Author: Ma He, Foresight News

On June 15, the Backpack exchange token BP surged over 30% again within 24 hours, currently quoted at $0.475 with a market cap of $118.48 million and a fully diluted valuation (FDV) of $473.94 million. Since early June this year, BP has skyrocketed from around $0.16, breaking through a high of $0.48.

The direct catalyst for this market surge stems from the platform's latest breakthroughs in traditional U.S. stock brokerage and asset tokenization services.

Venturing into U.S. Stock Brokerage and Tokenization Business

In March 2026, BP completed its Token Generation Event (TGE) on Solana with a total supply of 1 billion tokens and an initial circulating supply of 250 million. After listing, the token price briefly touched a high point before rapidly declining, with a single-day drop exceeding 40% at its worst, as the market was once filled with profit-taking pressure. For several weeks thereafter, the price consolidated at lower levels until a turning point emerged in early June.

On June 2, Backpack announced the launch of the Backpack Securities platform, which will provide regulated U.S. stock brokerage services while also supporting the tokenization of traditional stocks for circulation on the blockchain, enabling seamless conversion between traditional securities and on-chain assets. The brokerage service is planned to launch gradually in June, with initial tokenized products rolled out in the Solana ecosystem through a partnership with Sunrise. BP skyrocketed over 80% in a single day, rapidly climbing from the $0.14-$0.15 range to around $0.27, with its market cap approaching $70 million at one point.

On June 12, coinciding with SpaceX's listing on NASDAQ, its tokenized product SPCX launched on Solana. In the subsequent 24 hours, BP rose approximately 27% further, pushing its price above $0.347. This token is pegged 1:1 to real SpaceX shares, supports 24/7 on-chain trading, and can be redeemed through a Backpack brokerage account into a traditional securities account, achieving interoperability between on-chain and off-chain assets. On its first day of launch, the product generated around $35-38 million in on-chain trading volume across DEXs like Jupiter and Raydium. According to the latest official data, the total on-chain SPCX trading volume exceeds $86 million.

Backpack is building a bridge between traditional U.S. stocks and Solana DeFi. Users can not only trade crypto assets within the platform but also access real stocks through the same account and tokenize portions of their assets for use, trading, or composition on-chain. This pathway aligns highly with the current RWA (Real World Assets) narrative and provides the BP token with clearer use cases and demand support.

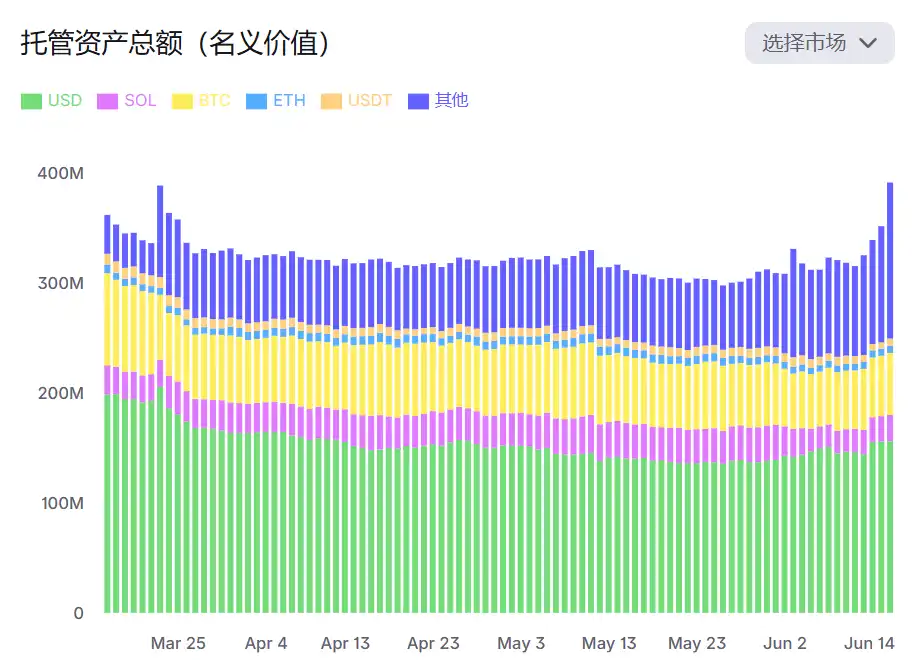

BP's recent surge stems more from substantial platform business expansion than short-term speculation. Currently, its official website shows that Backpack's total custodied assets (nominal value) have rebounded to $390 million.

No Tokens for the Team Unless the Company Goes Public

Supporting the above business development is the BP token and its unique economic structure launched as early as March. The total supply of 1 billion tokens is divided into three phases: 25% (250 million) at TGE was entirely airdropped to community users, with approximately 240 million allocated to participants in the points program and 10 million to Mad Lads NFT holders. At launch, the team, founders, and investors received 0 token allocation; 37.5% in the Pre-IPO phase is tied to growth triggers such as regulatory milestones and product launches, continuing to be distributed to users upon unlocking; 37.5% in the Post-IPO phase enters the company treasury, locked for at least one year after an IPO, with the team benefiting only through equity, not directly through tokens.

The most attention-grabbing mechanism is the equity conversion design: users who stake BP for at least 1 year gain the right to convert their tokens into company equity upon an IPO or acquisition, with the bonus increasing with holding time up to the 4th year based on the initial unlock.

Additionally, staking provides benefits such as tiered trading fee discounts, extra yield on USD collateral, free wire transfers, and priority access to the Backpack Card. Currently, about 66% (approximately 165 million) of the circulating supply is staked.

While the airdrop process was technically smooth, it also sparked community discussion. Supporters argue that the "no insider TGE allocation" model is quite radical, and the points system genuinely rewarded trading and ecosystem participation. Criticism focused on the relatively strict Sybil filtering mechanism, which led to some long-term users having their points removed, resulting in lower-than-expected allocations, as well as noticeable profit-taking during the post-listing price correction. CEO Armani Ferrante publicly denied allegations of team OTC sales.

These controversies temporarily affected market sentiment, but as tangible products like Backpack Securities were launched, the focus is gradually shifting from allocation details to the platform's long-term growth and the token's actual utility. Against the backdrop of the platform's expansion into U.S. stock brokerage and tokenization services, the long-term alignment value of BP's staking and equity mechanisms is being reevaluated.