注:原文作者为 Jeff Morris Jr,Chapter One 的创始人,是 Dapper Labs、Compound Finance、The Graph、Dharma Labs(收购 OpenSea)的种子投资者。Chapter One 是一家由红杉资本、马克·安德森和克里斯·迪克森支持的早期基金。

”“

Twitter 和加密货币的关系一直很尴尬。加密社区喜欢在 Twitter 上聊天,但 Twitter 的领导层似乎并不关心。

“”

自比特币诞生,哈尔·芬尼于 2009 年 1 月 10 日首次发帖提及比特币以来,Twitter 一直是加密货币行业最重要的信息分发渠道。哈尔以收到中本聪的第一笔比特币交易而闻名,并且是比特币代码的首批贡献者之一。他在推文中言简意赅:“运行比特币。”

哈尔的这条推文是在杰克·多尔西担任 Twitter 首席执行官的第一个任期(2006-2008 )之后不久,也是在埃文·威廉姆斯接任 Twitter 首席执行官时期(2008-2010 )发布的。

“”

在 16 年间多次更换 CEO(迪克·科斯特罗、杰克·多尔西的第二任期、帕拉格·阿格拉瓦尔、埃隆·马斯克)之后,Twitter 并没有认真对待加密货币和 Web3。

“”

为了进行研究,我与熟悉 Twitter 发展路线图、埃隆对加密货币的立场的 Twitter 内部人士进行了交谈,他们确认埃隆领导下的现任 Twitter 领导层并不关心加密货币,因为这与他们的核心产品无关。

“”

这就是现实。

“”

大约 2 年前,Twitter 似乎终于意识到它忽视了一个价值数万亿美元却极度依赖其平台的行业的事实。尽管如此,Twitter 依然无法在产品层面对加密社区做出回应。

“”

2021 年 Twitter 在内部建立了一个由苔丝·里尼尔森领导的加密货币团队,但这种情况却在 2022 年熊市发生了变化。据报道,该团队已经解散,里尼尔森也于 2022 年 11 月离开了公司。

“”

自 2013 年 11 月以 26 美元的价格公开上市以来,Twitter 的股票一直在挣扎,尽管其他“消费者互联网资产”(包括加密货币)的关注度都有所增长,但该公司从未想出如何在广告收入之外进行扩张。

“”

当我还是社交平台 Tinder 的副总裁时,我在 2017 年被一位高级产品主管邀请到 Twitter 进行友好访问,我们谈到了为产品添加订阅。

“”

那是在“杰克·多尔西的第二任期”期间——当我们正在享用一顿丰盛的午餐时,高级产品主管告诉我,杰克永远不会允许在 Twitter 上添加订阅,因为他认为所有信息都必须免费。

“”

我虽然并不知道当时 Twitter 的发展路线图是怎样的,但杰克对商业模式的顽固让我感到震惊,因为在 Tinder,如果你有能力创造独特的价值或内容,消费者将支付订阅费用以求访问。

“”

Tinder 有 5% 的活跃用户是付费订阅者,我们的经常性收入接近 10 亿美元,而 Twitter 的月活跃用户群要大得多。

“”

为什么一家苦苦挣扎的公共消费互联网公司不考虑添加订阅?

“”

我有时思考,如果 2017 年 Twitter 更加重视经常性收入和订阅,那么这家公司今天是否会归埃隆所有?

“”

这让我想到了加密货币和 Web3。

“”

Twitter 探索的潜在货币化机会是加密货币和 Web3,尤其是在 2017 年加密货币牛市期间。

“”

对于包括 Facebook 和 Twitter 在内的所有消费互联网公司而言, 2017 年的生活都很复杂。这两个平台都在接受美国国会审查,以了解它们在俄罗斯可能干预 2016 年总统大选中的作用。

“”

由于杰克将言论自由作为重点,Twitter 当时也在垃圾邮件和滥用问题上苦苦挣扎。

“”

在 Twitter 已经脆弱的时刻,将加密货币支付添加到存在垃圾邮件和滥用问题的平台会增加欺诈等风险。一直有传言称 Twitter 可能会利用加密技术,但至今没有新产品推动这一趋势。

“”

现在是 2023 年,Twitter 产品与加密货币的关系仍然很尴尬,尽管大多数加密货币社交话语都发生在 Crypto Twitter 上。

“”

Twitter 已经成为了加密货币投资者发现早期投机机会的地方,NFT 所有者可以在这里将他们的个人资料图片更改为经过验证的无聊猿,但该公司仍没有直接从加密货币或 Web3 中获得收入。

“”

那么为什么 Crypto Twitter 不完全离开 Twitter?或者 Web3 开发者创造一种能够以更直接的方式拥抱加密社区的产品?

“”

事实上,分发很重要,而 Twitter 仍然独具分发权优势。

“”“

新的社交产品将削弱加密 Twitter 的价值,但这将需要很多年时间,而 Twitter 不会感到受威胁。

”“

但 Twitter 确实需要更多的经常性收入。那么,为什么不拥抱加密货币和 Web3,进而成为加密货币和 Web3 行业最重要的 Web2 平台,或者它至少假装关心一下呢?

”“

在埃隆的领导下,人们继续希望 Twitter 成为一家对加密货币友好的公司(他喜欢狗狗币),但埃隆早期的货币化行动主要集中在订阅上。

”“

这是在熊市中的正确优先事项,但他们的收入路线图需要更多创造力,或者做一个更好的 Twitter Blue(订阅产品)。

”“

如果你与了解 Web2 和 Web3 的聪明人交谈,他们会告诉你,最简单的货币化机会就是关注 NFT 和加密货币交易。但两者似乎都不在 Twitter 的路线图上。

”“

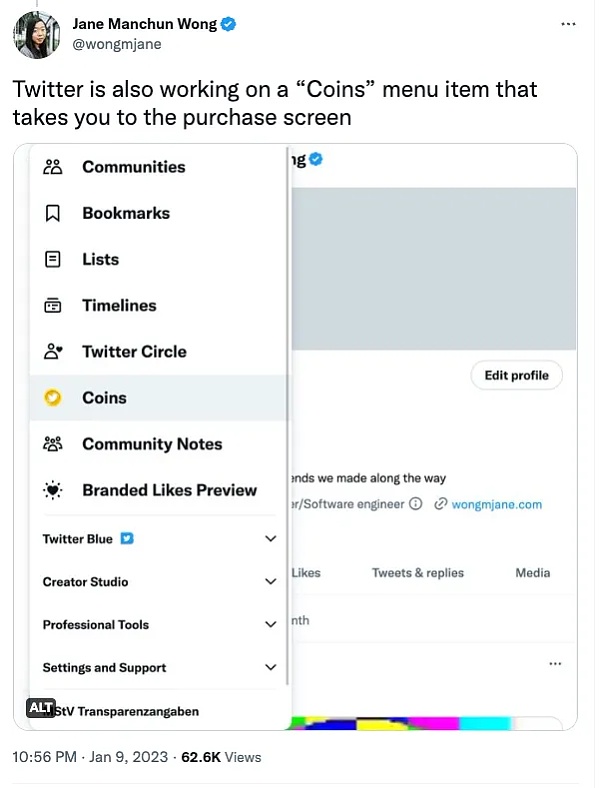

上周,Twitter 被曝出正在开发一项名为 Coins 的功能,该功能将允许用户支持平台上的创作者。尽管 Twitter Coins 将通过支付平台 Stripe 购买,Stripe 也接受加密货币作为支付方式,但这是面向创作者的产品,而不是面向加密货币的产品。

”“

2022 年 4 月,Stripe 测试了一项产品功能,该功能允许一组被选定的创作者以与美元挂钩的稳定币 USDC 接收付款。

”“

对于 Twitter Coins,用户在购买和向创作者发送时可能永远不会与 USDC 互动。

”“

USDC 可能有助于支付,但我们熟知的大多数以创作者为中心的产品都曾表示过,创作者更喜欢老式的法定货币,因此加密货币通通被 Pass 掉了。

Twitter 最近推出了一项小功能。如果你搜索加密货币或股票,你将获得价格图表和导向购买资产的链接。

”“

例如,我在 Twitter 网站上搜索 The Graph ($GRT),得到了 The Graph 的价格图表和通向 Robinhood 的链接。

需要明确的是,此功能也适用于亚马逊 ($AMZN) 等股票的搜索,因此,这并不是以加密货币为中心的产品。

”“

虽然合作伙伴关系的业务细节我们尚不清楚,但 Robinhood 链接不会对 Twitter 的直接收入产生实质性影响。Robinhood 拥有 1400 万月活跃用户,而 Twitter 的月活跃用户为 4.5 亿,因此可能只有一小部分 Twitter 用户可以在不注册 Robinhood 的情况下使用该功能。

”“

而且,这也可能与拥有 Robinhood 账户的 Crypto Twitter 用户存在重叠,所以这一功能不会对 Twitter 的收入产生重大影响。

”“

据报道,埃隆将更加迫切地希望在 2023 年找到直接收入,因为他的 130 亿美元债务的“迫在眉睫的利息支付”的第一期付款将于 1 月底到期。

”“

就在上周,The Information 分享了 Twitter 在 2023 年第一季度的收入数据:

”“

Twitter 在 2022 年第四季度的收入下降约 35% 至 10.25 亿美元。这是 Twitter 本季度内部目标的 72% 。周二晚上,Twitter 的一位高级经理告诉员工,公司在周二的每日收入比一年前的同一天下降了 40% 。

”“

对于订阅,即使你不是专家也可以明白 Twitter Blue 是半生不熟的、无法吸引主流用户的功能。

”“

然而,Twitter 还在继续提高订阅价格,现在 Twitter Blue 每月收费 11 美元。他们可能已经吸引了一小群对价格相对不敏感的订阅用户(即 Twitter 小鱼和鲸鱼)。但定价测试只会让收入团队走到这一步,如果他们继续提高价格,订阅用户会感觉受到“背叛”。

”“

也许有一天 Twitter 会拥抱并成为加密货币和 Web3 领域最具统治力的 Web2 社交公司—— 并为自 2009 年哈尔·芬尼首次发布比特币相关的推文以来一直存在于其平台上的 Web3 革命打造专属产品。

”“

但在那之前,Twitter 与加密货币已经陷入了尴尬的关系。

”“

Twitter 领导层不想与加密货币和 Web3 建立认真的关系,Crypto Twitter 也不会离开。