Despite crypto adoption rising rapidly, investor sentiment is currently favoring stability over risk. The desire for a safe investment choice is increasingly evident, as evidenced by the increase in Tether [USDT] usage as the dominant form of currency throughout the entire market.

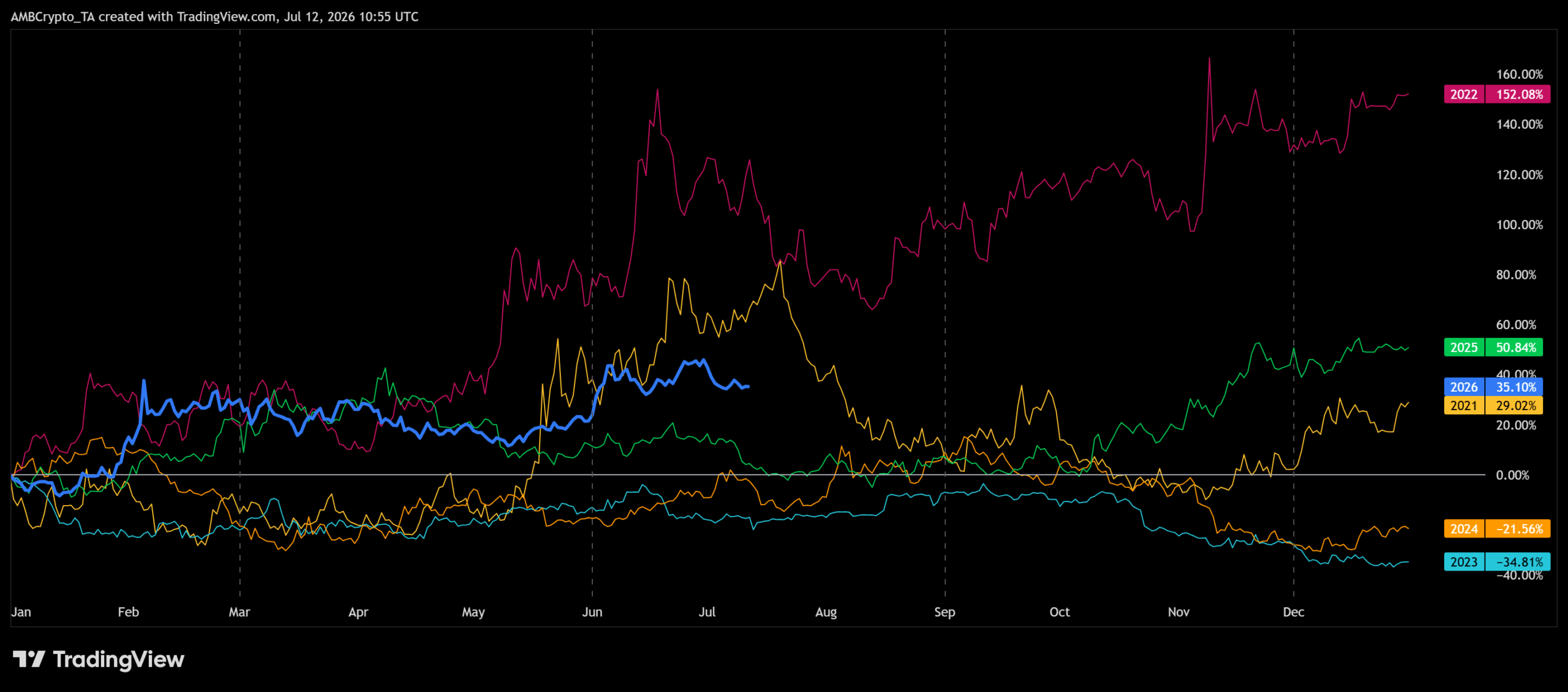

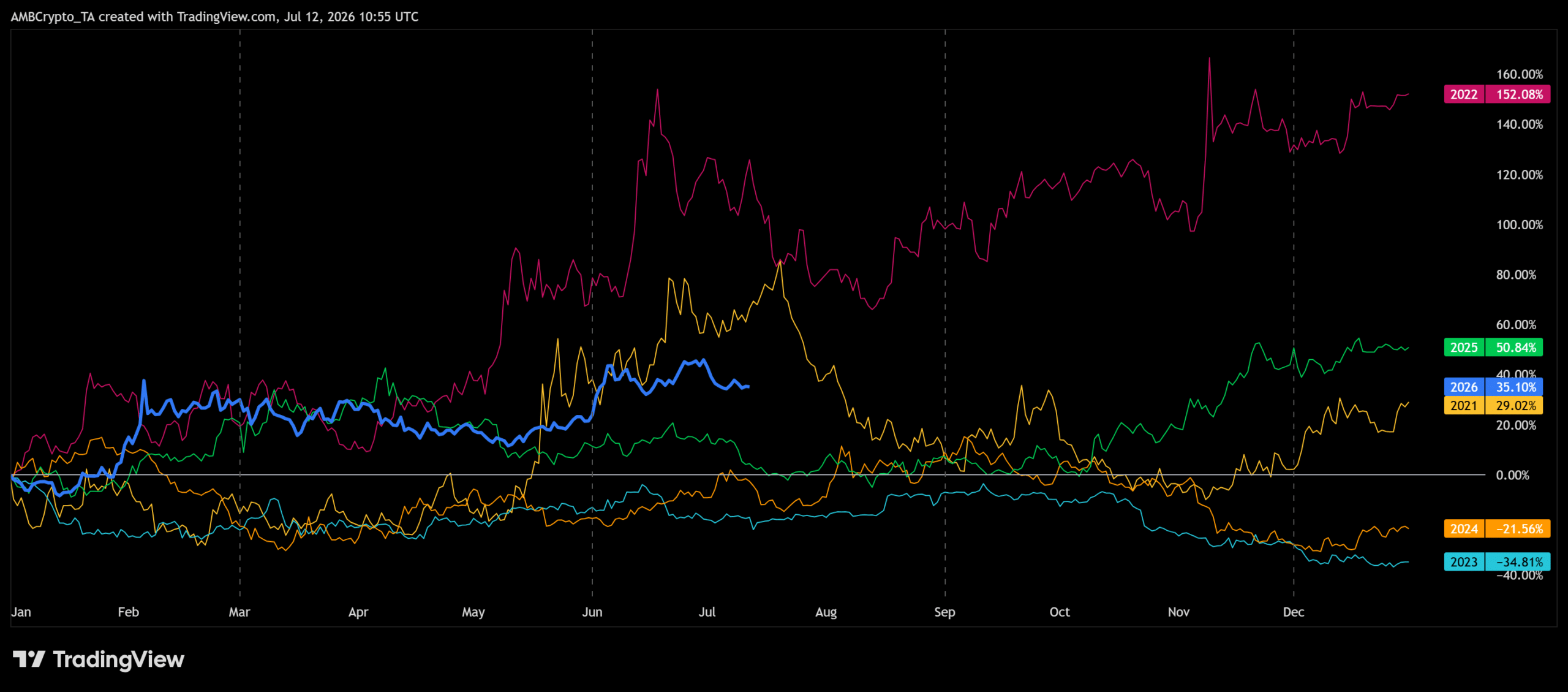

Seasonal data shows USDT usage at 35.1% by July 2026, outperforming 2021’s 29.0% in the same period.

It also stands well above 2024, during which usage remained in negative territory.

Cross-border payments drive stablecoin utility

That growing stablecoin preference is no longer reflecting caution alone. It is increasingly supporting real economic activity across blockchain networks.

As global payment firms expand stablecoin settlement, users are interacting with these assets far more frequently than in previous cycles.

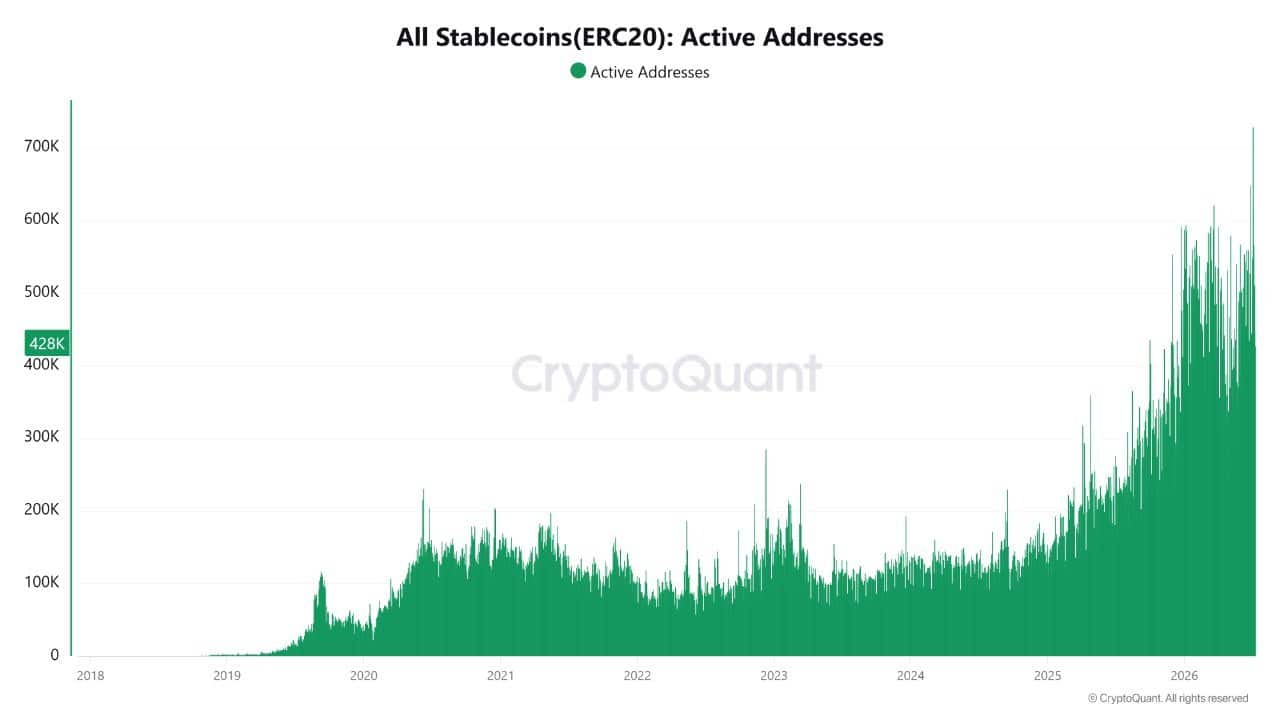

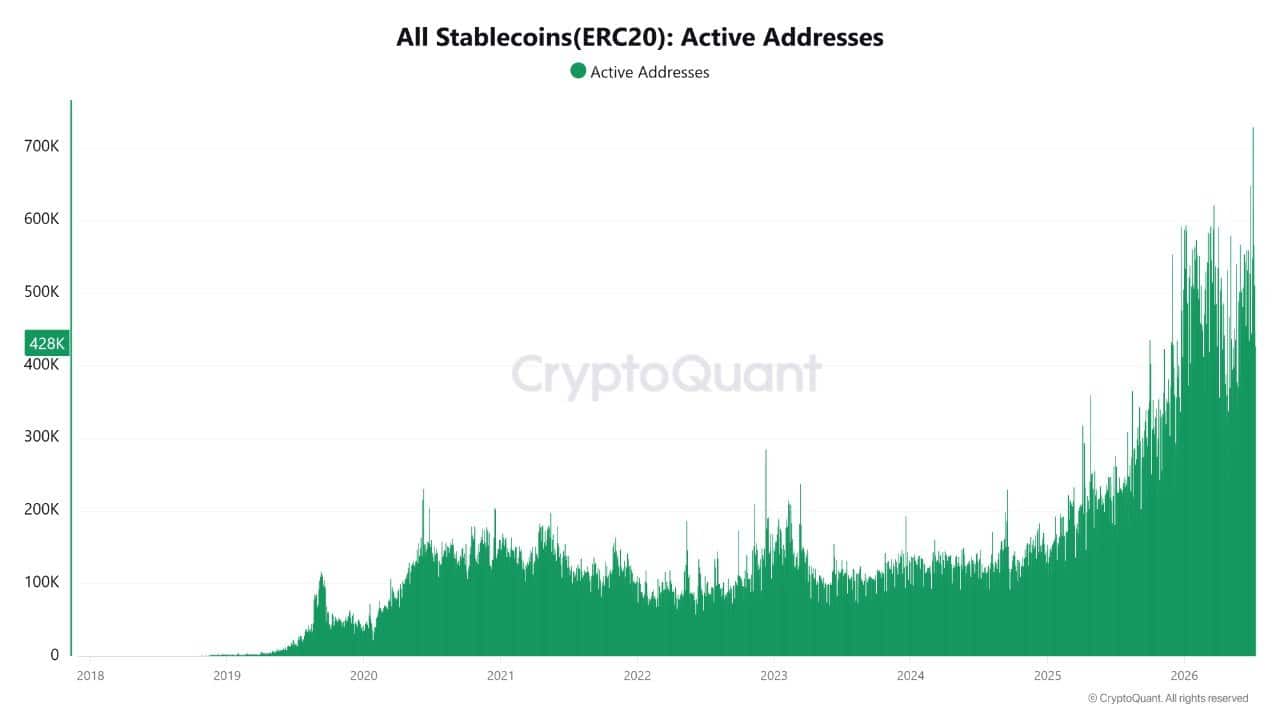

That shift is clear in the amount of ERC-20 stablecoin activity, which has increased significantly. Active addresses have surged, hovering between 400,000 and 700,000 daily since 2025.

Stablecoins are being increasingly utilized by enterprises to support their cross-border settlement processes and treasury operations. This expansion coincides with Visa, Mastercard, PayPal, and Stripe integrating stablecoins into cross-border payment infrastructure.

Meanwhile, the market has expanded to nearly $312 billion, reinforcing that demand now extends beyond crypto-native participants. If payment adoption accelerates, transaction utility could emerge as a primary growth driver.

As stablecoins gain wider acceptance in global payments, corporate adoption is beginning to strengthen blockchain’s long-term foundation.

The primary motivation for corporations to develop financial products utilizing stablecoins is no longer solely the cost savings associated with reducing settlement costs.

However, institutional investors have yet to rotate their investment into Bitcoin [BTC] or Ethereum [ETH]. This indicates continued preference by institutional investors for cost-efficient transactional outcomes versus speculative returns.

If sustained, corporates will play an increasingly pivotal role in blockchain adoption. This will be through delivering stability through real-world utility rather than cycle-driven speculation.

Final Summary

- USDT’s demand increasingly reflects payment utility alongside defensive investor positioning.

- Stablecoin adoption continues expanding as corporate integration strengthens blockchain’s long-term utility.