Author: Claude, Deep Tide TechFlow

Deep Tide Intro: Those betting on AI memory face a crucial test on June 24. Micron will announce its quarterly earnings after the market closes that day. Its stock price has soared from $103 a year ago to $1,134, roughly an 11-fold increase, with a market cap of $1.28 trillion. The market is betting on continued growth, with the Wall Street consensus expecting earnings per share (EPS) to skyrocket by about 932% year-over-year and revenue to grow by about 270% for the quarter. The higher the climb, the higher the expectations the earnings report must meet. This report is the moment to validate this bet and represents the toughest hurdle for this year's AI memory market rally.

If you hold Micron stock or are watching the AI, chip, or memory sector, this earnings report after the close on June 24 is worth paying attention to.

Micron's stock price has risen from $103 to $1,134 over the past year, an increase of about 11 times. Its market cap is $1.28 trillion, up about 297% year-to-date. At this level, anyone buying further up is certainly thinking "how much longer can this rally last?" The earnings report is the moment to validate this bet.

Currently, the market consensus remains bullish.

According to cryptobriefing, Wall Street expects Micron's EPS for this fiscal quarter to be around $19.72, compared to just $1.91 in the same period last year, a year-over-year increase of about 932%; revenue is expected to be around $34.5 billion, a year-over-year increase of about 270%. These numbers are supported by High Bandwidth Memory (HBM, specialized high-speed memory chips for AI accelerators). Micron's HBM production capacity for the full year 2026 is already completely sold out, with orders booked through the end of the year.

Analysts Have Been Revising All Year, Expectations Keep Chasing Higher

This rally didn't come out of thin air. Over the past three months, Wall Street has been consistently raising its profit forecasts for Micron, and doing so urgently.

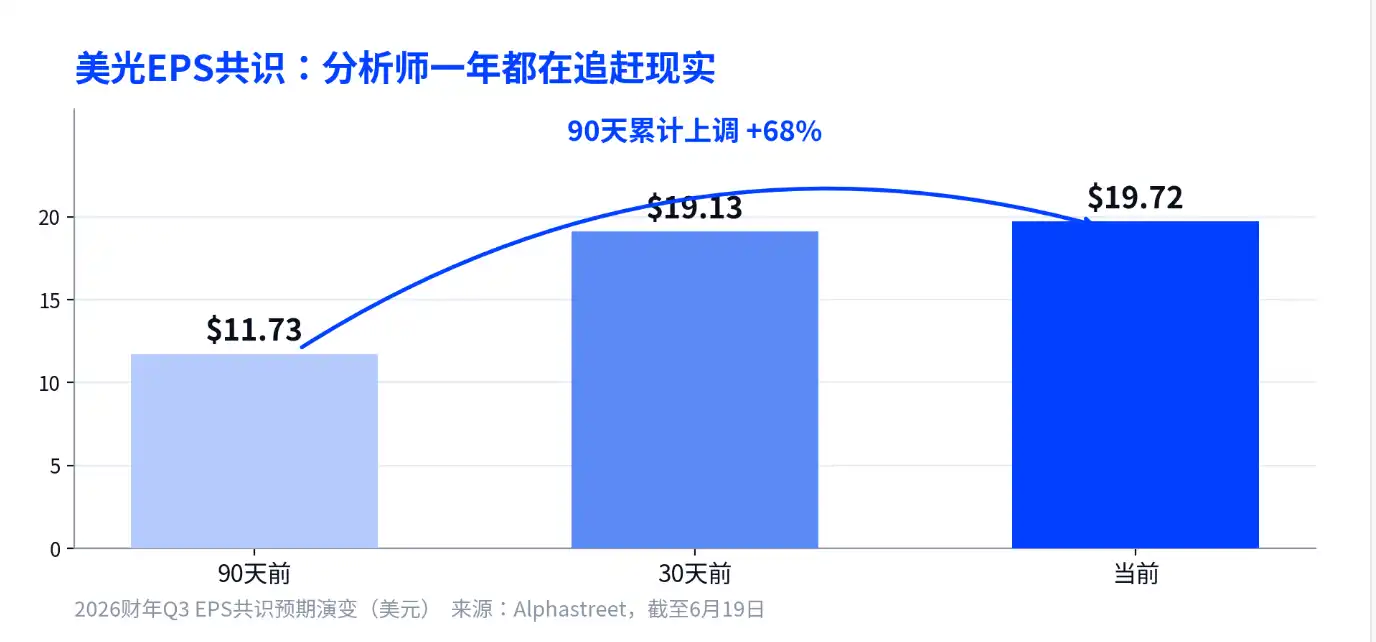

According to Alphastreet data, the consensus EPS for Micron this fiscal quarter was $11.73 90 days ago, rose to $19.13 30 days ago, and is now at $19.72, a cumulative increase of 68%. Wall Street's assessment of the company three months ago was nearly half of what it is now.

The 31 analysts' EPS forecasts range from $7.53 to $24.08, and revenue forecasts range from $19.7 billion to $40.1 billion, a huge gap. The steepness of this inflection point is something analysts themselves haven't fully figured out, forcing them to constantly revise estimates upwards based on actual data.

For the average investor, this is a double-edged signal.

Repeatedly raised expectations indicate that fundamentals are indeed exceeding expectations; but even if the earnings are good on report day, if they fall short of this pushed-to-the-limit consensus, the stock price could still fall.

Don't Believe "Citi Is Too Conservative," That's Actually One of the Most Aggressive Forecasts

There's a narrative on social platforms suggesting that Citi's assumptions on memory prices are too conservative, and that Micron's earnings will therefore significantly exceed expectations. This judgment has the direction wrong, and basing decisions on it could lead to pitfalls.

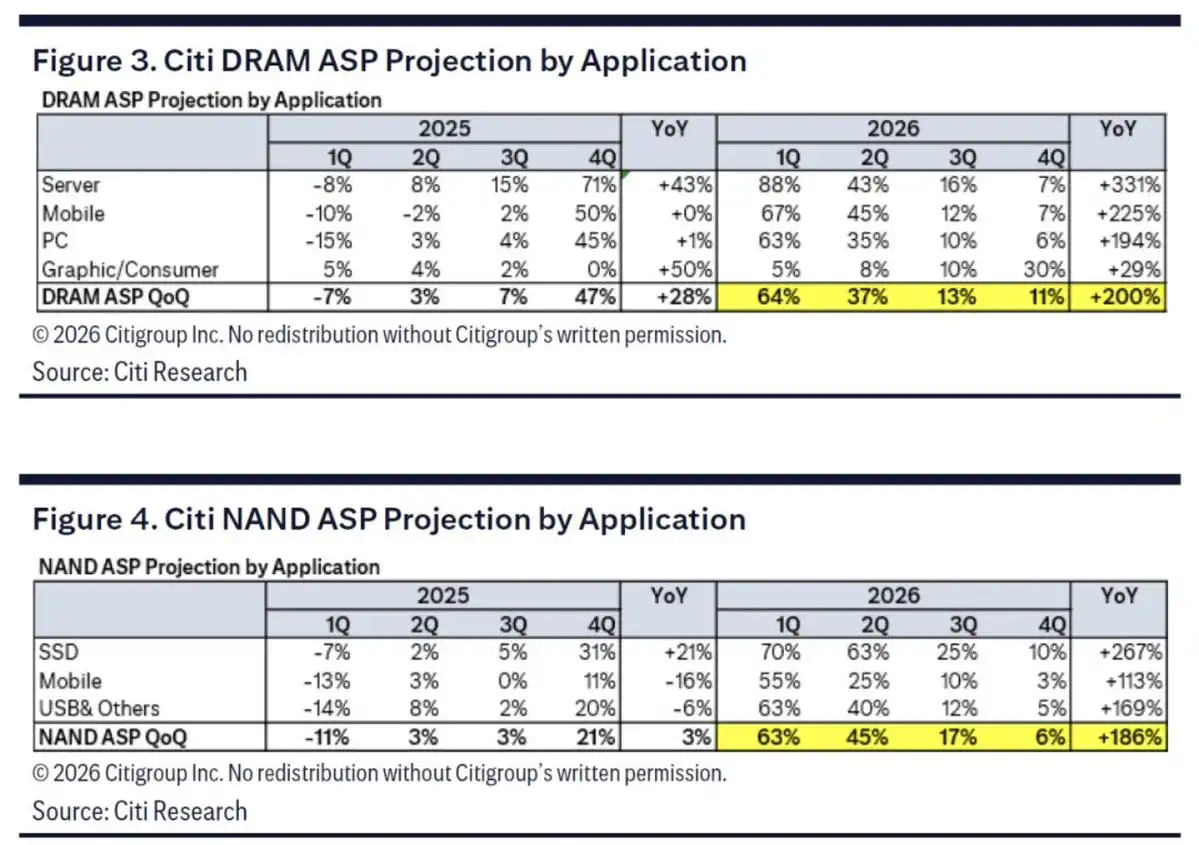

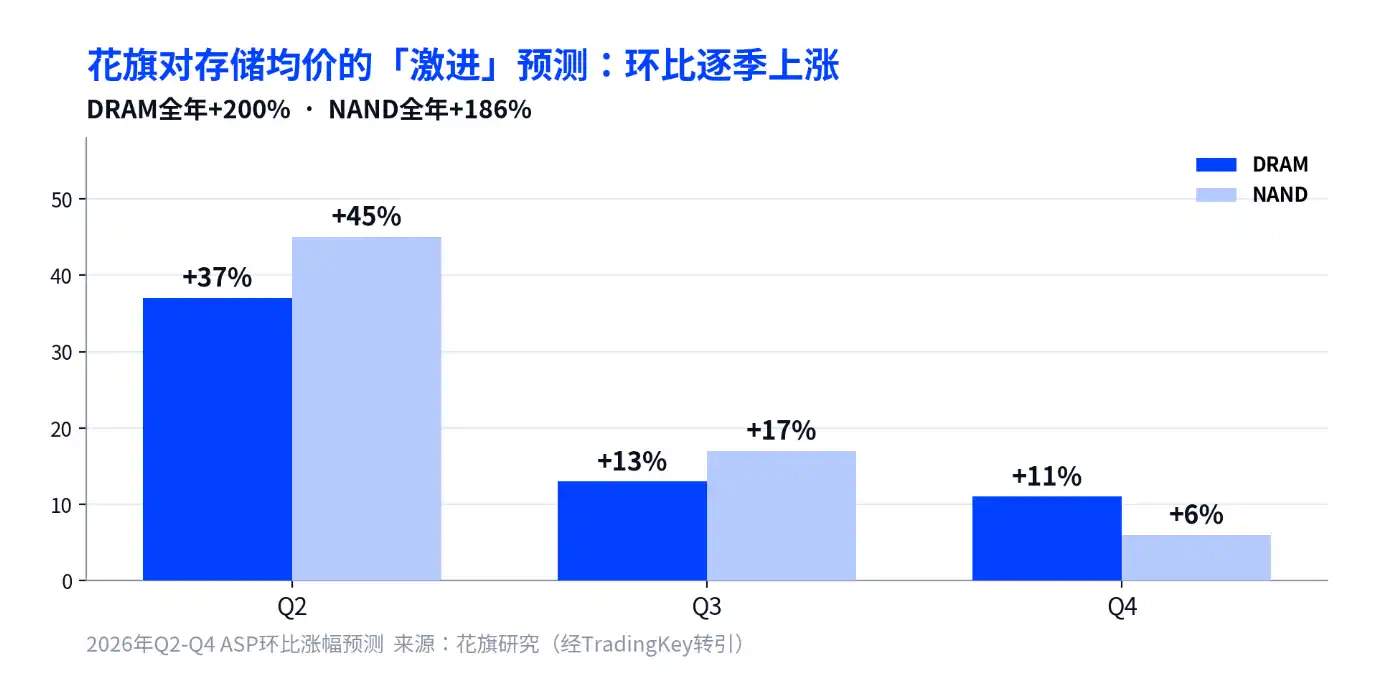

According to TradingKey, Citi forecasts DRAM average selling prices to rise about 200% for the full year 2026, with sequential increases of 37%, 13%, and 11% in Q2 to Q4, respectively; NAND flash prices to rise about 186% for the year, with sequential increases of 45%, 17%, and 6%. A 200% full-year increase is among the most aggressive forecasts on Wall Street for memory prices, not conservative. Based on this, Citi raised its price target to $1,200, while Deutsche Bank gave a target of $1,500; both extended their judgment of a memory shortage through 2028.

The risk lies here: even the most aggressive institutions have built their forecasts on "200% increases." The earnings report must surpass a bar that has already been repeatedly raised. Expecting to bet on an upside surprise based on "Citi underestimated" is not a solid logical foundation.

Gross Margin Around 81% is the Historical High, and Also the Day's Biggest Suspense

The figure to watch most closely in the earnings report is the gross margin.

According to TradingKey, Micron's own guidance is for revenue of $33.5 billion plus or minus $750 million, EPS around $19.15, and a gross margin around 81%. This is the company's highest historical gross margin and ranks among the top in the semiconductor industry. The net margin was 23.4% in the same period last year and 58.8% last quarter—more than doubling profitability in a year, a magnitude rarely seen in semiconductors.

The higher the gross margin, the more prominent the question of sustainability becomes. Micron has historically been one of the most cyclical tech stocks; everyone knows the boom and bust cycles of memory. On earnings day, any signs suggesting margins have peaked or that prices for mainstream memory categories are starting to soften, even if revenue numbers are impressive, will put pressure on the stock price.

According to TIKR, Micron's Executive Vice President of Global Operations, Manish Bhatia, said at a J.P. Morgan conference that the company's financial outlook is stronger than during the last earnings call, and this quarter is expected to set another free cash flow record; supply tightness for HBM, DRAM, and NAND will persist beyond 2026, and the ramp-up speed for HBM4 capacity is twice that of HBM3E last year. These statements are relatively optimistic, but they are all pre-earnings commentary; their truth will be verified by the day's data.

What Determines the Stock Price Direction is the Guidance, Not This Quarter's Performance

This quarter's revenue and profits are highly likely to be impressive—the market already expects that.

Which way the stock moves on the day depends more on Micron's guidance for the fourth fiscal quarter—for example, whether sequential growth can continue—that's the watershed. Next are the progress of HBM volume ramp and capacity allocation for 2027, as these two items determine whether the story for next year remains viable.

In the history of the memory industry, the easiest time to get caught is not when performance is worst, but when expectations are fullest. Micron is currently at the point of fullest expectations. If you plan to act after the earnings report, look at the guidance and HBM first, then at total revenue.