Author: CryptoSlate

Compiled by: Deep Tide TechFlow

Deep Tide's Guide: This article clarifies a structural issue that is easily overlooked: Bitcoin ETFs are not a floor; they are conditional buyers. Five weeks of net outflows totaling $3.8 billion are not just an ugly number; they represent the quiet closing of what was once the most stable institutional door at the peak of tariff uncertainty. After February 20th, the data reversed, but is this reversal a true signal or a tactical move? The author outlines three paths and four indicators to watch, making it worth a careful read.

Full Text Below:

Bitcoin ETFs have just experienced their longest net outflow cycle since early 2025. The uncertainty surrounding tariff policy is stirring interest rates and the stock market, making this outflow particularly critical as it alters Bitcoin's support structure under pressure.

For nearly two years, spot Bitcoin ETFs were almost seen as a one-way street. They liberated Bitcoin from the hassles of private keys and operational complexities, turning it into code that fits into any ordinary investment portfolio. Money flowed in, shares were created, and Bitcoin gained a stable, compliant source of demand.

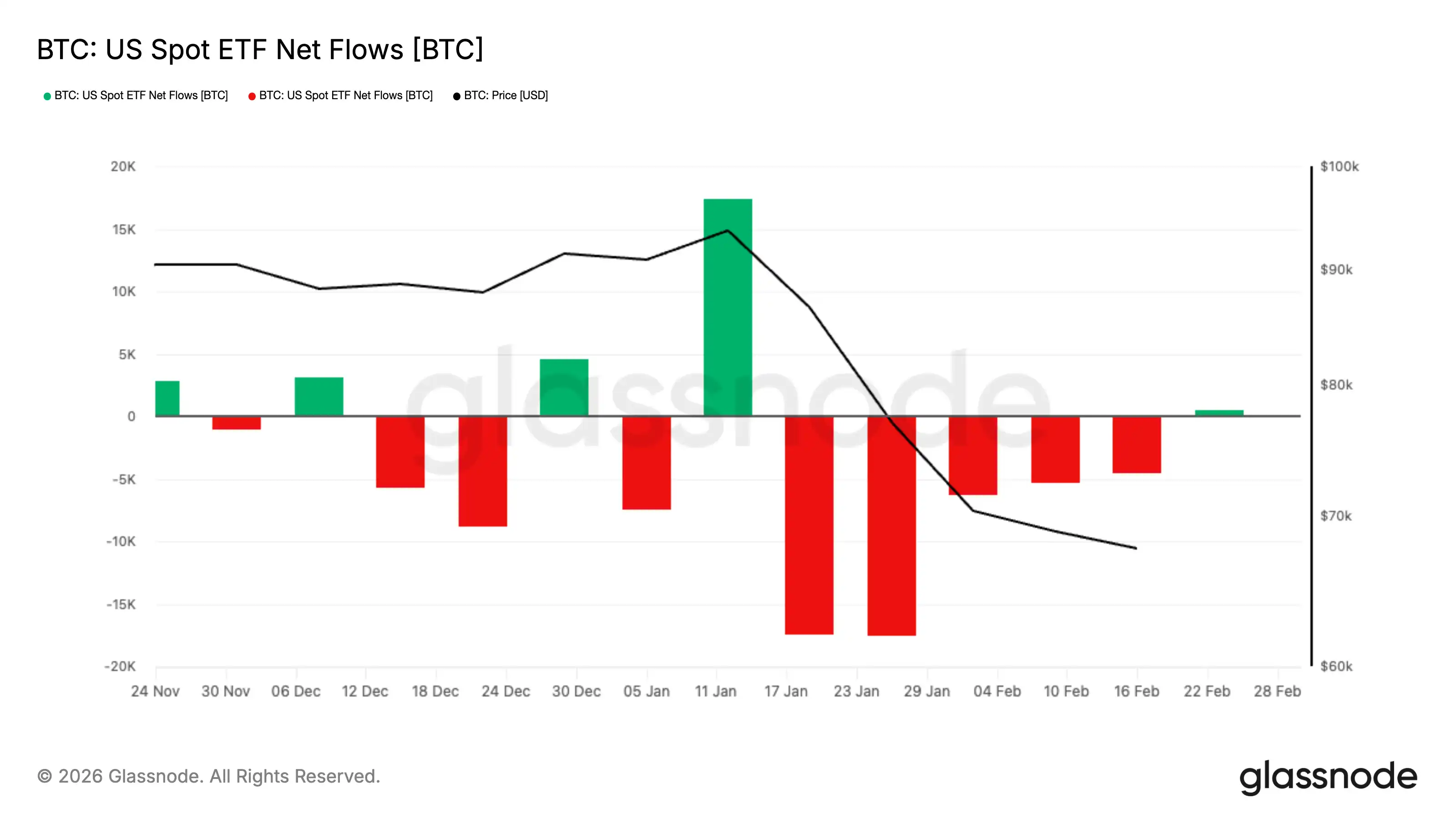

In the five consecutive weeks leading up to the end of February, investors withdrew approximately $3.8 billion from U.S.-listed spot Bitcoin ETFs, marking the longest streak of weekly net outflows since early 2025. Bitcoin mostly hovered around $60,000 during this period, with recent trading prices around $68,000 as the market attempts to regain balance.

The scale of this outflow is staggering, but the timing is even more critical. The outflow period coincided with tariff policy uncertainty seeping into interest rates, stocks, and commodities, making the entire macro environment jittery again.

However, since February 20th, the flow of funds has at least temporarily shifted.

Between February 20th and 27th, U.S.-listed spot Bitcoin ETFs recorded approximately $875.5 million in net inflows, with strong share creation on multiple consecutive days. This is not enough to erase the losses of the past five weeks, but it complicates the narrative.

What initially seemed like a one-way de-risking cycle may be turning into a reset—institutional demand is cautiously re-emerging amid ongoing macro uncertainty.

What Have ETFs Actually Done to the Bitcoin Market?

Spot ETFs operate through a share creation and redemption mechanism. When demand for ETF shares rises, authorized participants create new shares by injecting assets into the fund. When demand wanes and shares are redeemed, the mechanism contracts. This process connects the buying and selling activity in the stock market with Bitcoin exposure behind the scenes, which is why ETF flows serve as a daily scorecard for Bitcoin.

The SEC approved rules allowing certain crypto ETP shares to be created and redeemed in-kind, meaning authorized participants can exchange the underlying asset for shares directly without routing everything through cash. The SEC's focus was on efficiency and cost reduction.

But even if daily execution remains primarily cash-based, the core logic remains unchanged: ETF flows are one of the cleanest bridges between institutions and the Bitcoin market.

A simple framework to understand:

On net inflow days, the ETF expands, shares are created, and exposure grows. The market feels the presence of a buyer that doesn’t require a new catalyst every day.

On net outflow days, the ETF contracts, shares are redeemed, and exposure shrinks. The market loses that default buyer and must also absorb additional selling pressure.

How Are Five Consecutive Weeks Different from a Single Week of Large Outflows?

The cumulative withdrawal of approximately $3.8 billion over five weeks marks a record duration for weekly net outflows in the recent cycle. Such a prolonged streak of weekly net outflows has not been seen since early 2025. The macro backdrop adds extra weight to this.

Trade policy is once again impacting crypto markets. Tariff uncertainty creates a headline-driven environment where sudden repricing in one asset quickly spills over into others.

In such conditions, portfolios are managed more conservatively. When volatility rises, fund managers quickly cut positions that can be cut easily, forming a negative feedback loop that further depresses prices and exacerbates outflows. They often revisit the assets they cut later, but this does little to calm the outflows.

Whether one admits it or not, Bitcoin falls into the "quick to cut" bucket, and ETF flows are one of the first places this decision becomes visible.

Another comparison looming over this period is gold. Gold has gained safe-haven demand due to tariff uncertainty, with recent dollar weakness and geopolitical risks only amplifying this demand.

But this doesn’t mean Bitcoin has failed in this cycle. The market is clearly categorizing assets by behavior, and Bitcoin is trading more like risk exposure than a safe haven.

When ETF Buying Stops, Who Replaces It?

To understand this, set aside grand narratives and ask one simple question:

When Bitcoin drops 3% in a day, who becomes the buyer that doesn’t need convincing?

In 2024, ETFs gave the market a clear answer. Net inflows were the default demand. They didn’t need leverage, memes, or perfect sentiment—just a committee decision and broker execution.

But when this channel narrows, two specific things happen.

First, declines feel lonelier.

Without consistent ETF net inflows, price discovery relies more on active spot buyers and liquidity providers who require higher compensation to take the other side. This is why pullbacks feel sharper and rebounds feel more hesitant, even if the news doesn’t seem dramatic.

Second, net outflows can bring real market force.

Redemptions are not just a reflection of market sentiment; they are a mechanical contraction of institutional positions. Depending on the product structure and how participants hedge, redemptions can translate into actual Bitcoin sales, hedge adjustments, or basis trade unwinding.

The external result is the same: less support, more supply, weaker bounces.

We can attribute Bitcoin’s poor performance to an overall cooling of U.S. institutional participation and say that ETF net outflows and lighter overall positioning in regulated venues exacerbated this. You may disagree with the tone of this characterization, but it aligns with what the ETF data shows.

This shatters a misconception: ETFs are Bitcoin’s floor. A floor requires a consistently buying buyer. A buyer that steps away for five consecutive weeks was always a conditional buyer.

What to Watch?

To fully grasp the implications, watch four signals and understand what each means.

Watch the weekly net flow data. A single week turning positive is a pulse; two or three consecutive weeks indicate the channel reopening. If weekly data turns consistently positive, it means institutional money pipelines are reopening. If it slips back into sustained negative territory, rebounds may feel like climbing without a handrail, as the cleanest institutional money pipeline is still contracting.

Watch Bitcoin’s performance on macro-negative days. In tariff-driven markets, stocks swing with headlines, rates repricing, and volatility spikes. At such times, Bitcoin either holds up like a scarce asset or trades like risk beta.

Watch if the price can rise without ETF net inflows. If Bitcoin starts climbing while ETF flows are flat or negative, it means another type of buyer has taken the baton. Sometimes it’s derivative position resetting; other times, it’s crypto-native spot demand returning. Either way, that’s the moment it no longer relies solely on ETFs.

Watch the pattern of outflows. A slow drip is different from a sudden gush. A slow drip is position trimming; a sudden gush usually signals forced selling or rapid de-risking.

None of this predicts price, but it tells you whether the market’s biggest demand engine is running, idling, or reversing.

What’s Next?

The answer is no longer as one-directional as it was a week ago.

Five consecutive weeks and $3.8 billion in net outflows marked a clear contraction in institutional positioning. But the data since February 20th introduces a new variable: approximately $875.5 million in net inflows in just over a week.

This doesn’t negate the prior de-risking, but it does suggest the institutional money pipeline isn’t broken—it may have just undergone a stress test.

There are three realistic paths now.

The first is confirmation. If net inflows persist for multiple weeks and begin to stack steadily, these five weeks of outflows will look more like a position reset than a structural exit. In this scenario, ETFs resume functioning as a stable allocation channel, Bitcoin performs better under macro pressure, and recent volatility is reclassified as a shakeout rather than a demand collapse.

The second is fragility. A brief inflow rebound followed by a return to net outflows means last week’s share creation was tactical, not strategic—fast money reacting to price levels, not long-term capital rebuilding positions. If this happens, rebounds may continue to feel heavy, especially in a macro environment where fund managers are tariff-sensitive and quick to cut risk.

The third is stability without acceleration. Flows flatten near zero, extremes on both ends fade, Bitcoin trades in a compressed range, and positions quietly rebuild. This sideways repair may be less dramatic but is often more constructive, as it removes forced flows from the equation and returns price discovery to normal.

The key shift is this: the market is no longer facing one-directional, sustained ETF outflows. It is now testing whether the institutional demand engine is restarting.

The $3.8 billion outflow is eye-catching. But the more important question today is: has the marginal buyer returned, and are these buyers early allocators rebuilding positions, or just traders standing in front of what they perceive as a floor?

ETF flows don’t predict price. But they will continue to show whether Bitcoin’s cleanest institutional buying is expanding, idling, or sliding toward reversal again. And when macro uncertainty makes markets jittery once more, this pipeline matters most.