Author: David, Chaoxiang Research

Chaoxiang Guide: Cerebras (CBRS) delivered its first quarterly report since the IPO. Q1 core revenue was $191 million, a 92% year-over-year increase, exceeding market expectations. However, Q2 core gross margin guidance dropped sharply from 46.5% to 36%-38%, causing the stock price to fall over 10% after-hours. This company, which makes chips from an entire wafer and bets on the AI inference track, holds OpenAI contracts worth over $20 billion and an AWS cooperation framework. Full-year revenue guidance is $855-$865 million. The growth data is solid, but the valuation debate is equally significant.

Key Points of Focus

- Revenue beats expectations, guidance beats even more. Q1 core revenue was $191.3 million (up 92% YoY), higher than the consensus estimate of approximately $181 million. Full-year core revenue guidance of $855-$865 million (up 69% YoY) exceeds the market expectation of $828 million. On a GAAP basis, cloud and services revenue reached $82.8 million, a 178% YoY increase, making it the fastest-growing segment.

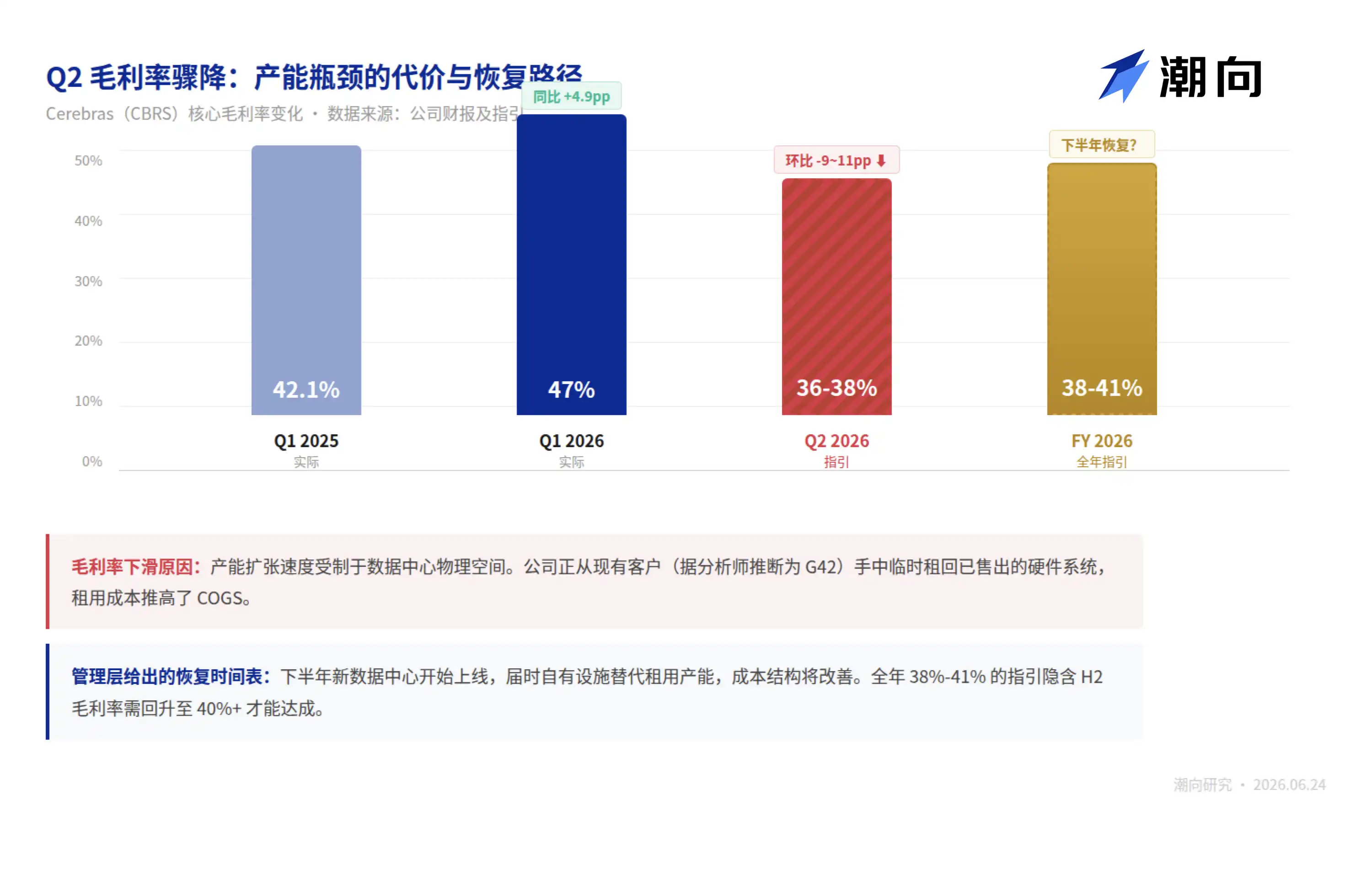

- The sharp drop in gross margin guidance is the biggest negative this quarter. Q1 core gross margin was 47%, up nearly 5 percentage points YoY. However, Q2 guidance fell to 36%-38%, a drop of about 10 percentage points from Q1; full-year guidance is 38%-41%. Management attributed this to insufficient data center capacity: the company is temporarily leasing back systems from existing customers who have already purchased the hardware to deploy capacity, worsening short-term costs. After-hours stock price fell over 10%.

- Customer concentration shows signs of improvement but is far from resolved. 86% of FY2025 revenue came from two UAE-related entities (MBZUAI accounted for 62%, G42 for 24%). OpenAI will start contributing revenue in February 2026, and the AWS cooperation is expected to reflect financially only in 2027. Genuine revenue diversification will not be verifiable until 2027.

- Valuation pricing extends to 2028. Based on the after-hours price of about $200, CBRS trades at about 90x trailing twelve-month revenue; even using the full-year guidance midpoint of $860 million, the forward P/S is still above 50x. The median price target from 10 covering analysts is $300 (range $250-$340), which implicitly assumes the OpenAI contract worth over $20 billion and AWS deployments are fulfilled on schedule and volume.

- Short-term catalysts and headwinds coexist. Catalysts: Accelerated deployment of OpenAI's 750MW computing power, AWS inference solution rollout, new data center capacity coming online in the second half. Headwinds: Lock-up period contains unconventional early release clauses (triggered if market cap exceeds $40 billion, current market cap is near that threshold), unclear path to gross margin recovery, OpenAI itself is not yet profitable and has already scaled back some computing power commitments.

Earnings Reveal Business Model Shift: From Selling Chips to Selling Computing Power

The most easily overlooked detail in the Q1 report is the change in revenue mix.

Under the core metric, hardware revenue was $111.6 million, accounting for 58% of total revenue; cloud and services revenue was $79.8 million, accounting for 42%. A year ago, this ratio was roughly 70:30. Cloud services revenue grew 167% YoY, nearly three times the growth rate of hardware.

Management made this trend clearer on the earnings call:

Hardware revenue will decline sequentially in the coming quarters because the company will deploy more hardware capacity into its own cloud to fulfill OpenAI's and AWS's inference computing power contracts, rather than selling directly to customers. Cerebras is shifting from a "chip-selling company" to a "computing power-selling company."

This transformation directly explains the sharp drop in Q2 gross margin guidance.

An analyst pressed for details on capacity deployment during the call. Management revealed:

The company's current bottleneck is not chip supply from TSMC, but the physical space in data centers. To deliver computing power to OpenAI as soon as possible, Cerebras is "temporarily leasing back" hardware systems already sold to G42 (its previous largest customer and a minority equity investor).

Deploying its own systems in leased third-party facilities worsens the cost structure in the short term, which is the main reason for the gross margin guidance drop from 47% to 36%-38%. Management's timeline indicates new data centers will start coming online in the second half of the year, easing cost pressures at that time.

The financial structure of the OpenAI contract is also worth unpacking. On the surface, it's a multi-year computing power purchase worth over $20 billion, but underneath, three relationships are layered: OpenAI provided Cerebras with a $1 billion operating capital loan (reflected on the Q1 balance sheet as $621 million in current loans and $362 million in non-current loans), while also receiving warrants for Cerebras stock.

In other words, OpenAI simultaneously plays the roles of largest customer, creditor, and potential shareholder for Cerebras. Risk disclosures in the S-1 indicate that if Cerebras fails to deliver capacity as agreed, OpenAI has the right to terminate the contract and trigger loan repayment.

The cooperation framework with AWS adopts a "split inference" architecture: AWS's Trainium 3 chip handles prompt input (prefill stage), while Cerebras's CS-3 system is dedicated to high-speed output generation (decode stage). This design allows Cerebras to handle only the part of the inference pipeline where its speed advantage is greatest. However, management declined to disclose the specific scale of the AWS cooperation during the Q&A and stated that revenue contribution would only appear on the financials in 2027.

The common feature of these two large contracts is: Contract sizes are massive, but realization paths are long, and heavily dependent on Cerebras's data center construction progress.

Full-year revenue guidance of $855-$865 million implies the next three quarters need to average around $220 million each, with sequential acceleration in growth. Management's statement is "year-over-year growth will increase each quarter in 2026, with more revenue concentrated in the second half."

The Bull Case: Nine Banks Initiate Coverage with Buy Ratings, What Are They Buying?

On June 8, the day the IPO quiet period ended, nine underwriting banks simultaneously initiated coverage, all issuing Buy or Outperform ratings. CBRS stock rose 18.3% that day. This kind of coordinated bullishness is not uncommon for US IPOs (underwriters have inherent interests), but their investment theses point to the same core proposition.

Thesis One: The battlefield for AI computing power is shifting from training to inference, and the rules of competition in inference differ from training.

Morgan Stanley analyst Joseph Moore issued an Overweight rating with a $250 price target in his June 8 initiation report. His core argument is: The training scenario competes on total computing throughput, where NVIDIA GPU clusters dominate absolutely; the inference scenario competes on the speed and latency of single responses, as models must process millions of user requests per second, and speed directly impacts service cost and user experience. Cerebras's wafer-scale chips, with their on-chip SRAM capacity far exceeding conventional GPUs (data doesn't need frequent movement to external memory), possess a structural advantage in inference latency. Moore's statement is that Cerebras is "the only company that has commercially deployed wafer-scale processors," giving it a first-mover advantage over NVIDIA.

Citi analyst Atif Malik gave the highest price target among coverages at $340. Mizuho added a technical detail in its June 8 report: The WSE-3 chip has 44GB of built-in SRAM, several times that of Google's latest TPU and Groq's LPU, a hardware gap that cannot be closed through architectural optimization in the short term.

Thesis Two: Two major contracts advance Cerebras from a "technology story" to a "revenue story."

The OpenAI contract exceeds $20 billion, covering 750MW of inference computing power, to be delivered over multiple years. Amortized over five years, this contract alone would contribute approximately $4 billion in annual revenue, nearly 5 times the midpoint of the 2026 full-year revenue guidance. Although management refused to disclose the specific amount for the AWS cooperation, the framework is confirmed: Cerebras's inference capabilities will be offered globally to enterprise customers through Amazon Bedrock.

Q1 earnings data provided early validation. OpenAI began deploying Cerebras systems in February, and cloud service revenue jumped from less than $30 million YoY to nearly $80 million in one quarter. Management's statement is "year-over-year growth will increase each quarter in 2026, with more revenue concentrated in the second half." The full-year guidance of $855-$865 million exceeds the consensus estimate of $828 million.

Thesis Three: The density of coverage right after the quiet period is itself a signal.

The median price target from 10 analysts is $300, with a low of $250 (Morgan Stanley) and a high of $340 (Citi). Based on the after-hours price of $200, the median target implies about 50% upside. Wedbush ($270 target), Needham ($300), Barclays ($280), TD Cowen ($275), and Craig-Hallum (Buy) all initiated coverage in the same week.

The underlying assumption of the bull case can be summed up in one sentence:

If AI inference becomes a larger computing power market than training (multiple institutions predict inference spending will surpass training by 2027), and Cerebras's speed advantage is real and sustainable, then it only needs to capture 3%-5% of the market where NVIDIA holds an 80%+ share to justify its current valuation.

The Bear Case: Gross Margin, Customer Concentration, and the Fragility of a $45 Billion Valuation

For each of the bull's three theses, the bears have counterarguments.

Counterargument One: The moat from inference speed advantage may be narrower than imagined.

Cerebras's speed advantage is built on on-chip SRAM capacity, but NVIDIA is not standing still. The B300 chip released by NVIDIA in March significantly increased HBM bandwidth, and Groq's LPU architecture is also iterating rapidly on the inference front.

Viewed from another angle: Cerebras's customers are currently highly concentrated in just OpenAI and AWS. OpenAI is also one of NVIDIA's largest GPU purchasing clients, and AWS's in-house Trainium chip is covering more and more inference scenarios. Cerebras's major customers are simultaneously betting on alternatives, meaning its speed premium will face continuous price negotiation pressure.

Counterargument Two: The gross margin decline might not be just "temporary."

Management attributed the Q2 gross margin drop from 47% to 36%-38% to temporary leasing costs due to insufficient data center capacity. But this explanation assumes "costs will improve when new data centers come online in the second half."

Considering that revenue scale is expected to jump in the second half (management explicitly stated revenue is back-end loaded), and new data center capacity ramp-up itself requires time and capital investment, this recovery path is not easy.

A deeper issue is the impact of the business model shift itself on gross margin. Cerebras's shift from selling hardware to selling cloud computing power means taking on data center construction, operation, and depreciation costs. As depreciation expenses for self-built data centers are accounted for, uncertainty remains over whether cloud service gross margins can stay above 50%. The profitability ceiling of this business model has yet to be tested.

Counterargument Three: Customer concentration is a problem that has "changed names but is not solved."

In 2024, G42 alone contributed 85% of Cerebras's revenue. In 2025, G42's share dropped to 24%, but MBZUAI (Mohamed bin Zayed University of Artificial Intelligence) surged from nothing to 62%. The S-1 prospectus clearly labels these two as "related parties." The two UAE-related entities combined still account for 86% of revenue. Revenue source diversification is more about a change in names rather than substantive dispersion.

Finally, CBRS's IPO lock-up period contains an unconventional clause:

If the company's market cap consistently exceeds $40 billion, insider shares can be released early. At the after-hours price of $200, the current market cap is about $45 billion, already near the trigger line. On the short side, as of May 29, the short interest was 17.15% of the float, which is on the high side. If the lock-up period triggers an early release, unleashing a large number of insider shares, combined with existing short pressure, the stock could face concentrated selling.