Author: 798.eth

The Bound platform, currently popular in the Bitcoin ecosystem, was formerly known as Radfi. It started as a platform I began using at the end of 2025, associated with the NodeStrategy monkey strategy token, and has now upgraded and rebranded as Bound Exchange. This platform features a unique asset, essentially the monkey strategy—a flywheel for Node Monkeys with underlying asset support. The key is whether the underlying assets can sustain it.

Today, I'll mainly discuss its asset deposit/withdrawal and trading logic. But before diving into the mechanisms, let me first explain the differences between the upgraded Bound and the original Radfi.

1. Past and Present: From Radfi to Bound

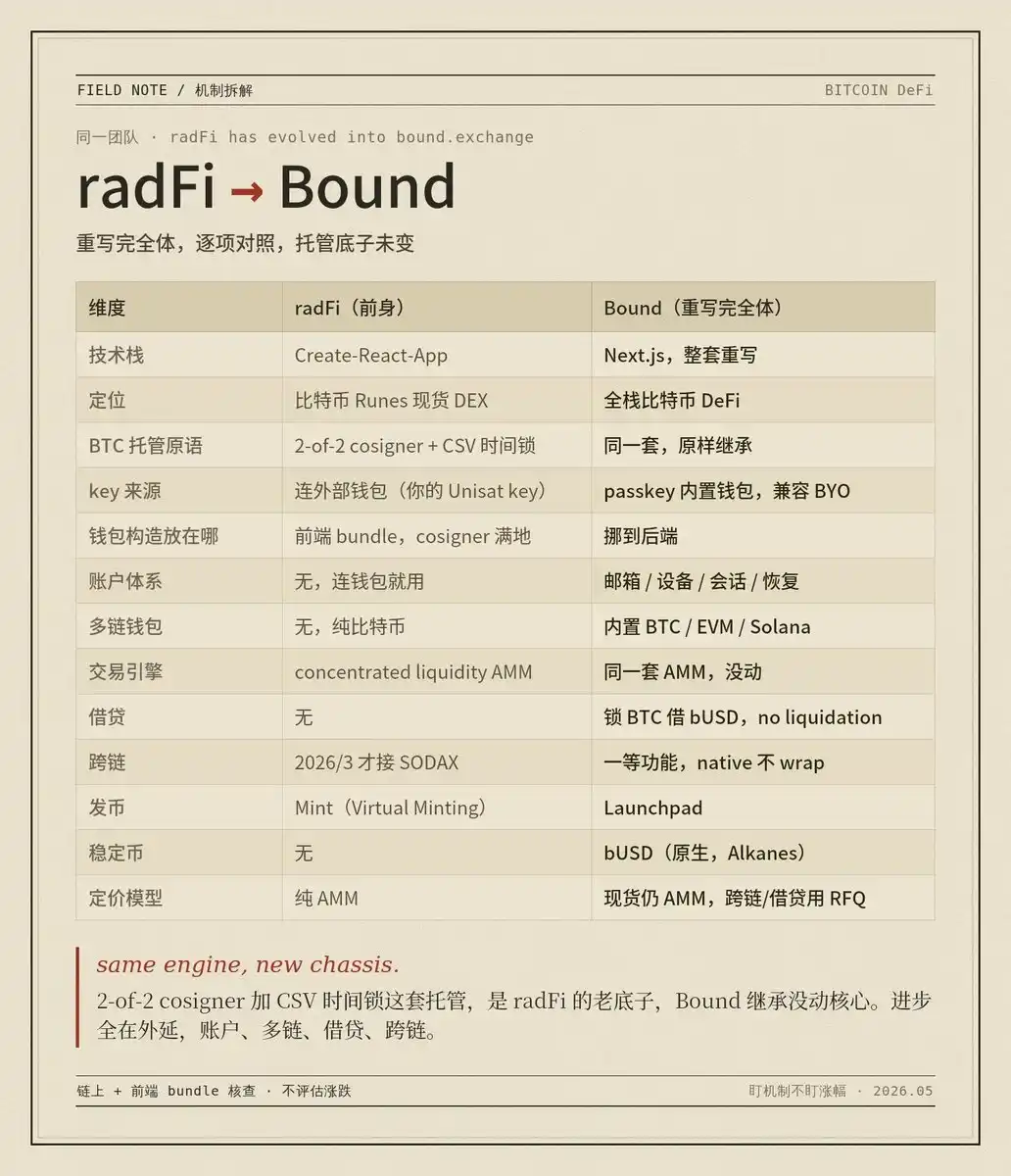

Bound didn't emerge out of thin air; it's a complete rewrite and evolution of Radfi. The Radfi website now displays a line stating, "Radfi has evolved into bound.exchange." It's the same team, with the tech stack migrated from Create-React-App to Next.js—a full rewrite.

Bound's key additions are a passkey-built-in multi-chain wallet, fixed-term loans collateralized by Bitcoin for bUSD, and SODAX cross-chain. The trading engine remains Radfi's concentrated liquidity AMM; the Runes swap functionality is unchanged.

This product line features two sets of 2-of-2 plus timelock. The account layer set protects you, allowing you to bypass Bound after three months; the lending set protects lenders, allowing them to directly take your collateral after the grace period expires. (See chart for a side-by-side comparison of Radfi → Bound)

2. Core Mechanism: Asset Deposit/Withdrawal and 2-of-2 Multi-Signature Custody

Understanding its positioning, let's examine its asset management logic. There are two main points: 2-of-2 multi-signature custody, and timelock countdown protection in the event of platform abandonment or downtime.

First, set up the scenario. You have BTC and want to trade on a platform. The traditional method is to send coins to the platform's wallet, where they are held for you. The problem is the coins are no longer in your possession; if the platform runs away or is hacked, your coins are gone—FTX and Celsius failed this way. Bound aims to solve this contradiction: achieving CEX-like transaction speed without relinquishing control of your coins.

Step 1: What is a deposit?

After registering, Bound provides you with a Bitcoin address, starting with "bc1p." To trade, you first transfer BTC from your wallet to this address. This is a standard Bitcoin transfer, taking about half an hour with 3 confirmations. Up to this point, it's no different from using a regular wallet. The real design lies in the next question.

Step 2: Who holds the private key for this address?

This is the core of the entire system. There are only two naive approaches: if the private key is solely with the platform, it's custodial, reverting to the FTX problem; if it's solely with you, the platform cannot facilitate fast trades, requiring manual signing for every transaction—slow.

Bound's solution is that this address doesn't have just one key; it has two. To move coins from it, both keys must sign. This is 2-of-2 multi-signature.

Step 3: Whose keys are these?

One is yours, stored on your device, invoked via passkey, with the private key never leaving the device. The other is in Bound's backend. During daily trading, you sign with your passkey, Bound's backend automatically adds the other signature, and with both combined, settlement is near-instantaneous.

Pause here to consider this. Bound holds only one key; it cannot move your coins unilaterally, so it's not custodial and cannot lend out or misappropriate your coins. But together, you can achieve instant settlement, recovering the speed. This is the intended effect of 2-of-2—achieving both security and speed.

Step 4: What problem does the timelock solve?

2-of-2 introduces a new issue. Since two keys are required, what if Bound runs away, goes down, or is shut down? The backend key might be lost forever, leaving you with only one key. Would your coins be locked in the address forever?

Timelock plugs this hole. The rule is simple: Bound's co-signing key has a 3-month validity period. Within 3 months, moving coins requires both keys. After 3 months, you can withdraw all coins with just your single key, no longer needing Bound.

Crucially, this isn't just a promise from Bound; it's encoded into the Bitcoin script and enforced by the Bitcoin network. Bound's consent is irrelevant; when the time comes, you can single-sign and leave. This is the foundation of its claim to be self-custodial.

Step 5: Withdrawals now make sense.

For normal withdrawals, your passkey signs plus Bound's backend co-signs—both keys ready, instant arrival. For emergency withdrawals, if Bound disappears, you wait out the 3-month timelock, then use your single key to sweep the coins to any address.

Linking these five steps together, the initial four terms form a chain: you deposit coins into a 2-of-2 address (deposit); daily, you and Bound spend together (fast-path withdrawal); Bound's key expires in 3 months (timelock); after expiry, you can leave with just one key (escape-hatch withdrawal).

3. Underlying Logic: Bound Exchange's Transaction Sequencing

Having understood how assets are deposited, let's discuss Bound Exchange's transaction sequencing.

There are no smart contracts on Bitcoin. So, for a native Bitcoin DEX's AMM, where is matching done, and who decides the order of your trades? Essentially, it's a CEX-like matching backend, with the Bitcoin blockchain serving as the settlement layer. Let's break it down:

-

First, the AMM curve is not on-chain. BTC L1 lacks contracts; states like reserves, ticks, and liquidity ranges have nowhere to be stored and must reside in Bound's backend database. The UTXOs on-chain only represent the settlement outcome of LPs' funds under custody.

-

Second, on-chain transactions are merely settlement receipts. I pulled the trade history of that pool; each inflow/outflow is a fixed, predetermined amount, containing no curve calculation itself. The multiplication along the curve is completed off-chain in the backend before anything goes on-chain. The dozens of trades in a block, each spending separate UTXOs, unconnected to each other, precisely because the price was fixed off-chain; going on-chain is just about recording a set of pre-calculated numbers.

-

Third, how is a single trade priced? When you want to buy/sell on the frontend, the frontend requests a quote from the backend. The backend calculates using its maintained concentrated liquidity curve, your order consumes liquidity along the tick, fees are deducted, and it gives you a number. You sign a PSBT locking in this number, the backend verifies and co-signs/broadcasts it, simultaneously advancing its off-chain curve by one step. The curve lives only in the backend.

-

Fourth, sequencing is mathematically forced by this curve and unavoidable. The curve has state; at any moment, there's only one current position. Each incoming order consumes a segment of liquidity, pushing the curve to a new position; the next order can only execute at the new position. This means all orders inherently cannot settle simultaneously; they must be arranged in a strict sequential order. The first trade executes at the original position, pushing the curve one step; the second executes at the new position, pushing it again, and so on.

-

Fifth, but who decides this order and based on what is another matter. Distinguish between two sequences: one is the real-time timestamp when you click confirm, the other is the processing order the backend actually uses to advance the curve. Nothing on-chain or in the protocol guarantees these two match. Your order enters Bound's backend queue. Whether it declares the order, processes by arrival time, or bumps someone ahead/behind, is entirely its internal affair—you cannot see it.

-

Sixth, this is the entry point for operator MEV, even sharper than typical on-chain MEV. In general DEXes, the transaction order is at least visible in the block; front-running, sandwiching can be analyzed afterward. Bound's sequencing occurs off-chain; after results are settled in a block, even sequential traces are absent—dozens of unrelated transactions show no order on-chain. However, at the moment you click confirm, the price is already calculated based on a point on the curve. You just don't know its position within the block's sequence.

Therefore, Bound does have order; order is mathematically mandatory. It simply centralizes the power to define this order entirely within a black box. At the principal level, it is indeed self-custodial—2-of-2 plus timelock, the platform cannot move your coins. But the price and sequence at which your trade executes are accounted for off-chain by it alone. Ultimately, this is a CEX-like matching backend, interfacing with the world's largest blockchain for settlement, finalizing roughly every ten minutes with an immutable block.

4. Practical Tips and Experience Feedback

Finally, two practical details to avoid pitfalls. This 2-of-2 address only accepts BTC and Runes. Sending BRC-20, Alkanes, or coins from other chains will result in permanent loss. Alternatively, you can bypass Bound's system and directly connect your own Unisat or Xverse wallet. That means no 2-of-2 or timelock; coins remain in your single-signature wallet, but the trade-off is requiring manual signing for every transaction.

Based on current experience, there are still minor issues. I tested; a previous transaction already had two block confirmations, but the Bound frontend still showed "pending," preventing me from placing the next order. Hopefully, @Bound_Exchange official can look into this problem.