In the current bear market, crypto options trading has been a rare bright spot, building momentum even as crypto prices have plunged.

A number of crypto exchanges have noted rising trading volume after reaching lows earlier this year. Options strategies have figured prominently among institutional investors and even miners as they try to weather crypto’s usual volatility and a downturn that could last for months, or longer, despite recent hopeful macroeconomic signs.

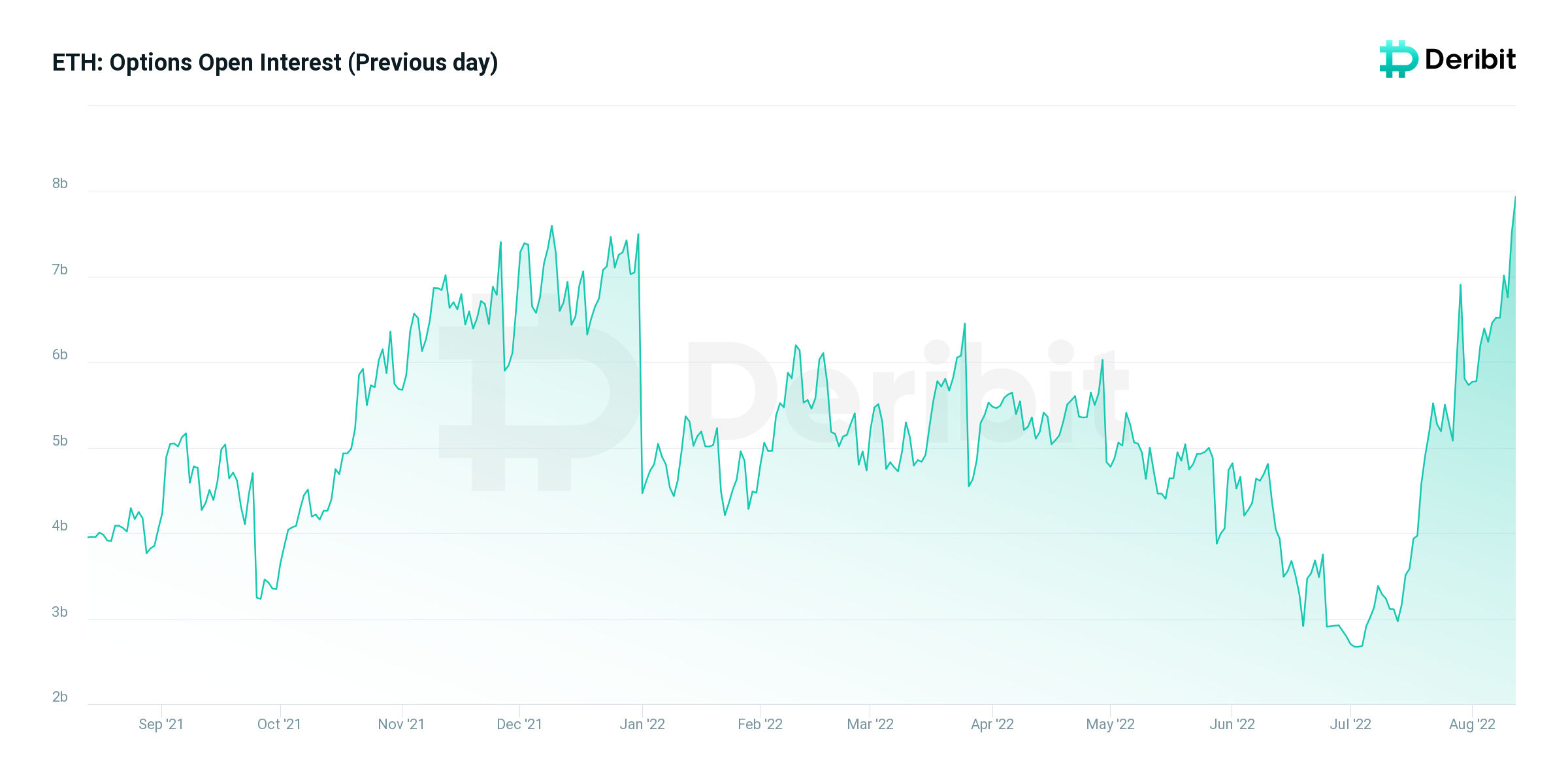

More recently, traders have been using the crypto options market to bet on ether (ETH) and hedge positions as the Ethereum blockchain’s hotly anticipated Merge approaches. Panama-based derivatives platform Deribit, which is among the world’s largest exchanges for crypto options trading volume, told CoinDesk demand is surging ahead of the Merge.

Earlier this week, in a disappointing second-quarter earnings report, crypto exchange giant Coinbase (COIN) even alluded to traders migrating to derivatives-focused platforms as a reason for declining trading volume. Coinbase’s dipping volume led to a 30% decline in the company’s revenues – below most analysts’ estimates.

“A larger amount of trading volume took place at offshore exchanges in Q2,” Coinbase said in its report, adding: “The sequential decline in Q2 institutional trading volume was primarily driven by lower market maker volume on our trading platform. These market participants gravitate towards products such as derivatives and financing products, which are areas we’re continuing to invest in but we don’t currently have product parity with offshore exchanges.”

A young market?

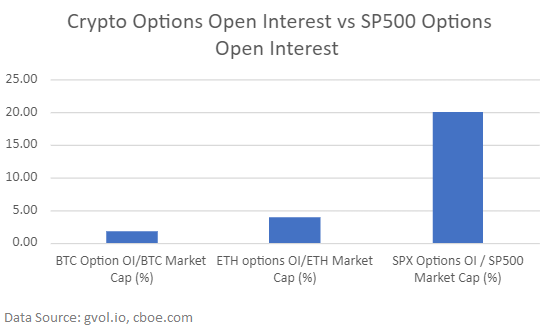

Bitcoin options trading accounts for only 2% of open derivatives contracts across exchanges trading the cryptocurrency, whose market cap is about $462 billion, according to structure product provider Enhanced Digital Group (EDG).

By comparison, traditional options trading of stocks accounts for 20% of the market cap of the S&P 500 at the Chicago Board Options Exchange (CBOE), EDG said. “When you think of all the other [S&P 500]-like products including [exchange-traded funds], SP Minis, etc., you can see that bitcoin options have multifold growth ahead of it,” EDG’s quant developer, Marcin Maksymiuk, told CoinDesk.

Sudden market shocks, technological improvements and a maturing futures market will all contribute to the growth of options, according to Delta Exchange CEO Pankaj Balani.

Delta generates over $200 million in options trading volume per day, and Balani said that “options provide a way for people to get engaged with the market even in a sideways environment.” He foresees options eventually accounting for 60% of the crypto trading market.

Peter Wisniewski, managing partner of crypto-focused alternative investment fund Europa Partners, told CoinDesk the firm expects “the market to continue to mature with greater price efficiency and liquidity.” Wisniewski said the markets will likely tie options to a widening range of digital assets.

“Currently, the only crypto derivatives markets with significant liquidity are priced to bitcoin and ether, but we expect to see a continual increase of derivative instruments priced to other types of digital assets, reducing volatility and driving more investment into the space,” Wisniewski added.

Miners

In recent months, cryptocurrency miners, who have been hit hard by bitcoin’s plunge, have used derivative strategies to hedge price exposure and limit their downside risk. Miner Argo Blockchain even hired an in-house derivatives trader in July to weather the market rout and determine hedging strategies going forward.

Crypto financial services firm Galaxy Digital, which has a division dedicated to lending and risk management for miners, avoided miner-related losses during the second quarter through the use of derivative strategies, according to CEO Michael Novogratz during the company’s earnings call this week.

Novogratz said that he expects to expand these offerings for miners and other clients.

How fast crypto options trading evolves remains uncertain, even as firms add exposure and pinpoint the products and services that can help them manage risk. EDG CEO Chris Bae noted that miner and institutional platforms’ use of derivative strategies remain in an early stage and that crypto options trading volumes "have yet to hit their j-curve when it comes to their adoption and growth.”

“We are seeing our partners use this sell off to hire option and derivative talent to staff for the opportunity,” Bae said.