Author: Claude, Shenchao TechFlow

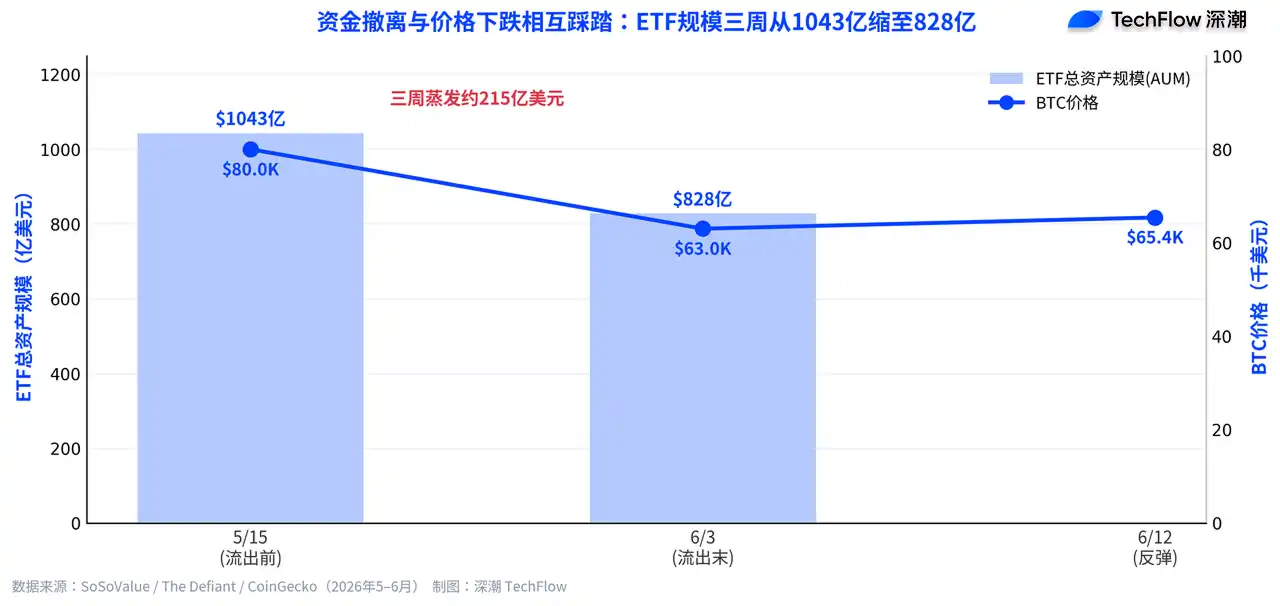

Shenchao Introduction: US spot Bitcoin ETFs have just weathered their most brutal withdrawal since listing: from May 15th to June 3rd, they experienced 13 consecutive trading days of net outflows, totaling $4.4 billion, more than double the old record set in February 2025. Combined with the drop in Bitcoin's price, the total assets under management (AUM) for these ETFs shrank from $104.3 billion to $82.8 billion over three weeks.

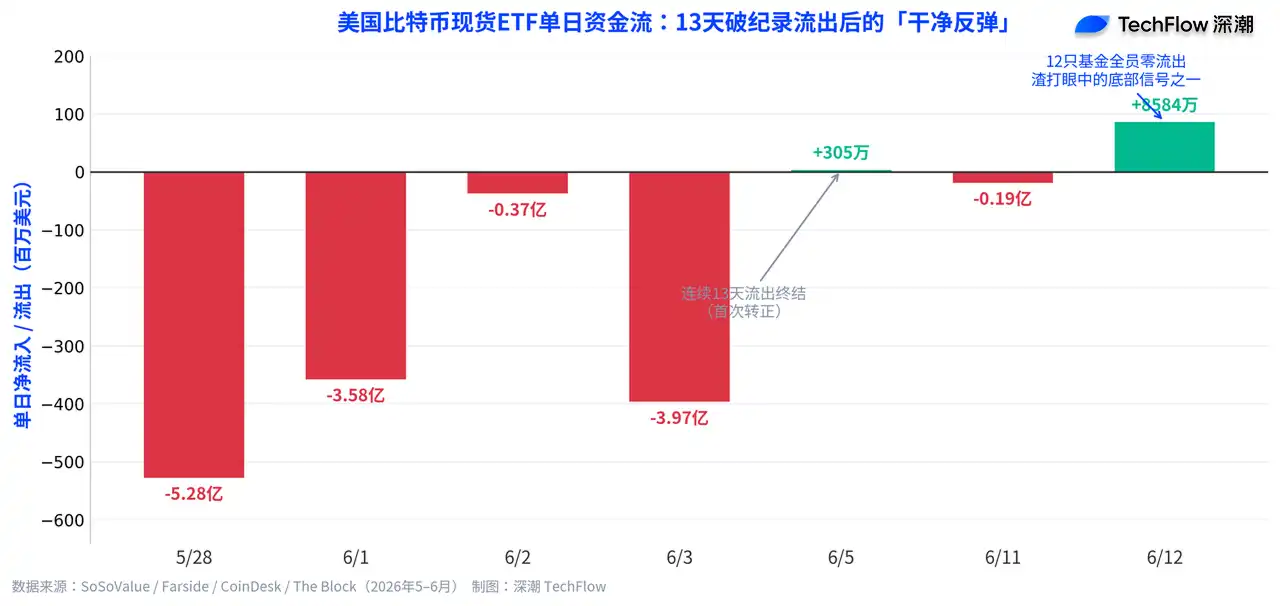

On June 12th, a turnaround signal emerged: all 12 funds saw zero outflows collectively, with a single-day net inflow of $85.84 million. Standard Chartered listed this signal as one of three pieces of evidence pointing to a Bitcoin price bottom.

13 Days, $4.4 Billion: Bitcoin ETFs End Longest Outflow Streak Since Listing

Measuring institutional sentiment towards Bitcoin, fund flows are the most direct yardstick.

These ETFs buy and sell spot Bitcoin in real-time based on investor subscriptions and redemptions. Money in and out directly corresponds to institutional position adjustments, free from the distortions of verbal statements.

Over the past month, this yardstick has revealed the worst numbers since their debut. According to Galaxy Research statistics, from May 15th to June 3rd, US spot Bitcoin ETFs saw net outflows for 13 consecutive trading days, accumulating approximately $4.37 billion, equivalent to about 59,000 BTC. This marks the longest continuous outflow streak since these products launched in January 2024. The previous record was 8 days and $3.2 billion in February 2025, a record this round more than doubled.

Galaxy Research also noted that outflow volumes across multiple time windows—7-day, 10-day, and 20-day—all hit historic highs during this period, indicating that selling pressure was not concentrated on a single day but persisted for a considerable duration. This round of withdrawals pushed the cumulative net inflows for 2026 into negative territory for the first time. Bloomberg ETF analyst Eric Balchunas confirmed that the year-to-date cumulative fund flows turned negative for the first time.

The most aggressive withdrawal came from BlackRock's IBIT. According to Farside Investors data, during the entire outflow period, IBIT alone saw outflows of about $3.3 billion, accounting for three-quarters of the total outflow. Fidelity's FBTC followed with outflows of approximately $456.6 million, and Grayscale's GBTC saw outflows of about $303.6 million. IBIT, the strongest fund in terms of attracting inflows since listing, became the epicenter of redemptions this time.

Capital Flight and Price Decline Mutually Reinforce, $21.5 Billion Evaporates in Three Weeks

The destructive force of the outflows was amplified by the simultaneous decline in Bitcoin's price.

According to The Defiant citing SoSoValue data, the total AUM of all US spot Bitcoin ETFs dropped from approximately $104.29 billion on May 15th to around $82.83 billion on June 3rd, shrinking by about $21.5 billion in three weeks. This decline stems from the combined effect of two forces: the redemptions themselves withdrawing capital, and Bitcoin's price falling from above $80,000 to around $63,000 during the same period—a drop of about 21%—causing the market value of holdings to shrink accordingly. The two factors exacerbated each other.

In terms of holdings, the ETFs' Bitcoin holdings fell to approximately 1.277 million BTC, about 7.2% lower than the peak in October 2025. These ETFs currently hold about 6.36% of Bitcoin's circulating market cap, down from over 7% in mid-May.

A particularly striking redemption occurred on May 28th. That day, BlackRock's IBIT saw a single-day net outflow of $527.8 million, the second-largest daily redemption in the fund's history. For the entire month of May, US Bitcoin ETFs recorded a monthly net outflow of $2.43 billion, setting a record for the largest monthly outflow, with the final week alone accounting for $1.42 billion.

A 'Clean Rebound' After the Outflow Ends, Standard Chartered Counts It as a Bottom Signal

The turning point arrived in early June.

On June 5th, Bitcoin ETFs ended the 13-day outflow streak with a meager net inflow of $3.05 million. While $3.05 million is almost negligible in a market of this size, the direction had changed. On the same day, Ethereum ETFs also ended a 17-day consecutive outflow streak, with a net inflow of $19.3 million, entirely from BlackRock's ETHA fund alone.

The signal truly regarded by institutions came on June 12th (Friday). According to SoSoValue data, US spot Bitcoin ETFs recorded a single-day net inflow of $85.84 million that day. Five funds saw inflows, while the other seven recorded zero net flow; none experienced net outflows. This state of "collective zero outflows" across all 12 products is a key indicator for bullish observers to gauge whether selling pressure has eased.

Geoff Kendrick, Global Head of Digital Assets Research at Standard Chartered, included it in his checklist for a Bitcoin bottom. In a brief report to clients on Friday, Kendrick stated that cryptocurrency asset prices have likely seen the low for this cycle, corresponding to a Bitcoin price around $59,000, down 53% from the $126,000 high. He said three indicators should be watched for confirmation: Strategy reportedly bought Bitcoin again last week, ETFs recorded positive inflows on Friday, and oil prices continue to decline. The report concluded with his words: "Winter is over, welcome back to crypto spring."

However, a single-day inflow of $85.84 million cannot reverse the $4.4 billion withdrawal over three weeks. But a clean trading day is the starting point for observing whether selling pressure has peaked.

ETF fund flows now exert increasing influence on Bitcoin's price. According to calculations cited by Cryptopolitan, ETF flows can currently explain about 45% of Bitcoin's weekly price volatility. The cumulative net inflows for this batch of Bitcoin ETFs since their January 2024 launch still exceed $55 billion, remaining less than $10 billion away from their historical peak. Balchunas therefore judges the $4.4 billion outflow as a significant momentum reversal, not a structural collapse.