Written by: Sanqing, Foresight News

On July 15, US securities clearing giant DTCC (The Depository Trust & Clearing Corporation) converted stocks, ETFs, and US Treasury bonds held in custody under The Depository Trust Company (DTC) name into on-chain tokens for the first time in a real transaction, completing a series of operations including treasury repo, collateral pledging, securities lending, and stock settlement in one day. About 40 institutions participated. DTCC called this its largest tokenization production test to date, paving the way for the DTCC Tokenization Service scheduled to launch in October.

Among them, JPMorgan Chase led the way by tokenizing the Invesco QQQ Trust and posting the tokenized assets as CCP margin to CME Group; State Street's SPDR S&P 500 ETF (SPY) was tokenized; Citadel Securities and DriveWealth completed equity token conversions; DriveWealth and Vanguard completed the DVD settlement of tokenized equities; Societe Generale completed treasury bond token conversion; Societe Generale and Citadel Securities jointly completed collateral pledge settlement; Marex executed real-time collateral transfers, repos, and equity buy/sell transactions involving tokenized US Treasuries, stocks, and ETFs.

DTCC is the clearing and settlement backbone of the US securities market, operating for over 50 years, jointly owned and governed by the industry. Its business is handled by three core subsidiaries: DTC (The Depository Trust Company) is responsible for the registration, custody, and settlement of securities; NSCC (National Securities Clearing Corporation) acts as the central counterparty for transactions like stocks, providing trade guarantees and netting; FICC (Fixed Income Clearing Corporation) handles the clearing of US Treasury bonds and mortgage-backed securities. Nearly every US securities transaction ultimately passes through this system. In 2025, DTCC subsidiaries processed approximately 4.7 quadrillion dollars in securities transactions; DTC alone holds securities valued at over $114 trillion, originating from more than 150 countries and regions.

Previously Bypassing Wall Street, This Time Wall Street Opens the Door Itself

To understand the significance of this day, one must first see how previous tokenized US stocks came to be.

Real stocks are held in accounts at DTC, beyond the reach of the on-chain world. Hence, various substitutes emerged: derivative contracts, which only speculate on price movements; SPVs (Special Purpose Vehicles), where the SPV buys the stock, and the token represents a claim against this shell company; licensed brokers holding real stocks 1:1 in custody, with the token being a beneficial interest certificate for these stocks, akin to an on-chain depositary receipt...

These approaches differ in their proximity to the "real stock," but share a common thread: they all circumvent the security itself. The real stock is locked away at DTC, inaccessible from the outside, so one can only create a replica outside the system.

This time, DTCC proactively opened the door, issuing an on-chain digital identity itself. It minted a one-to-one corresponding "digital twin" token on-chain for securities already held in custody at DTC, sharing the same CUSIP and code as the underlying security. DTCC emphasized these tokens enjoy "the exact same investor protections, rights, and ownership" as the traditional securities.

Source:DTCC Official Website

Among the roughly 40 institutions participating, besides well-known traditional players, there were also many crypto-native companies.

Circle used its stablecoin for cash-side settlement, and its own stock CRCL was also among the assets tokenized this time; Chainlink handled oracle and cross-chain services; Fireblocks, BitGo, Blockdaemon, and Kaleido provided custody, wallet, and node services; Talos provided institutional trading technology; Digital Asset behind the Canton chain and LF Decentralized Trust behind the Besu chain were naturally present as well.

But those directly building businesses around tokenized securities are Ondo and Prometheum. Ondo issues tokenized stocks aimed at the on-chain and DeFi world, while Prometheum is a licensed digital asset securities firm, integrating brokerage, trading platform, custody, and clearing, specifically designed to legally hold and trade tokenized securities.

Four Years of Preparation, Two Chains in Place

DTCC has a history with blockchain; this move was not impromptu.

In 2022, it launched Project Ion based on R3 Corda, a stock settlement platform running in parallel with its legacy system, handling over 100,000 transactions daily at its peak. This was its first time putting distributed ledger technology into live settlement.

In October 2023, it acquired blockchain firm Securrency, forming the DTCC Digital Assets division led by former State Street digital asset head Nadine Chakar. Securrency's technology was later integrated into its multi-chain tool, ComposerX.

Starting in 2024, DTCC shifted its focus to Hyperledger Besu, launching the blockchain platform Digital Launchpad and the collateral management platform Collateral AppChain.

Besu is its self-built private chain. Its predecessor was Pantheon, developed by ConsenSys in 2018. After being donated to Hyperledger in 2019, it was renamed. Its advantage lies in strict permission controls while maintaining compatibility with Ethereum development tools. DTCC's internal bookkeeping, settlement, and collateral management run on this chain, inaccessible from the outside.

In 2025, another chain entered the picture. DTCC participated in a $135 million funding round for Digital Asset, the developer of the Canton network. Other investors in the same round included Goldman Sachs, BNP Paribas, Circle, Citadel, and DRW. At the end of the year, DTC received a no-action letter from the SEC, allowing it to legally operate tokenization services for three years. It subsequently migrated Treasury bonds onto Canton and, together with Euroclear, became co-chairs of the Canton Foundation.

Canton is a public network built by Digital Asset using the Daml language but features "sub-transaction privacy," which typical public chains lack: in a single transaction, each party only sees the parts relevant to them. For example, in a Treasury repo transaction, the bank handling the cash side cannot see the transfer of the underlying securities. Previously, Goldman Sachs' GS DAP, HSBC's Orion, and Broadridge's DLR platform handling trillions in monthly repo volume were built on it, with nearly 400 institutions already participating.

One chain internally maintains control, the other externally connects to liquidity. By July this year, the industry working group behind DTCC had grown from a few dozen to over a hundred members. Capital, regulation, allies, technology... everything was prepared over four years, showing this is not a whimsical tech demo, but DTCC making a grand entrance on its own terms and at its own pace.

Issuance Rights Centralized, Others Fall Back to Access Points

First, consider what DTCC itself wants. It's not seeking proof-of-concept; it wants liquidity for collateral.

That day, JPMorgan tokenized Invesco's QQQ ETF and directly posted it as margin with CME, marking the first time a central counterparty accepted this type of on-chain token generated from traditional securities.

The significance lies in the fact that an asset originally confined to a specific account can now be mobilized 24/7 across venues, unlocking capital previously frozen by settlement delays. This also explains why clearing giant DTCC is driving this change. The tangible return for it is a substantial improvement in its own capital efficiency, leading to increased revenue.

Those who should truly reconsider their positioning are likely the projects tokenizing US stocks. Their core task in recent years has been proving to users that "tokens are indeed backed by real stocks." Now that the depository institution itself issues standardized tokens, this role has been assumed at the source. However, what DTCC does not do is distribution, liquidity provision, cross-chain bridging, and DeFi composability.

For all such projects, the user-facing product experience may not change drastically. They still don't connect directly to DTC but operate through participants. What users receive are still tokens issued by the projects themselves. What changes is the underlying support: instead of SPV claims or synthetic positions, it can now be DTCC-generated beneficial interest certificates sharing the same CUSIP as the underlying security, convertible to and from traditional forms.

This also makes it more transparent. The twin certificates are recorded at the depository layer, making proof-of-reserves a native capability. Anyone can verify on-chain whether a token corresponds 1:1 to a real DTC interest, whereas in the traditional system, DTC's ledger has never been visible to end investors. These projects lose their issuance premium but can borrow DTCC's credibility.

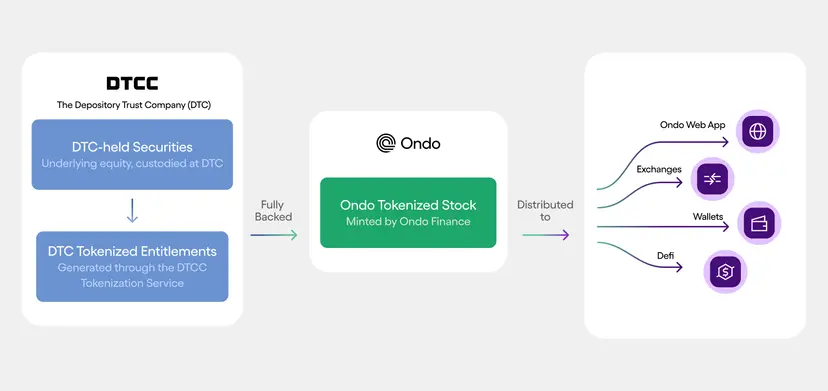

Take Ondo as an example. In this production-level test, it accessed the DTC participant network through Alpaca Markets and issued CRCLon (corresponding to Circle stock CRCL) and SPYon (corresponding to the S&P 500). Users still hold Ondo's tokens, but the underlying asset is now a DTC interest certificate with the same CUSIP.

Source:Ondo Finance Blog

And Ondo holds an advantage others don't: it's the only working group member whose primary business is on-chain stock tokenization. The DTCC Tokenization Service won't officially launch until October, but Ondo has already leveraged the production-level test to launch multiple tokens under this new model ahead of others.

The battle for tokenization ignited by crypto seems on the verge of being won. Except the one holding the steering wheel is DTCC, the entity that has always sat at the clearing hub and has now, in its own time, opened the door wide.