1. BTC turnover shows signs of shrinking

The BTC price obviously did not fall back after the drop in volatility, but continued to rebound in large quantities. Although there is little room for growth, it is indeed a rare bullish signal in the near future. In terms of pressure level, BTC rose by more than 20000 US dollars, which is just below the closing price of the previous 4-hour K-line decline. Before the closing of BTC on September 13, a decline of 7% appeared in the 4-hour chart, indicating that the pressure level was sold strongly. The short-term strength of BTC this time can be said to be a technical rebound in low price areas. Whether we can further expand the growth space depends on the confirmation of indicators.

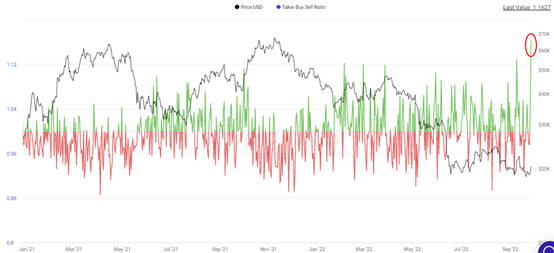

2. The position of BTC contract transaction rebounded

In contract trading, BTC investors' long and short currency holdings rebounded significantly. On September 27, the value reached around 1.162, a new high in more than a year. This shows that in the process of short-term price rise, the strength of bulls and shorts has changed significantly, and the influence of bulls on the market has increased rapidly.

In terms of position, BTC's total contract position rebounded to USD 9.26 billion on the 27th of the 9th page, an increase of USD 870 million compared with USD 8.39 billion the previous day. The position rebounded rapidly, and BTC entered an active trading state.

3. ETH horizontal arrangement

The K line chart of ETH day shows that the price has rebounded obviously, but it is still fluctuating in the neighborhood. The small change in trading volume means that the rebound strength of ETH brewing is not high. At present, the performance of the overall mainstream currency is consistent with that of ETH. Although it has experienced a full callback, the reversal intensity is weak, and further attention should be paid to the trend of bulls.

4. The number of ETH receiving addresses is abnormally low

The number of ETH out of the exchange rebounded, especially in the performance of the top ten transactions out of the exchange, which indicates that the main short-term protection has achieved good results. On September 27, the first 10 transactions out of the exchange reached 3297 ETHs, which means that the selling pressure has dropped and the strength of bulls is rising rapidly, which is synchronized with the rebound of 8% of the ETH price in 24 hours.

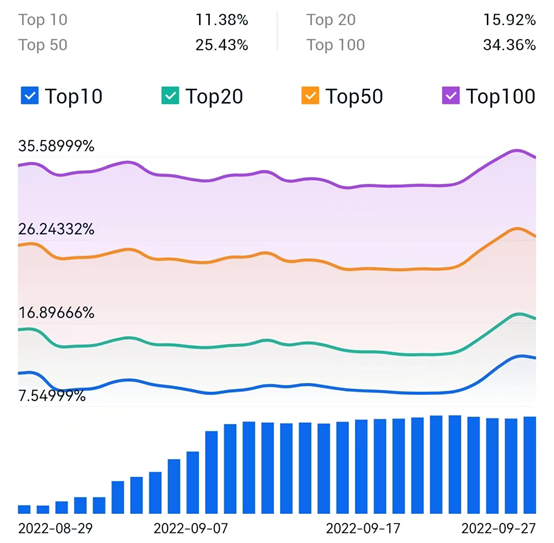

5. LUNC is strongly lifted

The 4-hour K-line chart shows that LUNC's short-term growth has reached 67%, and the synchronous volume shows that the main force is driving up LUNC's price. From the perspective of the volume and price performance after the increase, LUNC has significantly reduced its volume and collated sideways, which means that the energy of high selling is not high, forming a significant support for the price.

The number of coins held by the top 10, top 20, top 50 and top 100 also rebounded significantly, with the proportion rebounding to 11.38%, 15.92%, 25.43% and 34.36%. From the data on September 27, the growth rate reached 4, 4 and 3 percentage points respectively compared with that on September 21. Considering the short-term stability of LUNC's main currency, the price may remain strong.