Written by: ChandlerZ, Foresight News

The decentralized credit protocol Goldfinch, which secured a total of $37.7 million in funding across two rounds led by Andreessen Horowitz (a16z), has officially entered the shutdown process.

The core development team, Warbler Labs, posted GIP-87 on the governance forum, proposing to "approve the operational maintenance of Goldfinch and the orderly liquidation of Goldfinch Prime," to shut down its product Goldfinch Prime in an orderly manner and transition the protocol into a maintenance mode retaining only collection functions. The Snapshot vote will close on June 23, and as of writing, it has received 100% approval (over 1.1 million GFI votes, far exceeding the 250,000 threshold).

After six years of operation and issuing approximately $100 million in loans, this protocol, which promised to transform emerging market credit with DeFi, ended with widespread borrower defaults and frozen depositor funds.

Depositor's Dilemma: 70% Actual Loss Rate, Token Down 99.8%

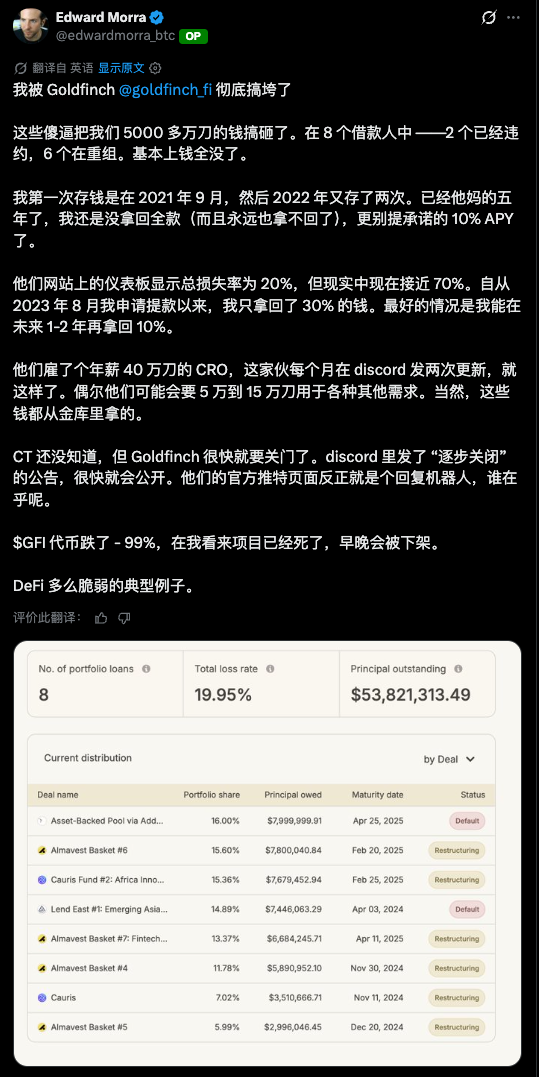

On June 19, a depositor named Edward Morra posted on X, stating that among the 8 borrowers in the protocol's loan book, 2 had defaulted and 6 were in restructuring, with funds essentially unrecoverable. This post received over 800 likes and 165 replies.

Morra said his first deposit was in September 2021, followed by two more deposits in 2022. After five years, he still hasn't recovered the full amount (and never will), let alone the promised 10% APY. Since requesting a withdrawal in August 2023, the user has only recovered 30% of the principal, with the best-case scenario being a possible recovery of 10% in the next 1 to 2 years.

He estimates the actual loss rate to be around 70%, far higher than the 20% displayed on the protocol dashboard.

DefiLlama shows that Goldfinch still has $56.15 million in outstanding loaned capital, while the TVL on Ethereum is only $1.63 million, with almost all deposit funds locked in loans and unavailable for withdrawal.

The protocol's governance token, GFI, has also suffered a severe decline. After reaching an all-time high of $32.94 on January 11, 2022, GFI is currently priced at $0.06524, a drop of 99.8%. Its market capitalization has shrunk from over $180 million in April 2024 to $5.7 million.

Shutdown Plan: Establish a Trust, Collection for at Least Two Years

The GIP-87 proposal was jointly signed by Mike Sall and Blake West of Warbler Labs. The core arrangements of the shutdown plan include: Warbler Labs immediately halting all new product development, growth initiatives, and marketing campaigns. The protocol will establish a new US trust entity, with the current Chief Restructuring Officer, Ted Gavin, serving as trustee, dedicated to collecting remaining borrower debts. Warbler Labs receives a $150,000 shutdown service fee ($100,000 from the DAO treasury, $50,000 transferred from existing operational budget). Legacy applications will be retained for at least 6 months after the final borrower repayment, allowing depositors to claim recoveries. The estimated recovery period is over 2 years.

Blake West responded to the community's anger in a Discord post on June 14, stating that the team spent six years from 2020 trying various on-chain private credit solutions but never found sustainable demand. The latest product, Goldfinch Prime, shifted towards tokenizing institutional-grade private credit funds (with partners including Apollo, Ares, KKR, etc., institutions managing over a trillion dollars in assets), launched on three chains, and partnered with Plume and R2 for promotion, but response was lukewarm, with no viable path to recovery within the existing financial runway.

West denied allegations of fraud, emphasizing that Warbler Labs contributed $7 million from its own pocket to repay depositors, returned over $1 million in revenue for repayments, and sold over $2 million worth of GFI for the same purpose. He stated that he personally lost money in V1 stage trades and emphasized that "average crypto investors don't actually want private credit products."

Regarding this project, former Cross River Bank employee Ramneek Ahluwalia offered his assessment, stating that Goldfinch essentially issued loans against physical assets like motorcycles in countries with weak governance and no credit systems. The team had impressive resumes but lacked actual lending experience. Technology cannot replace the core judgment in credit assessment regarding repayment ability, collateral, and borrower quality. He had issued the same warning as early as October 2023.

Starting from Coinbase, Using DeFi to Lend in Emerging Markets

Goldfinch was founded by Mike Sall and Blake West in 2020, both with backgrounds at Coinbase. Sall previously worked on data science at Coinbase and Earn.com, while West was part of the engineering team at Coinbase. The two left Coinbase at the end of 2019, subsequently established the development company Warbler Labs to incubate the Goldfinch protocol, which officially launched in 2021.

The protocol's core model was to channel crypto capital (USDC) through a two-tier structure of Backers and the Senior Pool to off-chain credit companies, which then issued real loans to small businesses and consumers in 18 countries like Nigeria, Kenya, and Southeast Asia. Collateral was held offline by borrowers locally, and the protocol promised depositors around 10% APY. This narrative was highly attractive in 2021, aiming to serve markets underserved by traditional banks using on-chain transparency and global liquidity.

In terms of funding, Goldfinch completed three rounds totaling $37.7 million. In February 2021, it completed an undisclosed amount seed round. In June of the same year, a16z led an $11 million Series A. In January 2022, a16z led another $25 million follow-on financing round, with participation from hedge fund manager Bill Ackman, Coinbase Ventures, BlockTower, Kingsway Capital, SV Angel, and Bain Capital. a16z general partner Arianna Simpson emphasized in the investment announcement that Goldfinch's outstanding loans had reached $38 million at the time, highlighting the enormous global demand for capital.

$100 Million in Loans, Three Major Defaults

Since launch, the protocol has issued approximately $100 million in loans, covering over 200,000 borrowers. However, starting in the second half of 2021, default events occurred one after another.

- Tugende Kenya, a Kenyan motorcycle taxi financing company, received a $5 million loan from Goldfinch in October 2021 but later transferred $1.9 million of it to its struggling Ugandan parent company without authorization, constituting a contract breach. The loan was written down, with partial recovery after restructuring.

- Stratos, a US credit fund, received a $20 million funding facility. According to a governance forum update in October 2023, among Stratos's three underlying investments, real estate tech company REZI and blockchain project POKT were highly likely to be worthless, resulting in approximately $7 million in impairments. Warbler Labs committed to covering these losses for Senior Pool investors.

- Lend East, a Singapore-based borrower, received a loan of $10.15 million. In April 2024, Lend East informed Warbler Labs that it could only repay $4.25 million, with the remaining $5.9 million in default, representing a 58% principal loss rate. Sall stated in the governance forum that this shortfall was inconsistent with all prior communications from the borrower and far exceeded expectations.

The three major defaults resulted in cumulative losses exceeding $18 million.

The Dilemma of the RWA Credit Sector

Goldfinch's failure is not an isolated case. Between 2021 and 2022, a batch of RWA lending protocols, with the core thesis that DeFi could scale the intermediation of real-world credit, attracted significant crypto capital.

A common weakness of this model is that while the transparency and programmability of on-chain capital address liquidity issues, the core risks of credit business lie off-chain, including borrower qualification assessment, collateral valuation, and legal recourse after default. In emerging markets with weak legal systems and difficult asset recovery, these off-chain risks are further amplified. In a similar case, Centrifuge encountered about $5.8 million in loan delinquencies in 2023, primarily concentrated in a French consumer microloan pool, ultimately resolved through liquidation and litigation.

For RWA credit projects still in operation, the key lesson from the Goldfinch case is that on-chain tools can reduce the cost of capital pooling and distribution but cannot replace professional credit underwriting, offline due diligence, and legal enforcement capabilities. When these elements are missing, the technological infrastructure itself cannot prevent loans from turning into bad debt.