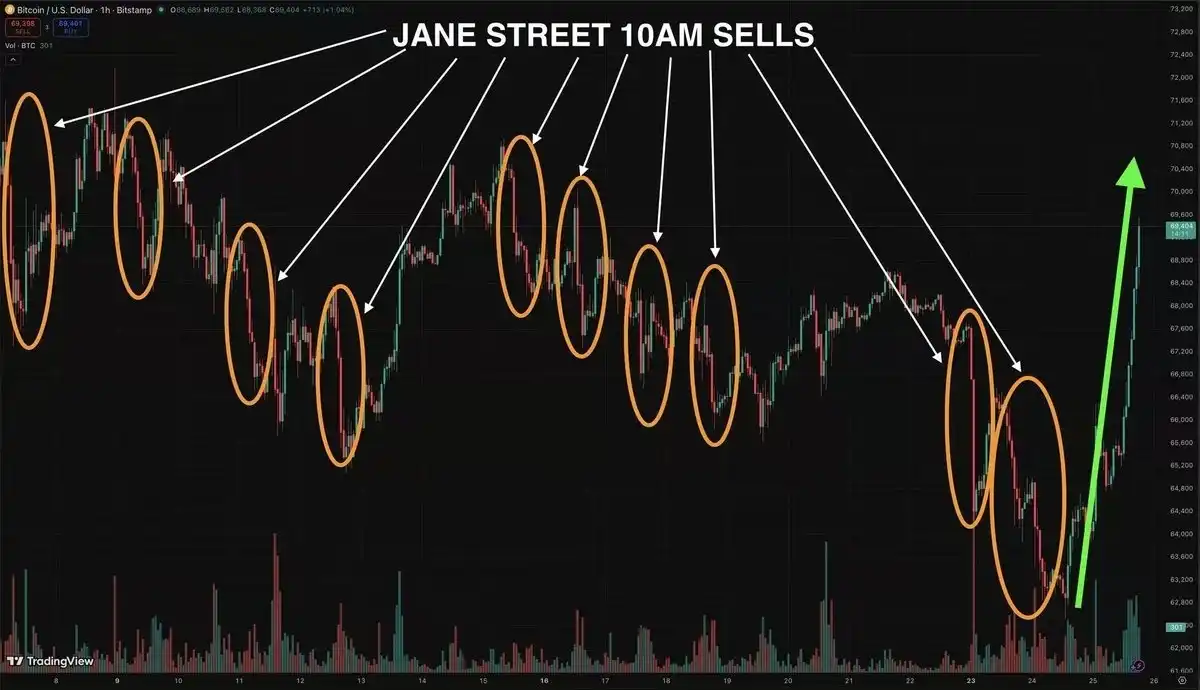

This expletive, circulating on Reddit and CT (Crypto Twitter) following the lawsuit, alongside an epic short squeeze with a liquidation scale exceeding $240 billion, directed the market's fury at the same target: Jane Street Capital.

At 10 AM, the liquidity low point in the Asian market for the past few months, the tip of the iceberg was finally revealed with the U.S. Department of Justice's complaint. It all stemmed from Jane Street Capital, a top-tier market maker founded in 2000, which was accused of executing a months-long 'sleight of hand' in the spot and derivative order books by means of targeted ETF arbitrage in the market, utilizing the spot ETF creation and redemption mechanism.

It wasn't until a legal complaint pushed this controversy into the public eye that discussions around the ETF arbitrage mechanism and price discovery structure rapidly heated up, triggering a violent market rebound and an epic short squeeze with a liquidation scale exceeding $240 billion.

But was Jane Street truly the culprit that pressed the suppression button? This is a question worth at least $10 billion.

I. Did Jane Street Really Suppress the BTC Price?

This question deserves an accurate answer. The most important thing to understand first is that this isn't just a question about Jane Street.

It's a question about the structural characteristics of the Bitcoin ETF framework, which applies equally to every Authorized Participant (AP) in the ecosystem. For BlackRock's IBIT alone, this list includes Jane Street Capital, JPMorgan, Macquarie, Virtu Americas, Goldman Sachs, Citadel Securities, Citigroup, UBS, and ABN Amro.

The role of these institutions is deeply misunderstood by the outside world, even among experienced industry veterans, and this misunderstanding deserves to be corrected before drawing any conclusions.

The first thing to understand about APs is that they occupy a marginal exception within the regulatory framework of Reg SHO (the SEC's rule on naked short selling). For instance, Reg SHO requires short sellers to locate shares (locate the stock) before shorting, but APs are exempted due to their contractual right to participate in creations and redemptions.

While this sounds procedural, its practical consequences are significant. It means any AP can create shares at will—no borrowing costs, no capital commitment traditionally associated with short selling, and aside from commercially reasonable timeframes, no hard deadline to close the position.

This is the gray area: a regulatory exemption designed for orderly ETF market making is, structurally, indistinguishable from regulatory arbitrage with an unmatched duration. This exemption is not unique to any single company. It is a prerequisite for membership in the AP club.

II. What Does This AP Exemption Mean?

Normally, if IBIT is trading below its Net Asset Value (NAV), you would expect arbitrage buyers to step in, redeem shares for bitcoin, and close the discount. But any AP *is* that arbitrage buyer; they control the pipeline. This means their incentive to close this discount is different from that of a third-party trading desk without creation/redemption rights.

It sounds complex, but a simple analogy makes it clearer:

First Layer: What is Normal 'Closing the Discount'?

Imagine there's a blind box on the market (this is the IBIT ETF). Everyone knows the blind box contains a real bitcoin voucher worth $100 (this is the NAV). But today, due to market panic, the blind box is priced at $95.

Following normal logic, smart merchants (arbitrage buyers) would frantically buy the blind box for $95, then go to the official source to open it, exchange it for the $100 bitcoin, sell it, and pocket the $5 difference.

And precisely because everyone is buying the blind boxes for arbitrage, the price of the blind box is quickly pushed up by buying pressure, returning to $100. This is called "closing the discount".

Second Layer: The AP with the 'Monopoly Channel'

But in the real world of Bitcoin ETFs, ordinary trading firms and retail investors are not qualified to go to the official source to "open the blind box" (i.e., they lack creation/redemption rights). Only a few privileged Wall Street investment banks (APs) in the entire market can do this. That is, APs monopolize the only channel to exchange ETFs for real bitcoin (they control the pipeline).

Third Layer: Why Don't APs Play by the Arbitrage Rules?

If it were an ordinary third-party merchant, seeing this $5 risk-free spread, they would act immediately. But APs are different; they calculate a more shrewd account: "Since only I can open the blind box, why should I hurry? If I intentionally don't pull the price back to $100, but instead use the current illusion of a low $95 price to go short or long in another casino (like the bitcoin futures market), I might make $20!"

In summary: The market originally has an automatic correction mechanism (if the price falls too much, someone will buy for arbitrage and push the price up). However, because the "only switch" to execute this correction mechanism is held by the APs, and the APs find that "not correcting, maintaining the discount" allows them to make more money elsewhere, they have no incentive to pull the price back to normal levels.

Retail investors suffer waiting for the arbitrage army to save the price, unaware that the only arbitrage army (the APs) is right next door, using this spread to make money in other markets.

III. The Problem Isn't Jane Street, It's the AP Structure

IBIT's short exposure could in principle be hedged by going long bitcoin spot, but this is not mandatory, as long as the chosen instrument maintains a tight correlation.

The obvious alternative is BTC futures, especially given their capital efficiency. This effectively means that if the hedging instrument is futures rather than spot, then the spot is never actually bought. And because the natural arbitrage buyer chooses not to buy spot, this discount cannot be closed through the natural arbitrage mechanism.

It's worth noting that the spot/futures basis is itself the domain of the entire basis trading community, which works to keep this relationship tight. But every separation between the hedging instrument and the underlying asset introduces impure basis risk (dirty basis risk), and this risk compounds throughout the structure—and it is under stress conditions that basis risk is where market dislocation appears.

The final piece of the puzzle involves the recently SEC-approved in-kind creation and redemption. Under the previous cash-only regime, APs were required to deliver cash to the fund, and then the custodian used this cash to buy bitcoin spot. This buying action was a structural regulator—it mechanically forced the purchase of spot as a consequence of creation.

In-kind creation/redemption completely eliminates this. Now any AP can deliver bitcoin directly, and the timing and counterparty for its source can be chosen at its own discretion: OTC desks, negotiated pricing, minimizing market impact.

The broadest interpretation of this flexibility is that an AP could maintain derivative positions aimed at capturing funding rate or volatility profits during the time between establishing a short and completing the in-kind delivery—all while ensuring each individual step still fits the definition of legitimate AP activity.

And this is precisely the crux of the problem. The beginning looks like normal market making, and the end looks like normal market making. It is the middle process that is difficult to clearly categorize. This is not an indictment of any single company. Every AP on the IBIT list, and by extension every AP for every Bitcoin ETF, operates within the same structural framework, enjoys the same exemptions, and therefore possesses the same theoretical capability. Whether any of them exercised this capability in a manner that verges on coordinated activity is a question that falls squarely within the purview of the "surveillance sharing agreements" the SEC required upon ETF approval.

Whether these agreements are sufficient to capture behavior that simultaneously spans spot, futures, and ETF markets (even including cross-border trading venues) remains a truly open question.

In a nutshell, Jane Street is just in the spotlight. The real problem is buried deep in the underlying architecture of the Bitcoin ETF, designed by Wall Street veterans. No specific AP is explicitly suppressing the bitcoin price. What the AP structure can suppress is the integrity of the price discovery mechanism itself, which may have far more profound implications than the former.

Therefore, the question truly worth asking is not whether a specific company is the villain, but whether a regulatory framework built for 20th-century traditional finance is suitable for hosting an emerging 21st-century asset whose "value lies in being free from control by regulatory agencies".

This is perhaps the tuition fee the crypto market must pay to enter the "era of big institutions." After all, while we crave the liquidity irrigation from Wall Street, we do not wish to passively accept the black-box games they construct using regulatory exemptions.

This is not just the answer about Jane Street, but the ultimate question of the Bitcoin ETF era.