Original|Odaily Planet Daily(@OdailyChina)

Author|Wenser(@wenser2010)

Amid the ongoing market decline, Strategy and Bitmine, the "Twin Titans of DAT Treasuries," have both incurred massive floating losses.

This morning, BTC briefly fell below $62,000, currently hovering around $63,800; ETH dropped below $1,800, currently around $1,780. At current prices, Strategy's floating loss has reached a staggering $10 billion; Bitmine's floating loss is also around $9 billion. For now, Michael Saylor and Tom Lee are "fellow sufferers in the same predicament," with Strategy and Bitmine ranking as the top two "DAT companies with the largest losses."

However, compared to Strategy, which requires continuous dividend payments, Bitmine faces less financial pressure and retains flexibility such as raising funds through STRC preferred shares. It is reported that Bitmine plans to raise $300 million by issuing perpetual preferred shares with an annual dividend yield of 9.5%. It seems Bitmine's pace of acquiring ETH continues; meanwhile, the Sword of Damocles hanging over Strategy becomes: Where will the funds for subsequent STRC dividend payments come from? Between the two, who faces greater financial pressure? Odaily Planet Daily will analyze for readers.

Bitmine VS Strategy: The Divergent Paths of DAT Holdings

Following today's BTC plunge, community members used AI to mock Saylor's "promotion" of BTC: "A man in his sixties personally promotes, ancestral BTC price drops to $62,000 per coin."

Returning to Bitmine and Strategy, currently, Bitmine's financial structure appears safer; whereas Strategy's leverage pressure is greater.

Bitmine's Equity Issuance Game: The Debt-Free DAT Financing Play

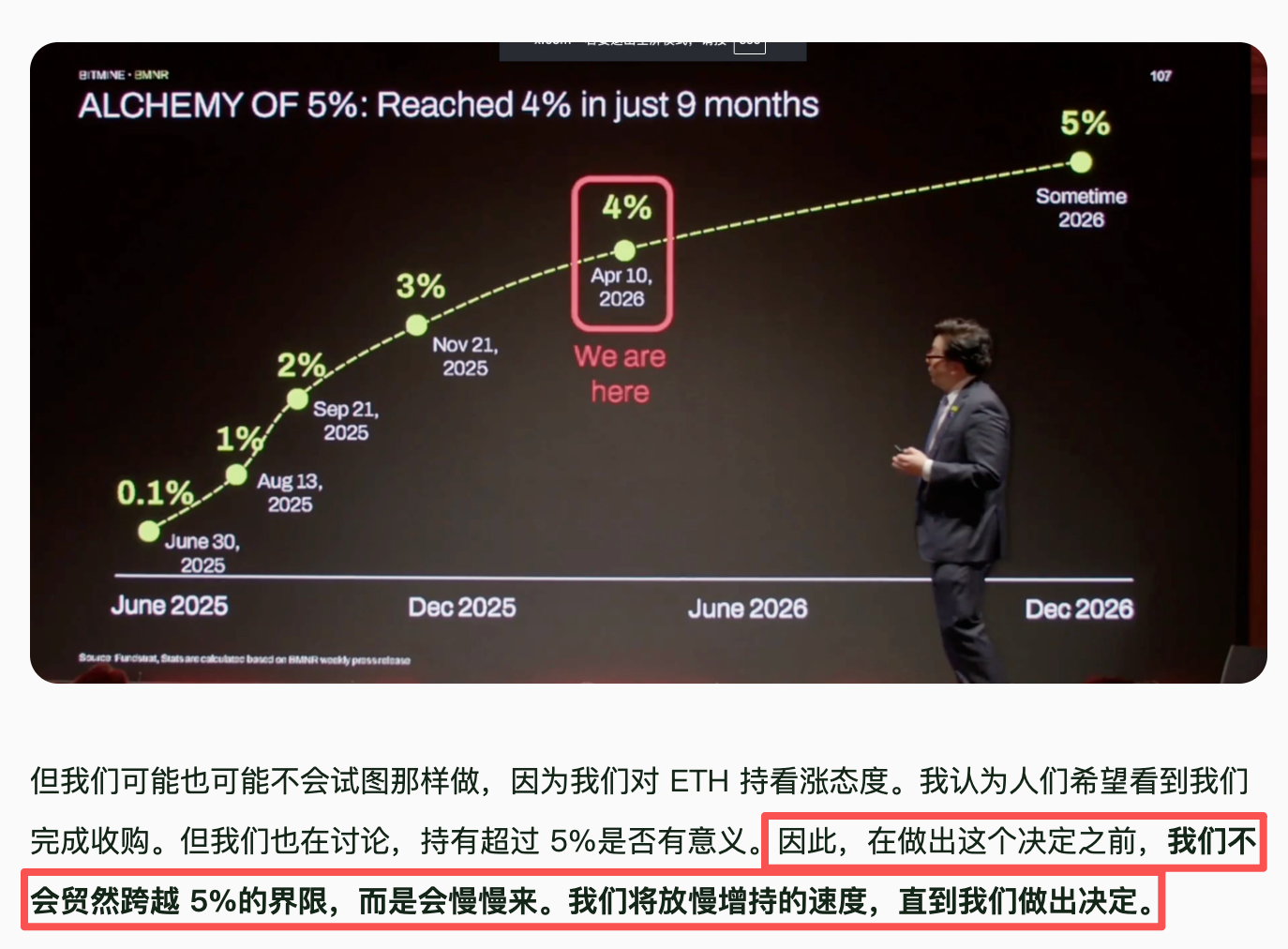

As of June 1, Bitmine holds 5,416,901 ETH; accounting for approximately 4.49% of ETH's total supply, nearing the '5% cap' repeatedly emphasized by Bitmine Chairman Tom Lee. Yesterday, Bitmine once again acquired 25,000 ETH via BitGo, valued at $48 million at the time. Currently, its holdings stand at 5,441,901 ETH.

The reason Bitmine has the confidence to continue accumulating during a market downturn is multifaceted. The primary reason is that Bitmine's funding source is equity issuance:

- When initiating its ETH treasury and establishing the DAT company in June last year, Bitmine obtained initial seed capital through financing — $250 million, along with a small PIPE financing.

- After July last year, Bitmine primarily relied on ATM equity issuance, gradually increasing this figure from $2 billion to $24.5 billion.

Sufficient funds give Tom Lee ample confidence, and Bitmine's book cash supports further acquisitions — in its June 1 public announcement, Bitmine also mentioned: The company's stake in Beast Industries is valued at $180 million; its stake in Eightco Holdings is valued at $93 million. The company's total cash amounts to $446 million.

Additionally, Tom Lee has previously boasted that Bitmine's Ethereum treasury generates daily staking rewards of $1 million. This refers to Bitmine staking approximately 87% (about 4.71 million ETH) of its ETH holdings through its MAVAN staking network, with estimated annualized returns of about 2.73%-3% (approximately $250-$300 million), which can also provide relatively stable cash flow.

In summary, Bitmine's financial condition is sound; and the latest preferred share financing with a 9.5% annualized dividend is expected to secure $300 million, further alleviating its financial pressure. For this company, the biggest risk points lie in equity dilution (issuing new shares) and further stock price declines due to book floating losses. If mNVA remains <1, it might trigger stock selling.

Strategy's Debt Leverage Game: Pressure from Convertible Bonds and Preferred Share Dividends

Compared to Bitmine's "using investors' money to buy ETH," Strategy faces greater financial pressure in acquiring BTC because it primarily "borrows money to increase BTC holdings."

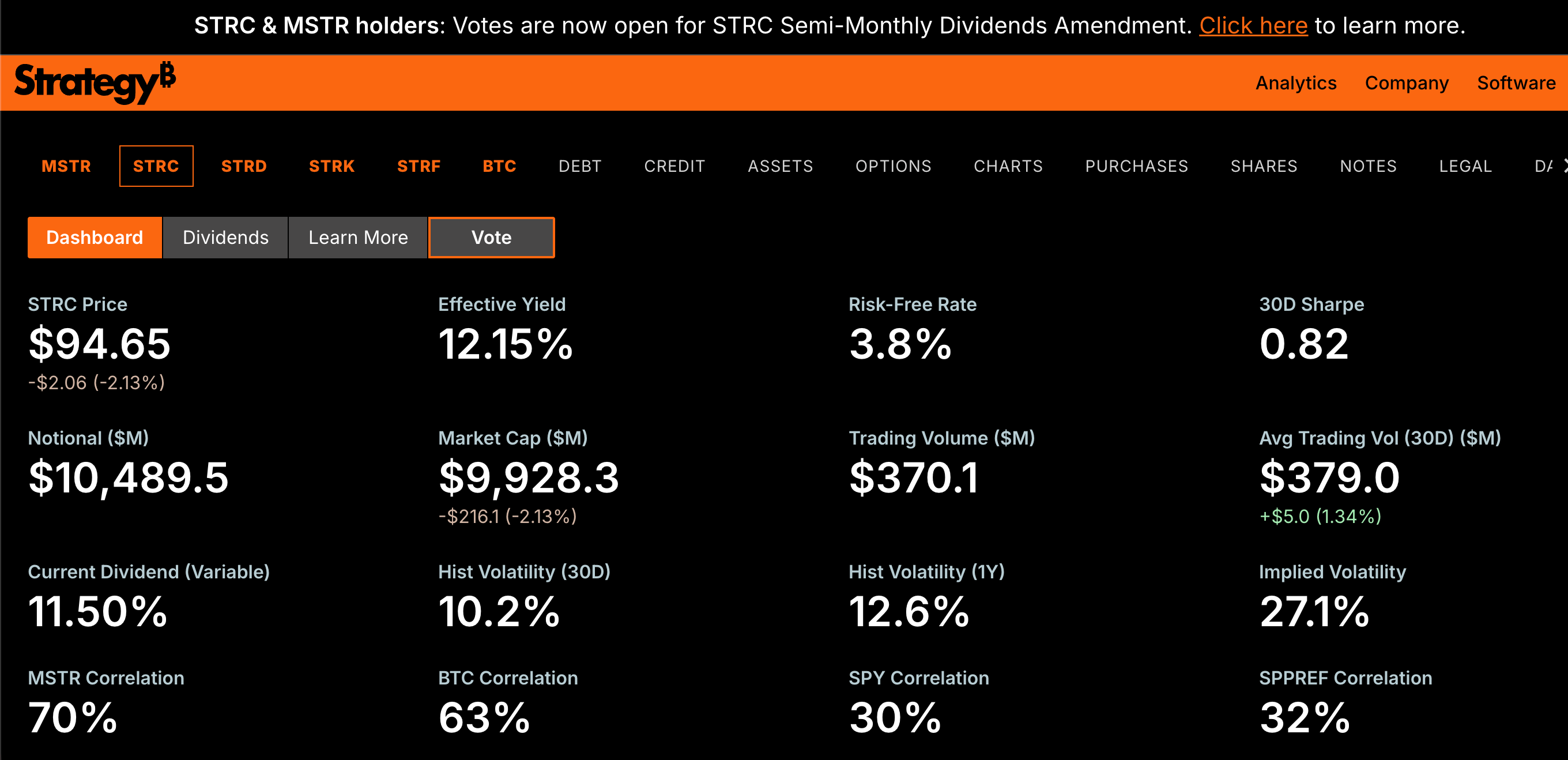

According to information on Strategy's official website, currently, Strategy holds approximately $6.7 billion in convertible bond debt, plus about $9.9 billion in STRC preferred shares and market-value-varying amounts of STRD, STRK, STRF, requiring annual massive dividend and interest payments. At the end of May, after repurchasing $1.5 billion in convertible debt, Strategy's cash reserves fell to about $871 million, covering only about 6 months of its estimated $1.7 billion annual preferred dividend obligation.

Moreover, Strategy previously initiated a vote on "proposing to increase STRC dividend payments from monthly to twice monthly." The voting began on April 28 and will conclude on the meeting day of June 8. If approved, the first record date under the new schedule is June 30, and the first payment date is July 15. Eligible voting shareholders (holders of MSTR and STRC shares) must have held shares before April 17.

Also worth mentioning is that STRC's authorized issuance cap is approximately $28.3 billion. Possibly affected by BTC's continuous decline and shaken market confidence, STRC fell below $95 this morning, currently at $94.65, "de-pegging" over 5% from the $100 target price.

Compared to Bitmine, Strategy currently faces a significant gap between excessive preferred share financing amounts and dividend payments, exacerbated by BTC's continuous decline. Furthermore, unlike ETH which has a staking ecosystem for additional liquidity, BTC lacks such options.

Therefore, after Strategy sold 32 BTC last month, the market began to doubt the identity of "diamond-handed Strategy that only buys and never sells." Amid BTC's persistent decline, Strategy might face a series of liquidity crises, leading to an inability to repay debts and dividends, thereby selling more BTC and driving down prices. Essentially, Strategy is playing a "high-leverage bet that the BTC price won't fall below a certain level" debt leverage game.

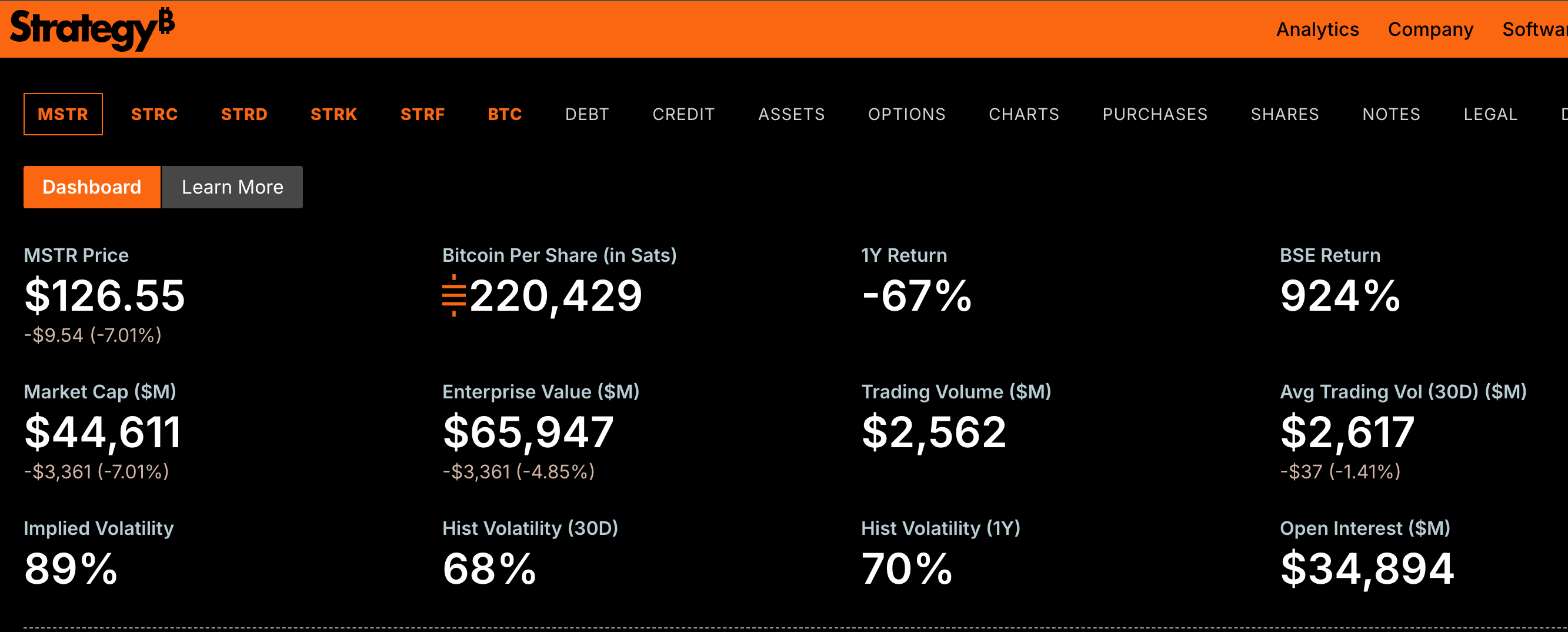

Thus, considering Strategy's current mNAV value of 0.83, the market remains highly skeptical of its future stock performance. Yesterday, its market capitalization already fell out of the top 200 US companies. Currently, Strategy (MSTR) stock is at $126, down 7% in 24 hours; market cap stands at $44.6 billion.

Of course, as a leader among DAT treasury companies, Bitmine Chairman Tom Lee remains quite optimistic about Strategy, previously stating: "Strategy selling Bitcoin and ETF outflows are typical bottoming behavior, not risk signals." At the recent "Proof of Talk 2026" conference at the Louvre in Paris, Tom Lee made bold claims: "With AI and tokenization driving major changes in financial infrastructure, ETH could ultimately reach $250,000." However, when discussing "Bitmine's actions after its ETH holdings reach 5% of the total supply," he also expressed caution about further ETH accumulation. (See "Tom Lee Recharges Faith: Crypto Spring Has Arrived, ETH Will Rise to $250,000")

Currently, Bitmine and Strategy find themselves in highly similar market situations, but Bitmine's financial condition is slightly better; Strategy faces the choice between "selling more BTC to obtain cash flow for dividend payments" and "sitting idle or continuing to borrow for acquisition as BTC keeps falling."