Author: Etherealize

Compiled by: Luffy, Foresight News

History Repeats: The Cathedral Eventually Loses to the Open Bazaar

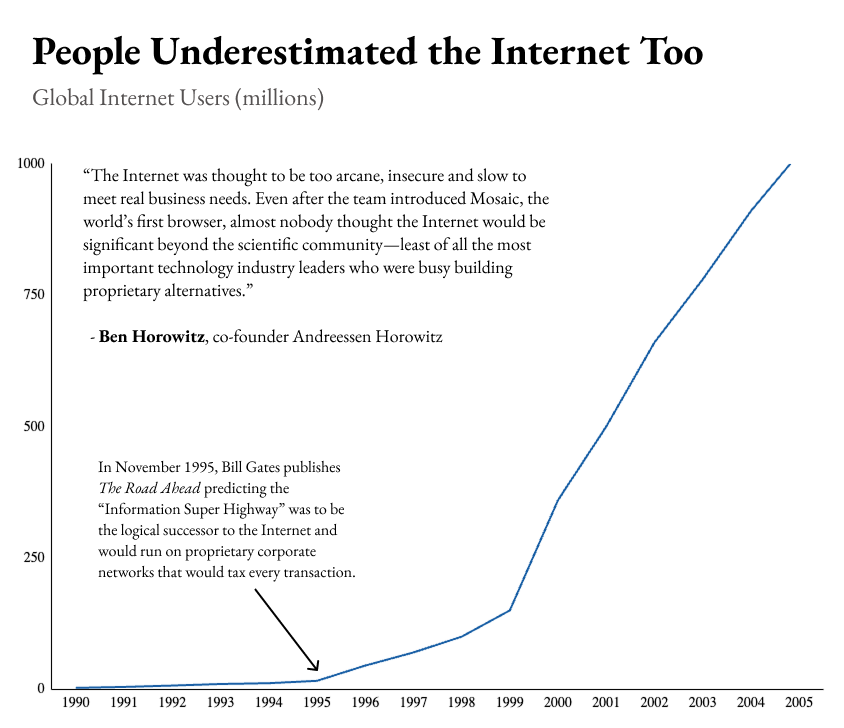

In 1995, the vast majority of tech industry authorities were convinced that the open internet would ultimately lose out to proprietary private enterprise networks. History proved them wrong, and today's skeptics of Ethereum are likely to be mistaken again for the same reasons. The most prominent figure at the time was Bill Gates, who argued in his book "The Road Ahead" that the future of digital commerce lay not with the open internet, but with private, proprietary networks controlled by companies like Microsoft and Oracle. This was the mainstream consensus in the industry. Ben Horowitz, co-founder of a16z, wrote: "Almost no one thought the internet would move beyond academia, let alone compete with the major tech giants, who at the time were all busy building their own private networks to fight against it."

Linux followed an identical path. In the late 1990s, Sun Microsystems dominated the high-end Unix server market. But by the early 2000s, cheap, generic hardware running the open-source Linux system rapidly ate away the vast majority of its business.

Today, the same historical script is playing out in the realm of financial infrastructure. Sensing both opportunity and threat, major corporations are racing to build private blockchains. In the short term, private chains appear to have the upper hand: faster transaction speeds, better user experience, and large business development teams pushing for adoption. But over time, open, credibly neutral alternatives will slowly erode their market share for two key reasons: 1) No single company can permanently keep up with the pace of innovation in a permissionless system. 2) No legitimate institution wants to build on infrastructure controlled by a competitor.

In 1997, Eric Raymond, a core Linux contributor, explained the underlying logic for the long-term victory of open, permissionless infrastructure in his essay "The Cathedral and the Bazaar." The previously accepted classic theory came from Fred Brooks's "The Mythical Man-Month": software must be developed by a single architect overseeing a small, tightly-knit team, otherwise communication costs would skyrocket exponentially. But Raymond observed that thousands of developers who had never met could simultaneously work on different modules of the Linux kernel, ultimately producing a product that dwarfed those from multi-billion dollar commercial companies. Traditional software was like a finely crafted "cathedral"; the "bazaar" was Fred's term for Linux's distributed development model: public, decentralized, and full of the chaotic, free-flowing energy of iteration. When Linus Torvalds open-sourced the kernel and accepted patches from anyone, he inadvertently pioneered this development paradigm. As Raymond put it: "Release early, release often. Delegate everything you can. Be open to the point of promiscuity." The operating system built using this model powered most internet services by the early 2000s.

Raymond explained that the bazaar model circumvented the problem of exponentially rising communication costs: developers don't need to coordinate directly with each other; everyone simply works synchronously around the code repository, interacting through patches and version updates. The project maintainer integrates all submissions to form a unified standard, which all other developers then use as a baseline. He wrote: "Brooks's law isn't repealed... but given a large enough beta-tester and co-developer base, almost every problem will be characterized quickly and the fix obvious to someone." He added that the negative effects predicted by the law were "overcome by other, nonlinear growth effects."

Raymond also pointed out that the bazaar model breaks down the barrier between users and developers. In the cathedral model, users are merely customers who report bugs to a support ticket system. In the bazaar model, users are co-builders who, upon finding a problem, either submit a fix directly or provide detailed technical descriptions for others to follow up. In the open-source community, "given enough eyeballs, all bugs are shallow." The collective effort of massive participation ultimately leads to overall efficiency surpassing any centralized competitor: "The Linux community... in many ways resembles a free market or an ecology. Many agents pursue their own self-interest, yet the combined result is a self-correcting, resilient system of astonishing complexity and efficiency, far beyond what any centralized planning could achieve."

The Ethereum ecosystem perfectly embodies this pattern. Fabian Vogelsteller, while developing a wallet, found the chaos in various token interface standards and wrote the now-ubiquitous ERC-20 standard. The NFT standard ERC-721 was born from the CryptoKitties development team. Uniswap, now the world's largest decentralized exchange, started as an idea in a Vitalik Buterin blog post, built by Hayden Adams, a mechanical engineer with no financial industry background. These individuals advanced network upgrades without needing anyone's permission. As Sun Microsystems co-founder Bill Joy famously said: "No matter who you are, most of the smartest people work for someone else." A permissionless system allows innovation to spring from anywhere.

The core distinction between the bazaar and the cathedral lies in this: the bazaar's integration layer is lightweight, completely public, and operates on credibility, not top-down authority. Core leaders like Linus Torvalds or Vitalik Buterin gain influence through the voluntary following of developers. Developers follow because core decisions are fully transparent, subject to public critique, and the community can always fork the project if necessary. The internet uses lightweight centralized coordination layers like the IETF and IANA. Wikipedia has a structured editorial review process. All projects that thrive on permissionless innovation manage to be truly open to contributions while having structured integration mechanisms to avoid the feared chaos. And the coordination layer must be maintained by credibility, not coercive control, or the system will quickly collapse.

The bazaar model also requires that the underlying infrastructure cannot be monopolized by a single entity. If Torvalds had tried to privatize the Linux kernel, developers worldwide would have immediately forked the project and continued iterating independently. Raymond refined this theory in "Homesteading the Noosphere." Open-source systems evolved rules similar to Lockean property rights: the developer who writes the initial code first gains founder ownership; continued contribution maintains that ownership; ownership is transferred through formal community succession. Open-source licenses are the formal guarantee of these rules, with community consensus as the soft constraint. If either is missing, developers will migrate to other open-source projects that won't appropriate their labor.

Ethereum's Unreplicable Core Moat

In the Ethereum community, Vitalik has summarized these underlying requirements as "credible neutrality." A coordination mechanism is credibly neutral if it possesses four characteristics simultaneously: the rules are completely transparent, apply equally to all participants, are difficult to arbitrarily change, and anyone can freely participate by following them. These four traits are distilled from mature systems like the internet, Linux, and Wikipedia that attract massive collaboration. Private networks, closed ecosystems, and enterprise blockchains all fail to meet these four points simultaneously.

Over a long enough timeline, credibly neutral systems tend to prevail: the open web replaced corporate private networks, Linux replaced proprietary Unix, Wikipedia replaced Encyclopædia Britannica. In each iteration, the private alternatives held tangible advantages: focused product positioning, strong financial backing, dedicated customer support, professional marketing, and business development teams. But as the open ecosystem matures, these advantages erode, and network effects completely reverse. Once an open system accumulates enough developer tools, applications, and credibility, establishing a perception of stable, unchanging rules, closed systems can no longer compete.

This development pattern is now permeating every layer of financial infrastructure. SWIFT, Visa, Mastercard, and the consortium chains being promoted to institutions today vary in product form and history, but share the same underlying logic: controlled by a centralized entity, harboring platform risk.

For forty years, SWIFT has been owned by member banks and should have remained neutral. But in 2012, under US pressure, it cut off Iranian banks, and in 2022, it was pressured to block several Russian financial institutions. Despite being registered in Belgium and governed by banks, SWIFT ultimately succumbed to US influence, a weakness observed globally. Subsequently, China accelerated its Cross-Border Interbank Payment System (CIPS), Russia built its own System for Transfer of Financial Messages (SPFS), India expanded its Unified Payments Interface (UPI), and Brazil's Pix became a core component of BRICS payment systems. Visa and Mastercard also started as bank cooperatives but have become toll collectors, charging merchants 1.5% to 3.5% fees. Current consortium chains (Canton, Tempo, Arc, etc.) share the same fatal flaw: the interests of the platform operator can always conflict with those of developers building on top.

"The original idea of consortium chains—multiple banks, large companies building their own blockchain together—has largely failed," Vitalik explained. "Such systems combine the worst of both centralized and decentralized worlds." He noted that while the first few participating banks might seem like equal co-builders, the twentieth institution joining is essentially plugging into a system controlled by its competitors. Companies bear all the development costs of a distributed system without gaining the core value blockchains were born to provide: open composability and credible neutrality. Past failures confirm this. From 2017 to 2019, multiple bank consortia tried to rebuild trade finance on blockchain: We.trade, backed by over a dozen institutions including HSBC and Deutsche Bank, went bankrupt in 2022; Marco Polo, with over thirty banks, entered liquidation the next year; Contour followed shortly after, shutting down. The Australian Securities Exchange spent six years and roughly A$250 million building a permissioned ledger with Digital Asset (now developer of Canton), ultimately scrapping the project in 2022. In contrast, Ethereum, owned by no one, has never experienced a full network outage in over a decade, with its ecosystem continually expanding.

This is also the fundamental reason developers choose Ethereum. According to Electric Capital, over 1 million developers have participated in the Ethereum ecosystem since its inception, with 232,000 active developers in the past year alone—no other public chain comes close. Some growth comes from the standard virtuous cycle: Ethereum's concentration of development tools, industry standards, and job opportunities naturally attracts newcomers to learn and build there, which in turn attracts more tools and jobs. But developers and institutions actively choose Ethereum precisely for its extreme decentralization and credible neutrality. For example, last year Robinhood chose to build its Layer 2 on Ethereum rather than develop its own base layer. Johann Kerbrat, head of crypto at the company, stated: "Today, many companies are building their own L1 chains. We also desired the control of our own system, but building a truly secure, decentralized base layer is extremely difficult. Ethereum inherently provides this security base for free. Many new L1s aren't truly decentralized, their security is questionable, and they're essentially just slower, improved databases. We saw no core value."

Erik Voorhees, founder of the privacy-focused AI inference platform Venice AI, expressed a similar view a few days ago. The platform has over 3 million users and generates tens of millions in annual revenue. When asked why they chose to build on Base, Coinbase's Ethereum Layer 2, he said: "We didn't hesitate at all. Among all smart contract platforms, the Ethereum ecosystem is the purest, most resilient, and most mature."

The most fundamental trait of a blockchain is sovereignty. Bitcoin's revolutionary nature lies in being the world's first sovereign computing platform. Before Bitcoin, all computer systems belonged to individuals, companies, or governments and had to obey their owner's will and local laws. A sovereign system follows only its own predetermined rules; no single entity can forcibly change Bitcoin's rules. In the past, sovereignty belonged to monarchs and nations; now, for the first time, a computing platform has achieved sovereignty. This is also why decentralization is so valued in crypto: it's the only path to sovereignty. A chain with only ten validating nodes has its rules dictated by those ten entities. Ethereum, with hundreds of thousands of independent validators spread across global jurisdictions, multiple independent client implementations, and a foundation that explicitly renounces governance power, has long crossed the sovereignty threshold. No single party can claim exclusive ownership of the network. The core value of sovereignty is this: the global financial system can build applications on Ethereum, and all participants need not worry about other institutions, governments, or foundations arbitrarily changing rules to their detriment.

Global Institutions Bet on Ethereum's Open Ecosystem

Ethereum's lead in sovereignty and credible neutrality stems from a historical path dependency that other chains cannot replicate. Ethereum launched in 2015 with Proof of Work, ran for seven years, and only transitioned to Proof of Stake in 2022. Network ownership was sufficiently decentralized through a public crowd sale in 2014 and mining accessible with consumer-grade GPUs, ensuring no single entity holds a large enough token stake to control the network (a key prerequisite for sovereignty in a Proof of Stake system). Most consortium chains today are venture-backed, with tokens concentrated among founding teams, giving a few entities absolute say over consensus. Competitors can copy the technical architecture but not Ethereum's development history.

Since then, Ethereum's lead has compounded: sovereignty and credible neutrality attract developers; an influx of developers brings better libraries, tools, and job markets, further lowering the barrier to entry and attracting more practitioners; applications deposit liquidity and tokenized assets, driving institutional participation. Each layer of the ecosystem reinforces the others. Competitors must build a complete industrial chain simultaneously, while Ethereum's scale advantage continues to grow with compound interest.

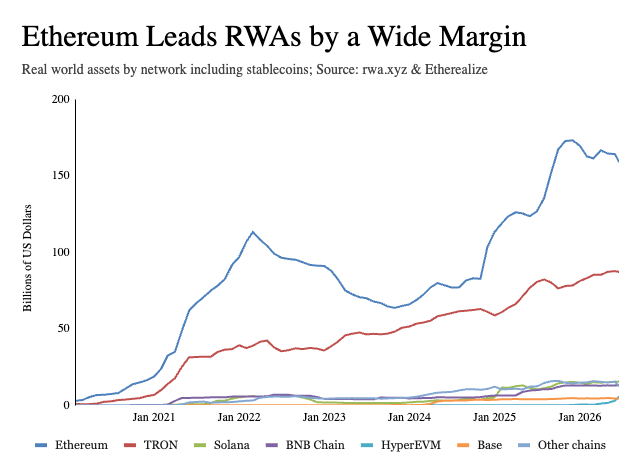

The industry's most sophisticated players are already betting on Ethereum: Coinbase and Robinhood built their Layer 2s on Ethereum; BlackRock and JPMorgan launched tokenized money market funds BUIDL and MONY, both on Ethereum; leading DeFi protocols like Aave, Maker/Sky, Maple, and Uniswap are primarily on Ethereum; the world's top stablecoin issuers settle on Ethereum. Data from Token Terminal's "Q1 2026 Ethereum Industry Report" shows: among the top five public chains, Ethereum hosts 79% of active DeFi lending, 62% of stablecoin issuance, 73% of tokenized funds, and 84% of tokenized commodity assets.

Ethereum's applications are also permissionless, further amplifying its advantages. For example, Uniswap's permissionless listing mechanism gives pricing and liquidity to thousands of long-tail assets, a service centralized exchanges would never provide. Aave's open and highly composable lending markets have spawned an entire ecosystem of specialized pools and risk management tools, far exceeding what the core team alone could develop. Closed systems require platform operators to anticipate all use cases in advance; open systems do not.

The most potent counter-argument to the thesis that "permissionless systems will ultimately win" is not technical but relates to the specific nature of finance: privately controlled networks might be an advantage, not a defect, for the financial industry. When payments fail or funds flow abnormally, regulators need a clear responsible entity; "no one in charge" sounds more like a huge risk than an advantage in a legal context. But this criticism confuses two completely separate layers: accountability mechanisms are built at the application layer; the settlement layer does not need to bear this function. For instance, the ERC-3643 token standard directly embeds KYC verification and cross-border transfer restrictions into smart contracts; issuers can set wallet whitelists, restrict asset transfers, freeze, or recover tokens. Privacy technologies work similarly; zero-knowledge proofs allow institutions to settle on a public chain while hiding transaction details. In contrast, on consortium chains, transaction data is visible only to the company itself and its competitors.

In the early days of the internet, it was widely believed its security was insufficient for commercial transactions. After the HTTPS protocol enhanced security capabilities, most commercial activity migrated to the open web, and such skepticism vanished. The skeptics back then weren't wrong about the internet's early flaws, but they underestimated the self-evolving potential of open networks.

Today, banks and fintech companies building private chains are repeating the mistakes of AOL and Microsoft: trying to replicate an open system but building a walled garden, extracting rent through platform control. This model is doomed to fail. The walls built to exert control also block out external innovation.

Netscape is the model for success. Netscape never tried to monopolize the internet; it built a browser to guide global users onto the open network. Riding the explosive growth of the internet, Netscape became a defining company of its era. Ethereum, with its almost unreplicable credible neutrality, already possesses the potential to become the global settlement layer for finance. The optimal industry strategy is to build applications on top of permissionless infrastructure, not to compete with it head-on.