Author: Gino Matos, CryptoSlate

Compiled by: TechFlow

TechFlow Introduction: Strategy has publicly stated it may sell Bitcoin to pay dividends, MARA sold 15,000 BTC to repay debt, and Sequans used Bitcoin to pay off convertible bonds for two consecutive quarters. The "never sell" narrative of Bitcoin treasuries is collapsing, as these companies transform Bitcoin from a "belief reserve" into a "liquidity tool." When falling prices trigger more selling, and selling further depresses prices, a spiral begins.

Saylor Softens His Stance: Selling Can Be More Cost-Effective Than Issuing Shares

During Strategy's earnings call on May 5, CEO Phong Le stated directly: "We will sell Bitcoin when it is beneficial for the company." Saylor added: Strategy might sell some Bitcoin to pay dividends, "to let the market get used to this idea."

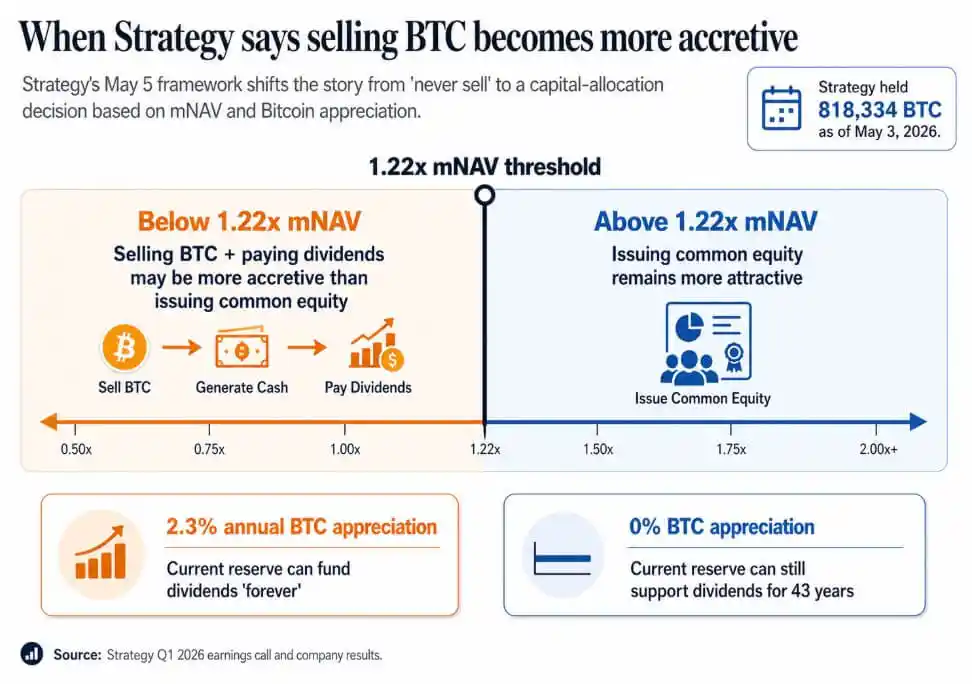

As of May 3, Strategy holds 818,334 BTC, a 22% increase year-to-date, with a market value of $64.14 billion.

This call officially established one thing: BTC selling behavior has been formally incorporated into the company's financial toolkit, backed by a quantitative framework.

Management drew a line—when the mNAV (market cap/net asset value) falls below 1.22 times, selling Bitcoin to pay dividends enhances per-share value more than issuing common stock. According to Saylor's calculation: as long as Bitcoin's annualized appreciation exceeds 2.3%, Strategy's existing Bitcoin reserves can pay dividends "forever"; even if Bitcoin appreciation is zero, the reserves are sufficient for 43 years.

Caption: Illustration of Strategy's 1.22x mNAV threshold—when mNAV falls below this line, selling Bitcoin for dividends is more beneficial to shareholders than issuing stock.

The slogan "never sell" has given way to a model: buy when it enhances value, issue shares when it enhances value, issue preferred shares when it enhances value, and sell Bitcoin when it enhances value. These companies are essentially leveraged treasuries + credit vehicles.

Investors who bought these stocks initially purchased a Bitcoin proxy built on scarcity and a promise of permanent holding. The 1.22x mNAV threshold and the 2.3% break-even appreciation rate represent a more honest version, and a more complex one.

When Bitcoin Becomes Working Capital

Sequans' Q1 report is more straightforward. Revenue fell 24.8% year-over-year to $6.1 million, with an operating loss of $50.5 million. The net realized loss from selling Bitcoin in Q1 was $11.7 million, with proceeds mainly used to repay convertible bonds and repurchase ADS.

As of March 31, Sequans held 1,514 BTC, of which 1,217 BTC served as collateral for $66.2 million in convertible bonds. By April 30, holdings decreased to 1,114 BTC, with 817 BTC securing $35.9 million in debt (due June 1).

This mirrors the operation from November 2025—when Sequans sold 970 BTC, redeeming 50% of its convertible bonds, reducing debt from $189 million to $94.5 million.

For two consecutive quarters, the same pattern: declining revenue, maturing debt, Bitcoin becoming operational working capital. The BTC used as collateral was locked into debt obligations long before any active selling decision.

Sequans is not in the same league as Strategy—its underlying business is weaker, and its treasury position is more fragile. When Bitcoin must be used to repay debt, the logic of "inventory management" takes over.

MARA did the same in March, on a larger scale—selling 15,133 BTC, cashing out approximately $1.1 billion to repurchase convertible notes, slashing 30% of its convertible bond balance at once, and locking in a spread gain of about $88.1 million.

MARA framed this move as "balance sheet optimization," driven by debt structure and financing conditions. This establishes a precedent: BTC selling can be a capital allocation decision independent of Bitcoin belief. The real question is—under what conditions is selling the highest-return choice?

The Bull-Bear Fork: Financing Conditions Determine Everything

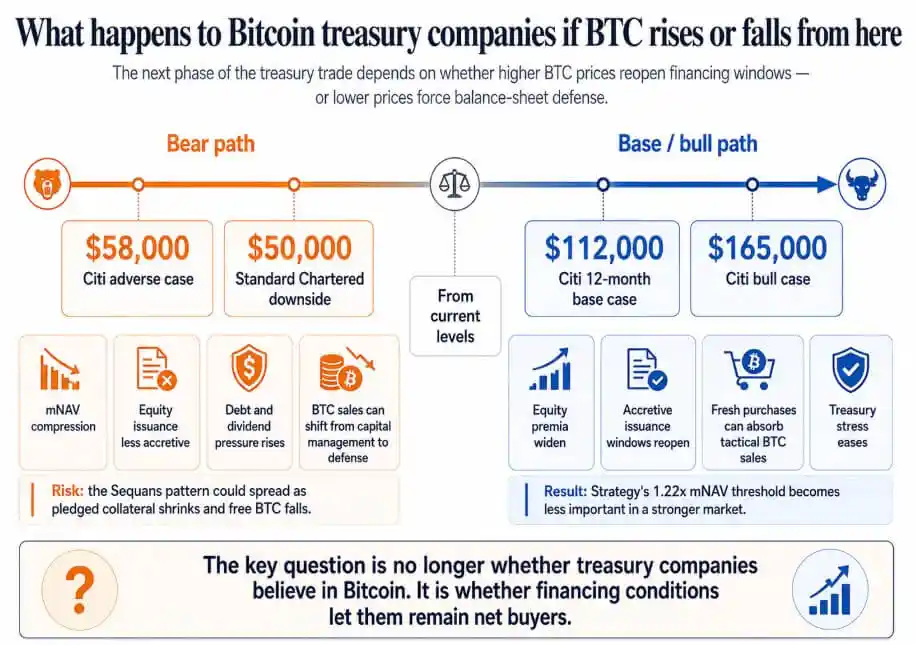

If Bitcoin rebounds to Citi's 12-month base case target of $112,000 or the bull case target of $165,000, the equity premium of treasury companies will expand, the window for share issuance will reopen, and large new purchases will be sufficient to absorb tactical BTC sales.

Strategy's 1.22x mNAV threshold would become a technical detail. Companies like Sequans, facing debt pressure during Bitcoin's weak periods, could also resolve their debt issues and enter the next cycle with unrestricted BTC.

If Bitcoin falls toward Citi's adverse scenario of $58,000 (Standard Chartered has hinted at a further drop to $50,000), companies trading near or below NAV will lose the value-enhancing effect of issuing shares.

In such a scenario, dividend obligations on preferred shares accumulate, and BTC selling transitions from capital management to balance sheet defense. Sequans' model could spread to all treasury companies with "thin-margin operations + BTC-collateralized borrowing"—selling Bitcoin to repay debt, shrinking collateral, and reducing free float becoming the only option.

At that point, corporate Bitcoin buying becomes a vicious cycle: falling prices trigger more selling, and more selling depresses prices.

Caption: Two paths for Bitcoin treasury companies—under a bear market scenario ($50,000-$58,000), they face balance sheet pressure; under a bull market scenario (above $112,000), financing pressure eases.

The corporate Bitcoin treasury trade was built on the promise of "permanent holding," which led investors to price these companies as Bitcoin proxies. Once selling becomes an openly acknowledged tool in the model, investors must factor debt maturities, collateral requirements, dividend obligations, and the mNAV level at which management would choose to sell Bitcoin rather than issue shares into their pricing.

Saylor's 2.3% annualized break-even and 1.22x mNAV threshold are more honest. In the next phase of the Bitcoin treasury trade, the weight of financing conditions will not be lower than that of Bitcoin belief.