Author: Oluwapelumi Adejumo

Compiled by: Saoirse, Foresight News

Key Highlights

- As Bitcoin prices continue to decline, the crypto industry is experiencing a wave of layoffs, yet the total value of M&A deals in the first half of 2026 reached $9.37 billion.

- Major banks, payment networks, and asset management institutions are opting to directly acquire licenses, custody services, and payment channels rather than building related systems from scratch.

- Market resources are clearly diverging: valuations of struggling companies holding crypto treasury assets have plummeted, while pure decentralized finance sectors are being neglected.

The prolonged decline in Bitcoin prices has forced crypto companies to conduct large-scale layoffs, push for automation, and shelve expansion plans from the previous bull market. However, at the same time, industry M&A activity is experiencing an unprecedented boom.

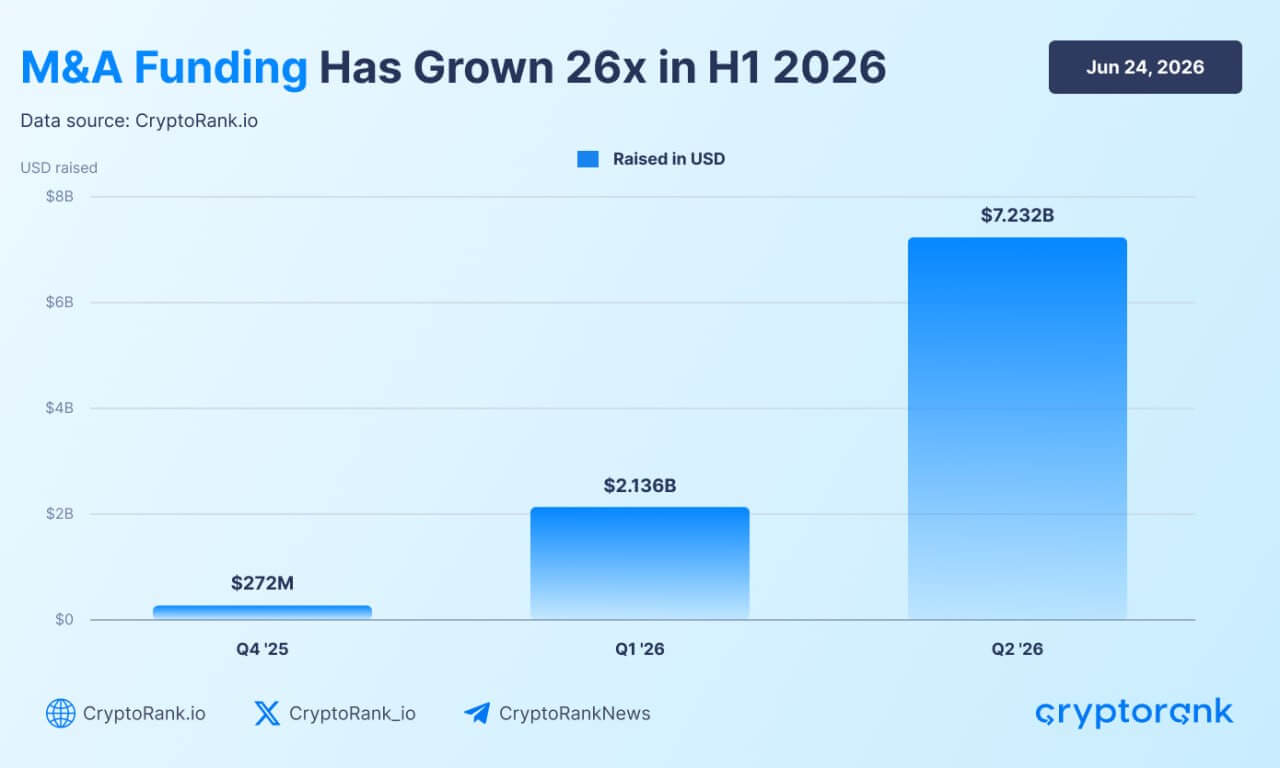

In the second quarter of 2026, the scale of crypto industry M&A deals reached $7.23 billion, far exceeding the $2.14 billion in the first quarter. The cumulative transaction investment across the two quarters totaled $9.37 billion. Data from the crypto platform CryptoRank shows that M&A volume in the first half of this year surged 26 times compared to the same period last year, clearly indicating that despite the weak spot market, industry M&A activity is heating up dramatically.

Growth in Cryptocurrency M&A (Source: Cryptorank)

This wave of M&A boom is happening against the backdrop of Bitcoin prices falling to nearly two-year lows and multiple leading industry companies continuing to downsize their workforce. These two phenomena form a stark contrast, clearly showing the shift in capital flow during the bear market: companies are no longer hiring massively or expanding blindly. Instead, traditional financial institutions and leading crypto companies with ample funds are acquiring payment systems, compliance licenses, custody facilities, and other industry infrastructure that would otherwise take years to build independently.

This has created a unique situation: the bear market has severely impacted many crypto companies, but institutional capital's demand for blockchain-related technology has not disappeared.

Traditional Finance Makes Major Moves to Acquire Crypto Infrastructure

Traditional financial institutions are the core driving force behind this wave of crypto acquisitions. They prefer to directly acquire mature, comprehensive digital asset infrastructure rather than build compliant systems and technological frameworks from the ground up.

Banks, payment service providers, and fintech companies are all targeting startups that already possess custody solutions, payment channels, and compliance qualifications. The gradual implementation of stable global regulatory policies is the core driver of this acquisition wave: the EU's MiCA establishes unified licensing standards, and stablecoin-related legislation is advancing in the US, giving large enterprises the confidence to make long-term plans in the crypto sector.

Professionals in the legal and consulting industries indicate that policy refinement is a key catalyst for this round of M&A. The first-quarter crypto M&A and financing report from Architect Partners points out that the banking and securities industries have fully embraced blockchain technology, reshaping it into the foundational layer of traditional financial markets.

Mastercard's $1.8 billion acquisition of the stablecoin company BVNK is a typical case. This acquisition gives the payment giant direct access to stablecoin payment technology and global compliance licenses, saving several years of independent R&D.

Other Wall Street giants are also seizing first-mover advantage through targeted investments: Intercontinental Exchange has invested in the prediction market platform Polymarket, Citadel Securities has invested in the brokerage services provider Alpaca, and the venture capital fund of Standard Chartered Bank has invested in the market maker Keyrock.

Asset management institutions are also capturing institutional client demand through full acquisitions. Franklin Templeton, with assets under management of $1.7 trillion, recently established a dedicated digital asset division, Franklin Crypto. This division landed by acquiring 250 Digital, integrating its investment research team with crypto active management products previously operated under CoinFund, directly providing crypto asset management services to Franklin Templeton's global clients.

Overall, private capital highly favors companies that can bridge blockchain with the traditional financial system. First-quarter financing data shows that funds are concentrated on real-world applications of stablecoins, such as foreign exchange, corporate payroll, and cross-border settlements, rather than on native crypto projects with stronger speculative attributes.

In the current market environment, compliance qualifications have become a core competitive barrier. Companies holding brokerage licenses, federal bank charters, or registered investment advisor qualifications (such as Alpaca, Anchorage, Superstate) are highly sought after by buyers, as acquirers can directly obtain legal operational qualifications.

While traditional finance is aggressively acquiring with substantial funds, various underlying public blockchains have also become active acquirers. In the past, Layer 1 and Layer 2 chains relied on external developers to build applications on-chain; now, with fierce competition for users in the public chain space, major chains are beginning to directly acquire consumer-facing application products.

Polygon's recent acquisitions of Coinme and the Sequence wallet exemplify this shift. By acquiring payment gateways and wallet infrastructure, this public chain has built a complete end-to-end user ecosystem, locking in on-chain transaction volume and proving that relying solely on underlying technology is no longer enough to maintain market share.

Crypto Industry Layoffs Continue to Intensify, AI and Compliance Reshape Talent Demand

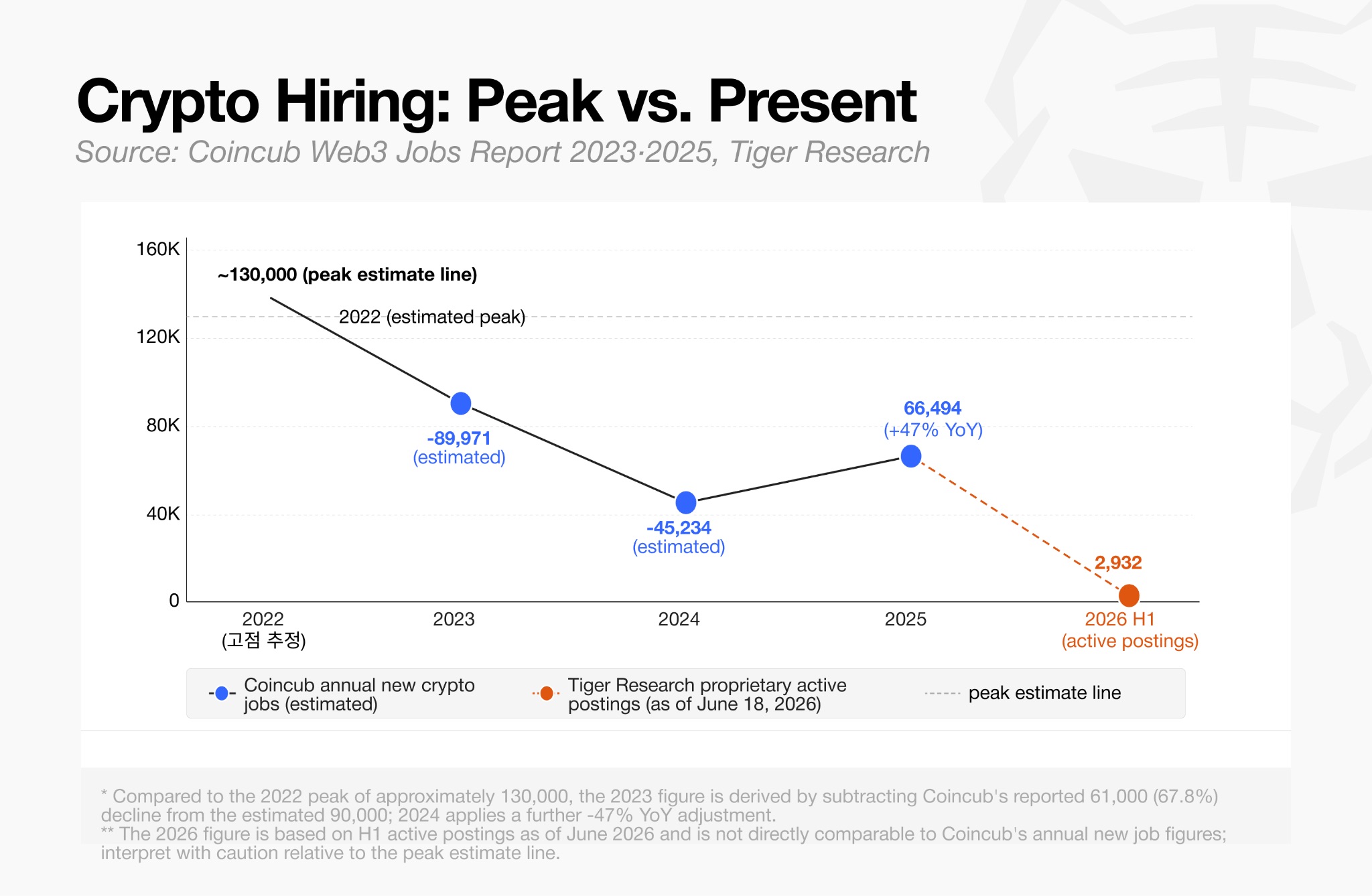

The vigorous corporate M&A activity forms a sharp contrast with the continuously contracting job market in the digital asset industry. According to Tiger Research data from June 2026, there are currently only 2,932 active job openings in the global crypto industry.

Decline in Cryptocurrency Hiring (Source: Tiger Research)

This figure is far from the hiring boom during the bull market from 2021 to early 2022, when major exchanges, DeFi protocols, and NFT platforms were simultaneously expanding. The industry's layoff wave began during the market downturn in 2022 and intensified after the FTX collapse. The total number of crypto jobs in North America and Europe shrank by about 40% and has not recovered to previous levels since.

In the first half of 2026, corporate downsizing continues. Gemini, Coinbase, Kraken, Algorand, Crypto.com, and recently the Ethereum Foundation have all initiated new rounds of layoffs.

Corporate executives state that layoffs are primarily due to low token prices and macroeconomic pressures, with AI-driven operational efficiency improvements also being a significant factor. Coinbase explicitly defines its organizational restructuring as a transition to an "AI-native operating model."

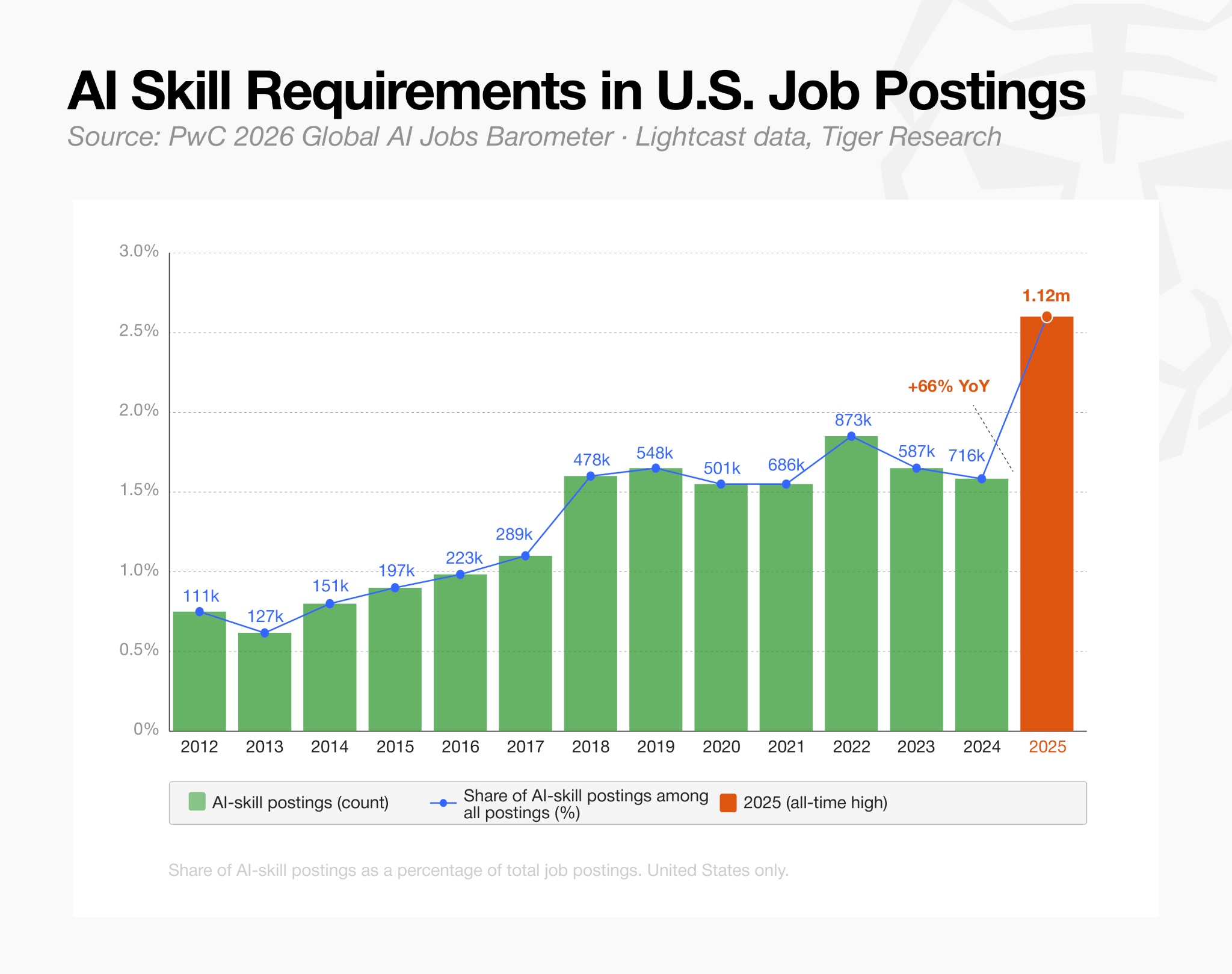

The change in talent demand is directly reflected in job postings: the proportion of crypto positions requiring AI-related skills has doubled in a year, rising from 23% in early 2025 to 53% in March 2026.

AI Skill Requirements for Cryptocurrency Positions (Source: Tiger Research)

Although overall hiring is sluggish, the industry's talent structure has fundamentally changed: companies are not freezing all hiring but are highly concentrating recruitment efforts on technical and compliance roles.

Tiger Research data shows that technical development roles account for 34% of all hiring demand, while legal/compliance roles account for 10%. Compliance positions at centralized exchanges make up 16% of total hiring, more than double the number of marketing and business development roles.

This indicates that companies prioritize retaining personnel involved in license applications, risk control, and core infrastructure maintenance, while significantly cutting spending on marketing, community operations, and similar functions.

The few remaining hiring opportunities are highly concentrated at leading companies rather than distributed among startups. Centralized exchanges provide nearly one-third of industry positions. Job numbers in the stablecoin and payment sectors are also considerable, but resources are highly concentrated: just two companies, Tether and Ripple, account for 80% of the hiring demand in this sector.

Overall data reflects that industry companies are generally conducting targeted organizational adjustments and adopting defensive operational strategies, with no signs of a broad-based recovery in industry employment.

Struggling Crypto Companies Become Acquisition Targets

The acquisition of data firm Messari by Blockworks perfectly illustrates the concurrent situation of large-scale layoffs and industry consolidation. The crypto analytics service provider Blockworks acquired Messari for approximately $10 million, while Messari's valuation reached $300 million after a funding round in 2022, now suffering a significant devaluation. Prior to this sale, Messari had undergone three rounds of layoffs since 2023.

The暴跌 in valuation reflects the harsh reality faced by crypto startups relying on venture capital, advertising, and subscription revenue. Persistent cash flow pressure and weak revenue growth force many small and medium-sized enterprises to actively seek mergers and acquisitions, allowing well-funded buyers to acquire professional talent, exclusive data, and traffic channels at low prices.

Industry analysts predict that financial pressure will soon spread to the crypto asset treasury sector. In 2025, shares of several listed crypto treasury companies traded above the total value of the crypto assets they held, successfully completing multiple funding rounds. However, with persistently falling token prices and weak company stock prices, many such companies now have market capitalizations lower than the actual value of their crypto holdings, making it difficult to continue accumulating crypto assets through stock issuance.

Galaxy Digital's research team suggests that industry consolidation is a viable path for such companies. High-quality treasury companies, like Michael Saylor's Strategy, could acquire peers at low prices, consolidate balance sheets, and simultaneously acquire profitable operating businesses to reduce reliance on a single factor—token price appreciation.

Meanwhile, as relevant legal frameworks gradually improve, Decentralized Autonomous Organizations (DAOs) are also expected to join the M&A wave. The state of Wyoming in the US has introduced the Decentralized Unincorporated Nonprofit Association (DUNA) legal framework, granting DAOs the legal entity status to hold off-chain assets and intellectual property. Clear governance and ownership rules enable protocol treasuries to acquire complementary software projects or specialized development teams.

However, compared to the current mainstream, compliance-focused traditional corporate M&A, acquisitions involving decentralized projects remain highly experimental.

Market Capital Has Not Dried Up, but Investment Criteria Have Become Extremely Stringent

Despite the nearly $10 billion in crypto M&A volume in the first half of 2026, capital deployment choices have become increasingly selective.

The prediction market sector is the only area not subject to stringent screening limitations. Various event trading platforms continue to receive large funding rounds, fiercely competing for mainstream market share. Reports suggest that the federally regulated trading platform Kalshi is in talks for a funding round that would value the company at $40 billion post-money, nearly double its previous valuation of $22 billion. Polymarket is also receiving massive financial backing, with both platforms continuing to vie for leadership in the prediction market.

Apart from the prediction market sector, industry investment logic has narrowed significantly. Capital is almost entirely directed towards companies that can bridge traditional finance and digital assets.

Tokenization service providers and institutional trading platforms are more likely to secure large financing rounds. These companies rely on providing compliant services to banks, brokerages, and asset managers, earning stable fees with business models unaffected by retail crypto market fluctuations. Superstate recently completed an $82.5 million funding round to expand its blockchain securities issuance business; Alpaca holds a leading position in the tokenized U.S. stocks and ETF settlement sector.

Financing trends indicate that investors are no longer backing conceptual tokenization pilot projects but are instead betting on mature, regulated financial products that are already operational.

Notably, purely decentralized finance protocols and new underlying public chains without real-world applications are completely absent from this quarter's major funding rounds.

The screening logic for capital deployment closely aligns with the overall M&A trend: market liquidity has not disappeared, but funds only flow to startups holding compliance licenses, institutional channels, and possessing genuine traditional finance application scenarios.

This bear market has essentially completed industry consolidation: companies with weak business models and lacking compliance qualifications either merge or downsize through layoffs; meanwhile, companies building compliant financial infrastructure reap the dual benefits of M&A acquisitions and investment financing.