过去一周,受FTX暴雷的影响,大量交易所遭遇挤兑危机,做市商为规避风险集体停摆,加之感恩节节前效应来袭,市场进入交投清淡的阶段。虽然加密借贷公司Genesis的破产危机在市场上引起轩然大波,但是投资者对利空的反应已经逐渐麻木,大饼仅下挫不到3%便开始探底回升。那么,跌无可跌是否意味着市场进入磨底阶段?

由于链上清算具有程序化和透明化两大特征,DeFi在去杠杆的过程中产生了惊人的破坏力,这导致市场一度陷入流动性危机。然而,灾难性的下跌也使DeFi去杠杆达到了釜底抽薪的效果。所以,在LUNA暴雷后,市场仅用了三周的时间就完成底部构筑,并开启强劲反弹。

与DeFi去杠杆不同,CeFi的杠杆主要集中信息披露极不透明的交易所。只有当流动性无法覆盖短期债务时,交易所的杠杆风险才会充分释放。而在CeFi去杠杆的过程中,交易所风险敞口的暴露需要用户反复地进行提款测试。所以,CeFi去杠杆的过程显得尤为缓慢,这也是行情的走势一直非常焦灼的缘故。

尽管FTX暴雷的外溢风险尚未完全消除,但零散的出险点对市场的影响已经逐渐减弱。从行业自律性的信息披露来看,占据市场份额70%以上的交易所仍旧保持着良好的经营态势,甚至还出资10亿美元用于支持陷入流动性危机的优秀项目。而随着Gate、Kucoin、CRYPTO等二三线交易所也在相继熬过挤兑期,市场恐慌情绪已经明显降温。

从过往的经验来看,当前市场已经出现明显的底部特征,主要理由有以下三点:

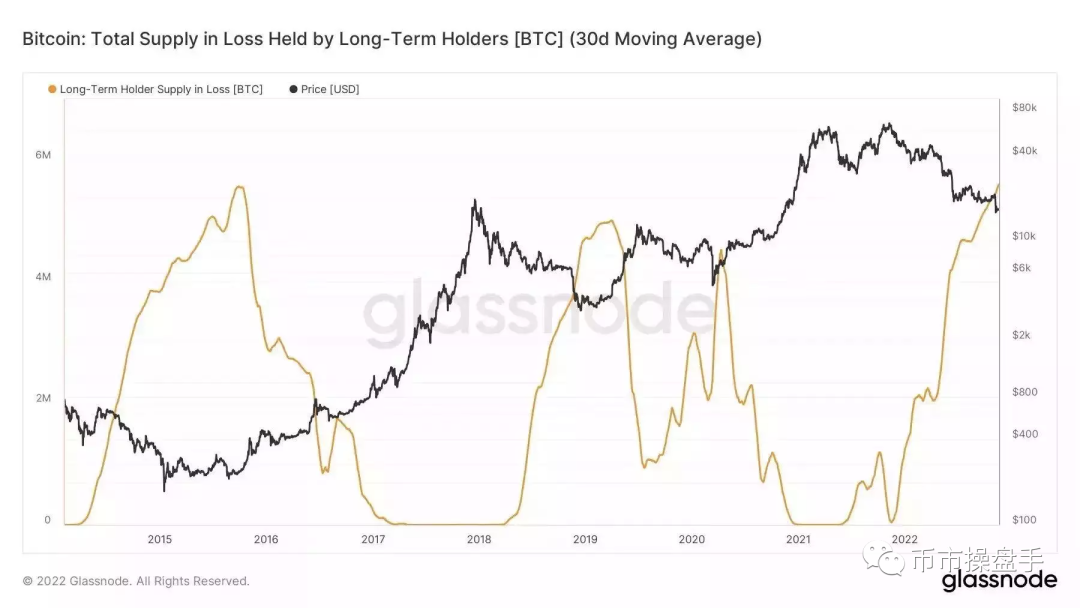

1、长期持有者大面积亏损。11月21日,Glassnode 数据显示,BTC 长期持有者亏损持仓量已突破 500 万枚 BTC,亏损情况已超过 2018 年熊市,与 2015 年熊市时长期持有者的亏损情况接近。

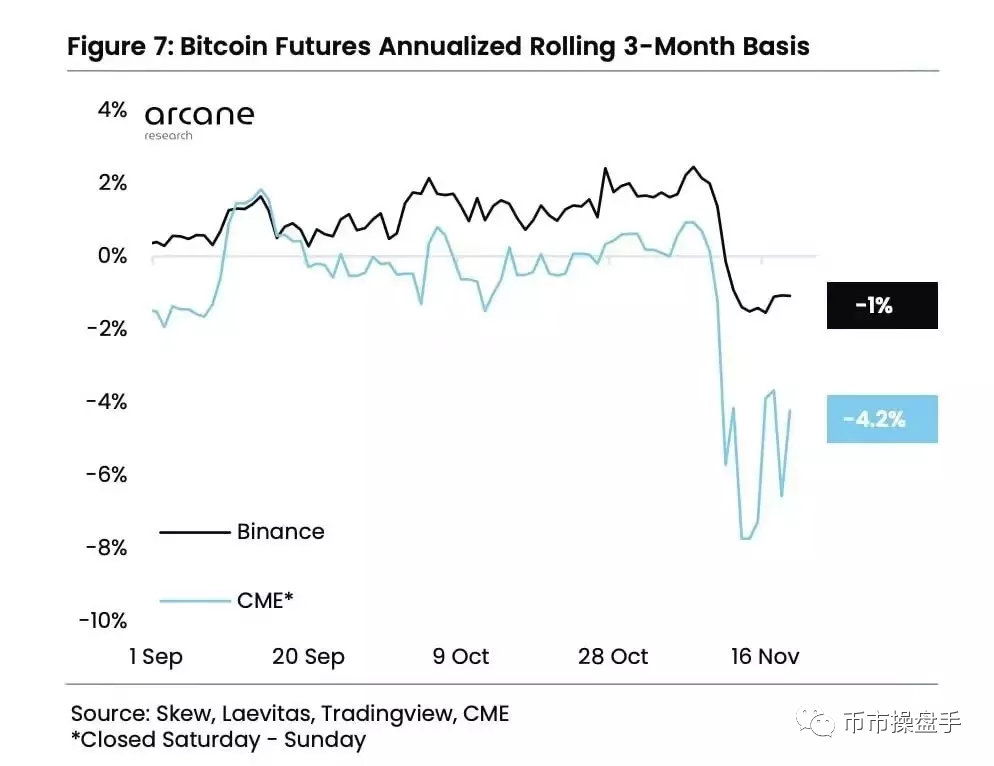

2、市场投资者对后市普遍悲观。公开数据显示,FTX暴雷后,币安和CME的比特币季度合约贴水率极速飙升。币安季度合约贴水率曾一度达到1.23%,刷新2020年5月份以来的最高记录。而CME的比特币贴水率更是达到惊人的4.2%。历史上,当卖空交易处于极度拥挤的状态时,轧空行情也就随之到来。

3、机构投资者恢复买入。Ark Invest Daily Trades数据显示,ARK基金10月份增持了2500万美元的Coinbase股票,这6月以来的首次增持,而在FTX暴雷后,方舟基金于11月8日-11月22日期间继续增持了5600万美元的Coinbase股票。同时,ARK基金还于11月14日、15日、21日连续买入灰度信托GBTC,使得GBTC的溢价率从-45%收窄至-39%。除此之外,方舟投资创始人木头姐在上周二的采访中继续重申了对比特币的看多立场。她认为,比特币将从FTX的崩中浴火重生,并变得比以往更加强大。

在Genesis暴雷后,市场传闻DCG将清算63万枚比特币以偿还债务,这把不明真相的群众吓得不轻。但实际上,稍有常识的人都知道,GBTC是一个受SEC监管,且每个季度都有严格审计的信托产品,信托管理人的DCG仅负责GBTC份额的发行,对GBTC锚定的实物比特币没有处置权。从公开数据来看,DCG过去一共回购价值8亿美元的GBTC(目前账面价值不到5亿美金),其中部分回购资金从旗下的借贷平台Genesis拆借。因为GBTC不支持赎回,DCG只能通过抛售GBTC偿债,这将使美股市场的GBTC流动性承压,但对现货比特币的影响十分有限。

宏观方面,美联储11月份的会议纪显示,美联储委员们一致认为通胀几乎没有缓解的迹象,有目的地转向限制性更强的货币政策符合风险管理的考量,将通胀降低到2%的水平仍是美联储的长期目标,鹰派立场依然没有动摇。但与9月份议息会议一致强鹰的态度不同,11月的议息会议开始出现鸽派的声音:大部分美联储委员认为,不久的将来放慢加息步伐是合适的。一部分委员甚至认为继续快速收紧货币将增加金融市场的不稳定性。同时,委员们还讨论了英国国债暴跌和养老金暴雷对美国金融市场的影响。结合美国财政部长耶伦近期提出回购美国国债的建议,美债流动性的恶化已经成为美联储重点警惕的风险点。总之,美联储12月加息50基点已经成为大概率事件,而美债流动性恶化未来很可能会成为美联储紧缩政策的制约因素。

在FTX暴雷后,USDT的溢价率近一个月来一直维持在1.5%以上,这也表明场外增量仍源源不断地流入市场。如果将投资的周期拉长,那么当下无疑是新一轮反弹的起点。