On Tuesday, April 7, 2026, at 19:45 GMT, nearly three hours before Trump announced a "two-week ceasefire" between the U.S. and Iran on Truth Social. This time was a vacuum period when London traders were off work and Asian traders had not yet started, typically with only a few hundred crude oil futures contracts traded per minute. Within this one hour, someone sold approximately 6,200 Brent crude oil futures contracts plus 2,400 WTI crude oil futures contracts, totaling 8,600 contracts with a notional value of about $950 million.

The next day, as the Asian market opened, crude oil prices dropped by about 15% at the open, with WTI falling below $100. According to Reuters, citing LSEG trading data, the size of this short position was "completely atypical for that time period." Representative Ritchie Torres wrote to the U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) on April 8, requesting an investigation.

This was not the first time. More precisely, it was the second recorded instance of the same "script" during this round of U.S.-Iran tensions.

The Same Trading Signature, Two Precise Entries

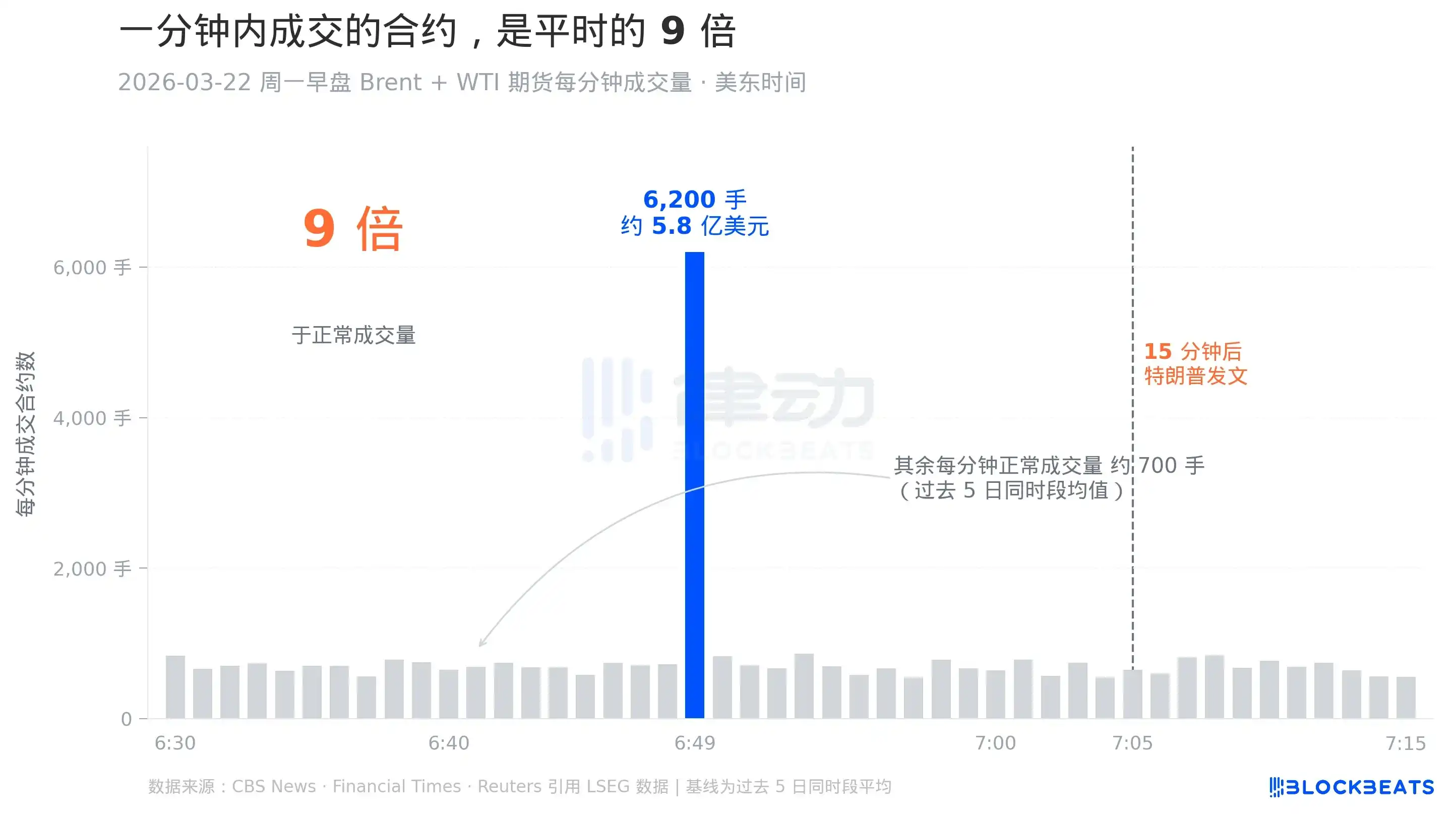

The one on the morning of Monday, March 22, 2026, was less famous than the April 7 incident because it did not trigger a significant drop in oil prices. But from a trading structure perspective, it was the prototype of this "script." According to trading data cited by CBS News and the Financial Times, between 6:49 and 6:50 AM Eastern Time that day, which was 10:49 GMT, a total of 6,200 Brent and WTI futures contracts were traded, worth approximately $580 million.

Fifteen minutes later, Trump posted on Truth Social, saying he was engaged in "constructive dialogue" with Iran and announced a five-day delay in the plan to strike Iranian energy facilities. Crude oil prices plummeted that day, the S&P 500 jumped, and the Dow Jones Industrial Average rose over 1,000 points in a single day.

Aligning the timelines of these two events reveals a detail: the "Brent leg" of the 8,600 contracts on April 7 was also exactly 6,200 contracts. The same number appearing in two completely different time periods could be a coincidence or indicate the same position size. In trading circles, this repetition is called a "signature," referring to a fixed formula used by a particular group of traders. CBS's report cited two anonymous former CFTC investigators, stating that such precise repetition is "itself an investigative signal."

9 Times the Norm, Occurring in the Unwatched Hour

Many readers who first saw this news thought 19:45 GMT was an "after-hours period." Actually, it was not. Brent crude oil futures are traded almost 24 hours electronically, closing only briefly on weekends. 19:45 GMT is a more subtle point in time. Just moments before (19:28 to 19:30 London time), the day's "settlement window" had ended—the two minutes used by the exchange to determine the official daily settlement price.

Once the settlement window ends, most European professional traders leave work. Asian trading desks in Tokyo and Singapore come online only a few hours later. This hour is typically one of the thinnest liquidity windows of the day. According to ICE's official product specification documents, Brent's true trading peaks are concentrated during European daytime hours.

Zooming in on the anomaly of that minute on March 22 provides a clearer comparison. According to LSEG transaction details cited by CBS, the normal trading volume for the same time period over the surrounding five days was about 700 contracts per minute. That minute saw 6,200 contracts traded, nearly nine times the usual volume. The long blue bar in the chart represents that minute. The other gray bars, densely packed at the bottom, represent the other minutes of the same hour.

The significance of this comparison is that the ninefold surge did not occur during the most liquid daytime hours but was concentrated in the thinnest minute of the trading book. Paul Krugman, writing about this on his Substack, used an analogy: it was like "driving a truck down an empty street in the middle of the night and honking the horn"—either not caring about being heard or having a compelling reason to act at that moment.

Three Trades in the Same Direction

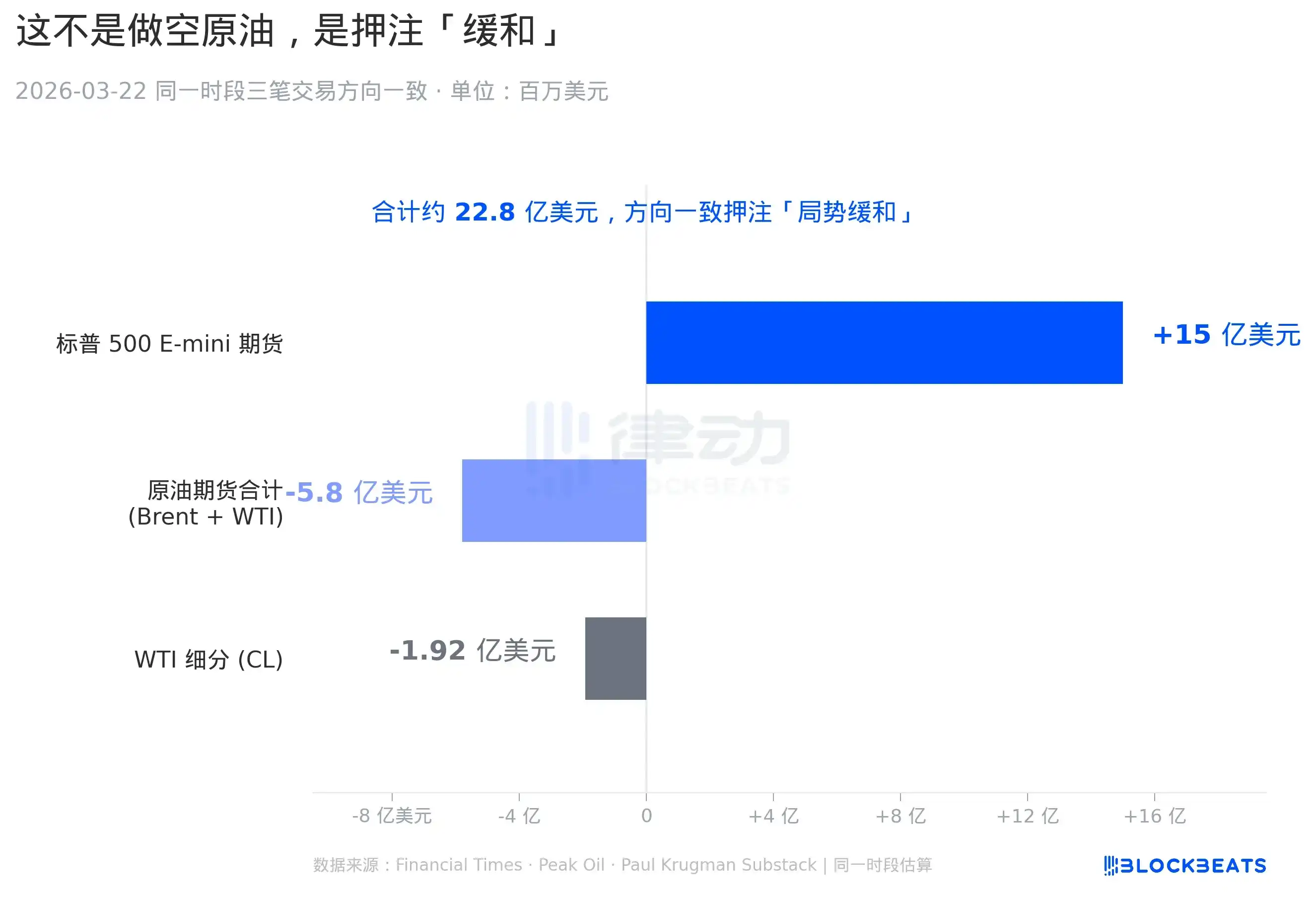

This chart shows the other half of the anomaly on March 22 that many reports overlooked. Follow-up articles by the Financial Times and Peak Oil in late March mentioned that, during the same period, besides the $580 million crude oil short, two other positions were established in the same direction: a purchase of approximately $1.5 billion in S&P 500 E-mini futures and a separate $192 million short position in WTI (CL contract).

"S&P 500 E-mini futures" are the most active U.S. stock index futures contract on the exchange, with one contract corresponding to about $250,000 of the S&P 500 index value, making it a standard tool for institutions to hedge the overall direction of U.S. stocks. "Buying E-mini" is equivalent to betting on a rise in U.S. stocks. The "WTI细分空单" (WTI细分空单) was an additional separate short position added on another futures product line (U.S.-traded WTI) for crude oil. Together, these three positions had a notional value of about $2.28 billion.

Looking at these three orders in isolation, they resemble a perfectly aligned pair trade (paired trade), betting on the same macro scenario: a de-escalation of U.S.-Iran tensions. How would de-escalation affect the market? Oil supply panic subsides, oil prices fall. Geopolitical risk premium disappears, stocks rebound. These three positions combined form the cleanest profit-making combination for this scenario. As Paul Krugman roughly put it, "If you knew you would see the words 'constructive dialogue' in two hours, these are the three trades you would place."

The Same Script, Also Appearing in Prediction Markets

Shifting perspective from the futures market to the crypto-world prediction market Polymarket reveals an almost identical mirror image.

Polymarket is a binary prediction contract platform built on Ethereum, where users bet on whether a specific event will occur. Odds are determined by market participants themselves, and winners split the pool after the event outcome is confirmed. All its transactions are on-chain, and anyone can view each wallet's history.

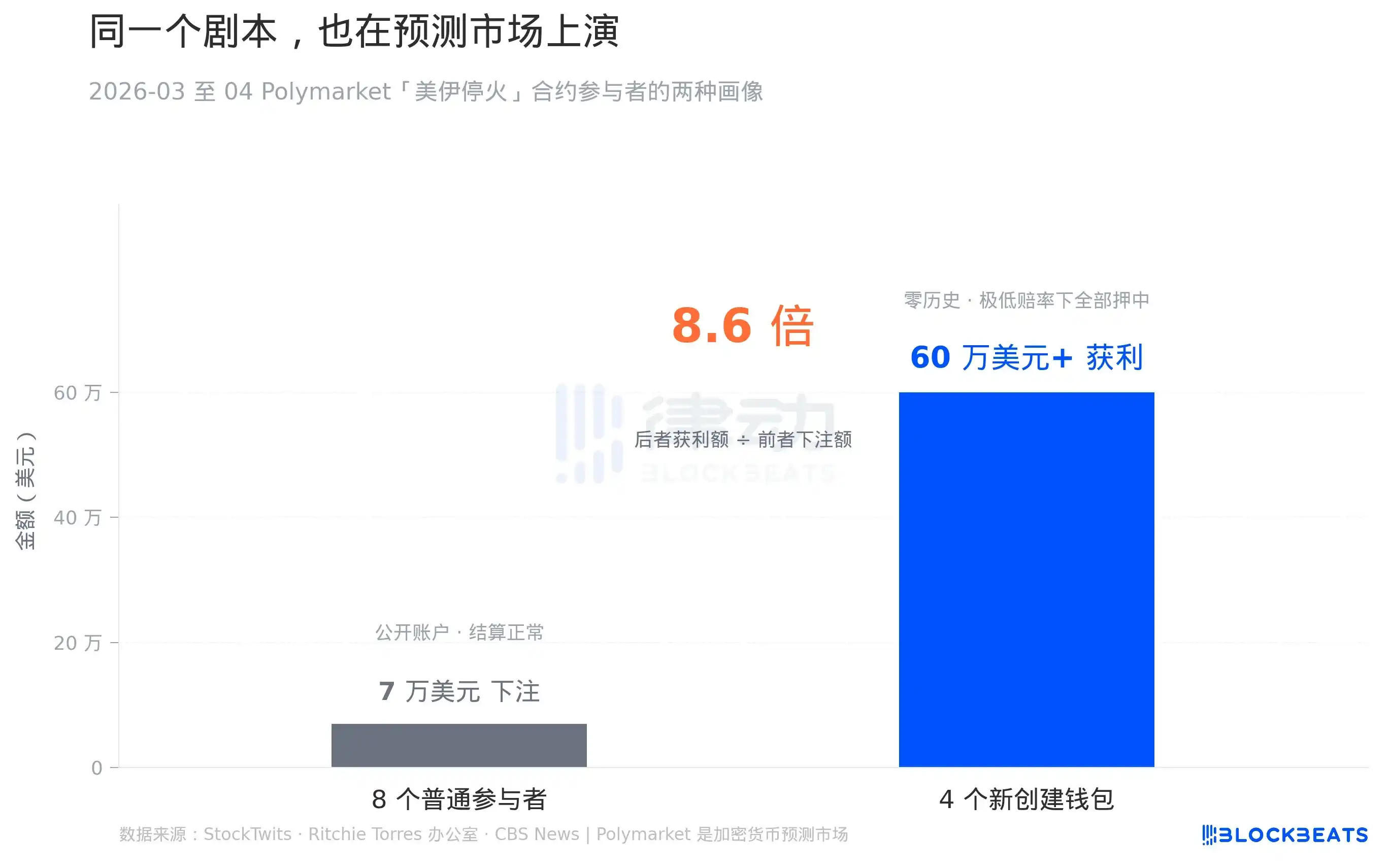

According to on-chain data cited by StockTwits, in the final week of the Polymarket contract "Will the U.S. and Iran ceasefire within 30 days?", 8 accounts fit a "normal profile." These were all public, established accounts, placing a total of about $70,000 in bets, with wins and losses, and the settlement process showed no suspicious activity. However, simultaneously, 4 other accounts had a completely different profile. These 4 wallets were newly created just before the event, with no prior on-chain transaction history. Their first action was to heavily bet on "ceasefire will happen" at extremely low odds. They all won, collectively profiting over $600,000.

$70,000 versus $600,000—a multiple of about 8.6 times. The latter's profit was almost nine times the total bet amount of the former. According to Polymarket's own settlement rules, the winner's amount = bet amount × (1/odds). To make $600,000 within a week, these 4 wallets must have either placed heavy bets at a time when the odds were extremely low (meaning the market thought "no ceasefire" was very likely) or placed multiple分散下注 (dispersed bets). On-chain data indicates it was the former.

Ritchie Torres's office mentioned this detail in their letter to the SEC and CFTC, listing it alongside the crude oil futures anomaly as evidence of "cross-market synchronous signals." This is also why Torres had already pushed for legislation草案 (draft legislation) targeting insider trading in prediction markets regarding Polymarket back in late March. For him, the crude oil futures side was not an isolated incident.

Will There Really Be an Investigation?

First, consider the reality at the federal level. According to the SEC's enforcement report for fiscal year 2025 released in early April, the SEC initiated 313 new cases in the past year, the lowest number in the past decade, down 27% from 583 cases in fiscal 2024. The CFTC did not release a report of the same level simultaneously, but law firms Sullivan & Cromwell and Skadden, which track CFTC enforcement trends, noted in comments released in early April that the CFTC's Division of Enforcement had noticeably slowed down in early 2025.

But just about a week before Torres wrote his letter, the CFTC had announced its top 5 enforcement priorities for 2026. According to Sullivan & Cromwell's梳理 (analysis), ranked first was "Insider Trading, including prediction markets," and second was "Market Manipulation, particularly in energy markets."

The微妙之处 (subtlety) here is that the CFTC itself has verbally placed this matter at the top of its list, but historically, the CFTC has极少 (very rarely) initiated cases based on "single anomalous trade" types in the futures market. Past successful energy commodity cases, such as the penalties against Trafigura, Freepoint, and TotalEnergies in 2024, were all long-term over-the-counter manipulation cases, lasting 2 to 4 years, not targeting a single anomalous short order on the screen.

What could truly bring this matter to a result is another avenue. According to reports from OilPrice.com and Peak Oil, New York State Attorney General Letitia James has been using New York State's Martin Act since April 2025 to track a series of "well-timed, high-return trades related to Trump's public statements."

The Martin Act is New York State's securities anti-fraud law. It has a key feature that federal law lacks: prosecutors do not need to prove the defendant had a subjective intent to defraud. They only need to prove that the trading activity itself has objectively fraudulent characteristics to file a lawsuit. For events like "precise lurking," subjective intent is precisely the hardest element to prove in federal insider trading cases.